Chapter 12 – Accounting for Partnerships

Comparative Analysis — BTN 12-2

1. Apple was organized/founded in 1976, and Google was

2. Apple’s initial public offering occurred in 1980. Google’s initial public

offering occurred in 2004.

12-681

Chapter 12 – Accounting for Partnerships

Ethics Challenge — BTN 12-3

1. Income allocation per original agreement

Mobey Oak Chesterfield Total

Salary allowance…........... $ 3,000 $ 3,000 $ 3,000 $ 9,000

2. Income allocation per Chesterfield’s proposal

Mobey Oak Chesterfield Total

(.10 x 50,000)

(.30 x 50,000)

(.60 x 50,000)

3. The ethical concern here is that Chesterfield has proposed a change to

the partnership agreement that appears to be only self-serving. It is true

that Chesterfield is the group’s largest producer and, therefore, is

A potentially fair compromise would be to study the referral patterns of

Mobey and Oak. Through analysis, a dollar value can be assigned to the

12-682

Chapter 12 – Accounting for Partnerships

Communicating in Practice — BTN 12-4

— STUDY NOTES –—

ORGANIZATIONS WITH PARTNERSHIP CHARACTERISTICS

I. Limited Partnerships

II. Limited Liability Partnerships

III. S Corporations

IV. Limited Liability Companies

I. Limited Partnerships

These organizations are identified in its name with the words “Limited

Partnership,” or “Ltd.,” or “L.P.”

A limited partnership has two classes of partners, general and limited. At

partners have no active role except as specified in the partnership

agreement.

A limited partnership agreement often specifies unique procedures for

allocating incomes and losses between general and limited partners.

The same basic accounting procedures are used for both limited and

from malpractice or negligence claims resulting from the acts of another

partner. When a partner provides service resulting in a malpractice claim,

that partner has personal liability for the claim. The remaining partners

who were not responsible for the actions resulting in the claim are not

personally liable for it.

12-683

Chapter 12 – Accounting for Partnerships

Communicating in Practice (Concluded)

Continued

III. S Corporations

Certain corporations with 100 or fewer stockholders can elect to be

treated like a partnership for income tax purposes. These corporations are

called Sub-Chapter S or simply “S” corporations. This distinguishes them

from other corporations, called Sub-Chapter C or simply “C” corporations.

“S” corporations provide stockholders with the same limited liability

feature as “C” corporations. The advantage to an “S” corporation is it

doesn’t pay income taxes. If stockholders work for an “S” corporation,

their salaries are treated as expenses of the corporation.

IV. Limited Liability Companies

A new form of business organization is the limited liability company. The

names of these businesses usually include the words “Limited Liability

Company” or an abbreviation such as “LLC” or “LC.”

This form of business has certain features like a corporation and others

A limited liability company usually has a limited life.

For income tax purposes, the IRS usually classifies a limited liability

company as a partnership.

12-684

Chapter 12 – Accounting for Partnerships

Taking It to the Net — BTN 12-5

1. The account titles given in the equity section of Advanced BioEnergy,

LLC are:

2. There are 25,410,852 units and 24,714,180 units issued and outstanding

at September 30, 2013 and 2012, respectively.

