Appendix C – Activity-Based Costing

Problem C-2B (concluded)

4. Mixing & Cooking ($4,500 + $11,250)/1,500 MH $10.50/MH

Product testing $112,500/600 batches $187.50/batch

Machine calibration $250,000/400 production runs $625/run

Extra Fine Family Style

Mixing & cooking 500 MH x $10.50…….......….. $ 5,250 1,000 MH x $10.50…………. $ 10,500

Product testing 200 batch. X $187.50……..... 37,500 400 batch. x $187.50……… 75,000

Mach. calibration 200 runs x $625………..…..... 125,000 200 runs x $625…............. 125,000

Labeling & defects 20,000 cases x $0.15……..... 3,000 100,000 cases x $0.15.... 15,000

Recipe formulation 30 groups x $2,000............. 60,000 15 groups x $2,000..…...... 30,000

Heat, light, & water 500 MH x $18…………......….. 9,000 1,000 MH x $18……………... 18,000

5. Extra Fine Family Style

Selling price per case $18.00 $9.00

Using ABC, the Extra Fine salsa is not profitable, but the Family Style is

the plantwide rate was used for assigning cost.

6. Departmental overhead rates would be a modest improvement over the

plantwide rate because they could show differences across

AppC-1999

Appendix C – Activity-Based Costing

Problem C-3B (25 minutes)

1. The major costs of making the boxes are designing the boxes, setting

up machines to make the right cuts, cutting the cardboard, printing

2. Lakeside has taken on more custom-made boxes for smaller-volume

customers.

3. Yes. Lakeside’s old customers bought the same type of boxes over

and over, so the design costs were spread over many units. The new

4. Possibly. If ABC had been used rather than a volume-based system,

Lakeside would have realized that small customers who want

custom-designed and custom-made boxes require different activities

the activity was required for all orders.

5. ABC gives managers information about the activities and the costs of

AppC-1999

Appendix C – Activity-Based Costing

Problem C-4B (45 minutes)

