Appendix C – Activity-Based Costing

Exercise C-6 (30 minutes)

Calculation of predetermined overhead rates to apply ABC

Overhead Cost

Category (Activity

Cost Pool) Total

Cost

Total Amount

of Cost Driver Predetermined Overhead Rate

Supervision…………………………$ 5,400 $36,000 15% of direct labor cost

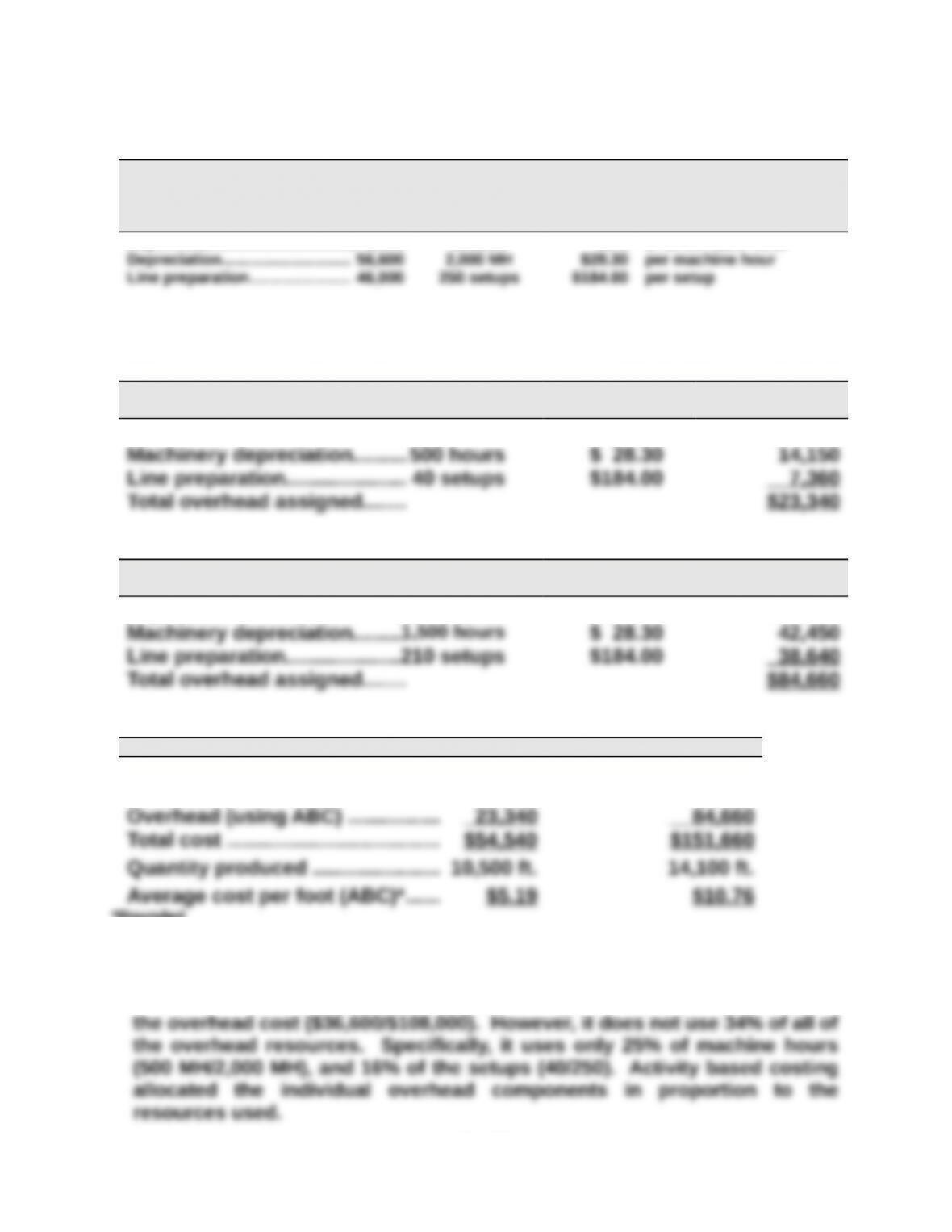

1. Assignment of overhead costs to the two products using ABC

Rounded edge

Cost

Driver

Cost per

Driver Unit Assigned Cost

Supervision………………………. $12,200 15% $ 1,830

Squared edge

Cost

Driver

Cost per

Driver Unit Assigned Cost

Supervision………………………. $23,800 15% $ 3,570

2. Average cost per foot of the two products

Rounded edge Squared edge

Direct materials ……………………… $19,000 $ 43,200

Direct labor …………………………… 12,200 23,800

*Rounded

3. Using ABC, the average cost of rounded edge shelves declines and the

average cost of squared edge shelves increases. Under the current

allocation method, the rounded edge shelving was allocated 34% of all of

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

PROBLEM SET A

Problem C-1A (40 minutes)

