Chapter 13 – Accounting for Corporations

Exercise 13-3 (15 minutes)

1. Cash……………………………………………………………..………... 35,000

Common Stock, $5 Par Value*…………………………….. 20,000

2. Organization Expenses……………………………………….…… 40,000

Common Stock, $1 Stated Value…………………………. 2,000

Issued stock to promoters.

3. Organization Expenses……………………………………….…… 40,000

Common Stock, No-Par Value………………..…….…….. 40,000

Issued stock to promoters.

4. Cash………………………………………………………….……………..60,000

Preferred Stock, $50 Par Value*.……….…………….…… 50,000

Exercise 13-4 (15 minutes)

Land…………………………………………………………………….… 45,000

Building………………………………………….….…………….……. 85,000

13-725

Chapter 13 – Accounting for Corporations

Exercise 13-5 (20 minutes)

1.

a. Retained earnings

Before dividend……………………………………………….…………….. $ 660,000

$10 par value of 25,000 dividend shares.……….……………..... (250,000)

After dividend………………………………………………….….…………. $ 410,000

b. Total stockholders’ equity

Common stock$10 par value, 120,000 shares

2.

a. Retained earnings (no change)

Before and after stock split…………………………………………….. $ 660,000

b. Total stockholders’ equity

Common stock$6.67 (rounded) par value, 180,000 shares

authorized, 75,000 shares issued and outstanding………….. $ 500,000

3. From a stockholder’s point of view, there is no practical difference

between the stock dividend and the stock split. The number of

shares will be increased equivalently under either approach, and the

market value change, if any, should be approximately the same.

13-726

Chapter 13 – Accounting for Corporations

Exercise 13-6 (25 minutes)

1.

Feb. 5 Retained Earnings*……………………..……….…………….….480,000

Common Stock Dividend Distributable**..……….… 120,000

Paid-In Capital in Excess of Par Value,

2.

Before After

Total stockholders’ equity……….….……….. $1,575,000 $1,575,000

Issued and distributable shares..……....... 60,000 72,000

* 800 shares x 120% = 960 shares.

3.

February 5 February 28

Market value per share…………….………….. $ 40 $ 33.40

Note: The total market value of investor’s holdings is approximately the same

Exercise 13-7 (10 minutes)

