Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

EXERCISES

Exercise 14-1 (15 minutes)

2. Journal entries

2015

(a)

Jan. 1 Cash..............................................................................3,400,000

(b)

June 30 Bond Interest Expense.................................................153,000

(c)

Dec. 31 Bond Interest Expense.................................................153,000

3.

2015

(a)

Jan. 1 Cash*.............................................................................3,332,000

(b)

Jan. 1 Cash*.............................................................................3,468,000

Exercise 14-2 (30 minutes)

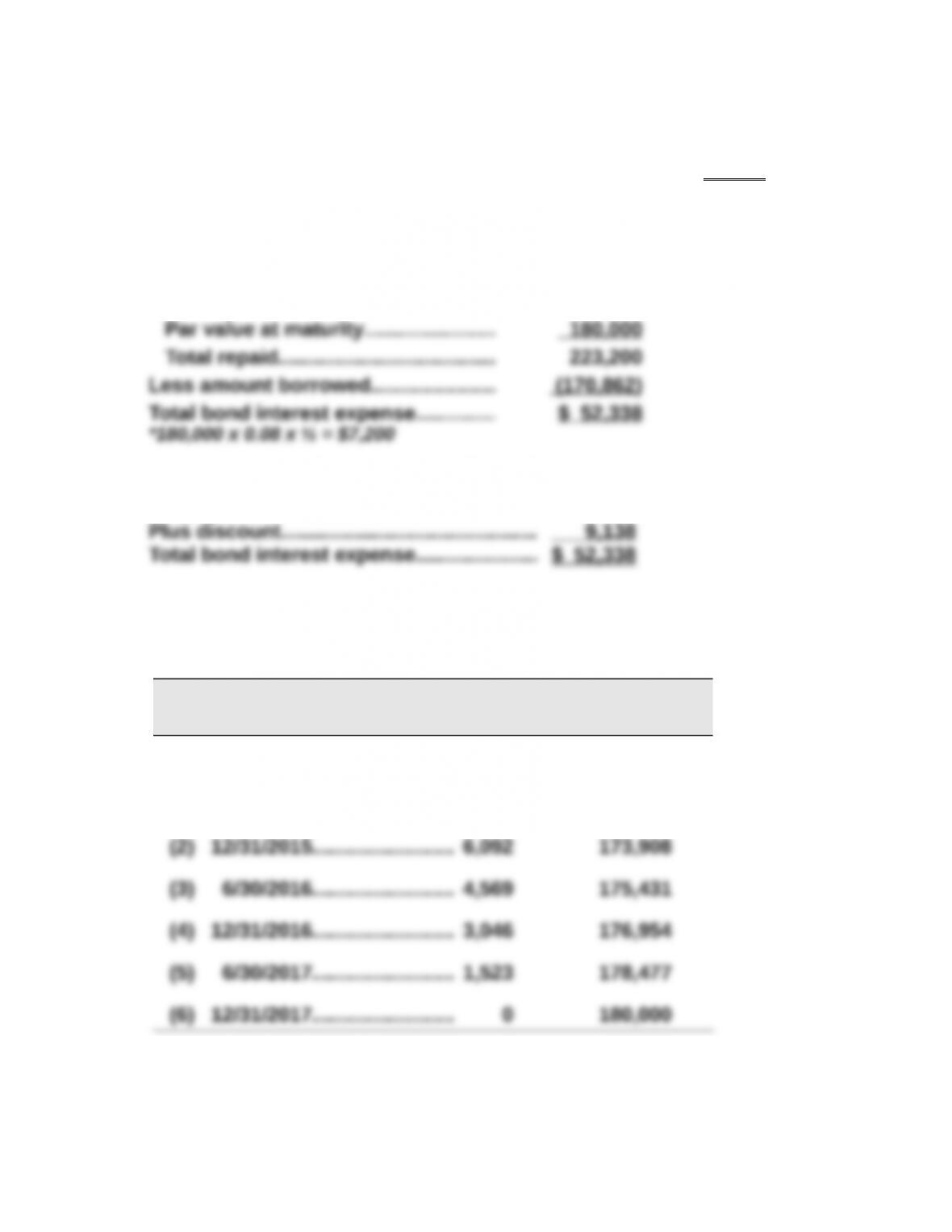

1. Discount = Par value - Issue price = $180,000 - $170,862 = $9,138

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $7,200*................. $ 43,200

or:

Six payments of $7,200............................. $ 43,200

3. Straight-line amortization table ($9,138/6 = $1,523)

Semiannual

Period-End

Unamortized

Discount

Carrying

Value

(0) 1/01/2015........................$9,138 $170,862

(1) 6/30/2015........................ 7,615 172,385

Exercise 14-3 (25 minutes)