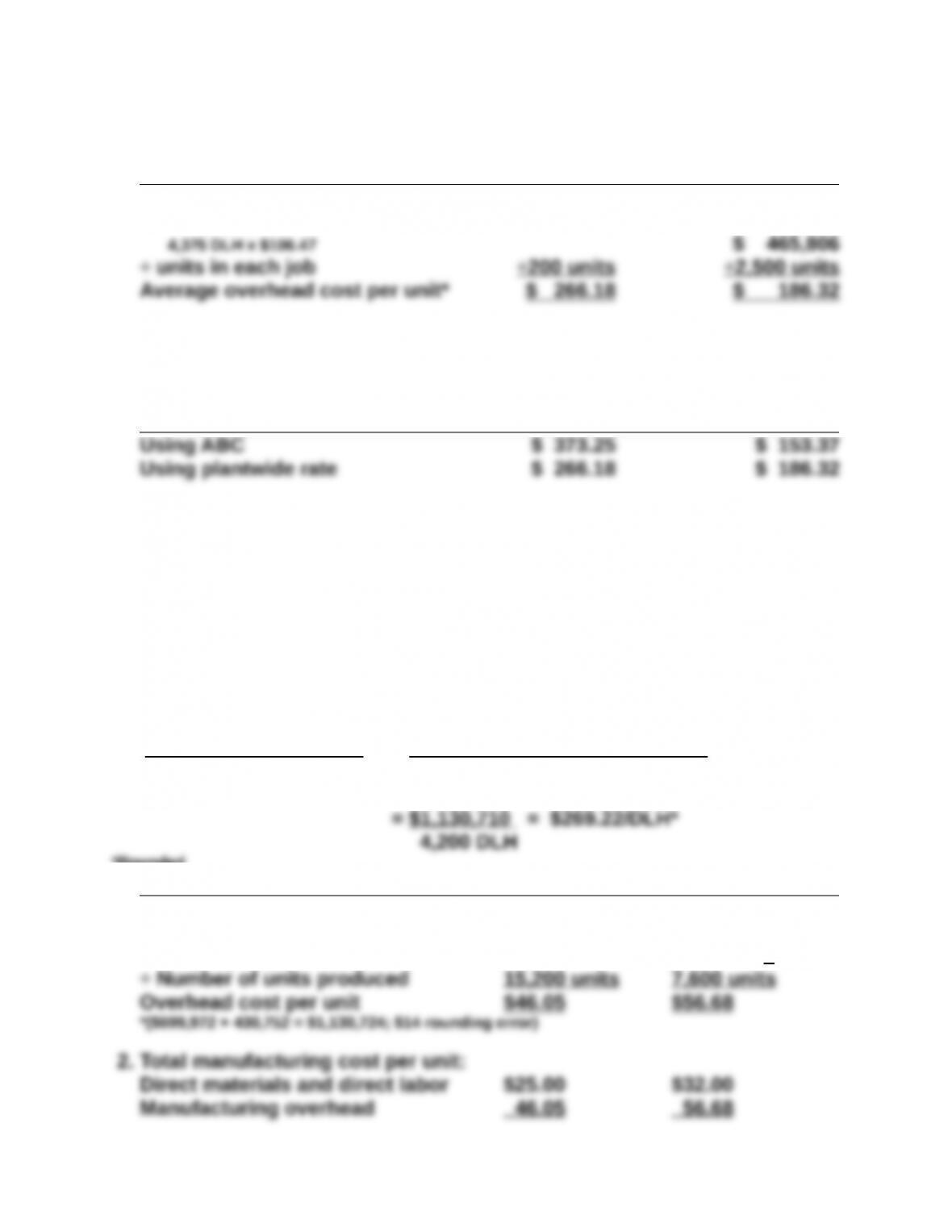

1. Grinding & Polishing ($320,000+$135,000)/13,000 MH $35/MH

2.