13-727

Chapter 13 – Accounting for Corporations

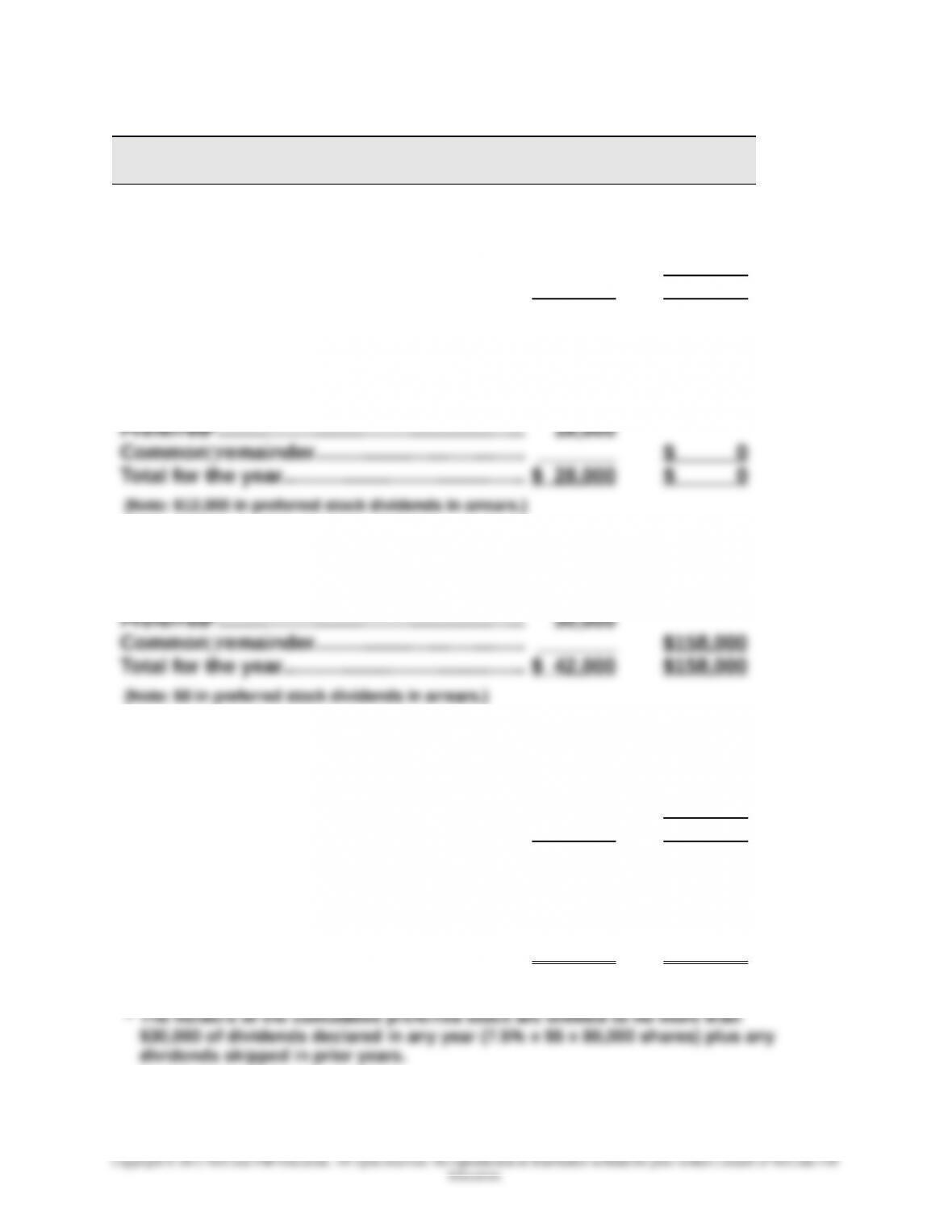

Exercise 13-8 (30 minutes)

Non-Cumulative

Preferred Common

2015 ($20,000 paid)

2016 ($28,000 paid)

2017 ($200,000 paid)

Preferred*………………………………………………. $ 30,000

Commonremainder………………….….……….. _______ $170,000

Total for the year………………………………..….. $ 30,000 $170,000

2018 ($350,000 paid)

2015-2018 ($598,000 paid) _______ _______

Total for four years……………….….………….… $108,000 $490,000

* The holders of the noncumulative preferred stock are entitled to no more than

$30,000 of dividends in any one year (7.5% x $5 x 80,000 shares).

13-728

Chapter 13 – Accounting for Corporations

Exercise 13-9 (25 minutes)

Cumulative

Preferred Common

2015 ($20,000 paid)

Preferred*………………………………………………. $ 20,000

Commonremainder………………….….……….. _______ $ 0

Total for the year………………………………..….. $ 20,000 $ 0

(Note: $10,000 in preferred stock dividends in arrears.)

2016 ($28,000 paid)

Preferredarrears from 2015……………….….. $ 10,000

2017 ($200,000 paid)

Preferredarrears from 2016……………….….. $ 12,000

2018 ($350,000 paid)

Preferred*………………………………………………. $ 30,000

Commonremainder………………….….……….. _______ $320,000

Total for the year………………………………..….. $ 30,000 $320,000

(Note: $0 in preferred stock dividends in arrears.)

2015-2018 ($598,000 paid)

_______ _______

Total for four years……………….….………….… $120,000 $478,000

13-729

Chapter 13 – Accounting for Corporations

Exercise 13-10 (25 minutes)

1. (a)

Oct. 11 Treasury Stock (5,000 x $25)………………..…………….…..125,000

Cash………………………………………………………………… 125,000

Purchased treasury stock.

(b)

