Problem 10-8B (20 minutes)

1.

2015 (a)

To record payment for sublease.

(b)

To record prepaid annual lease rental.

(c)

To record costs of leasehold improvements.

2.

2015 (a)

Dec. 31 Rent Expense……………………………………………………..8,000

(b)

Dec. 31 Amortization Expense—Leasehold Improvements………4,000

Accumulated Amortization—Leasehold

(c)

Dec. 31 Rent Expense……………………………………………………..36,000

Serial Problem — SP 10

Serial Problem — SP 10, Business Solutions (45 minutes)

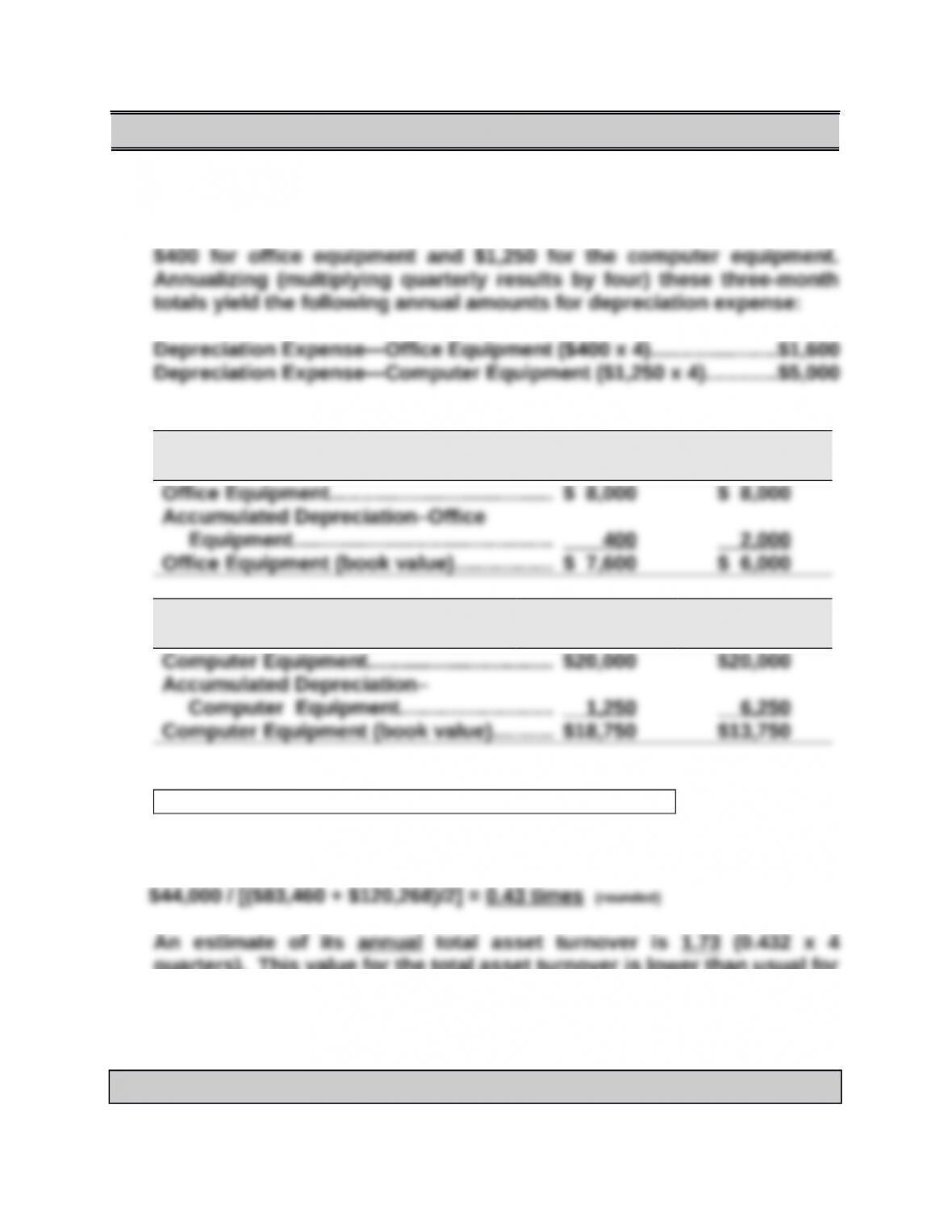

1. For the three months ended March 31, 2016, depreciation expense was

2.

