Chapter 10 – Plant Assets, Natural Resources, and Intangibles

Problem 10-2B (25 minutes)

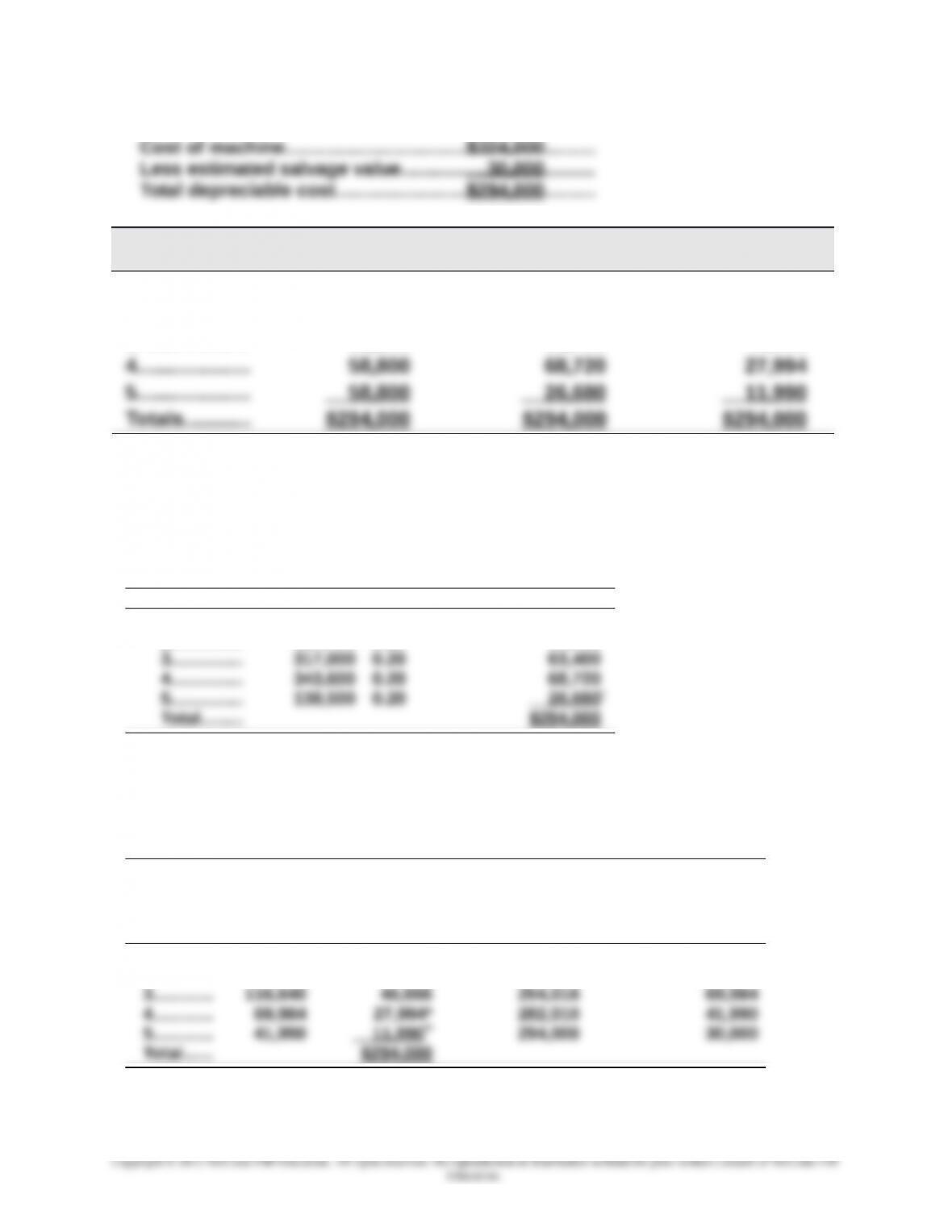

Year Straight-LineaUnits-of-Productionb

Double-Declining-

Balancec

1…..…………... $ 58,800 $ 71,120 $129,600

2…..…………... 58,800 64,080 77,760

3…..…………... 58,800 63,400 46,656

aStraight- line:

Cost per year = $294,000/5 years = $58,800 per year

bUnits-of-production:

Cost per unit = $294,000/1,470,000 units = $0.20 per unit

Year Units Unit Cost Depreciation

1………...... 355,600 $0.20 $ 71,120

2………...... 320,400 0.20 64,080

* Take only enough depreciation in Year 5 to reduce book

value to the asset’s $30,000 salvage value.

cDouble-declining-balance (amounts rounded to the nearest dollar):

(100%/5) x 2 = 40% depreciation rate

Year

Beginning

Book Value

Annual

Depreciation

(40% of

Book Value)

Accumulated

Depreciation

at the End of

the Year

Ending Book Value

($324,000 Cost less

Accumulated

Depreciation)

1…......... $324,000 $129,600 $129,600 $194,400

2…......... 194,400 77,760 207,360 116,640

* rounded

** Take only enough depreciation in Year 5 to reduce book value to the asset’s

$30,000 salvage value.