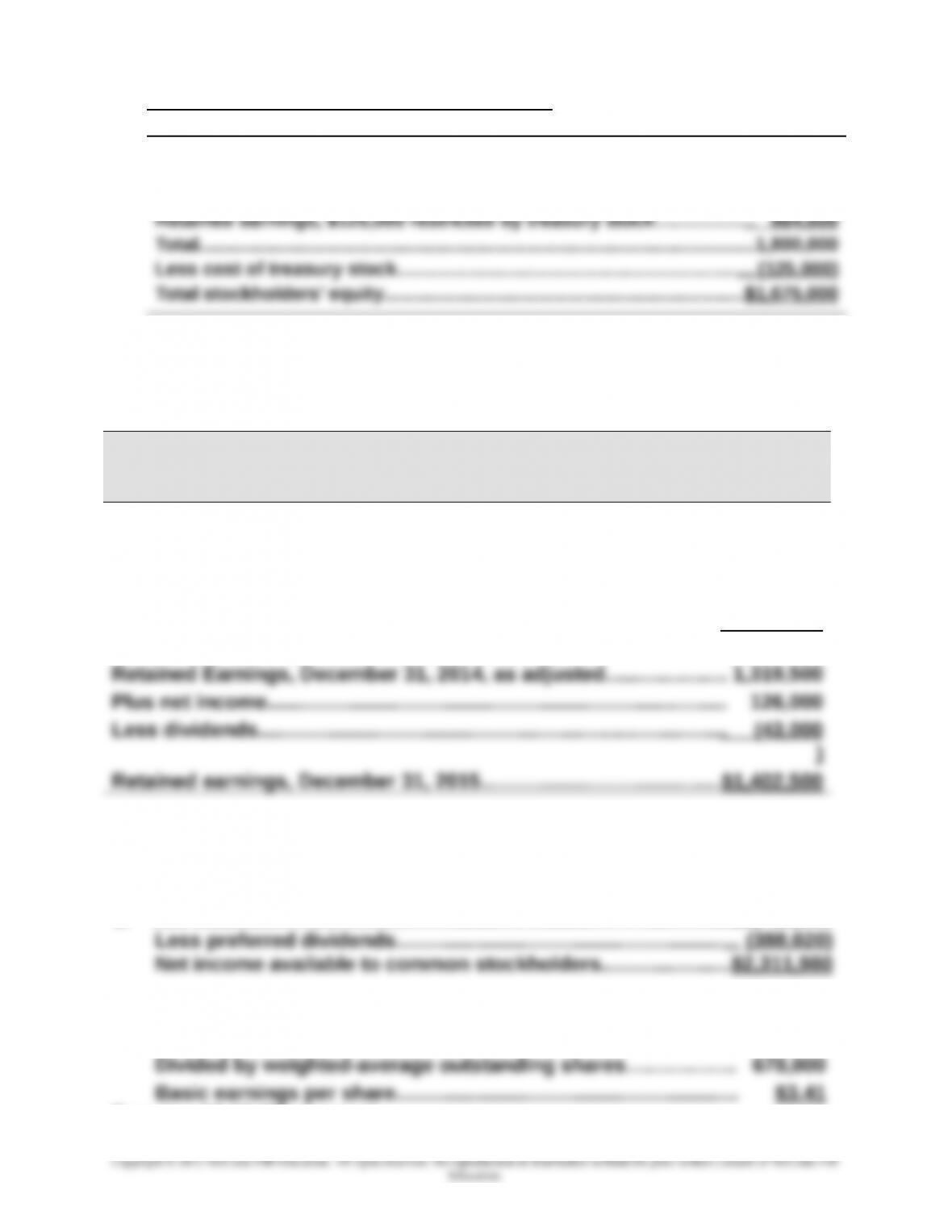

2. Changes to the equity section include the following

(i) The common stock account description line will change. After the

treasury stock purchase, it should read:

(iii) The retained earnings dollar balance will not change but its

description should change to read:

Retained earnings ($125,000 restricted for treasury stock).............$864,000

(v) Total stockholders’ equity will change from $1,800,000 to $1,675,000.

Exercise 13-10 (Concluded)

13-730

Chapter 13 – Accounting for Corporations

Revised equity section appears as follows

Common stock$10 par value; 72,000 shares authorized

and issued; 5,000 shares in treasury……………..………………..…..…..….

$ 720,000

Paid-in capital in excess of par value, Common stock………………..….. 216,000

Exercise 13-11 (15 minutes)

Amos Company

Statement of Retained Earnings

For Year Ended December 31, 2015

Retained earnings, December 31, 2014, as previously

reported…………………………………………………………………………………………………………………..……

$1,375,000

Prior period adjustment

Depreciation expense not recorded in 2013 (net of $4,500

in

tax benefits)………………………………………………..….…………….…..

($55,500

)

Exercise 13-12 (25 minutes)

1. Net income…………………………………………………………..….………….$2,700,000

2. Net income available to common stockholders……………………$2,311,980

Exercise 13-13 (30 minutes)

13-731

1. Net income……………………………………………………….…………….……$960,000

2. Net income available to common stockholders….…………….. $840,000

Exercise 13-14 (15 minutes)

Stock

Market Value

per Share

Divided

by

Earnings

per Share

Price-Earnings

Ratio

1…………. $176.40 $12.00 = 14.7

2…………. 96.00 10.00 = 9.6

Exercise 13-15 (15 minutes)

Dividend yield

1. $16.06 / $220.00 = 7.3%

Analysis: The yield of 1.2% on stock #4 is sufficiently low that it

13-732