Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 12 - Accounting for Partnerships

Problem 12-3B (30 minutes)

Part 1

Income (Loss)

Sharing Plan Calculations Cook Xi Schwartz Total

(a) $240,000/3....................................................$80,000 $ 80,000 $ 80,000 $240 ,000

(c) Net income.................................................. $240,000

Salary allowances.......................................$40,000 $ 30,000 $ 80,000 (150 ,000)

Balance of income...................................... 90,000

Interest allowances

12-681

Chapter 12 - Accounting for Partnerships

Problem 12-3B (Concluded)

Part 2

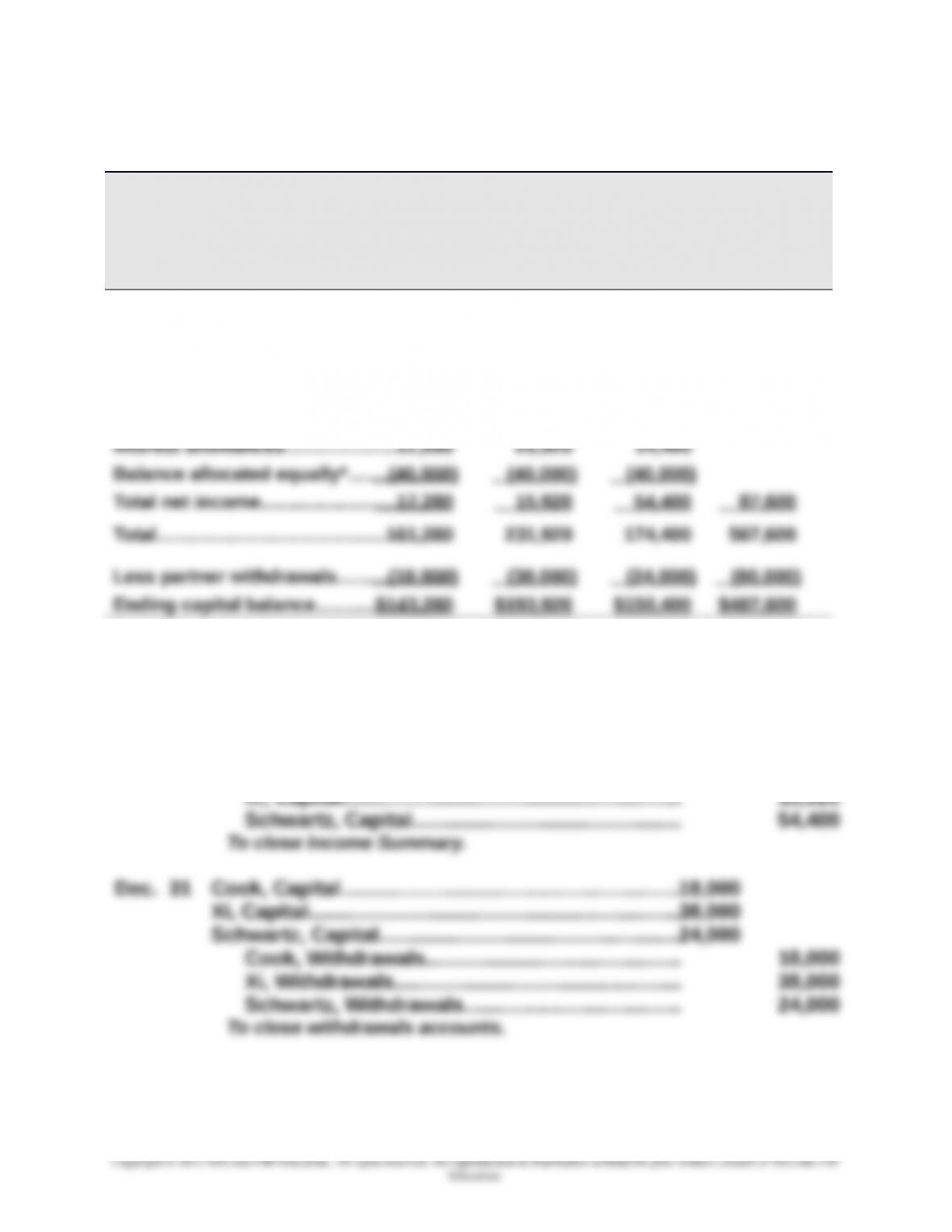

CXS PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Cook Xi Schwart

z

Total

Beginning capital balances..................$ 0 $ 0 $ 0 $ 0

Plus

Investments by owners.........................144,000 216,000 120,000 480,000

Net income

Salary allowances..................................40,000 30,000 80,000

* [$87,600 – ($40,000 + $30,000 + $80,000) – ($17,280 + $25,920 + $14,400)] /3

Part 3

Dec. 31 Income Summary.....................................................87,600