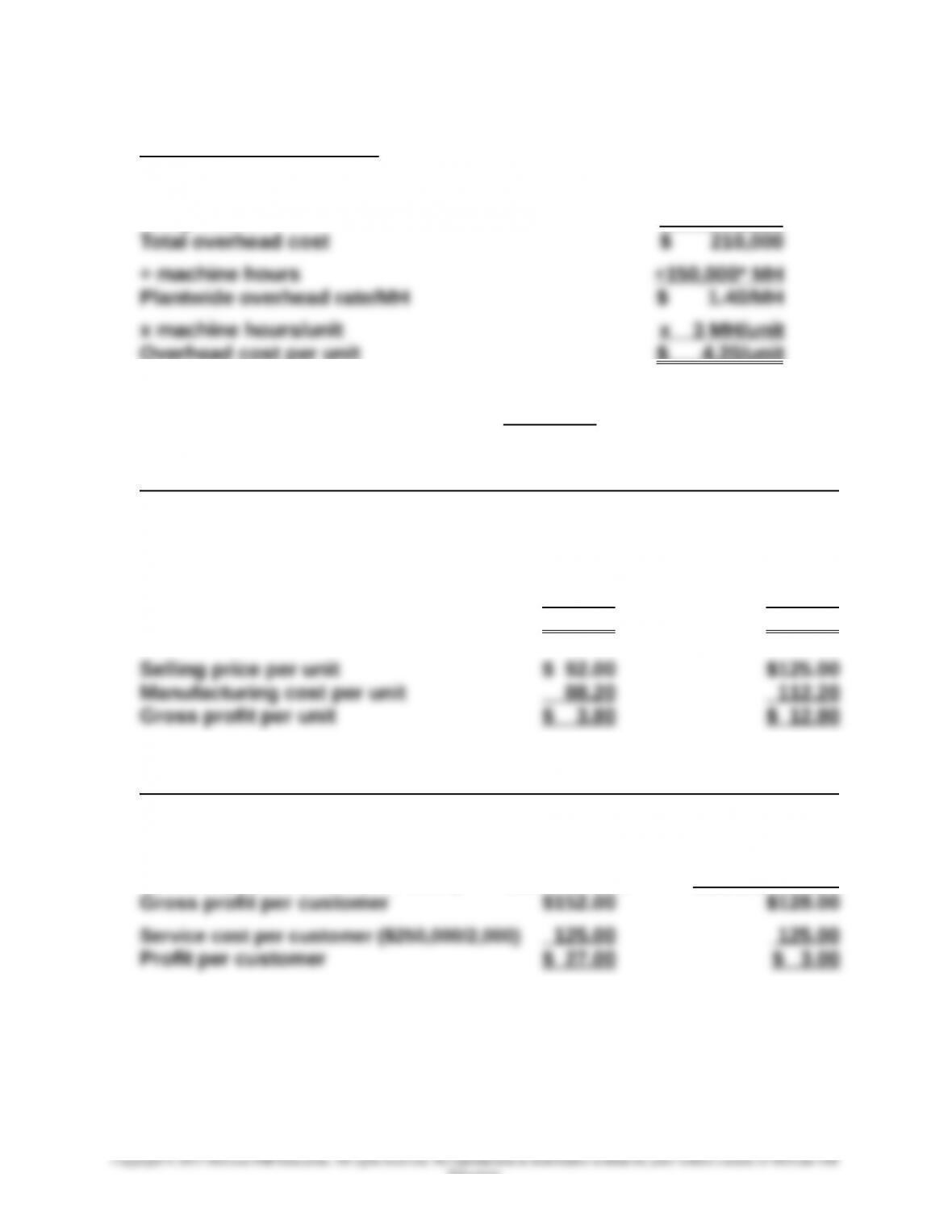

1. Plantwide overhead rate:

Engineering support $ 56,250

Electricity 112,500

Setup costs 41,250

Overhead cost per unit $ 4.20/unit

*Standard: 40,000 units x 3 MH/unit = 120,000 MH

Deluxe: 10,000 units x 3 MH/unit = 30,000 MH

Total machine hours 150,000 MH

Standard Deluxe

Direct materials cost per unit $ 4.00 $ 8.00

Direct labor cost per unit

Standard: 4 DLH x $20/DLH 80.00

Deluxe: 5 DLH x $20/DLH 100.00

Overhead cost per unit 4.20 4.20

Manufacturing cost per unit $ 88.20 $112.20

2.

Profit per customer Standard Deluxe

Gross profit per unit $3.80 $ 12.80

x units per customer

Standard (40,000 units/1,000 cust.) x 40 units/cust.

Deluxe (10,000 units/1,000 cust.) ___________ x 10 units/cust.

This comparison shows that gross profit per customer exceeds service

cost per customer for both products. Thus, both products appear to be

profitable.

AppC-1999

Education.

Appendix C – Activity-Based Costing

Problem C-4B (concluded)

3. Eng. support $56,250/(50 + 25) modifications = $750/modification

Electricity $112,500/150,000* machine hours = $0.75/machine hour

Setup $41,250/(175 + 75) batches = $165/batch

* From part 1

Standard Deluxe

Engineering 50 mods. x $750 $37,500 25 mods. x $750 $ 18,750

Electricity 120,000 MH x $0.75 90,000 30,000 MH x $0.75 22,500

Setups 175 batches x $165 28,875 75 batches x $165 12,375

Total overhead $156,375 $53,625

÷ units ÷ 40,000 ÷ 10,000

Gross profit/unit $ 4.09 $ 11.64

4. Standard Deluxe

Gross profit per unit $ 4.09 $ 11.64

x units per customer* x 40 units x 10 units

Gross profit per customer $ 163.60 $ 116.40

*From Part 2

This analysis shows that the Standard product is in fact profitable, but

the high cost of production and service for the small volume of the

Deluxe product is unprofitable.

5. ABC gives more appropriate information to managers because it

identifies the resources consumed by each product line, and assigns

AppC-1999

Appendix C – Activity-Based Costing

Problem C-5B (30 minutes)

1. Components $495,000/(450,000 + 100,000) parts $0.90/part

Assembly labor $244,800/(15,000 + 2,000) DLH $14.40/DLH

Maintenance $100,800/(5,000 + 2,000) MH $14.40/MH

Total cartons 1,900 cartons

Fun with Fractions Count Calculus

Components 450,000 parts x$0.90……..... $ 405,000 100,000 parts x $0.90........ $ 90,000

Assembly 15,000 DLH x$14.40……...... 216,000 2,000 DLH x $14.40…...…... 28,800

Maintenance 5,000 MH x$14.40…….…...... 72,000 2,000 MH x $14.40………….. 28,800

2. Cost per unit Fun with Fractions Count Calculus

Total manufacturing cost $1,240,200 $275,760

*Rounded

3. Selling price of Count Calculus $59.95

4. Since the cost associated with Fun with Fractions is $8.27, the price

should be at least $8.27 to cover these costs. A higher price would

make the product profitable.

AppC-1999

Appendix C – Activity-Based Costing

Problem C-6B (45 minutes)

Part 1

Determination of cost per driver unit

Cost Center Cost Driver Cost per Driver

Professional salaries...........$600,000 10,000 hours $60 per hour

Part 2

Allocation of costs to the landscaping departments using ABC

GENERAL LANDSCAPING

Cost

Driver

Cost per

Driver Unit

Allocated

Cost

Professional salaries.............2,500 hours $60 per hr. $150,000

Customer supplies..…………...

600 customers $187.50 per customer 112,500

Average cost per customer…………………………..………………………. $ 597.50

CUSTOM DESIGN LANDSCAPING

Cost

Driver

Cost per

Driver Unit

Allocated

Cost

Professional salaries.............7,500 hours $60 per hr. $ 450,000

Customer supplies..…………...

200 customers $187.50 per customer 37,500

Part 3

If costs were allocated on the number of customers, the average cost of

general landscaping would increase. Since 75% of the customers are general

AppC-1999

Appendix C – Activity-Based Costing

SERIAL PROBLEM — SP C

1. Direct materials $2,500

2. Setting up machines $20,000/25 batches

$800/batch

Inspecting components $7,500/5,000 parts $1.50/part

Providing utilities $10,000/5,000 machine hours $2.00/MH

Inspecting: 400 parts @$1.50/part……….……………. 600

Utilities: 600 MH @$2.00/MH..…………………….... 1,200 3,400

Total manufacturing cost………………………………….... $9,400

3. ABC gives a better representation of the cost of producing Job 6.15

because it reflects the resources consumed in the production

AppC-1999