Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Appendix C - Activity-Based Costing

Exercise C-5 (continued)

Part 3

Allocation of costs to the general surgery department using ABC

GENERAL SURGERY

Cost

Driver

Cost per

Driver Unit

Allocated

Cost

Professional salaries............. 2,500 hours $160 per hr. $400,000

Patient services & supplies.......400 patients $45 per patient 18,000

Exercise C-6 (30 minutes)

Calculation of predetermined overhead rates to apply ABC

Overhead Cost

Category (Activity

Cost Pool) Total

Cost

Total Amount

of Cost Driver Predetermined Overhead Rate

1. Assignment of overhead costs to the two products using ABC

Rounded edge

Cost

Driver

Cost per

Driver Unit Assigned Cost

Supervision............................. $12,200 15% $ 1,830

Machinery depreciation......... 500 hours $ 28.30 14,150

Squared edge

Cost

Driver

Cost per

Driver Unit Assigned Cost

Supervision............................. $23,800 15% $ 3,570

Machinery depreciation.........

1,500 hours $ 28.30 42,450

Line preparation.....................210 setups $184.00 38,640

Total overhead assigned....... $84,660

AppC-1999

2. Average cost per foot of the two products

Rounded edge Squared edge

Direct materials ........................... $19,000 $ 43,200

Direct labor .................................. 12,200 23,800

Overhead (using ABC) ................ 23,340 84,660

*Rounded

3. Using ABC, the average cost of rounded edge shelves declines and the

average cost of squared edge shelves increases. Under the current

allocation method, the rounded edge shelving was allocated 34% of all of

PROBLEM SET A

Problem C-1A (40 minutes)

1. Grinding & Polishing ($320,000+$135,000)/13,000 MH $35/MH

Product modification $600,000/1,500 Eng. Hrs. $400/Eng. Hr.

2.

Job 3175 Job 4286

Grinding & polishing 550 MH x $35.................... $19,250 5,500 MH x $35................... $192,500

Product modification 26 Eng.Hr x $400.............. 10,400 32 Eng. Hr. x $400............... 12,800

AppC-1999

3. Job 3175 Job 4286

Total overhead cost of job $74,650 $383,425

4. Plantwide rate

Grinding............................................................................... $ 320,000

Polishing.............................................................................. 135,000

Product modification.......................................................... 600,000

AppC-1999

Appendix C - Activity-Based Costing

Problem C-1A (concluded)