Cook, Capital...................................................... 17,280

12-682

Chapter 12 - Accounting for Partnerships

Problem 12-4B (50 minutes)

Part 1

a)

Apr. 30 Gibbs, Capital...........................................................606,000

Brady, Capital..................................................... 606,000

To record admission of Brady.

d)

Apr. 30 Gibbs, Capital...........................................................606,000

Cook, Capital*...................................................... 51,200

Chan, Capital**.................................................... 204,800

Cash..................................................................... 350,000

To record Gibbs’s withdrawal and the

bonus to old partners.

* ($606,000 - $350,000) x 1/5

**($606,000- $350,000) x 4/5

e)

12-683

Chapter 12 - Accounting for Partnerships

Problem 12-4B (Concluded)

Part 2

a)

Apr. 30 Cash...........................................................................300,000

Chip, Capital*...................................................... 300,000

To record admission of Chip.

* Supporting calculations

$606,000 + $148,000 + $446,000 = $1,200,000

($1,200,000 + $300,000) x 20% = $300,000

Thus, no bonus is received or granted.

b)

Apr. 30 Cash...........................................................................196,000

Gibbs, Capital ($83,200* x 5/10)................................ 41,600

c)

Apr. 30 Cash...........................................................................426,000

Gibbs, Capital ($100,800* x 5/10).......................... 50,400

12-684

Chapter 12 - Accounting for Partnerships

Problem 12-5B (75 minutes)

Note: All entries in this problem are dated Jan. 18.

1.

(a) Cash...........................................................................650,000

Equipment............................................................ 617,200

Gain on Sale of Equipment................................. 32,800

2.

(a) Cash...........................................................................530,000

Loss on Sale of Equipment.....................................87,200

Equipment............................................................ 617,200

(b) Lasure, Capital ($87,200 x 2/5)................................34,880

Ramirez, Capital ($87,200 x 1/5)..............................17,440

Toney, Capital ($87,200 x 2/5)..................................34,880

Loss on Sale of Equipment................................ 87,200

12-685

Chapter 12 - Accounting for Partnerships

Problem 12-5B (Concluded)

3.

(a) Cash...........................................................................200,000

Loss on Sale of Equipment.....................................417,200

Equipment........................................................... 617,200

Cash..................................................................... 342,600

(d) Lasure, Capital ($300,400 - $166,880).....................133,520

Ramirez, Capital ($195,800 - $83,440).....................112,360

Cash*................................................................... 245,880

* $348,600 + $200,000 + $39,880 - $342,600

4.

(a) Cash...........................................................................150,000

Loss on Sale of Equipment.....................................467,200

Equipment........................................................... 617,200

(d) Lasure, Capital*........................................................73,600

Ramirez, Capital**.....................................................82,400

Cash***................................................................ 156,000

*$300,400 - $186,880 - $39,920

**$195,800 - $93,440 - $19,960

***$348,600 + $150,000 - $342,600

12-686

Chapter 12 - Accounting for Partnerships

Serial Problem — SP 12

1. The owner should consider several factors:

a. If the company continues to earn profits, at a 1:1 ownership, she will

have to share profits equally with her new partner. On the other hand,

at a 4:1 ownership, she will only have to share one-fifth of the profits

c. If the partner invests in the business equal to their partnership

interest, there will be more total equity in the business if the partner

invests at the 1:1 level.

2a.

Jan. 1 Cash........................................................................... 80,360

New Partner, Capital............................................ 80,360

To admit a new partner at a 1:1 ownership interest

4. Total capital before admission of partner..........................$ 80,360

Partner investment............................................................... 20,090

Total capital after admission of partner.............................$100,450

New partner’s equity percentage ($20,090 / $100,450)..... 20%

Reporting in Action — BTN 12-1

12-687

1. The founders of Apple are Steve Wozniak, Steve Jobs and Ron Wayne.

Each Apple I personal computer kit was single-handedly designed and

hand-built by Steve Wozniak. The Apple I went on sale in July 1976 and

was market-priced at $666.66 ($2,763 in 2014 dollars, adjusted for

inflation).

2. At least two differences would be immediately apparent between

Apple’s corporate income statement and a partnership income

statement.

3. Specifically, the balance sheet for a partnership would not have the

following accounts as reported in the Apple balance sheet reproduced

in Appendix A:

12-688