Job 3175 Job 4286

Grinding & polishing 550 MH x $35……………….. $19,250 5,500 MH x $35………………. $192,500

3. Job 3175 Job 4286

Total overhead cost of job $74,650 $383,425

4. Plantwide rate

Grinding………………………………………………………………….. $ 320,000

Polishing…………………………………………………………………. 135,000

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Per DLH (rounded)……………………………………………………. $106.47/DLH

Problem C-1A (concluded)

Job 3175 Job 4286

Overhead

500 DLH x $106.47 $ 53,235

*Rounded

5. Average overhead cost

Job 3175 Job 4286

The plantwide rate, which is closely associated with the volume of

production, overstates the cost of the high-volume product (in this case

Job 4286), and understates the cost of the low-volume product (Job

3175). ABC more accurately represents the cost of producing a product

because it considers how much of each resource is consumed by each

product in the manufacturing process.

Problem C-2A (50 minutes)

1. Total overhead = $215,630 + $399,480 + $515,600

Total direct labor hours 2,600 DLH + 1,600 DLH

*Rounded

Pup Tent Pop-Up Tent

Overhead cost by product line

Pup: 2,600 DLH @ $269.22/DLH $699,972*

Pop-Up: 1,600 DLH @ $269.22/DLH $430,752*

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

It appears that the Pup Tent is not profitable and management may

decide to eliminate this product line if it cannot reduce cost (or raise the

selling price) to generate a profit.

4. Pattern alignment $64,400/560 batches $115/batch

Cutting $50,430/12,300 machine hours $4.10/MH

Moving product $100,800/2,400 moves $42/move

Pup Tent Pop-Up Tent

Pattern alignment 140 batches x $115……….$ 16,100 420 batches x $115………..$ 48,300

Cutting 7,000 MH x $4.10…………..28,700 5,300 MH x $4.10……………21,730

Moving product 800 moves x $42…………..33,600 1,600 moves x $42…………67,200

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Problem C-2A (concluded)

5.

