PROBLEM SET B

Problem 12-1B (45 minutes)

Preliminary calculations

Plan (a) & Plan (c)

Percentages based on initial investments

Plan (b)

Percentages based on time

Plan (c) & Plan (d)

Salary allowance

Plan (d)

Interest allowances

Income (Loss)

Year 1

Sharing Plan

Calculations

Bell

Green

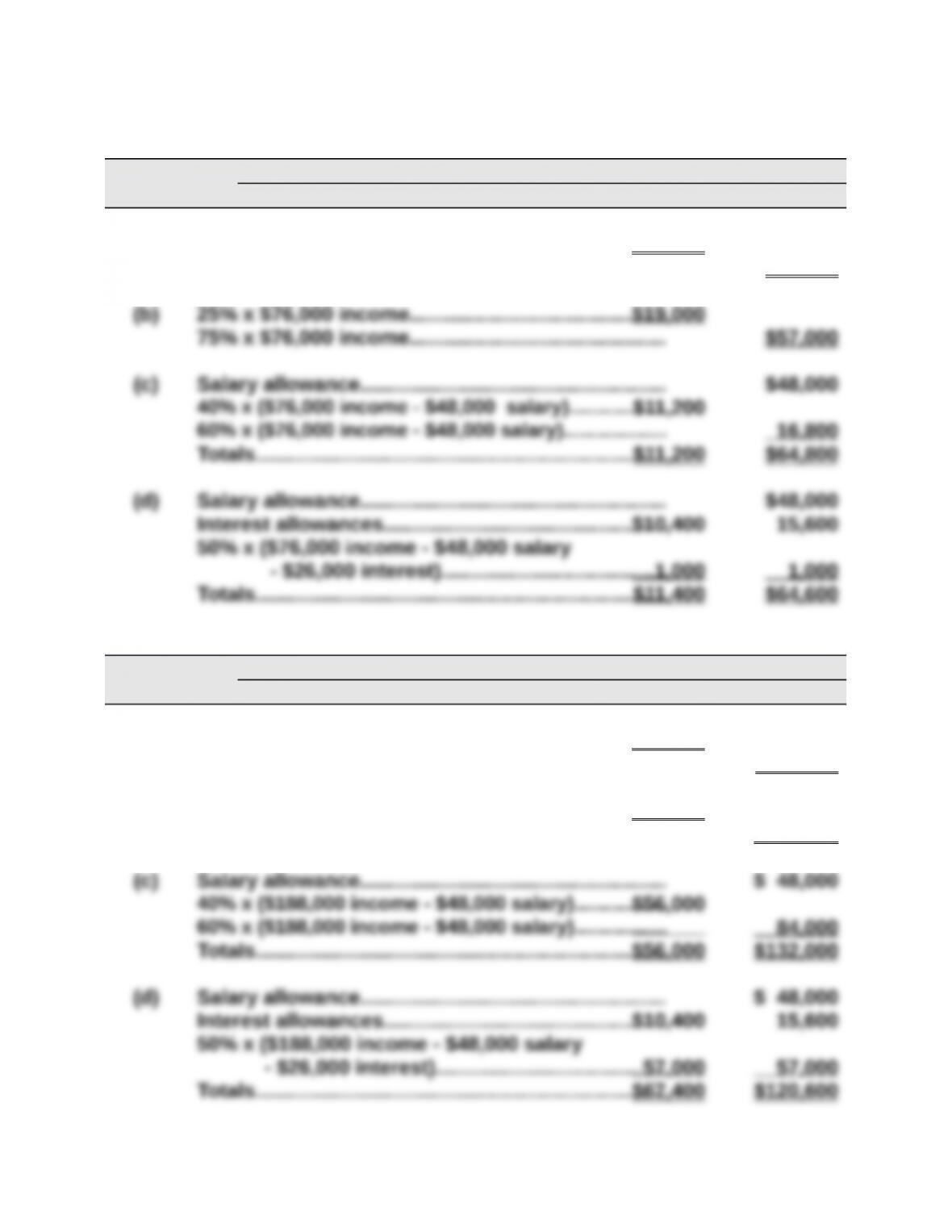

(a)

(b)

(c)

Salary allowance……………………………………………..

Totals……………………………………………………………..

(d)

Salary allowance……………………………………………..

Interest allowances………………………………………….

Totals……………………………………………………………..

Problem 12-1B (Concluded)

Income (Loss) Year 2

Sharing Plan Calculations Bell Green

(a) 40% x $76,000 income……………………………………..$30,400

60% x $76,000 income…………………………………….. $45,600

Income (Loss) Year 3

Sharing Plan Calculations Bell Green

(a) 40% x $188,000 income……………………………………$75,200

60% x $188,000 income…………………………………… $112,800

(b) 25% x $188,000 income……………………………………$47,000

75% x $188,000 income…………………………………… $141,000

Problem 12-2B (50 minutes)

1.