December 31,

2015

December 31,

2016

December 31,

2015

December 31,

2016

3.

Total asset turnover = Net sales / Average total assets

The 3-month total asset turnover at March 31, 2016:

quarters). This value for the total asset turnover is lower than usual for

companies competing in this industry (2.5). However, the company is

in its first year of operations, and its turnover will improve if it can

generate increased sales throughout the year while maintaining a

similar asset level.

Reporting in Action — BTN 10-1

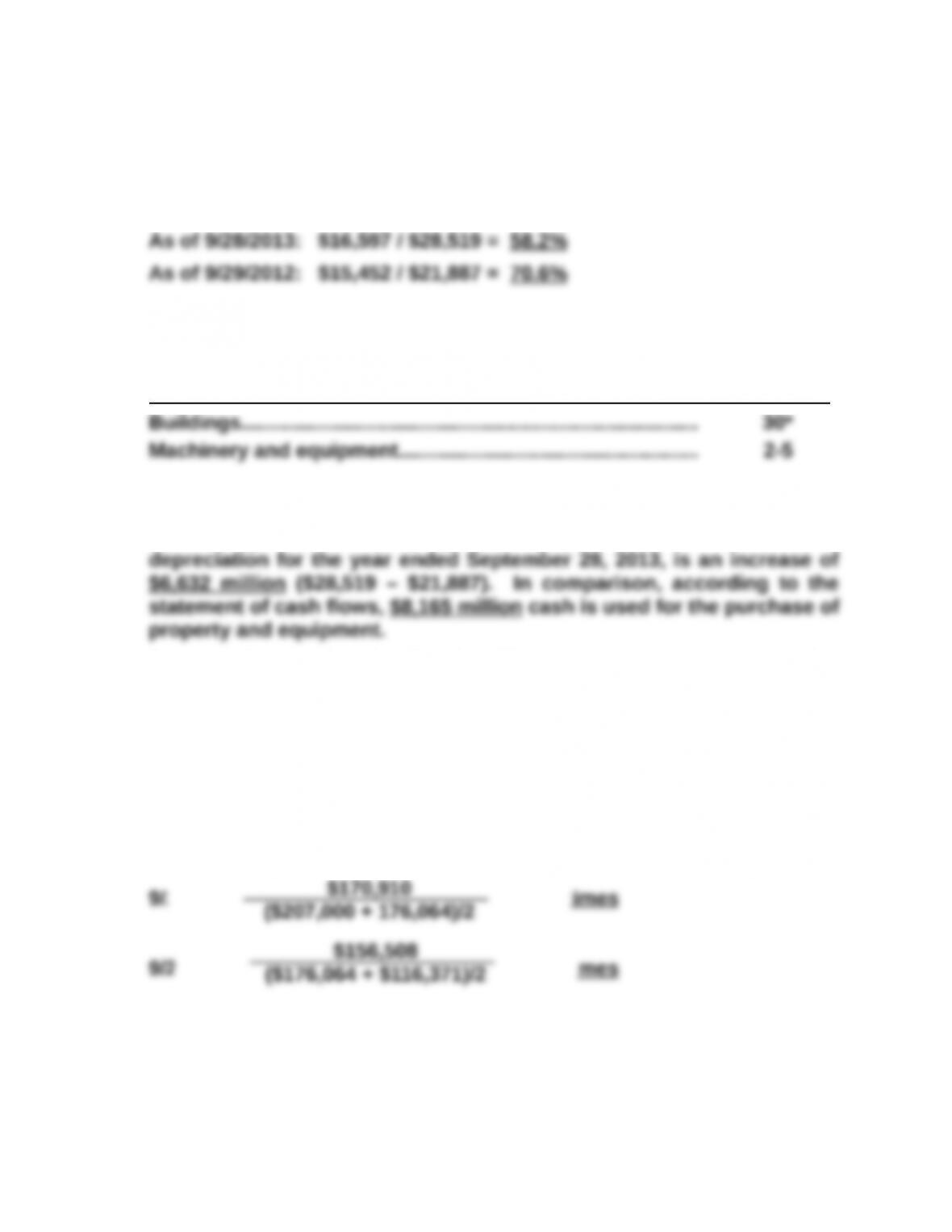

1. The percent of original cost remaining to be depreciated is computed

by taking the ratio of the book value of property and equipment to the

original cost ($ millions):