Pup Tent Pop-Up Tent

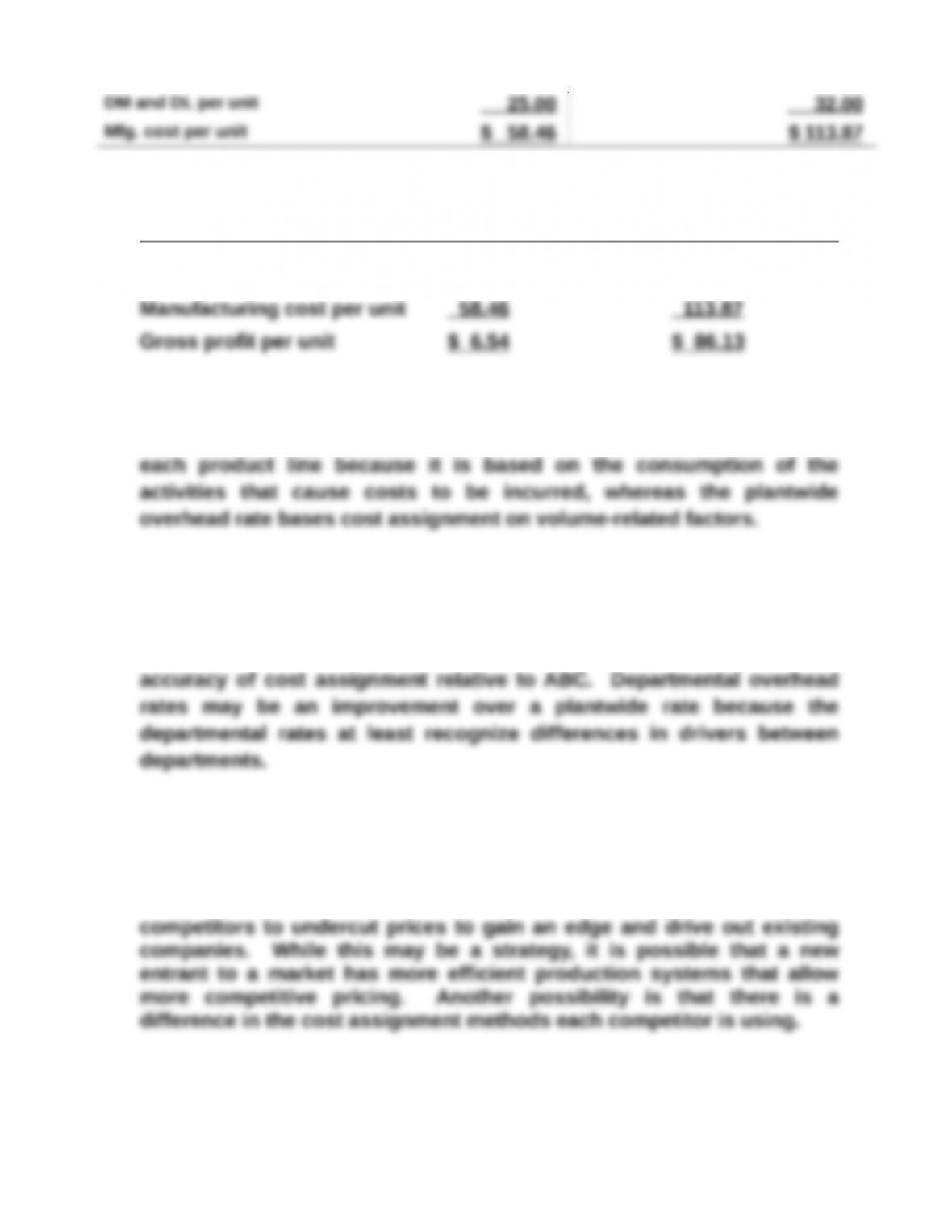

Selling price $65.00 $200.00

Both product lines are profitable without any cost cutting. The ABC cost

assignment method more accurately reflects the costs associated with

6. Departmental overhead rates based on direct labor hours and machine

hours are still volume-based measures and would not improve the

Problem C-3A (25 minutes)

1. When companies experience strong price pressure on their

high-volume, commodity-type products, they should be concerned.

Many managers will blame competitive price cutting on attempts by

2. The company may be charging less for its low-volume, custom-order

products than the competitors because the company is using a

volume-based costing system, which understates the true cost of

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

3. While prices are really set in the marketplace based on customer

demand and supply of the product, companies still look at costs to

4. Custom-order furniture requires handling special fabrics, buying in

smaller quantities (which may be more expensive than buying “in bulk”),

5. In addition to obtaining a more accurate picture of the costs of making

various products, activity based costing also gives information about

the cost of the activities that are performed. Managers may be surprised

Problem C-4A (45 minutes)