10-581

Chapter 10 – Plant Assets, Natural Resources, and Intangibles

Problem 10-3B (45 minutes)

Part 1

Land

Building

B

Building

C

Land

Improve-

ments B

Land

Improve-

ments C

Purchase price*..........$ 868,000 $527,000 $155,000

Demolition……............. 122,000

Allocation of

purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost

Land…….………….…................... $ 795,200 56% $ 868,000

Part 2

2015

Jan. 1 Land……………………………………………….…..……..….. 1,164,500

Building B………………………………………………………. 527,000

Part 3

2015

Dec. 31 Depreciation Expense—Building B………………..………………..

……………………………………………………………………………………….

……………………………………………………………………………………….

28,500

Accumulated Depreciation—Building B….………….......... 28,500

To record depreciation [($527,000 – $99,500)/15].

10-582

31 Depreciation Expense–Land Improvements C………

……………………………………………………………………..…….

10,350

10-583

Chapter 10 – Plant Assets, Natural Resources, and Intangibles

Problem 10-4B (50 minutes)

2014

Jan. 1 Equipment…………………………………………………..……….27,670

Cash…………………………………………………………….… 27,670

To record costs of van ($25,860 + $1,810).

To record depreciation.

*2014 depreciation after January 3rd betterment

Total original cost……………………………………………………….…..$27,670

Plus cost of betterment…………………………………………………... 1,850

2015

Jan. 1 Equipment…………………………………………………..………. 2,064

Cash…………………………………………………………….… 2,064

To record extraordinary repair on van.

*2015 depreciation after 1/1 extraordinary repair

Total cost ($29,520 + $2,064)…………………………………………………..…..………....$31,584

Less accumulated depreciation……………………………………………………………… 5,124

Book value…………………………………………………………………………………………....26,460

10-584

Chapter 10 – Plant Assets, Natural Resources, and Intangibles

Problem 10-5B (40 minutes)

