Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

Exercise 10-3 (20 minutes)

Purchase price........................................................... $375,280

Allocation of total cost

Appraised

Value

Percent

of Total

Applying %

to Cost

Apportioned

Cost

Land..............................$157,040 40% $395,380 x .40 $158,152

Journal entry

Land........................................................................ 158,152

Land Improvements............................................... 59,307

Exercise 10-4 (10 minutes)

Exercise 10-5 (10 minutes)

Units-of-production

10-581

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

Exercise 10-6 (15 minutes)

Double-declining-balance

Double-declining-balance rate = (100% / 10 years) x 2 = 20% per year

Exercise 10-7 (15 minutes)

Year Annual Depreciation Year-End Book Value

2015........ $ 32,250 $121,750

Exercise 10-8 (20 minutes)

Double-declining-balance depreciation

Year

Beginning-Year

Book Value

Depreciation

Rate

Annual

Depreciation

Year-End

Book Value

2015....... $154,000 50% $ 77,000 $77,000

10-582

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

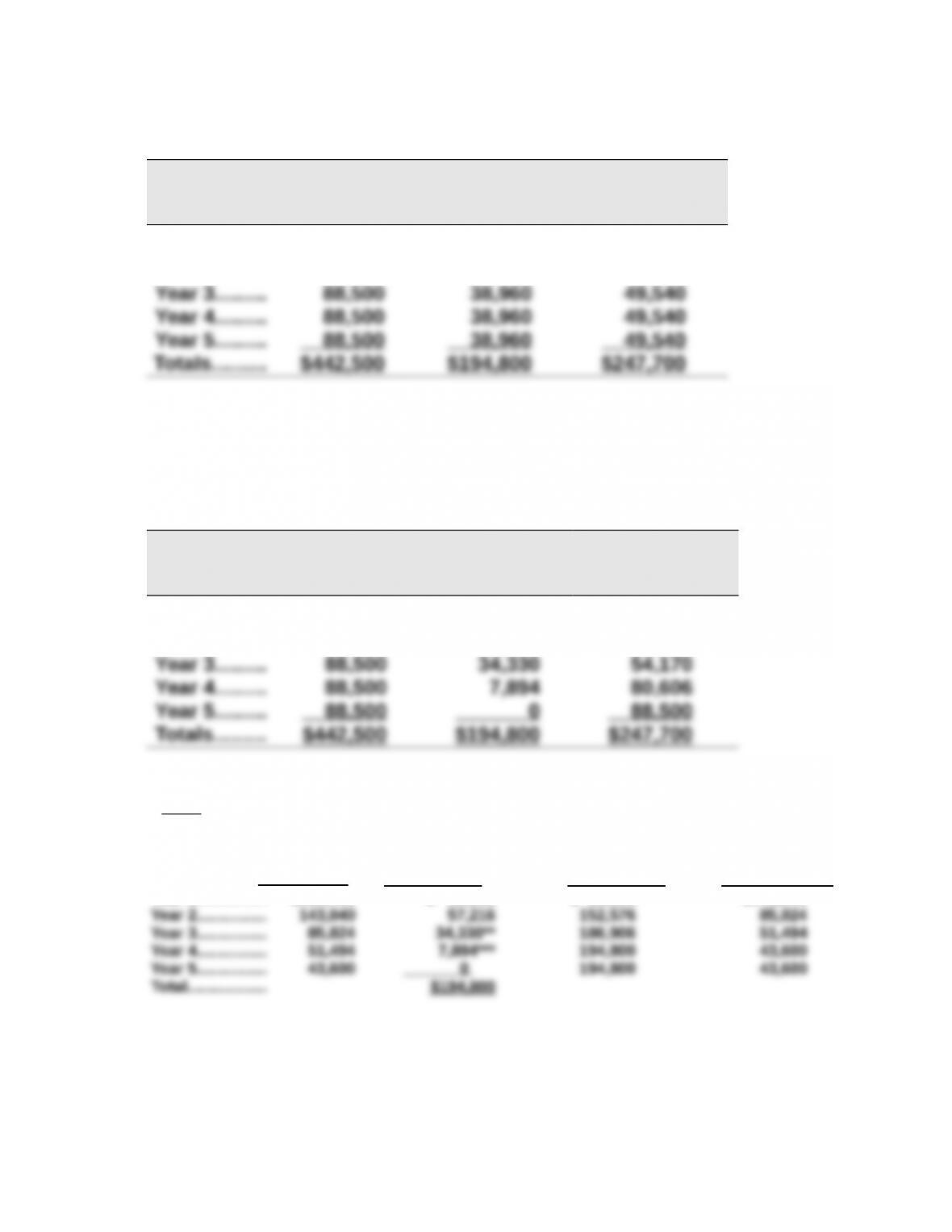

Exercise 10-9 (30 minutes)

Straight-line depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

Year 1......... $ 88,500 $ 38,960 $ 49,540

Year 2......... 88,500 38,960 49,540

*($238,400 - $43,600) / 5 years = $38,960

Exercise 10-10 (30 minutes)

Double-declining-balance depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

Year 1........ $ 88,500 $ 95,360 $ (6,860)

Year 2......... 88,500 57,216 31,284

Supporting calculations for depreciation expense

*Note: (100% / 5 years) x 2 = 40% depreciation rate

Beginning

Book

Value

Annual

Depreciation

(40% of

Book Value)

Accumulated

Depreciation at

the End of the

Year

Ending Book Value

($238,400 Cost Less

Accumulated

Depreciation)

Year 1................ $238,400 $ 95,360 $ 95,360 $143,040

** rounded

***Must not use $20,598; instead take only enough depreciation in Year 4 to reduce book value

to the $43,600 salvage value.

10-583

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

Exercise 10-11 (10 minutes)

Straight-line depreciation for 2014

Straight-line depreciation for 2015

Exercise 10-12 (15 minutes)

Double-declining-balance depreciation for 2014 and 2015:

Alternate calculation

Exercise 10-13 (15 minutes)