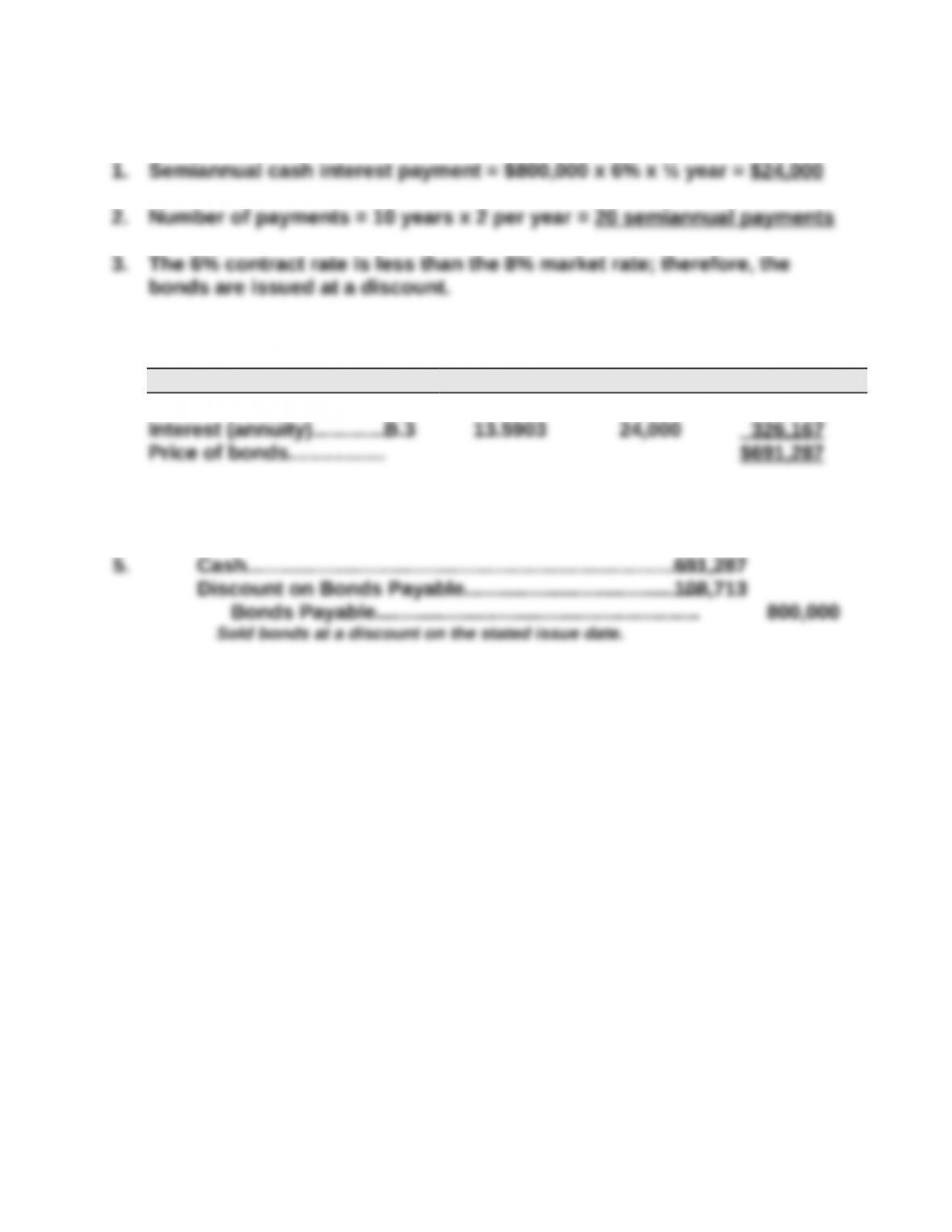

4. Estimation of the market price at the issue date

Cash Flow Table Table Value* Amount Present Value

Par (maturity) value........B.1 0.4564 $800,000 $365,120

* Table values are based on a discount rate of 4% (half the annual market rate) and

20 periods (semiannual payments).

