Exercise 13-13 (30 minutes)

1. Net income…………………………………………………………………………$960,000

Exercise 13-14 (15 minutes)

Stock

Market Value

per Share

Divided

by

Earnings

per Share

Price-Earnings

Ratio

1…………. $176.40 $12.00 = 14.7

Analysis: Stocks with PE ratios less than about 5 to 8 are likely viewed as

potentially undervalued by the market. Of the stocks above, an analyst

might investigate stock #4 as possibly undervalued with a PE ratio of 5.0.

Exercise 13-15 (15 minutes)

Dividend yield

1. $16.06 / $220.00 = 7.3%

Analysis: The yield of 1.2% on stock #4 is sufficiently low that it

Exercise 13-16 (20 minutes)

1.

Total stockholders’ equity……………………………………… $1,585,000

Less equity applicable to preferred shares

Call price ($30 x 10,000)………………………………………. $300,000

2.

Total stockholders’ equity……………………………………… $1,585,000

Less equity applicable to preferred shares

Call price ($30 x 10,000)………………………………………. $300,000

Exercise 13-17 (20 minutes)

1. Share capital Common stock

2. Cash………………………………………………………………. 624

3. 2013 Retained profit = 2012 Retained profit + 2013 Income – 2013 Dividends

Exercise 13-18 (40 minutes)

Part 1

Jan. 2 Treasury Stock, Common………………………………………75,000

Cash………………………………………………………………. 75,000

Purchased treasury stock (3,000 x $25).

Jan. 7 Retained Earnings………………………………………………..40,500

Feb. 28 Common Dividend Payable……………………………………40,500

July 9 Cash*…………………………………………………………………..36,000

Treasury Stock, Common**……………………………… 30,000

Aug. 27 Cash*…………………………………………………………………..30,000

Paid-In Capital, Treasury Stock………………………………6,000

Sept. 9 Retained Earnings………………………………………………..59,400

Oct. 22 Common Dividend Payable……………………………………59,400

Dec. 31 Income Summary………………………………………………….52,000

Exercise 13-18 (Concluded)