2014

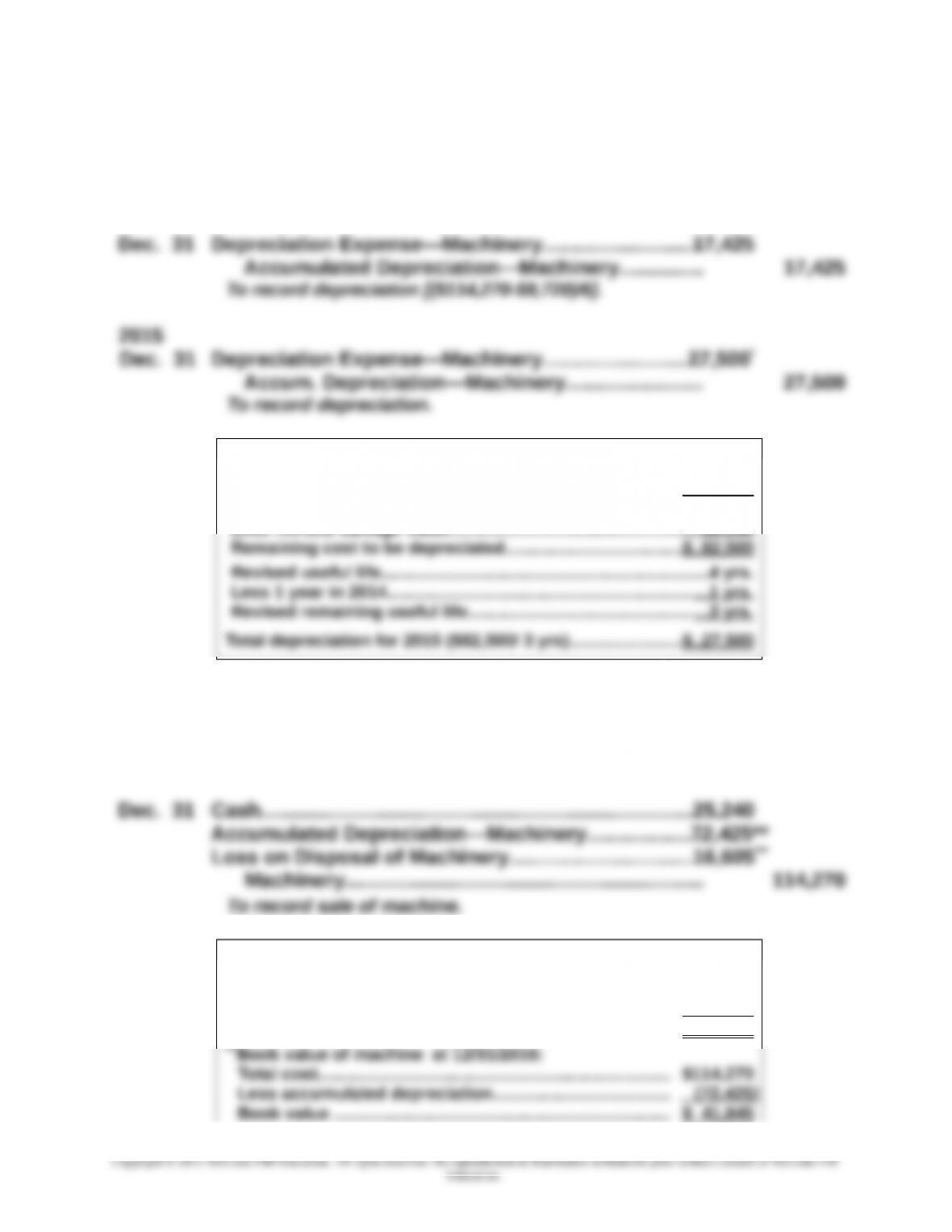

Jan. 1 Machinery…………………………………………………………....114,270

Cash…………………………………………………………….… 114,270

To record costs of machinery ($107,800 +$6,470).

*2015 depreciation:

Total cost……………………………………………………………...………...$114,270

Less accumulated depreciation (from 2014)….……………….….. 17,425

Book value……………………………………………………………………….96,845

Less revised salvage value…………………………………………….... 14,345

2016

Dec. 31 Depreciation Expense—Machinery..……………………..27,500

Accumulated Depreciation—Machinery…………… 27,500

To record depreciation.

**Accumulated depreciation on machine at 12/31/2016:

2014………………………………………………………………………. $ 17,425

2015………………………………………………………………………. 27,500

2016………………………………………………………………………. 27,500

Total…………………………………………………..………..……….. $ 72,425

10-585

Chapter 10 – Plant Assets, Natural Resources, and Intangibles

10-586

Chapter 10 – Plant Assets, Natural Resources, and Intangibles

Problem 10-6B (20 minutes)

1.

Jan. 1 Machinery………………………………..………………………. 150,000

Cash………………………………..…………………………. 150,000

To record machinery costs.

2. a. First year

Dec. 31 Depreciation Expense—Machinery..……………………..20,000

Accumulated Depreciation—Machinery…………… 20,000

To record depreciation [($158,110-$18,110)/7 =

$20,000].

b. Sixth year

3. Accumulated depreciation at the date of disposal

First six years’ depreciation (6 x $20,000)………………….$120,000

Book value at the date of disposal

Original total cost……….………..……………..…..….…..…..….$158,110

Accumulated depreciation…………….……….……….…..…... (120,000)

Total……….……….………..………..……….………..………………...$ 38,110

c. Destroyed in fire and collected $25,000 cash from insurance

Dec. 31 Cash………………………………………………………………….…25,000

Loss from Fire………………………….………………………….13,110

10-587

10-588

Chapter 10 – Plant Assets, Natural Resources, and Intangibles

Problem 10-7B (20 minutes)

a.

Feb. 19 Mineral Deposit…………………………………………………....5,400,000

Cash…………………………………………………………….… 5,400,000

To record purchase of mineral deposit.

b.

c.

Dec. 31 Depletion Expense—Mineral Deposit………………..…..342,900

Accum. Depletion—Mineral Deposit……………..…. 342,900

To record depletion [$5,400,000/

4,000,000 tons = $1.35 per ton.

254,000 tons x $1.35 = $342,900].

Analysis Component

Similarities—Amortization, depletion, and depreciation are similar in that

they are all methods of allocating costs of long-term assets to the periods

that benefit from their use.

10-589

Chapter 10 – Plant Assets, Natural Resources, and Intangibles

Problem 10-8B (20 minutes)

1.

2015 (a)

Jan. 1 Leasehold………………………………………………………….…40,000

Cash…………………………………………………………….… 40,000

To record payment for sublease.

(b)

2.

2015 (a)

Dec. 31 Rent Expense……………………………………………………….8,000

Accumulated Amortization—Leasehold…………… 8,000

To record leasehold amortization ($40,000/5).

(b)

10-590