Appendix C – Activity-Based Costing

Appendix C

Activity-Based Costing

QUESTIONS

1. Manufacturing overhead costs cannot be directly traced to units of product like

direct materials and direct labor. Assigning overhead costs to units of product

requires some sort of allocation on some “reasonable” basis.

2. In the first stage, service department costs are assigned to operating departments.

In the second stage, a predetermined overhead rate is computed for each operating

department and used to assign overhead to output (or jobs or products).

3. Operating departments are directly involved in manufacturing or selling the products

or services of a business. Service departments support operating departments

through activities such as accounting, payroll, and legal services.

4. Activity-based costing (ABC) is a method for allocating shared costs among

departments or products. It is especially common for overhead allocation. The goal

of ABC is to provide reliable information about costs and their sources. One

advantage of ABC is that it forces managers to examine the behavior of cost drivers

and cost levels, with the result that costs are more likely to be managed effectively.

5. Anything to which costs would be assigned is considered a “cost object.” Common

cost objects are units of product, product lines, departments, activities, and

projects.

6. An activity cost driver is the measure of the activity that causes costs to be incurred.

For instance, the activity driver for the activity “printing checks” might be number of

checks printed.

7. Activity-based costing is typically used when a company produces many different

and complex products or when products are directed at many different types of

customers.

8. Typical activity cost pools include: purchasing, order processing, accounting,

engineering, factory maintenance, and legal services (other answers are possible).

9. In activity-based costing, costs in a cost pool are allocated to output (or jobs or

products) using predetermined overhead rates.

10. While ABC may provide more accurate cost assignments, the additional cost to

implement activity-based costing may not be justified. That is, the value of the

improved accuracy may not result in higher profitability. Like any business decision,

the choice of accounting method depends on weighing the costs against the

benefits.

11. Activity-based costing may be used in any type of organization. The premise of ABC

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

is that activities cause costs. Since all organizations engage in activities, these activities

may be associated with costs they incur. Service enterprises must determine

appropriate fees for the services they provide, so it would be just as appropriate for such

a company to determine the cost of providing those services as it is for a manufacturer

to determine the cost of making a product.

QUICK STUDIES

Quick Study C-1 (10 minutes)

Quick Study C-2 (10 minutes)

2. Assign overhead costs to Fast and Standard models

Fast

Standard

Quick Study C-3 (15 minutes)

Expected Activity Activity

Activity Cost Driver Rate

Handling material $ 625,000 100,000 parts $6.25/part

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

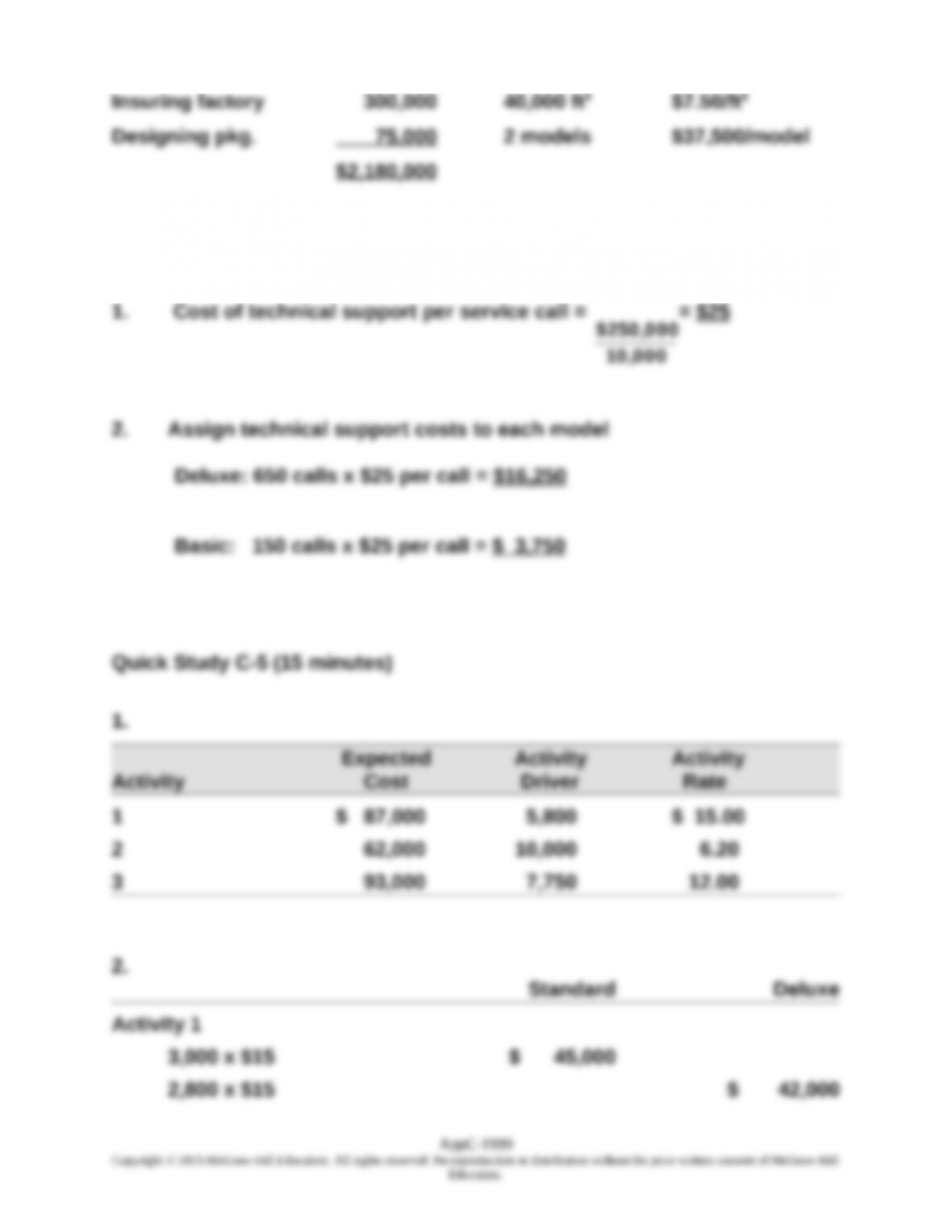

Quick Study C-4 (10 minutes)