Part 2

ALEXANDER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2016

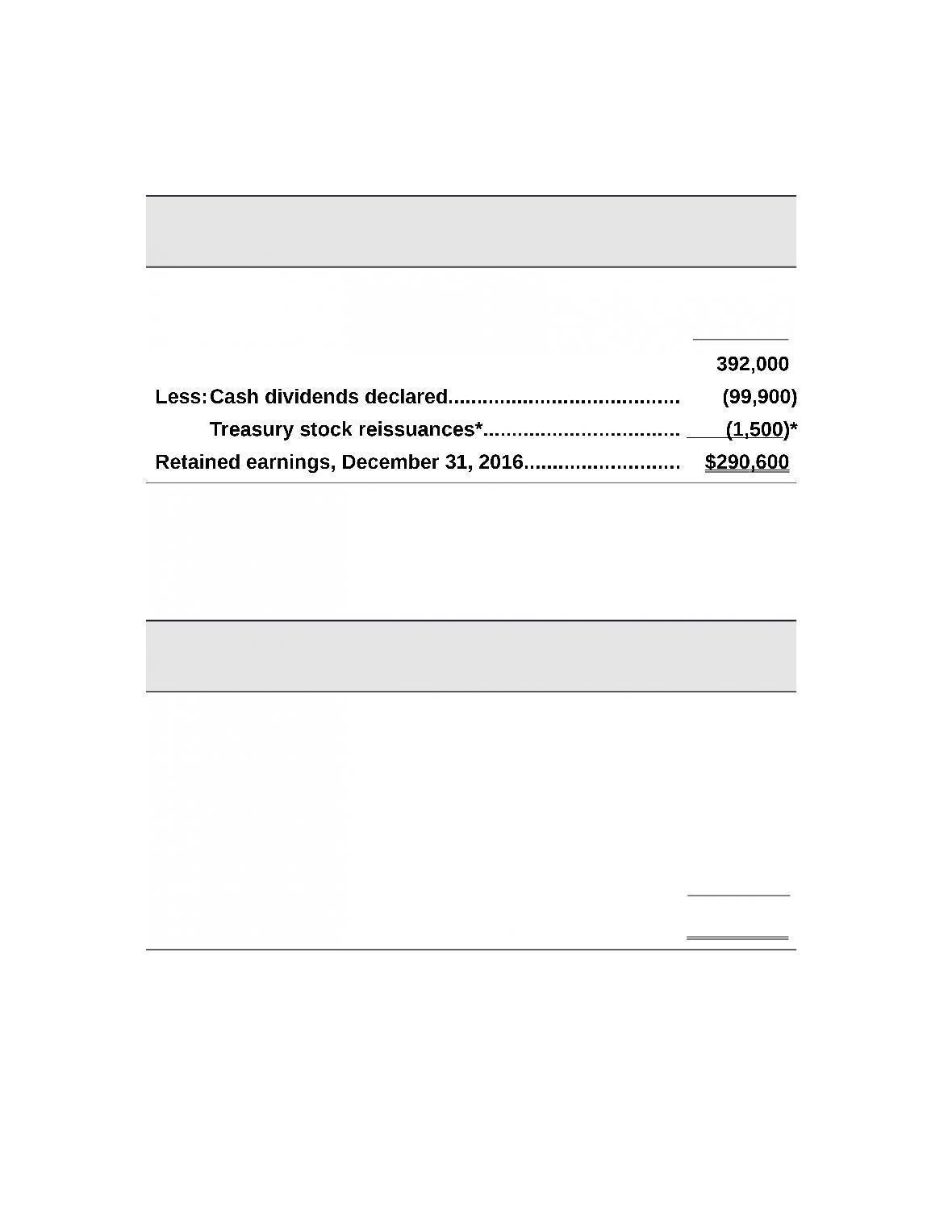

Retained earnings, December 31, 2015……………………… $340,000

Plus net income………………………………………………………. 52 ,000

*From August 27 transaction of reissuance of treasury shares.

Part 3

ALEXANDER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2016

Common stock$25 par value, 50,000 shares

authorized, 30,000 shares issued and outstanding;

300 shares in treasury……………………………………………. $ 750,000

PROBLEM SET A

Problem 13-1A (30 minutes)

Part 1

b. To record issuance of 5,000 ($125,000/$25 per share) shares of $25

c. To record acquisition of assets and liabilities by issuing 2,000

Part 2

Number of outstanding shares

Issued in (a)………………………………… 10,000

Part 3

Minimum legal capital = Outstanding shares x Par value per share

Part 4

Total paid-in capital from common stockholders

From transaction (a)…………………… $300,000

Part 5

Book value per common share

Problem 13-2A (60 minutes)

Part 1

Jan. 1 Treasury Stock, Common………………………………………80,000

Jan. 5 Retained Earnings………………………………………………..72,000

Feb. 28 Common Dividend Payable……………………………………72,000

July 6 Cash*…………………………………………………………………..36,000

Treasury Stock, Common**……………………………… 30,000

Aug. 22 Cash*…………………………………………………………………..42,500

Sept. 5 Retained Earnings………………………………………………..80,000

Oct. 28 Common Dividend Payable……………………………………80,000

Dec. 31 Income Summary………………………………………………….388,000

Problem 13-2A (Concluded)

Part 2

KOHLER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2016

Retained earnings, December 31, 2015……………………… $270,000

Plus net income………………………………………………………. 388 ,000

Part 3

KOHLER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2016

Common stock$10 par value, 100,000 shares

authorized, 40,000 shares issued and outstanding…… $400,000

Problem 13-3A (45 minutes)