Job 3175 Job 4286

Overhead

500 DLH x $106.47 $ 53,235

4,375 DLH x $106.47 $ 465,806

*Rounded

5. Average overhead cost

Job 3175 Job 4286

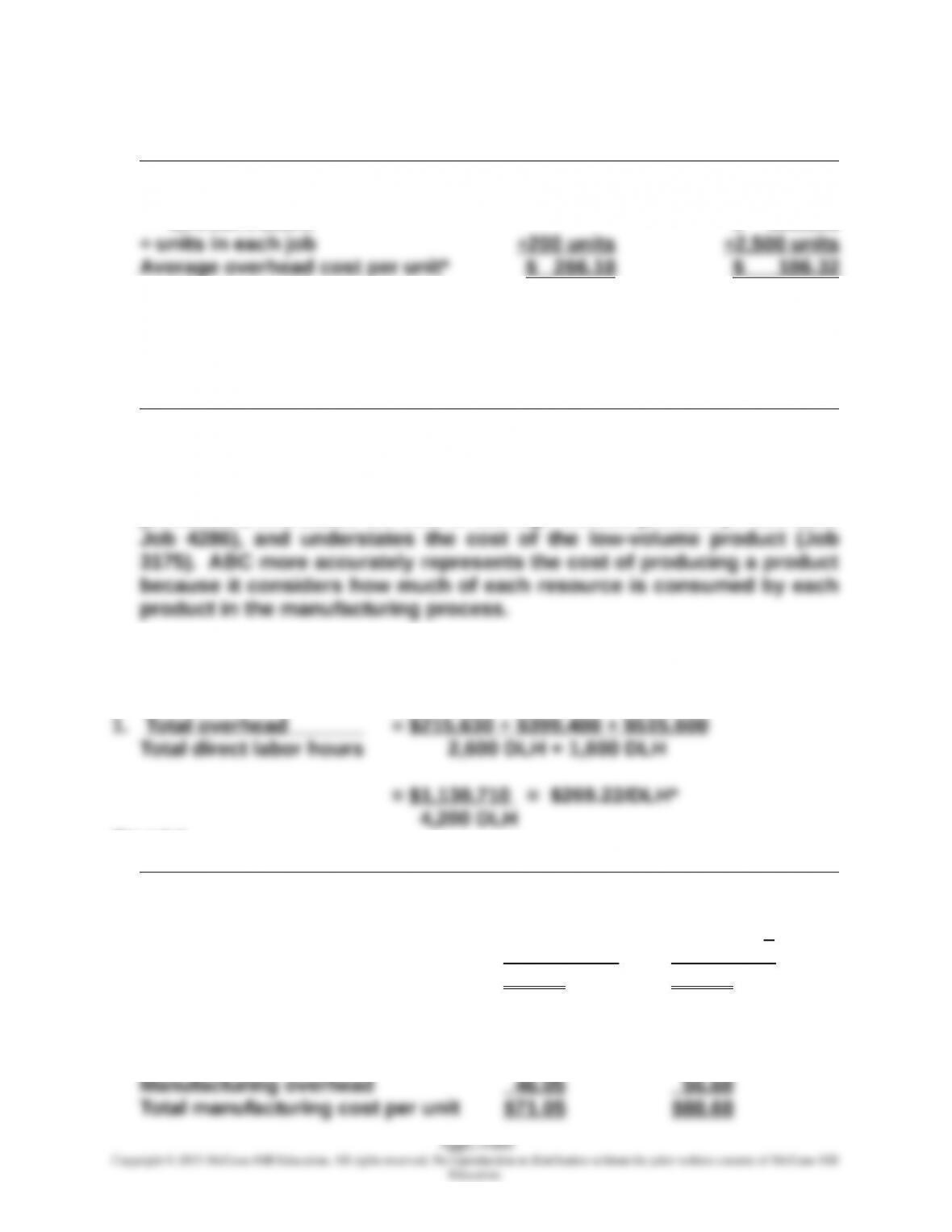

Using ABC $ 373.25 $ 153.37

Using plantwide rate $ 266.18 $ 186.32

The plantwide rate, which is closely associated with the volume of

production, overstates the cost of the high-volume product (in this case

Problem C-2A (50 minutes)

*Rounded

Pup Tent Pop-Up Tent

Overhead cost by product line

Pup: 2,600 DLH @ $269.22/DLH $699,972*

Pop-Up: 1,600 DLH @ $269.22/DLH $430,752*

÷ Number of units produced 15,200 units 7,600 units

Overhead cost per unit $46.05 $56.68

*($699,972 + 430,752 = $1,130,724; $14 rounding error)

2. Total manufacturing cost per unit:

Direct materials and direct labor $25.00 $32.00

Appendix C - Activity-Based Costing

AppC-1999

Appendix C - Activity-Based Costing

Problem C-2A (continued)

3. Gross profit per unit

Selling price per unit $65.00 $200.00

Gross profit (loss) per unit $ (6.05) $111.32

4. Pattern alignment $64,400/560 batches $115/batch

Cutting $50,430/12,300 machine hours $4.10/MH

Moving product $100,800/2,400 moves $42/move

Pup Tent Pop-Up Tent

Pattern alignment 140 batches x $115..........$ 16,100 420 batches x $115...........$ 48,300

Cutting 7,000 MH x $4.10..............28,700 5,300 MH x $4.10...............21,730

Moving product 800 moves x $42..............33,600 1,600 moves x $42............67,200

Sewing 2,600 DLH x $78...............202,800 1,600 DLH x $78................124,800

Inspecting 240 insp. x $40................. 9,600 360 insp. x $40..................14,400

÷ units ÷ 15,200 ÷ 7,600

Overhead per unit (rounded) $ 33.46 $ 81.87

DM and DL per unit 25.00 32.00

Mfg. cost per unit $ 58.46 $ 113.87

AppC-1999

Appendix C - Activity-Based Costing

Problem C-2A (concluded)

5.

Pup Tent Pop-Up Tent

Selling price $65.00 $200.00

Both product lines are profitable without any cost cutting. The ABC cost

assignment method more accurately reflects the costs associated with

overhead rate bases cost assignment on volume-related factors.

6. Departmental overhead rates based on direct labor hours and machine

hours are still volume-based measures and would not improve the

AppC-1999

Appendix C - Activity-Based Costing

Problem C-3A (25 minutes)

1. When companies experience strong price pressure on their high-

volume, commodity-type products, they should be concerned. Many

managers will blame competitive price cutting on attempts by

2. The company may be charging less for its low-volume, custom-order

products than the competitors because the company is using a volume-

based costing system, which understates the true cost of producing

3. While prices are really set in the marketplace based on customer

demand and supply of the product, companies still look at costs to

determine the price they would like to get if they could affect market

4. Custom-order furniture requires handling special fabrics, buying in

smaller quantities (which may be more expensive than buying “in bulk”),

5. In addition to obtaining a more accurate picture of the costs of making

various products, activity based costing also gives information about

the cost of the activities that are performed. Managers may be surprised

AppC-1999

Appendix C - Activity-Based Costing

Problem C-4A (45 minutes)

1. Plantwide overhead rate:

Engineering support $ 24,500

Electricity 34,000

÷ 6,200* direct labor hours = $17.90/DLH

* Product A 10,000 units x 0.3 DLH/unit = 3,000 DLH

Product B 2,000 units x 1.6 DLH/unit = 3,200 DLH

6,200 DLH

Product A Product B

Direct materials per unit $15.00 $24.00

Direct labor per unit

A: 0.3 DLH/unit @ $20/DLH 6.00

B: 1.6 DLH/unit @ $20/DLH 32.00

Product A Product B

Selling price per unit...................... $30.00 $120.00

Manufacturing cost per unit.......... 26.37 84.64

Gross profit per unit....................... $ 3.63 $ 35.36

AppC-1999