Chapter 13 – Accounting for Corporations

Exercise 13-16 (20 minutes)

1.

Total stockholders’ equity………………………………..…….. $1,585,000

Less equity applicable to preferred shares

Call price ($30 x 10,000)……………….……..……………..… $300,000

Cumulative dividends in arrears (none).…………........ 0 (300,000)

2.

Total stockholders’ equity………………………………..…….. $1,585,000

Less equity applicable to preferred shares

Call price ($30 x 10,000)……………….……..……………..… $300,000

Cumulative dividends in arrears (3 x 6% x $250,000)... 45,000 (345,000)

Exercise 13-17 (20 minutes)

1. Share capital Common stock

Retained profit Retained earnings

2. Cash………………………………………………………………… 624

3. 2013 Retained profit = 2012 Retained profit + 2013 Income – 2013 Dividends

€ 20,468 € 20,964 € 5,263 € 5,759

13-725

Chapter 13 – Accounting for Corporations

Exercise 13-18 (40 minutes)

Part 1

Jan. 2 Treasury Stock, Common………………………….……..…….75,000

Cash………………………………………………………………… 75,000

Purchased treasury stock (3,000 x $25).

July 9 Cash*………………………………………………..…..…………..….36,000

Treasury Stock, Common**…………………………..….. 30,000

Paid-In Capital, Treasury Stock***….…..…………..... 6,000

Reissued treasury stock.

*(1,200 x $30) **(1,200 x $25) ***(1,200 x $5)

Oct. 22 Common Dividend Payable……………………………..……..59,400

Cash………………………………………………………………… 59,400

Paid cash dividend.

Dec. 31 Income Summary………………………..………..…………..…..52,000

Retained Earnings…………………………………….……… 52,000

Closed Income Summary account.

13-726

Chapter 13 – Accounting for Corporations

Exercise 13-18 (Concluded)

Part 2

ALEXANDER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2016

Retained earnings, December 31, 2015………………….…… $340,000

Plus net income………………………………………………………... 52 ,000

Part 3

ALEXANDER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2016

Common stock$25 par value, 50,000 shares

authorized, 30,000 shares issued and outstanding;

300 shares in treasury…………………………..………..………. $ 750,000

Paid-in capital in excess of par value, common stock.... 50,000

13-727

Chapter 13 – Accounting for Corporations

PROBLEM SET A

Problem 13-1A (30 minutes)

Part 1

a. To record sale of 10,000 ($250,000/$25 per share) shares of $25 par

value common stock for $30 ($300,000/10,000 shares) per share.

d. To record sale of 3,000 ($75,000/$25 per share) shares of $25 par

value common stock for $40 ($120,000/3,000 shares) per share.

Part 2

Number of outstanding shares

Issued in (a)……………………………..….. 10,000

Issued in (b)…………………………….…… 5,000

Total…………………………………………..… 20,000

Part 3

Minimum legal capital = Outstanding shares x Par value per share

= 20,000 x $25 = $500,000

Part 4

Total paid-in capital from common stockholders

From transaction (a)……………………. $300,000

Part 5

Book value per common share

Total stockholders’ equity (given).... $695,000

13-728

Chapter 13 – Accounting for Corporations

Problem 13-2A (60 minutes)

Part 1

Jan. 1 Treasury Stock, Common………………………….……..…….80,000

Cash………………………………………………………………… 80,000

Purchased treasury stock (4,000 x $20).

July 6 Cash*………………………………………………..…..…………..….36,000

Treasury Stock, Common**……………………..……….. 30,000

Paid-In Capital, Treasury Stock***...…………..……... 6,000

Reissued treasury stock.

*(1,500 x $24) **(1,500 x $20) ***(1,500 x $4)

Oct. 28 Common Dividend Payable……………………………..……..80,000

Cash………………………………………………………………… 80,000

Paid cash dividend.

Dec. 31 Income Summary………………………..………..…………..…..388,000

Retained Earnings…………………………………….……… 388,000

Closed Income Summary account.

13-729

Chapter 13 – Accounting for Corporations

Problem 13-2A (Concluded)