Part 1

Explanations for each of the journal entries

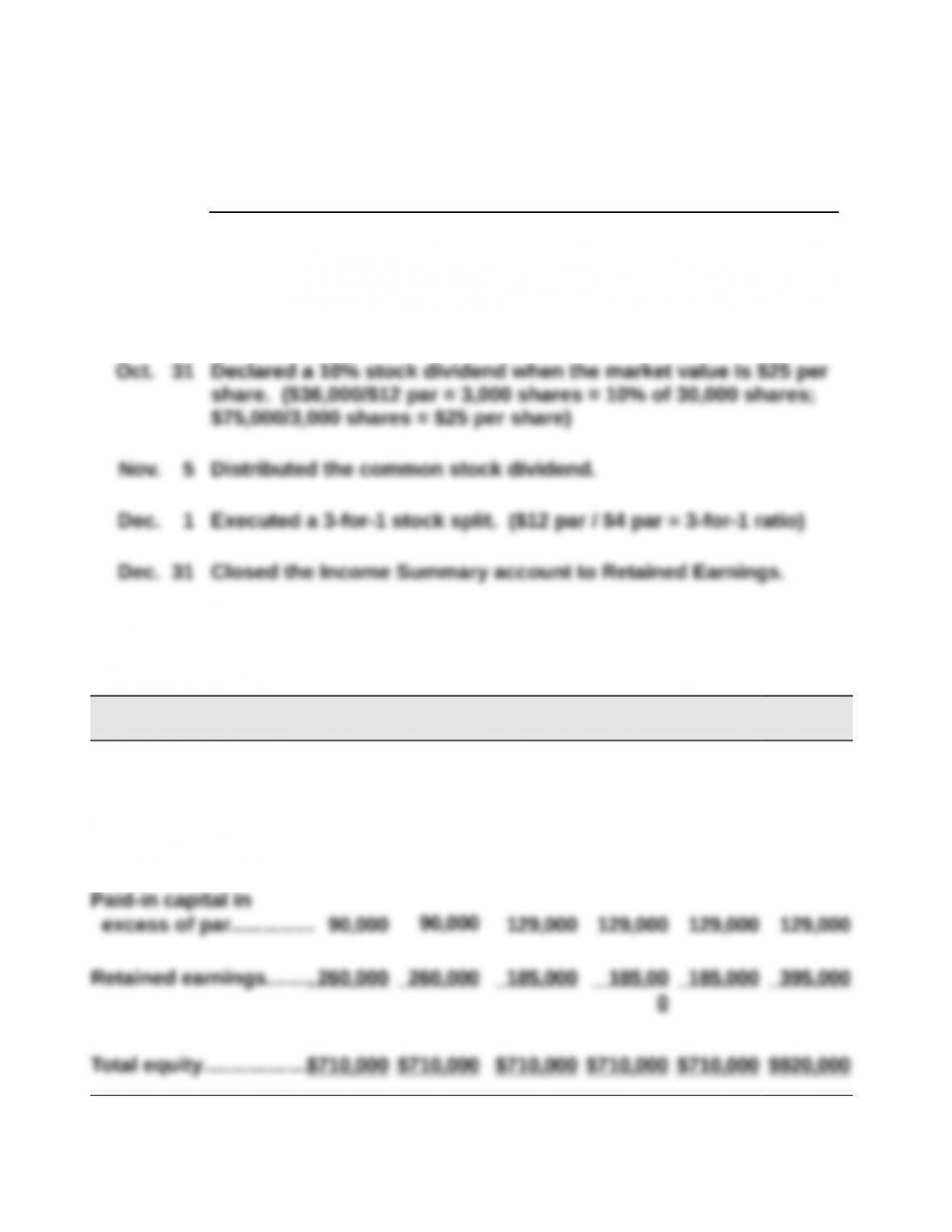

Oct. 2 Declared a cash dividend of $2 per share of common stock.

($60,000 / 30,000 shares)

Oct. 25 Paid the cash dividend on common stock.