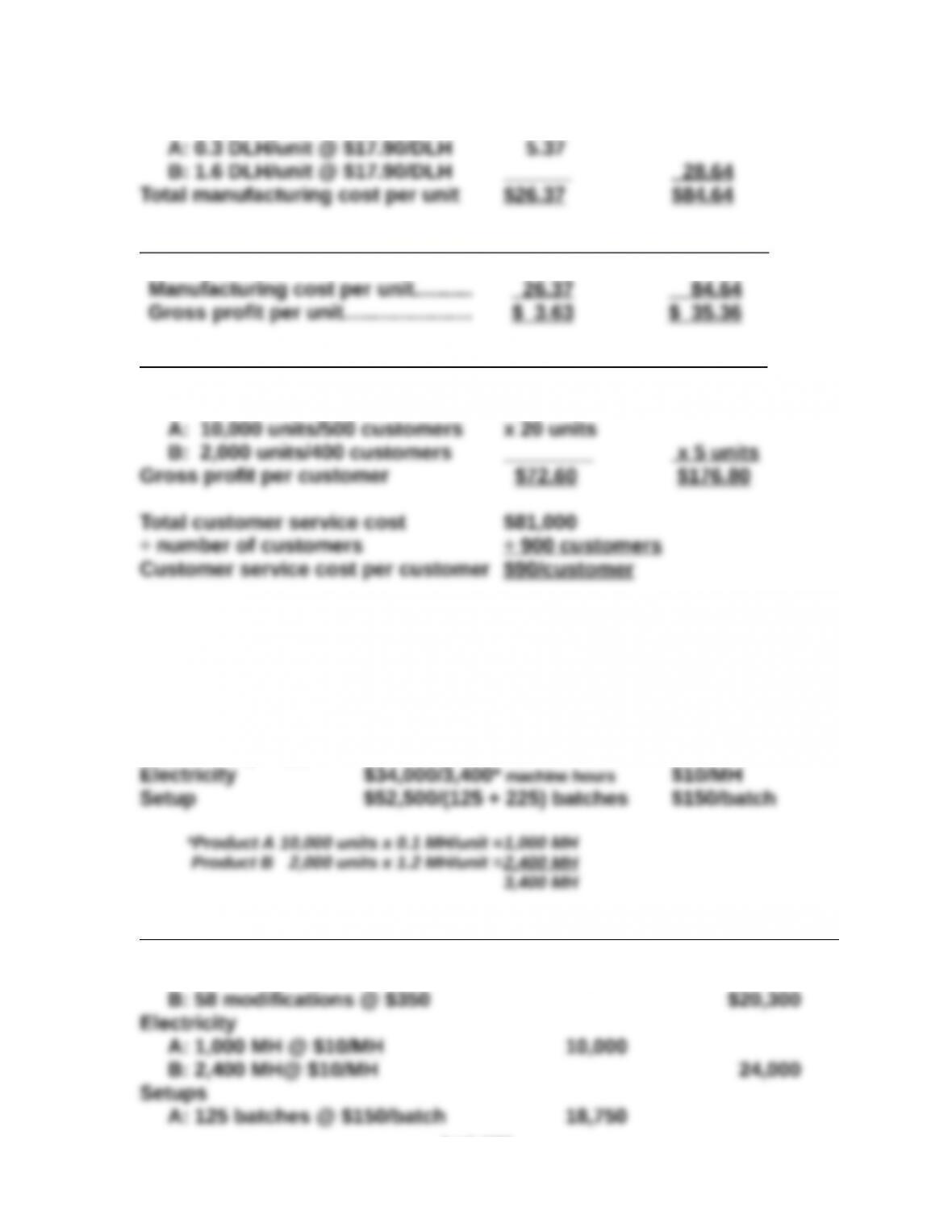

1. Plantwide overhead rate:

Engineering support $ 24,500

* Product A 10,000 units x 0.3 DLH/unit = 3,000 DLH

Product A Product B

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

B: 1.6 DLH/unit @ $20/DLH 32.00

Manufacturing overhead per unit

Product A Product B

Selling price per unit………………… $30.00 $120.00

2. Product A Product B

Gross profit per unit $ 3.63 $35.36

x units purchased per customer

We see that the gross profit per customer from Product A ($72.60) is not

adequate to cover the cost of providing service to customers of this

product ($90). It appears that the company is incurring a loss of $17.40

($72.60 – $90) associated with each customer of Product A.

Problem C-4A (concluded)

3. Engineering Support $24,500/(12 + 58) modifications $350/modification

Product A Product B

Engineering support

A: 12 modifications @ $350 $ 4,200

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

B: 225 batches @ $150/batch ______ 33,750

Total overhead cost by product line $32,950 $78,050

4. Product A Product B

Gross profit per unit (from above) $5.70 $24.97

The gross profit per customer is adequate to cover the cost of providing

customer service under ABC for both Product A and Product B.

Problem C-4A (concluded)

5. Activity based costing gives better information than the plantwide rate

based on volume-related measures because ABC associates the cost of

the various activities that must be performed in order to make, sell, and

Problem C-5A (25 minutes)

1. Liquid materials $2,304/(1,400 + 37,000) gallons $0.06/gallon

Dry materials $6,941/(620 + 12,000) pounds $0.55/pound

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

PowerPunch SlimLife

Liquid material 1,400 gal x $0.06……………… $ 84 37,000 gal x $0.06……….$ 2,220

Dry material 620 pounds x $0.55………… 341 12,000 pounds x $0.55. . 6,600

2. PowerPunch SlimLife

Total cost of line $19,122 $95,070

*Rounded

Problem C-5A (concluded)

3. For PowerPunch:

4. The price of SlimLife must cover the costs associated with the product,

so the minimum price for this product is $0.53/bottle.

Problem C-6A (45 minutes)

Part 1

Determination of cost per driver unit

Cost Center Cost Driver Cost per Driver

Professional salaries…………………..$2,000,000 10,000 hours $200 per hour

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Part 2

Allocation of cost to the surgical departments using ABC

GENERAL SURGERY

Cost

Driver

Cost per

Driver Unit

Allocated

Cost

Professional salaries…………. 2,500 hours $200 per hr. $ 500,000

Problem C-6A (concluded)

ORTHOPEDIC SURGERY

Cost

Driver

Cost per

Driver Unit

Allocated

Cost

Professional salaries…………. 7,500 hours $200 per hr. $1,500,000

[Note that the sum of the amounts allocated to General Surgery and Orthopedic

Part 3

If all center costs were allocated on the number of patients, the average

cost of general surgery would increase. Since general surgery sees 80% of

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.