Part 2

KOHLER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2016

Retained earnings, December 31, 2015………………….…… $270,000

Plus net income………………………………………………………... 388 ,000

658,000

Part 3

KOHLER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2016

Common stock$10 par value, 100,000 shares

authorized, 40,000 shares issued and outstanding...... $400,000

Paid-in capital in excess of par value, common stock... 60,000

13-730

Chapter 13 – Accounting for Corporations

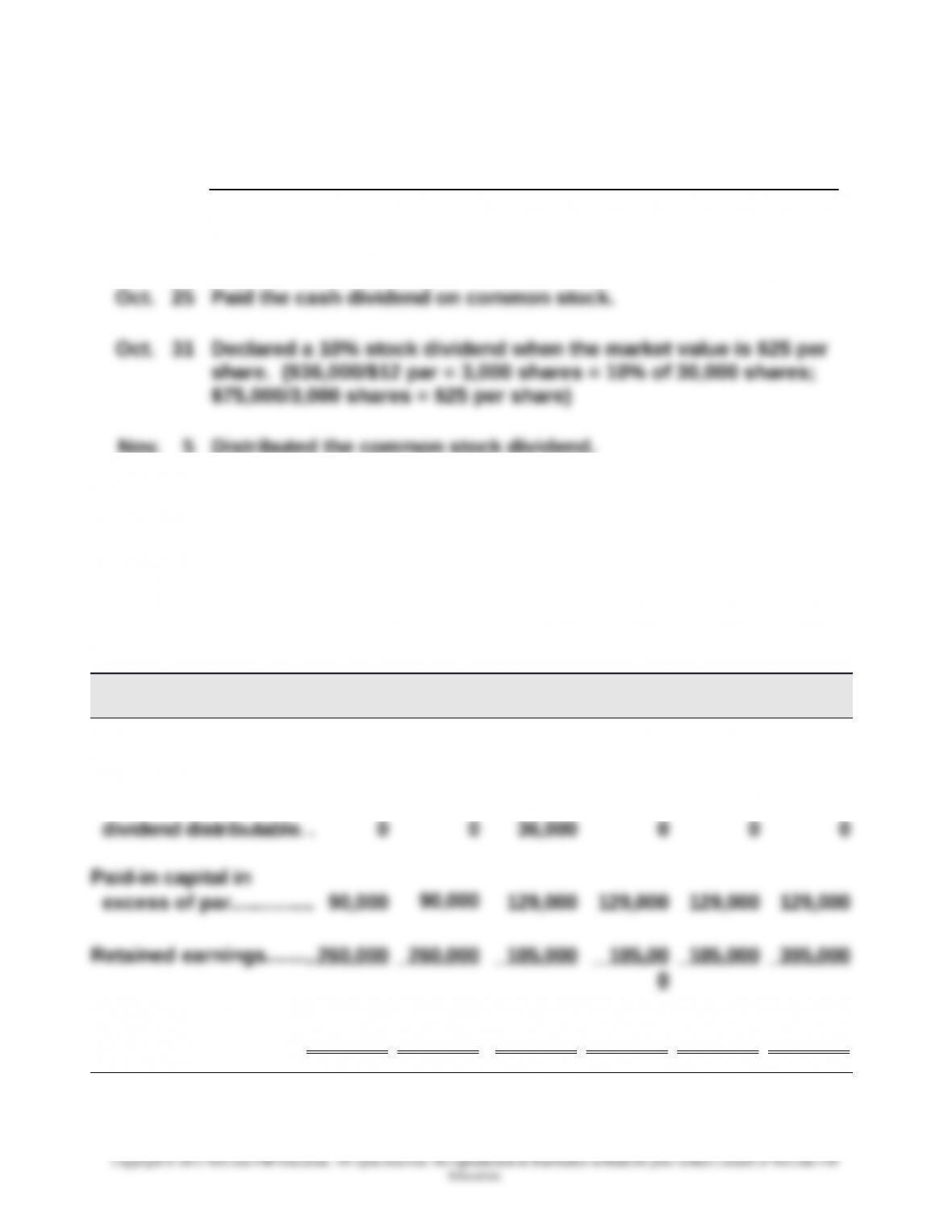

Problem 13-3A (45 minutes)

Part 1

Explanations for each of the journal entries

Oct. 2 Declared a cash dividend of $2 per share of common stock.

($60,000 / 30,000 shares)

Nov. 5 Distributed the common stock dividend.

Dec. 1 Executed a 3-for-1 stock split. ($12 par / $4 par = 3-for-1 ratio)

Dec. 31 Closed the Income Summary account to Retained Earnings.