2. In Apple’s “Summary of Significant Accounting Policies” (Note 1:

Property, Plant and Equipment) it discloses estimated useful lives by

major asset category as follows:

Asset Life (in years)

*Or the remaining life of the building, if less

3. The change in total property and equipment before accumulated

One possible explanation for the difference in these amounts is that

Apple likely disposed of property and equipment during the year. Since

the investing section of the cash flow statement does not list proceeds

from the sale of property and equipment, these assets could have been

scrapped for no proceeds. Another possible explanation is that it wrote

off assets that were fully depreciated. Still another is that Apple

acquired property and equipment for something other than cash.

4. Total asset turnover for year ended ($ millions):

5. Solution depends on the financial statement data obtained.

Comparative Analysis — BTN 10-2

Note: Total asset turnover = Net sales / Average total assets

1. Total asset turnover for Apple ($ millions)

2. Each dollar of Apple’s assets produces $0.89 and $1.07 in net sales for

Apple employs its assets more efficiently than Google for both years.

Ethics Challenge — BTN 10-3

1. When managers acquire new assets a number of decisions relative to

2. When assets are placed in use on a day other than the first day of the

month an assumption is often made that the assets are placed in use

on the first day of the month nearest to the date of the purchase. For

($93,798 + $72,574)/2

$170,910

By selecting the first day of the following month, Choi is getting a

one-time deferral of some partial months of depreciation. She is still

2. By always assuming the first day of the following month as the date of

purchase, less depreciation is (initially) accrued for the assets

Communicating in Practice — BTN 10-4

The solution to this activity will vary based on the industry and the

companies chosen for analysis. Many instructors find it useful to report

the results from the teams to the class for purposes of classroom

discussion and analysis.

