Chapter 12 – Accounting for Partnerships

Problem 12-4A (50 minutes)

Part 1

a)

Feb. 1 Benson, Capital…………………………..…….….…….…...138,000

North, Capital……………………………………………... 138,000

To record admission of North.

b)

**($214,000 – $138,000) x 5/8

e)

Feb. 1 Benson, Capital…………………………..…….….…….…...138,000

Accumulated Depreciation—Equipment………..….. 23,200

Meir, Capital*…………………………………………….… 22,950

Lau, Capital**………………………..….….…….….…… 38,250

Equipment…………………………………………….….… 70,000

12-681

Chapter 12 – Accounting for Partnerships

Problem 12-4A (Concluded)

Part 2

a)

Feb. 1 Cash…………………………………………………………………200,000

b)

Feb. 1 Cash…………………………………………………………………145,000

Meir, Capital ($41,250* x 3/10)……..…….….….…….… 12,375

Benson, Capital ($41,250* x 2/10).….….….…….….... 8,250

c)

Feb. 1 Cash…………………………………………………………………262,000

Meir, Capital ($46,500* x 3/10)….…….….….…….. 13,950

Benson, Capital ($46,500* x 2/10)..…….…......... 9,300

Lau, Capital ($46,500* x 5/10)……….…….….……. 23,250

Rhodes, Capital…………………………….….…….….. 215,500

To record admission of Rhodes and bonus to old partners.

12-682

Chapter 12 – Accounting for Partnerships

Problem 12-5A (75 minutes)

Note: All entries in this problem are dated May 31.

1.

(a) Cash…………………………………………………………………600,000

Inventory……………………………….….…….….……... 537,200

Gain on Sale of Inventory……………….…….….…. 62,800

* $180,800 + $600,000 – $245,500

2.

(a) Cash…………………………………………………………………500,000

Loss on Sale of Inventory………………………………….37,200

Inventory……………………………….….…….….……... 537,200

(b) Kendra, Capital ($37,200 x 3/6)…………………………..18,600

Cogley, Capital ($37,200 x 2/6)……..….….…….….…..12,400

Mei, Capital ($37,200 x 1/6)…………………..….…….…. 6,200

Loss on Sale of Inventory………………………….... 37,200

Problem 12-5A (Concluded)

3.

12-683

Chapter 12 – Accounting for Partnerships

(a) Cash…………………………………………………………………320,000

Loss on Sale of Inventory………………………………….217,200

Inventory……………………………….….…….….……... 537,200

(d) Cogley, Capital ($212,500 – $72,400)……..…….….….140,100

Mei, Capital ($167,000 – $36,200)…………………..…...130,800

Cash*…………………………………….…….….…….…... 270,900

*(180,800 + 320,000+15,600-245,500)

4.

(a) Cash…………………………………………………………………250,000

Loss on Sale of Inventory………………………………….287,200

Inventory……………………………….….…….….……... 537,200

Cash………………………………………………………..…. 245,500

(d) Cogley, Capital*………………………….…….….…….….… 83,034

Mei, Capital**………………………………………………….…102,266

Cash***…………………………..…….….…….….….…… 185,300

*$212,500 – $95,733 – $33,733

**$167,000 – $47,867 – $16,867 ***$180,800 + $250,000 – $245,500

12-684

Chapter 12 – Accounting for Partnerships

PROBLEM SET B

Problem 12-1B (45 minutes)

Preliminary calculations

Plan (a) & Plan (c)

Percentages based on initial investments

Bell = $104,000/$260,000 = 40%

Green = $156,000/$260,000 = 60%

Plan (d)

Interest allowances

Bell = 10% x $104,000 = $10,400

Green = 10% x $156,000 = $15,600

Income (Loss)