Dec. 31 Income Summary…………………………………………….270,000

Mark Albin, Capital…………………………………….. 90,000

2.

Dec. 31 Income Summary…………………………………………….270,000

Mark Albin, Capital…………………………………….. 135,000

3.

Dec. 31 Income Summary…………………………………………….270,000

Mark Albin, Capital…………………………………….. 118,800

*Supporting calculations Albin Peters Ramsey Total

Net income…………………………………………… $270,000

Salary allowances

Albin………………………………………………….$ 96,000

Peters……………………………………………….. $72,000

Problem 12-3B (30 minutes)

Part 1

Income (Loss)

Sharing Plan Calculations Cook Xi Schwartz Total

(b) $240,000 x ($144,000/$480,000)………………..

$72,000

(c) Net income………………………………………….. $240,000

Salary allowances…………………………………$40,000 $ 30,000 $ 80,000 (150 ,000)

Balance of income……………………………….. 90,000

Interest allowances

Problem 12-3B (Concluded)

Part 2

CXS PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Cook Xi Schwart

z

Total

Beginning capital balances………………$ 0 $ 0 $ 0 $ 0

Plus

Investments by owners……………………144,000 216,000 120,000 480,000

Net income

Part 3

Dec. 31 Income Summary…………………………………………….87,600

Cook, Capital…………………………………………….. 17,280

Dec. 31 Cook, Capital…………………………………………………..18,000

Xi, Capital……………………………………………………….38,000

Problem 12-4B (50 minutes)

Part 1

a)

Apr. 30 Gibbs, Capital………………………………………………….606,000

Brady, Capital……………………………………………. 606,000

To record admission of Brady.

b)

Apr. 30 Gibbs, Capital………………………………………………….606,000

Cannon, Capital………………………………………….. 606,000

To record admission of Cannon.

c)

e)

Apr. 30 Gibbs, Capital………………………………………………….606,000

Accum. Deprec.—Manufacturing Equipment……..336,000

Problem 12-4B (Concluded)

Part 2

a)

Apr. 30 Cash……………………………………………………………….300,000

Chip, Capital*…………………………………………….. 300,000

To record admission of Chip.

* Supporting calculations

b)

Apr. 30 Cash……………………………………………………………….196,000

Gibbs, Capital ($83,200* x 5/10)………………………….. 41,600

c)

Apr. 30 Cash……………………………………………………………….426,000

Gibbs, Capital ($100,800* x 5/10)……………………. 50,400

Cook, Capital ($100,800* x 1/10)…………………….. 10,080

Problem 12-5B (75 minutes)

Note: All entries in this problem are dated Jan. 18.

1.

(a) Cash……………………………………………………………….650,000

(b) Gain on Sale of Equipment……………………………….32,800

(c) Accounts Payable……………………………………………342,600

(d) Lasure, Capital ($300,400 + $13,120)………………… 313,520

2.

(a) Cash……………………………………………………………….530,000

(b) Lasure, Capital ($87,200 x 2/5)………………………….34,880

(d) Lasure, Capital ($300,400 – $34,880)………………….265,520

Problem 12-5B (Concluded)

3.

(a) Cash……………………………………………………………….200,000

(b) Lasure, Capital ($417,200 x 2/5)………………………..166,880

Ramirez, Capital ($417,200 x 1/5)………………………83,440

(c) Accounts Payable……………………………………………342,600

Cash…………………………………………………………. 342,600

(d) Lasure, Capital ($300,400 – $166,880)………………..133,520

4.

(a) Cash……………………………………………………………….150,000

(b) Lasure, Capital ($467,200 x 2/5)………………………..186,880

(c) Accounts Payable……………………………………………342,600

Cash…………………………………………………………. 342,600

(d) Lasure, Capital*……………………………………………….73,600

Serial Problem — SP 12

1. The owner should consider several factors:

a. If the company continues to earn profits, at a 1:1 ownership, she will

have to share profits equally with her new partner. On the other hand,

b. At the 1:1 ownership, her partner will have more of a say in how the

c. If the partner invests in the business equal to their partnership

d. It would likely be easier to attract a partner if there is a lower amount

2a.

Jan. 1 Cash………………………………………………………………. 80,360

2b.

Jan. 1 Cash………………………………………………………………. 20,090

3.

Jan. 1 Cash………………………………………………………………. 20,090

4. Total capital before admission of partner……………………. $ 80,360