Exercise 14-4 (20 minutes)

2015

(a)

Dec. 31 Cash..............................................................................186,534

2016

(b)

June 30 Bond Interest Expense.................................................7,684

(c)

Dec. 31 Bond Interest Expense.................................................7,684

Discount on Bonds Payable**................................ 1,684

Exercise 14-5 (35 minutes)

2015

(a)

Dec. 31 Cash..............................................................................188,000

(b)

2016

June 30 Bond Interest Expense.................................................8,000

Discount on Bonds Payable*................................. 3,000

Dec. 31 Bond Interest Expense.................................................8,000

Discount on Bonds Payable*................................. 3,000

2017

June 30 Bond Interest Expense.................................................8,000

Discount on Bonds Payable*................................. 3,000

Dec. 31 Bond Interest Expense.................................................8,000

Discount on Bonds Payable*................................. 3,000

½

(c)

Dec. 31 Bonds Payable..............................................................200,000

Exercise 14-6 (20 minutes)

2014

(a)

Dec. 31 Cash..............................................................................216,222

2015

(b)

June 30 Bond Interest Expense.................................................8,378

(c)

Dec. 31 Bond Interest Expense.........................................................8,378

Premium on Bonds Payable*...............................................1,622

Exercise 14-7 (30 minutes)

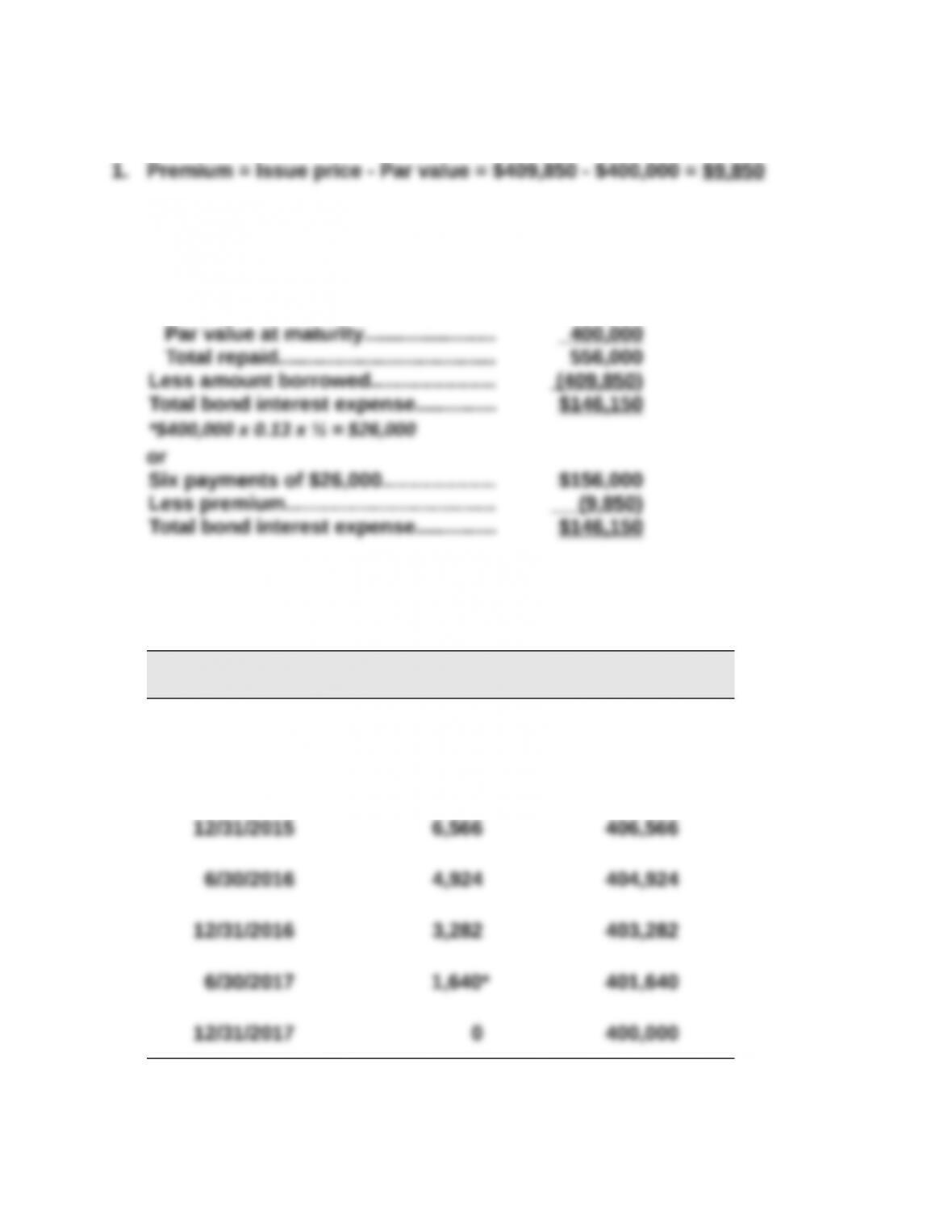

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000*............... $156,000

3. Straight-line amortization table ($9,850/6 = $1,642)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015 $9,850 $409,850

6/30/2015 8,208 408,208

*Adjusted for rounding.