Year 1

Sharing Plan

Calculations

Bell

Green

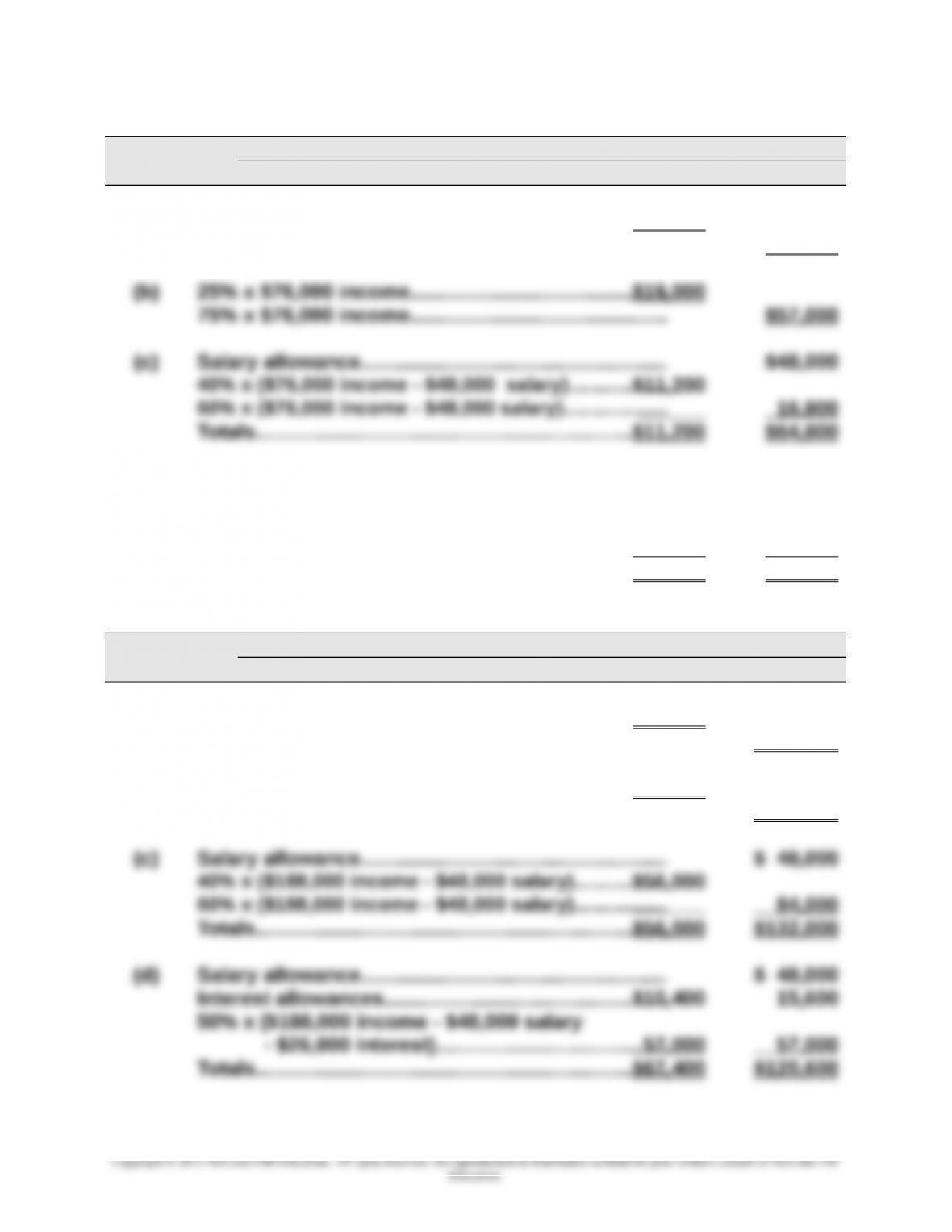

(a)

12-685

Chapter 12 – Accounting for Partnerships

40% x $36,000 loss………………………………….….…….

$(14,400)

(b)

25% x $36,000 loss………………………………….….…….

$ (9,000)

(c)

12-686

Chapter 12 – Accounting for Partnerships

60% x ($36,000 loss + $48,000 salary)…..….…….….

_______

(50,400)

50% x ($36,000 loss + $48,000 salary

+ $26,000 interest)……………….….….…….…..

(55,000)

12-687

Chapter 12 – Accounting for Partnerships

Problem 12-1B (Concluded)

Income (Loss) Year 2

Sharing Plan Calculations Bell Green

(a) 40% x $76,000 income……………………………………….$30,400

60% x $76,000 income………………………………………. $45,600

(d) Salary allowance…………………..….…….….…….….….. $48,000

Interest allowances…………………………….….…….…..$10,400 15,600

50% x ($76,000 income – $48,000 salary

– $26,000 interest)…………………….….…….…. 1,000 1,000

Totals…………………………………………….….….….……...$11,400 $64,600

Income (Loss) Year 3

Sharing Plan Calculations Bell Green

(a) 40% x $188,000 income……………………………………..$75,200

60% x $188,000 income…………………………………….. $112,800

(b) 25% x $188,000 income……………………………………..$47,000

75% x $188,000 income…………………………………….. $141,000

12-688

Chapter 12 – Accounting for Partnerships

Problem 12-2B (50 minutes)

1.

Dec. 31 Income Summary……………………….….…….….….……270,000

Mark Albin, Capital……………………….….…….…... 90,000

Roland Peters, Capital……………..…….….…….…. 90,000

Sam Ramsey, Capital……………..….…….….….….. 90,000

To close Income Summary.

2.

3.

Dec. 31 Income Summary………………….….…….….…….….…..270,000

Mark Albin, Capital……………………….….…….…... 118,800

Roland Peters, Capital…………….…….….…….….. 88,240

Sam Ramsey, Capital……………..….…….….….….. 62,960

To close Income Summary.*

*Supporting calculations Albin Peters Ramsey Total

12-689