Problem 12-1A (Concluded)

Income (Loss) Year 2

Sharing Plan Calculations Watts Lyon

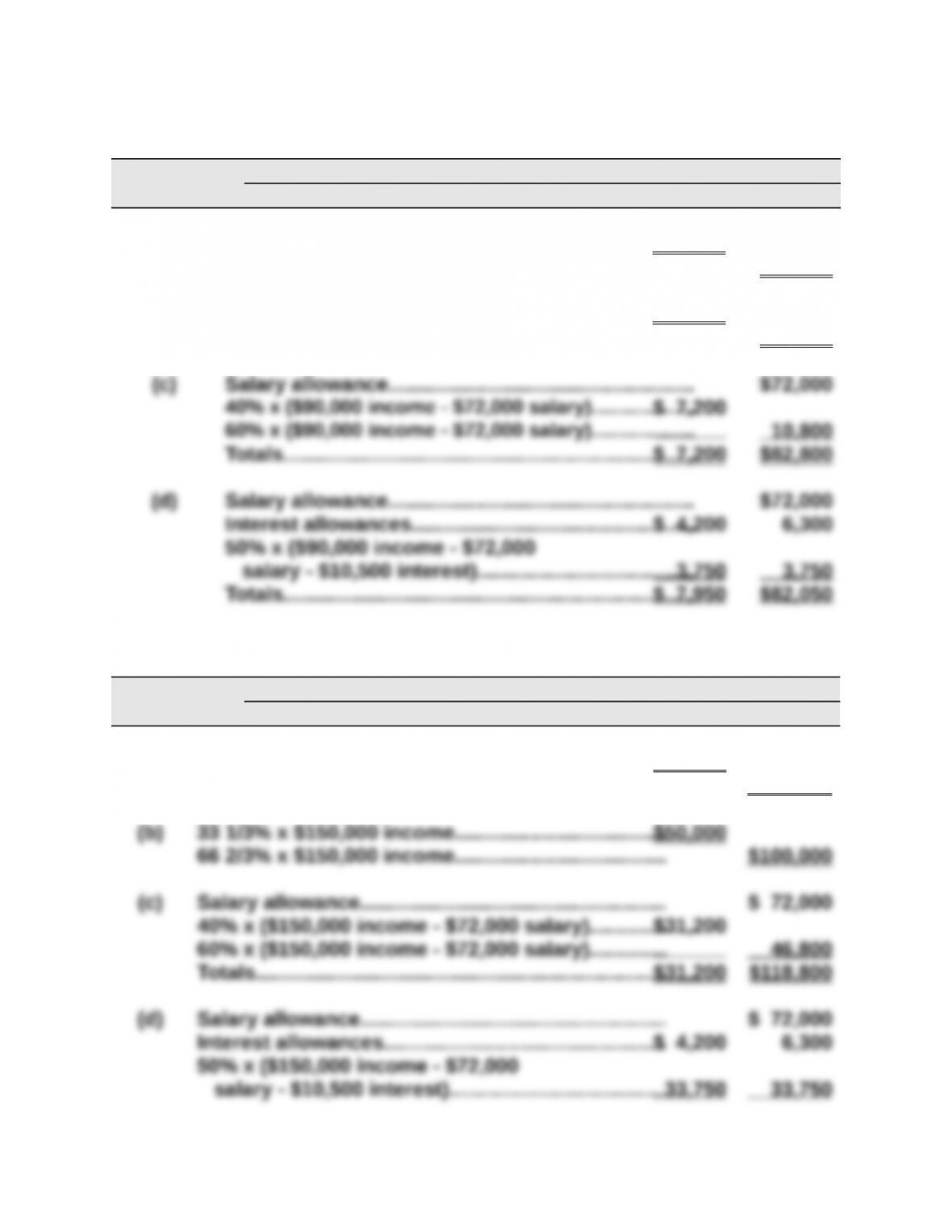

(a) 40% x $90,000 income……………………………………..$36,000

60% x $90,000 income…………………………………….. $54,000

(b) 33 1/3% x $90,000 income………………………………..$30,000

66 2/3% x $90,000 income……………………………….. $60,000

Income (Loss) Year 3

Sharing Plan Calculations Watts Lyon

(a) 40% x $150,000 income……………………………………$60,000

60% x $150,000 income…………………………………… $ 90,000

Problem 12-2A (50 minutes)

1.