Exercise 14-8 (25 minutes)

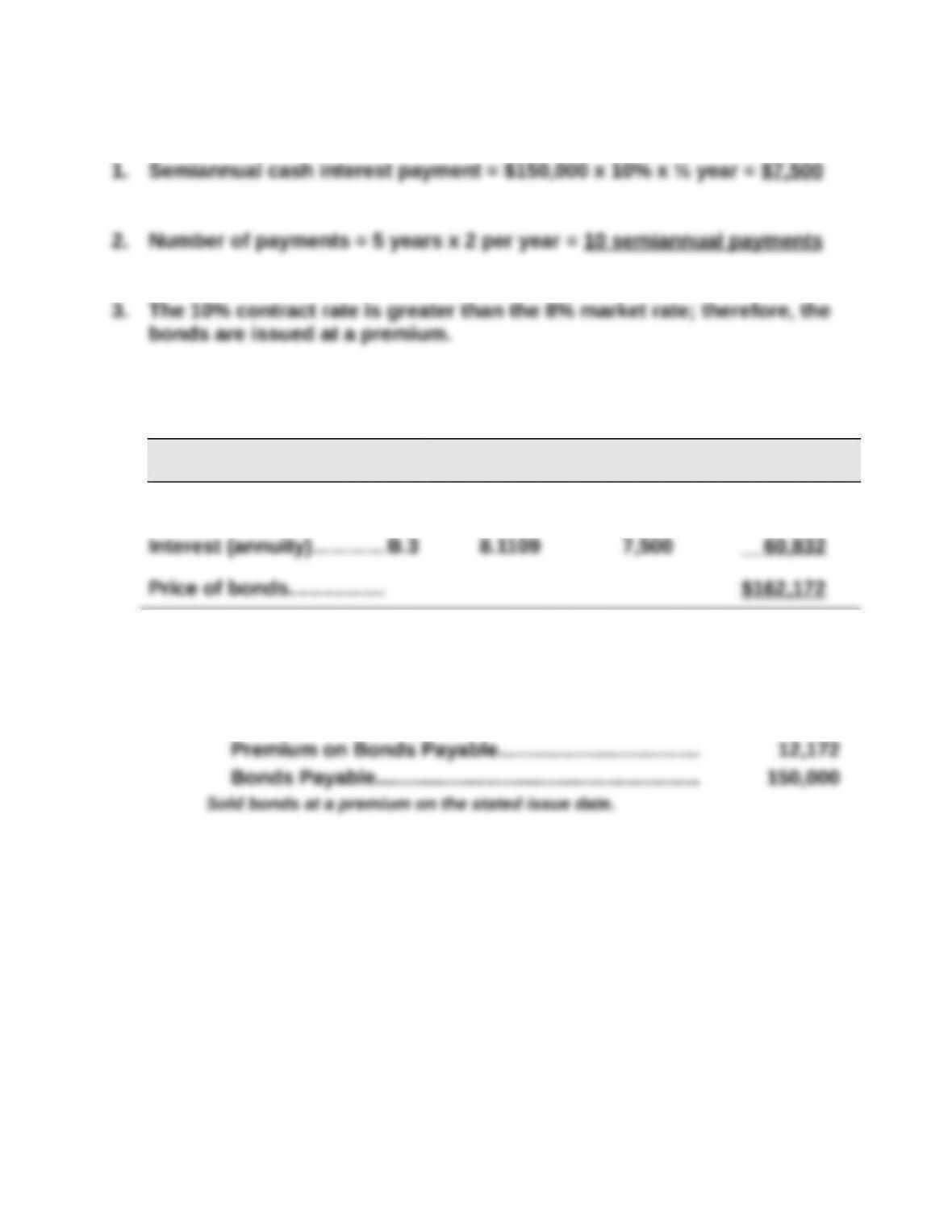

4. Estimation of the market price at the issue date

Cash Flow Table Table Value* Amount Present Value

Par (maturity) value........B.1 0.6756 $150,000 $101,340

* Table values are based on a discount rate of 4% (half the annual market rate) and

10 periods (semiannual payments).

5. Cash..............................................................................162,172

Exercise 14-9 (20 minutes)

1. Cash proceeds from sale of bonds at issuance

2. Discount at issuance

Par value............................................... $700,000

3. Total amortization for first 6 years

The first six years (from 1/1/15 to 12/31/20) equals 40% of the bonds’

15-year life. Therefore, the total amortization equals 40% of the total

discount (since straight-line amortization is being used), which is

4. Carrying value of the bonds at 12/31/2020

Discount at issuance (from part 2)......