Taking It to the Net — BTN 10-5

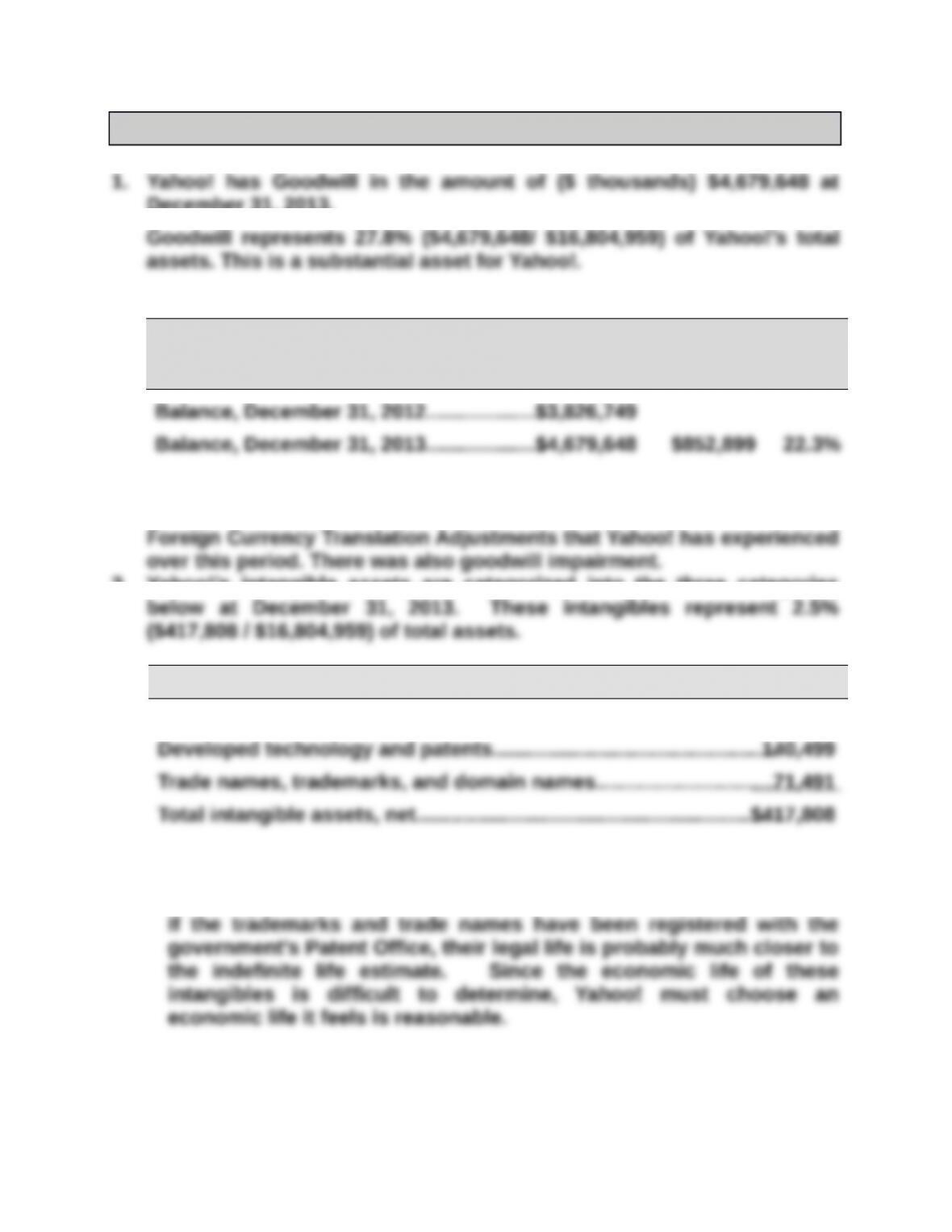

December 31, 2013.

2.

Goodwill (in $ thousands)

Total

Amount

$ Change

from Prior

Year

%

Change

Goodwill has increased over this period. The increase is due mainly to

new goodwill recorded due to acquisitions in 2013 and, secondly, to

3. Yahoo!’s intangible assets are categorized into the three categories

December 31, 2013 (in thousands)

Customer, affiliate and advertiser related relationships……………..$ 205,818

1. Note 6 indicates that Trade names, trademarks, and domain names

have original estimated useful lives of “one year to an indefinite life.”

Teamwork in Action — BTN 10-6

1. Annual depreciation for each year of the asset’s useful life:

Year Straight-line Double-Declining-Balance Units-of-Production

2013 ($44,000-$2,000)/4

= $10,500

(100%/4) x 2 = 50% is

declining-balance rate.

BV x rate = $44,000 x 50%

= $22,000

($44,000-$2,000)/60,000 miles

= $.70 per mile.

12,000 miles x $.70 = $ 8,400

salvage) = $3,500

* Depreciation is based on the estimated capacity of 60,000 miles. Even though the van is

driven 10,000 miles in the last year, depreciation can only be taken for the remaining 9,000

miles of estimated capacity. This will record depreciation to the estimated salvage value.

2. Depreciation is recorded in an adjusting entry at the end of each

period. The entry is:

Depreciation Expense……………………………. xxxx*

Accumulated Depreciation………….. xxxx*

*Amount varies by method and year (see part 1).

3. Each expert’s presentation of the comparison of methods will be slightly

different. The experts should make the following points: The

Teamwork in Action — BTN 10-6 – continued

4. Book value at the end of each year

= Cost – Accumulated depreciation

Year Straight-line

Double-Declining-

Balance Units of Production

2013…….. $33,500 $22,000 $35,600

For reporting purposes, each expert will have different results. But

each should show:

Plant Assets:

* Amounts vary by the method and the year selected for illustration. Experts should explain

the amounts shown.

Entrepreneurial Decision — BTN 10-7

Part 1

(a) Under current conditions, the total asset turnover is 3.2. This is

* Total asset turnover =

(b) Under this proposal, its asset turnover would increase to 4. This is

Part 2

The proposal would yield an improved total asset turnover of 4 vis-à-vis the

current total asset turnover of 3.2. However, we need to recognize that this

*We must remember that total asset turnover is only one dimension of a complete analysis of this

proposal. For example, we would want to explore the impact of this proposal on net income and

other activities.

Net sales

Average total assets

Hitting the Road — BTN 10-8

No formal solution exists for this activity. It is usually interesting for the

class to exchange their discoveries via class discussion. This is

particularly the case with respect to patents, copyrights, and trademarks.