1. Original cost of machine...........................................................$ 23,860

Less two years' accumulated depreciation

10-584

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

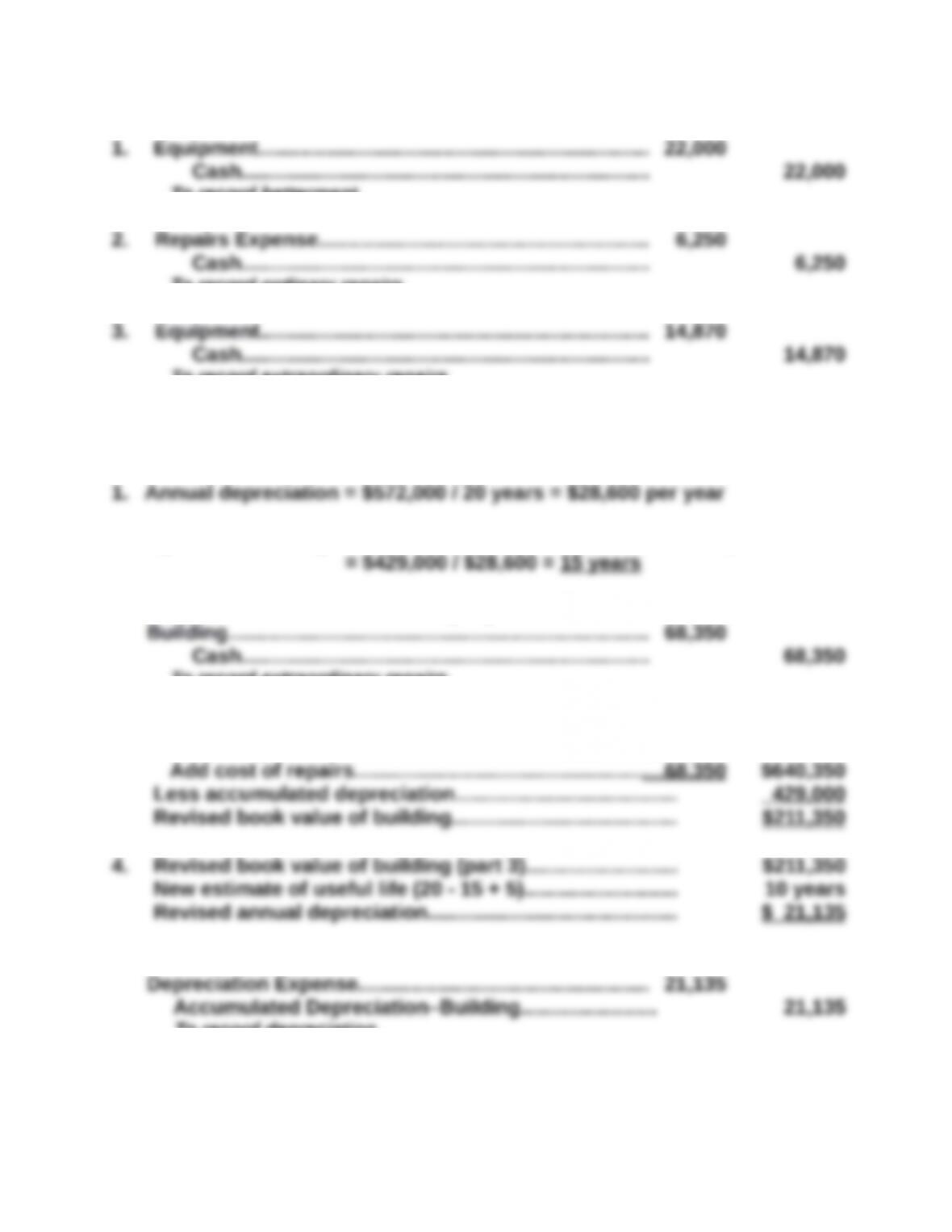

Exercise 10-14 (15 minutes)

To record betterment.

To record ordinary repairs.

To record extraordinary repairs.

Exercise 10-15 (25 minutes)

Age of the building = Accumulated depreciation / Annual depreciation

2. Entry to record the extraordinary repairs

To record extraordinary repairs.

3. Cost of building

Before repairs................................................................$572,000

Journal entry

To record depreciation.

10-585

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

Exercise 10-16 (20 minutes)

1. Disposed at no value

To record disposal of milling machine.

2. Sold for $35,000 cash

To record cash sale of milling machine.

3. Sold for $68,000 cash

To record cash sale of milling machine.

4. Sold for $80,000 cash

Jan. 3 Cash.............................................................................80,000

To record cash sale of milling machine.