Part 2

Oct. 2 Oct. 25 Oct. 31 Nov. 5 Dec. 1 Dec. 31

Common stock………….$360,000 $360,000 $360,000 $396,000 $396,000 $396,000

Common stock

dividend distributable. . 0 0 36,000 0 0 0

0

Part 2

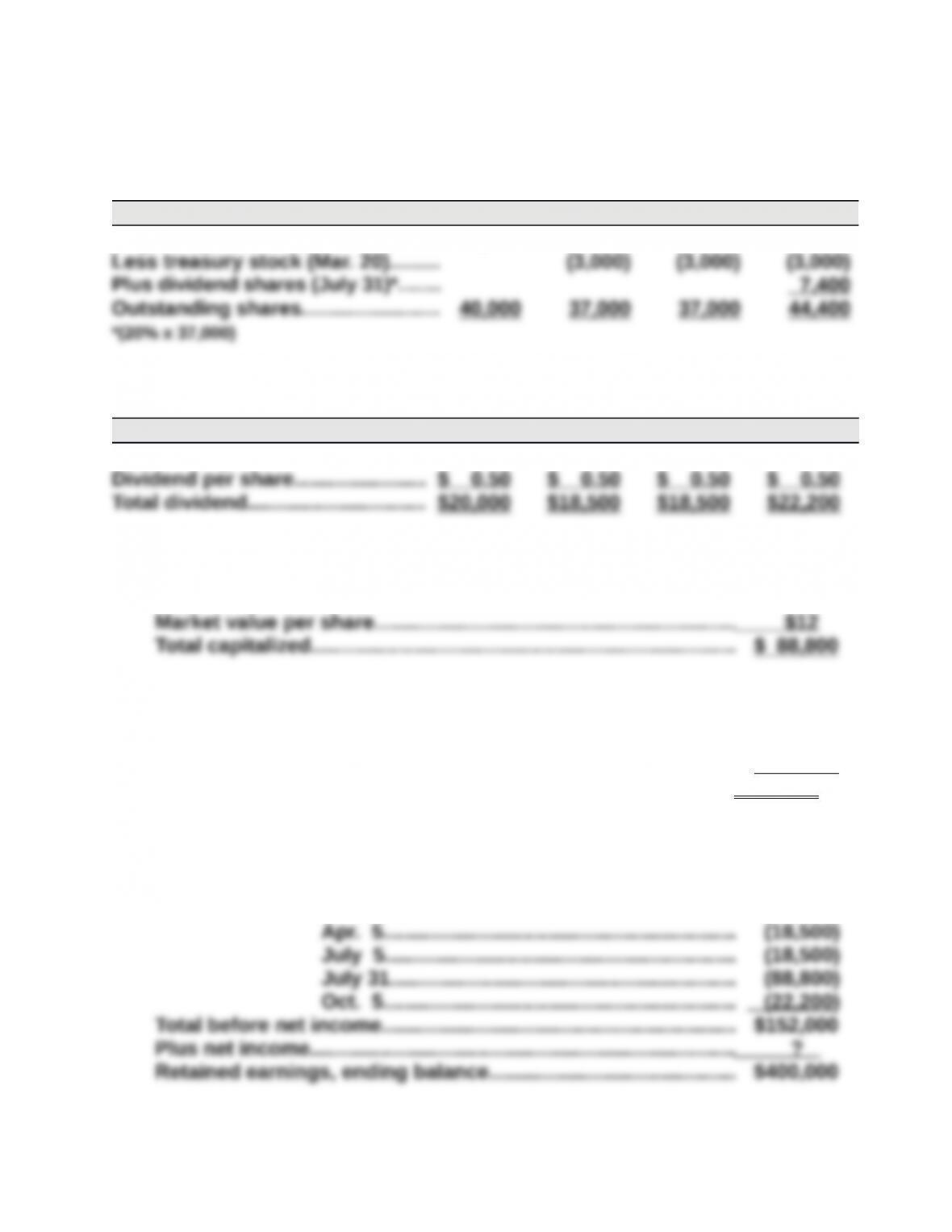

Cash dividend amounts

Jan. 5 Apr. 5 July 5 Oct. 5

Outstanding shares………………… 40,000 37,000 37,000 44,400

Part 3

Capitalization of retained earnings for small stock dividend

Number of shares…………………………………………………………….. 7,400

Part 4

Cost per share of treasury stock

Total amount paid…………………………………………………………….. $ 30,000

Shares purchased……………………………………………………………. 3 ,000

Cost per share………………………………………………………………….$ 10

Part 5

Net income

Retained earnings, beginning balance………………………………. $320,000

Less dividends: Jan. 5……………………………………………………. (20,000)