Dec. 31 Income Summary…………………………………………….249,000

Kara Ries, Capital………………………………………. 83,000

2.

Dec. 31 Income Summary…………………………………………….249,000

Kara Ries, Capital………………………………………. 62,250

3.

Dec. 31 Income Summary…………………………………………….249,000

Kara Ries, Capital………………………………………. 79,000

Tammy Bax, Capital…………………………………… 72,200

Joe Thomas, Capital………………………………….. 97,800

To close Income Summary*.

*Supporting calculations Ries Bax Thomas Total

Net income…………………………………………… $249,000

Problem 12-3A (40 minutes)

Part 1

Income (Loss)

Sharing Plan Calculations Bill Bruce Barb Total

(b) $450,000 x ($67,500/$750,000)…………………………………..

40,500

(c) Net income…………………………………………………………. $450,000

Salary allowances………………………………………………..$ 80,000 $ 60,000 $ 90,000 (230 ,000)

Balance of income………………………………………………. 220,000

Interest allowances

Problem 12-3A (Concluded)

Part 2

BBB PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Bill Bruce Barb Total

Beginning capital balances…………..$ 0 $ 0 $ 0 $ 0

Plus

Investments by owners………………67,500 262,500 420,000 750,000

Net income

Salary allowances……………………. 80,000 60,000 90,000

Part 3

Dec. 31 Income Summary…………………………………………….209,000

Bill Beck, Capital……………………………………….. 67,550

Dec. 31 Bill Beck, Capital……………………………………………..34,000

Bruce Beck, Capital…………………………………………48,000

Problem 12-4A (50 minutes)

Part 1

a)

Feb. 1 Benson, Capital……………………………………………….138,000

b)

Feb. 1 Benson, Capital……………………………………………….138,000

c)

Feb. 1 Benson, Capital……………………………………………….138,000

d)

Feb. 1 Benson, Capital……………………………………………….138,000

e)

Feb. 1 Benson, Capital……………………………………………….138,000

Accumulated Depreciation—Equipment…………… 23,200

Meir, Capital*…………………………………………….. 22,950

Problem 12-4A (Concluded)

Part 2

a)

Feb. 1 Cash……………………………………………………………….200,000

Rhodes, Capital*……………………………………….. 200,000

To record admission of Rhodes.

b)

Feb. 1 Cash……………………………………………………………….145,000

Meir, Capital ($41,250* x 3/10)………………………….. 12,375

Benson, Capital ($41,250* x 2/10)……………………… 8,250

c)

Feb. 1 Cash……………………………………………………………….262,000

Meir, Capital ($46,500* x 3/10)……………………… 13,950

Problem 12-5A (75 minutes)

Note: All entries in this problem are dated May 31.

1.

(a) Cash……………………………………………………………….600,000

Inventory…………………………………………………… 537,200

Gain on Sale of Inventory…………………………… 62,800

(b) Gain on Sale of Inventory…………………………………62,800

(c) Accounts Payable……………………………………………245,500

Cash…………………………………………………………. 245,500

2.

(a) Cash……………………………………………………………….500,000

Loss on Sale of Inventory………………………………..37,200

Inventory…………………………………………………… 537,200

(b) Kendra, Capital ($37,200 x 3/6)………………………….18,600

(d) Kendra, Capital ($93,000 – $18,600)……………………74,400

Problem 12-5A (Concluded)

3.

(a) Cash……………………………………………………………….320,000

(b) Kendra, Capital ($217,200 x 3/6)………………………..108,600

Cash………………………………………………………………. 15,600

(c) Accounts Payable……………………………………………245,500

(d) Cogley, Capital ($212,500 – $72,400)………………….140,100

4.

(a) Cash……………………………………………………………….250,000

(b) Kendra, Capital ($287,200 x 3/6)………………………..143,600

Cogley, Capital ($50,600 x 2/3)…………………………. 33,733

(c) Accounts Payable……………………………………………245,500

(d) Cogley, Capital*………………………………………………. 83,034

(a) Cash……………………………………………………………….250,000

Loss on Sale of Inventory………………………………..287,200