10-586

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

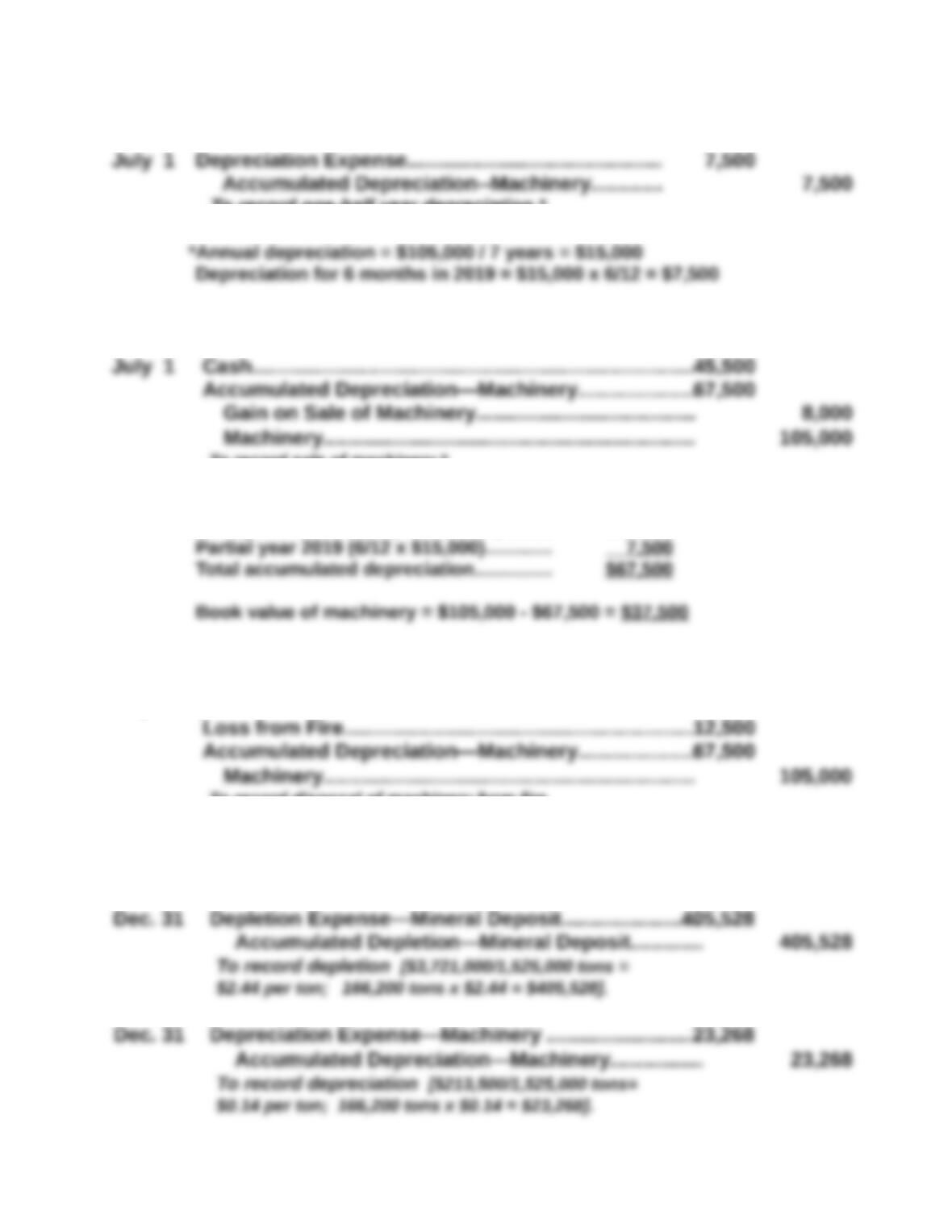

Exercise 10-17 (25 minutes)

2019

To record one-half year depreciation.*

1. Sold for $45,500 cash

To record sale of machinery.*

*Total accumulated depreciation at date of disposal:

Four years 2015-2018 (4 x $15,000)......... $60,000

2. Destroyed by fire with $25,000 cash insurance settlement

July 1 Cash.............................................................................25,000

To record disposal of machinery from fire.

Exercise 10-18 (10 minutes)

10-587

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

Exercise 10-19 (10 minutes)

Cash........................................................................

418,000

00

To record purchase of copyright.

To record amortization of copyright

[$418,000 / 10 years].

Exercise 10-20 (10 minutes)

1. Goodwill = $2,500,000 - $1,800,000 = $700,000

2. Goodwill is not amortized. Instead, Robinson must test the value of the

Goodwill each year, and if the value is impaired, it must be written down.

3. Goodwill is only recorded when it is purchased. Goodwill is not

recorded by the company that has created it.

Exercise 10-21 (15 minutes)

1. $7,358 million cash for property and equipment

2. $2,781 million for

depreciation and amortization

3. $13,679 million cash used in investing activities

Exercise 10-22 (15 minutes)

Analysis comments. Based on these calculations, Look turned its assets over

10-588

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

Exercise 10-23A (15 minutes)

1. Book value of the old tractor ($96,000 - $52,500)..........................$ 43,500

2. Loss on the exchange

3. Debit to new Tractor account

Alternatively, answers can be taken from the following journal entry:

Tractor (new)*.................................................................................. 112,000

Exercise 10-24A (25 minutes)

1. Sold for $18,250 cash

Jan. 2 Cash.............................................................................18,250

To record cash sale of machine.

2. $25,000 trade-in allowance exceeds book value; but no gain is

recognized on an asset exchange that lacks commercial substance

($5,625 gain is ‘buried’ in the cost of the new machinery)

Jan. 2 Machinery (new)*........................................................54,575

To record asset exchange.

3. $15,000 trade-in allowance is less than book value (yielding a loss)

Jan. 2 Machinery (new)..........................................................60,200

10-589

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Chapter 10 - Plant Assets, Natural Resources, and Intangibles

10-590

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.