1. Cost of technical support per service call =

10,000

$250,000

= $25

2. Assign technical support costs to each model

Deluxe: 650 calls x $25 per call = $16,250

Basic: 150 calls x $25 per call = $ 3,750

Quick Study C-5 (15 minutes)

1.

Expected Activity Activity

Activity Cost Driver Rate

1 $ 87,000 5,800 $ 15.00

2.

Standard Deluxe

Activity 1

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Activity 2

Activity 3

Quick Study C-6 (15 minutes)

Overhead cost allocation of indirect labor and supplies to Department 1:

Overhead cost allocation of rent and utilities, general office, and

depreciation to Department 1

Total overhead allocated to Department 1

Quick Study C-7 (5 minutes)

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

EXERCISES

Exercise C-1 (25 minutes)

1. $1,004,000 + $465,300 + $232,000 = $283.55 per machine hour

6,000 machine hours

Model 145

1,800 machine hours x $283.55/machine hour $ 510,390

Model 212

4,200 machine hours x $283.55/machine hour $ 1,190,910

2. Model 145

Materials and labor $250.00

Model 212

Materials and Labor $180.00

3. Model 145 Model 212

Price per unit $800.00 $470.00

Using a single plantwide overhead rate, Model 212 appears to be

unprofitable. Management may be inclined to stop producing this

product, increase its selling price, or look for ways to cut the cost of

producing Model 212 in order to make it appear profitable. The

plantwide rate may be inappropriate in this case, since machine

hours are only accumulated in the components department, and over

40% of the overhead is incurred outside of that department.

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Exercise C-2 (35 minutes)

1.

Components

Changeover $500,000 / 800 batches $625/batch

Finishing

Welding $180,300 / 3,000 welding hours $60.10/WH

Support

Model 145 Model 212

Changeover

400 batches x $625/batch $ 250,000 $ 250,000

Machining

1,800 MH x $46.50/MH 83,700

4,200 MH x $46.50/MH 195,300

Setups

60 setups x $1,875/setup 112,500 112,500

Welding

800 WH x $60.10/WH 48,080

2,200 WH x $60.10/WH 132,220

Inspecting

400 inspections x $300/inspection 120,000

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Exercise C-2 (concluded)

2. Model 145 Model 212

Materials & labor cost per unit $250.00 $180.00

3. Model 145 Model 212

Price per unit $800.00 $470.00

Both product lines appear profitable. Using ABC we see that Model

145 is not generating nearly as much profit as it appeared to generate

using the volume-based systems in Exercise C-1. Furthermore,

Exercise C-3 (35 minutes)

1. Total direct labor hours:

Product A: 10,000 units x 0.20 DLH/unit = 2,000 DLH

Plant-wide overhead rate:

Exercise C-3 (continued)

Product A Product B

Direct materials

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Direct labor

A: 2,000 DLH x $24/DLH 48,000

B: 500 DLH x $24/DLH 12,000

Overhead

A: 2,000 DLH x $99.60/DLH 199,200

2. Product A Product B

Price per unit $20.00 $60.00

It appears that Product A is not profitable. The company may decide

that this product line should be eliminated if it cannot reduce the cost

of Product A or increase the selling price.

Exercise C-3 (concluded)

3. Overhead rates

Machine setup $121,000/(10 + 12) setups $5,500/setup

*Product A: 1 part/unit x 10,000 units = 10,000 parts

Parts handling

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

A: 10,000 parts x $3/part 30,000

B: 6,000 parts x $3/part 18,000

Quality control inspections

A: 40 insp. hr. x $320/insp. hr. 12,800

4. Product A Product B

Using this approach (activity-based costing) the company sees that

Product B is not profitable, and Product A is profitable. The company

should evaluate the activities used to produce Product B and

determine how costs can be reduced. If they cannot be reduced, the

company should consider discontinuing Product B. Volume-based

costing overstates the cost of high-volume products and understates

the cost of low-volume products. ABC more accurately reflects the

cost of production by assigning costs to product lines based on the

activities required to produce them.

Exercise C-4 (20 minutes)

1.

Client consultation $270,000/1,500 contact hours $180/con.hr.

Drawings $115,000/2,000 design hours $57.50/design hr.

2.

Client consultation 450 contact hours x $180/con. hr. $ 81,000

Drawings 340 design hrs. x $57.50/design hr. 19,550

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Appendix C – Activity-Based Costing

Exercise C-5 (25 minutes)

Part 1

Part 2

Determination of cost per driver unit

Cost Center Cost Driver Cost per Driver

Professional salaries…………………..$1,600,000 10,000 hours $160 per hour

Exercise C-5 (continued)

Part 3

Allocation of costs to the general surgery department using ABC

GENERAL SURGERY

Cost

Driver

Cost per

Driver Unit

Allocated

Cost

Professional salaries…………. 2,500 hours $160 per hr. $400,000

AppC-1999

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.