Global Decision — BTN 10-9

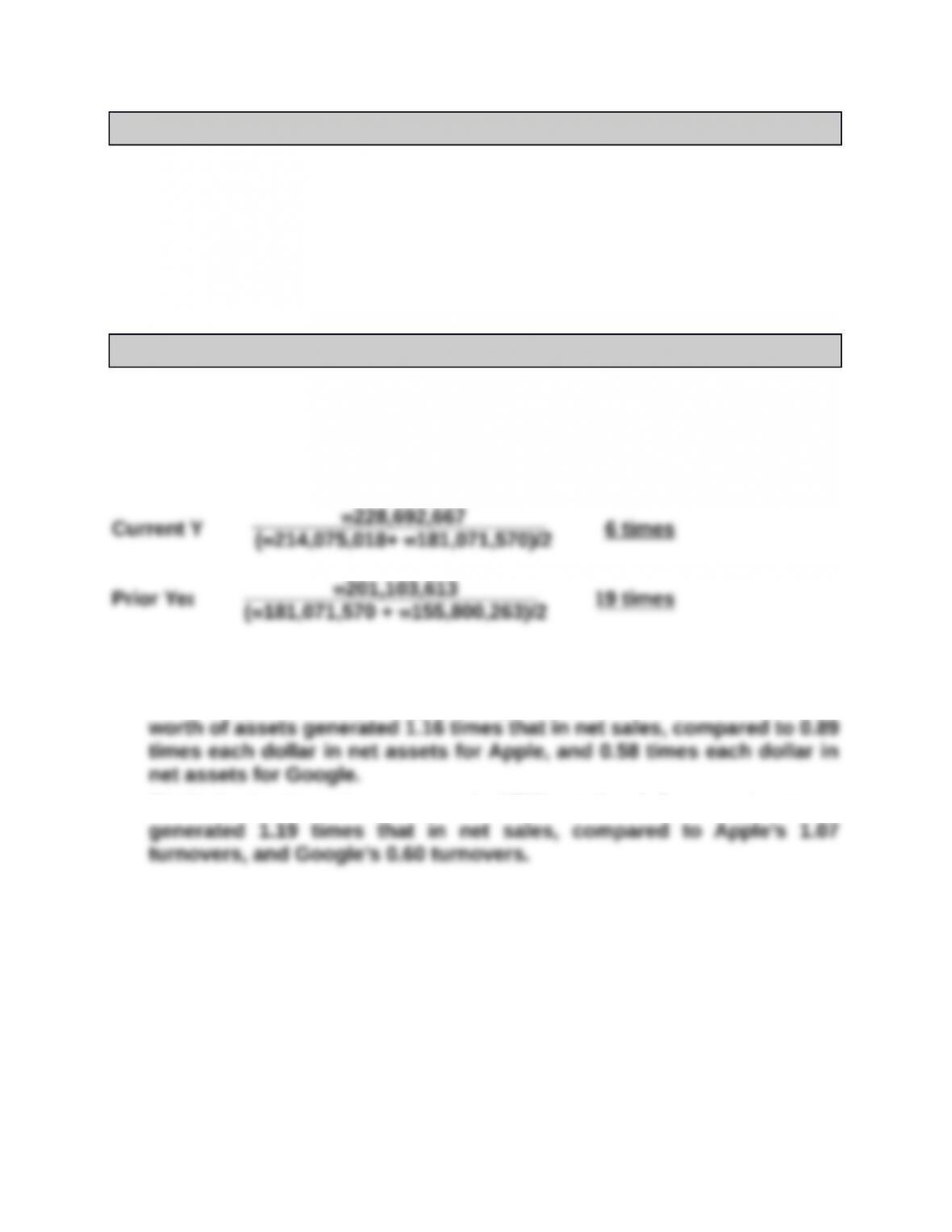

Note: Total asset turnover = Net sales / Average total assets

1. Total asset turnover for Samsung (KRW in millions):

2. Samsung was more efficient in using its assets to generate net sales

than Google and Apple. Specifically, in the current year, each KRW

Similarly, in the prior year, each KRW worth of Samsung’s assets

generated 1.19 times that in net sales, compared to Apple’s 1.07

turnovers, and Google’s 0.60 turnovers.

₩228,692,667

(₩181,071,570 + ₩155,800,263)/2