Part 2

Oct. 2 Oct. 25 Oct. 31 Nov. 5 Dec. 1 Dec. 31

Common stock.............$360,000 $360,000 $360,000 $396,000 $396,000 $396,000

Common stock

0

Total equity………………..$710,000

$710,000

$710,000

$710,000

$710,000

$920,000

13-731

Chapter 13 – Accounting for Corporations

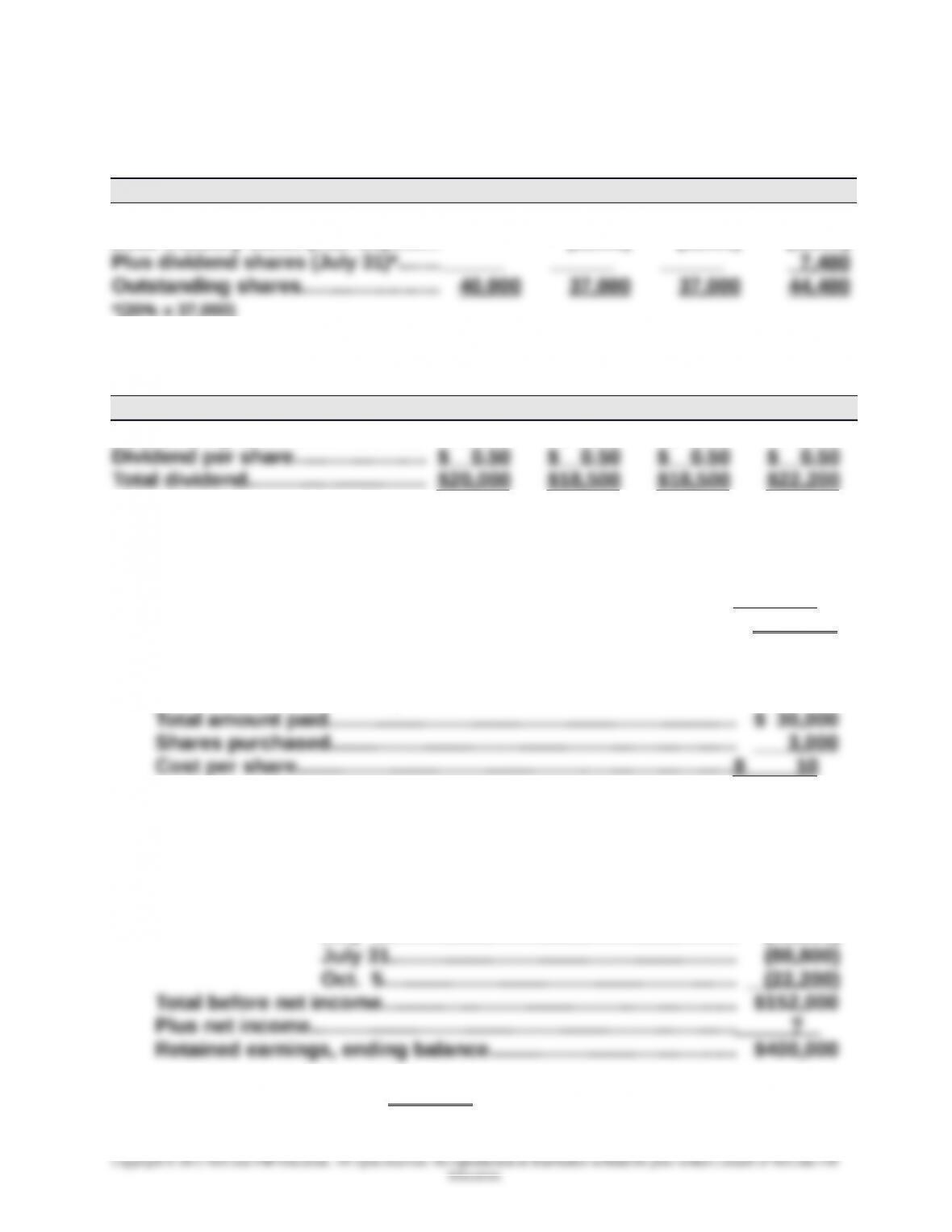

Problem 13-4A (45 minutes)

Part 1

Outstanding common shares

Jan. 5 Apr. 5 July 5 Oct. 5

Beginning balance…....…………..….. 40,000 40,000 40,000 40,000

Less treasury stock (Mar. 20)….….. (3,000) (3,000) (3,000)

Part 2

Cash dividend amounts

Jan. 5 Apr. 5 July 5 Oct. 5

Outstanding shares……………….... 40,000 37,000 37,000 44,400

Part 3

Capitalization of retained earnings for small stock dividend

Number of shares………………………………………………………...……. 7,400

Market value per share…………………………….………..…………….... $12

Total capitalized……………………………………………………………..….. $ 88 ,800

Part 4

Cost per share of treasury stock

Part 5

Net income

Retained earnings, beginning balance..…..……………..………….. $320,000

Less dividends: Jan. 5……………………………………………………... (20,000)

Apr. 5………………………………………………...…… (18,500)

July 5……………………………………………………... (18,500)

Therefore, net income = $248,000

13-732

Chapter 13 – Accounting for Corporations

Problem 13-5A (40 minutes)

1. Market price = $85 per share (current stock exchange price given)

3. Book values with no dividends in arrears

Book value per preferred share = par value (when not callable) = $50

Common stock

Total equity…………………....…………..……… $280,000

4. Book values with two years’ dividends in arrears

Preferred stock

Preferred stock par value…..……………....... $ 50,000

Plus two years’ dividends in arrears*........ 5,000

Preferred equity………………………………..….. $ 55,000

*2 years’ dividends = 2 x ($50,000 x 5%) = $5,000

Number of outstanding shares.................. 1,000

Book value per preferred share................. $ 55.00 ($55,000 / 1,000 shares)

13-733