12-685

Chapter 12 – Accounting for Partnerships

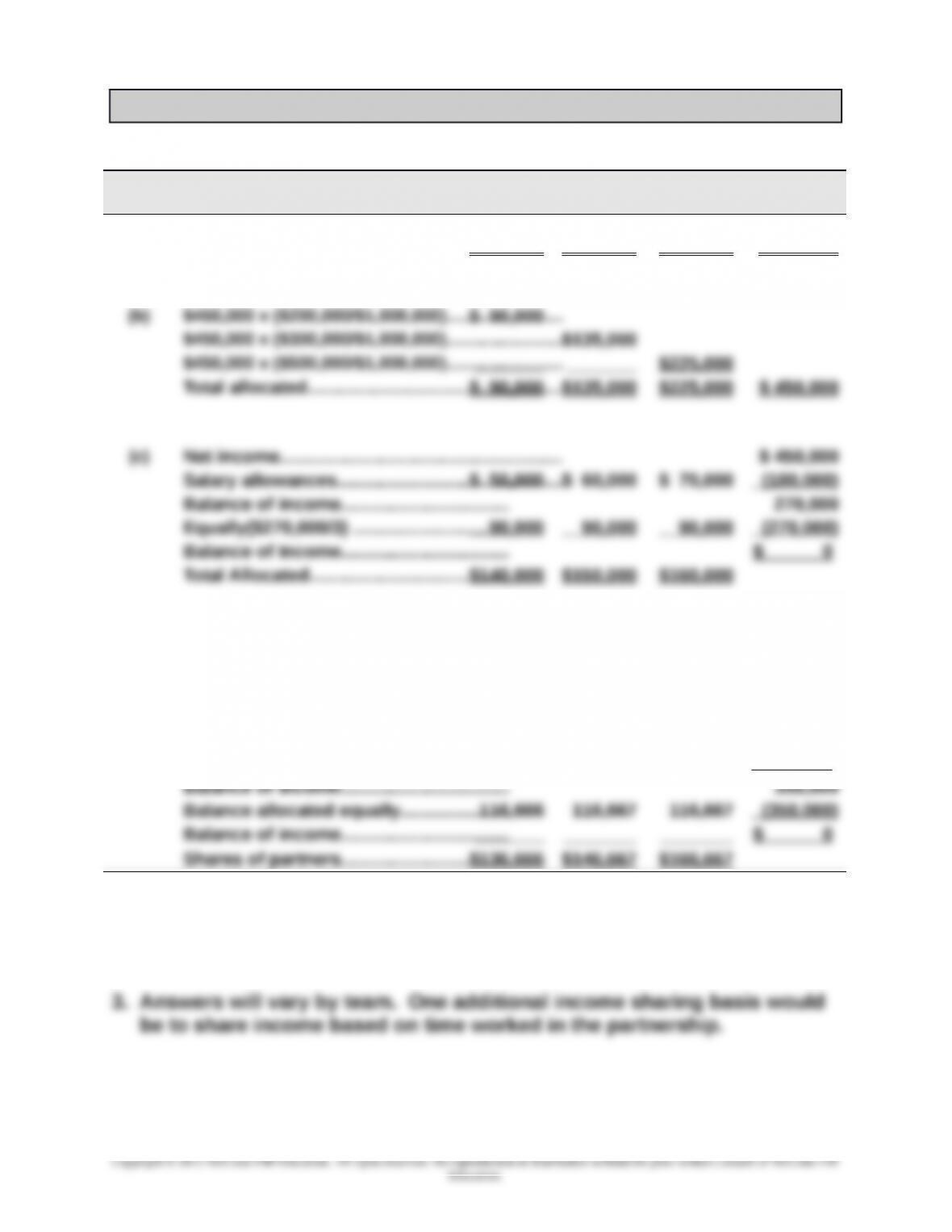

Teamwork in Action — BTN 12-6

1.

Income (Loss)

Sharing Plan Calculations Baker Warner Rice Total

(a) $450,000/3……………………………………..…..…..….$150,000 $150,000 $150,000 $ 450 ,000

(d) Net Income…………………………….…..….... $ 450,000

Interest allowances:

10% x $200,000………………..…..…..…...$ 20,000

10% x $300,000………………..…..…..…... $ 30,000

10% x $500,000………………..…..…..…... $ 50,000

Total interest…………………………..…..…... (100 ,000)

2. Team members share solutions.

12-686

Chapter 12 – Accounting for Partnerships

Entrepreneurial Decision — BTN 12-7

1. Daniel, Craig, and their future partners would be wise to construct an

agreement that includes the following:

a) names (reputations) and contributions

2. The partnership form of business organization will have several

advantages for Daniel, Craig, and their partners. Three of these

3. Several disadvantages exist with the partnership form of organization.

Three of these include: (a) The greatest disadvantage is that each

Global Decision — BTN 12-8

1. Byung-Chull Lee (also referred to as Lee Byung-Chull)

organized/started the company in 1938 in Taegu, Korea.

12-687

Chapter 12 – Accounting for Partnerships

2. In the beginning, the company focused primarily on trade export,

selling dried Korean fish, vegetables, and fruit to Manchuria and

3. Samsung groups its affiliated companies into five areas:

Electronics

12-688