$ 15,750

Entire Group

Retired 20%

Par value................................................

Remaining discount..............................

Carrying value.......................................

5. Cash purchase price

6. Loss on retirement

7. Journal entry at retirement for 20% of bonds

2021

Jan. 1 Bonds Payable..............................................................140,000

Exercise 14-10 (20 minutes)

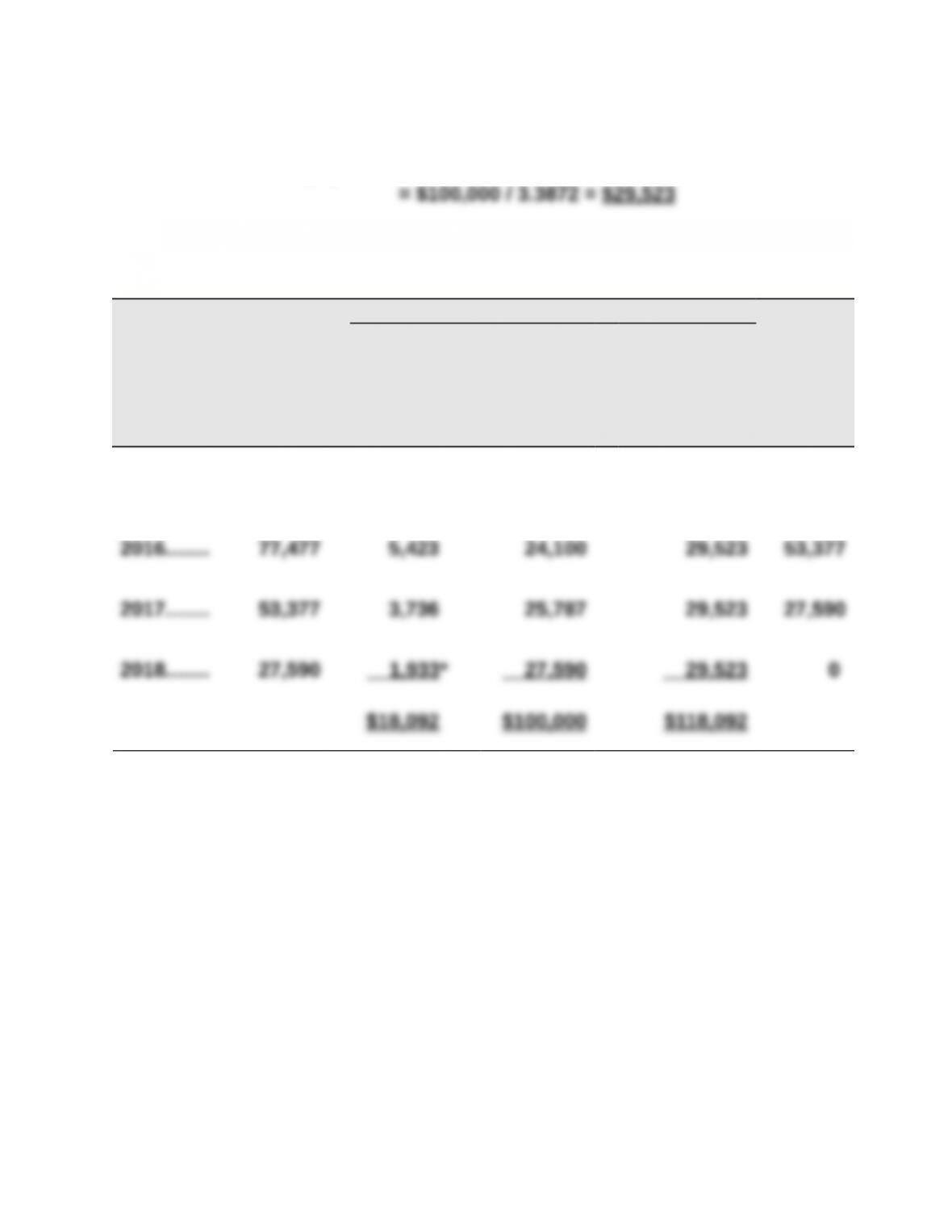

1. Amount of each payment = Initial note balance / Table B.3 value

2. Amortization table for the loan

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[7% x (A)]

+

(C)

Debit

Notes

Payable

[(D) - (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) - (C)]

2015....... $100,000 $ 7,000 $ 22,523 $ 29,523 $77,477

*Adjusted for rounding.