Appendix C – Activity-Based Costing

APPENDIX C

ACTIVITY-BASED COSTING

Related Assignment Materials

Student Learning Objectives Discussion

Questions

Quick

Studies*

Exercises* Problems* Beyond the

Numbers

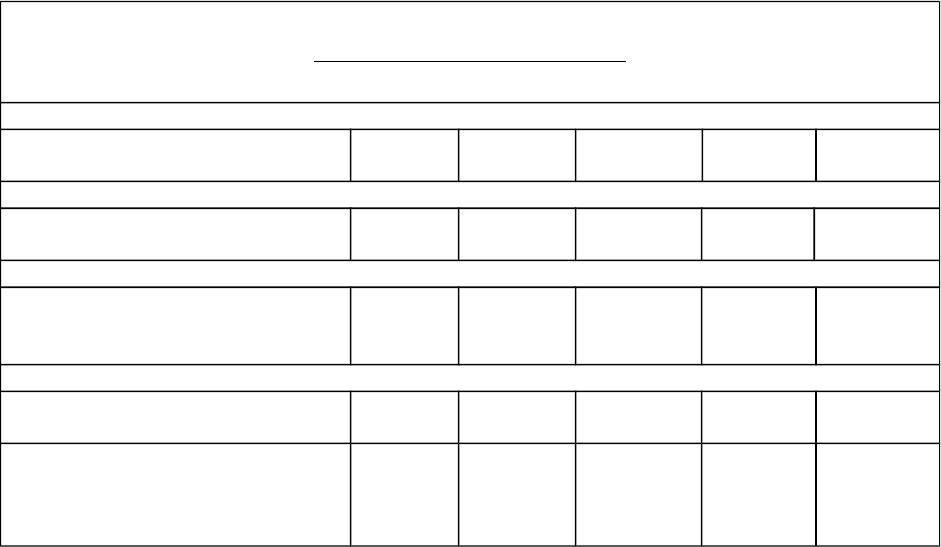

Conceptual objectives:

C1. Explain cost flows for activity

based costing

1,3,4

Analytical objectives:

A1. Identify and assess advantages and

disadvantages of activity-based

costing

7,10,11 C-1, C-7 C-2, C-3,

Procedural objectives:

P1. Assign overhead costs using the

plantwide overhead rate method

2 C-2 C-1, C-3 C-1, C-2

P2. Assign overhead costs using

activity-based costing

5,6,8,9 C-3, C-4,

C-5, C-6

C-2, C-3,

C-4, C-5

C-1, C-2,

*See additional information on next page that pertains to these quick studies, exercises and

problems.

C-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Appendix C – Activity-Based Costing

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Corresponding problems in set B also relate to learning objectives identified in grid on previous page.

The Serial Problem for Success Systems continues throughout many chapters of the text and can be

completed with Sage 50 Software.

Chapter Revision

Revised discussion of advantages and disadvantages of ABC

C-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Appendix C – Activity-Based Costing

Chapter Outline

I. Overhead Cost Allocation Methods

A. Plantwide Overhead Rate Method

1. Uses one overhead rate to allocate overhead costs to products.

2. The target of the cost assignment, or cost object, is the unit of

product.

3. The rate is determined using volume related measure, such as

direct labor hours, machine hours, or direct labor cost dollars

4. Applying the Plantwide Overhead Rate Method:

a. Total budgeted overhead costs are combined into one cost

pool

b. The cost pool is divided by the selected allocation base

(direct labor hours, machine hours, direct labor cost dollars)

to arrive at a single plantwide overhead rate

c. The rate is then applied to assign costs to all products based

on the allocation base such as direct labor hours or machine

hours required to manufacture each product.

B. Activity-Based Costing

1. Attempts to better allocate costs to proper users of overhead

activities by focusing on activities.

2. Costs are traced to individual activities and then allocated to cost

objects

3. Exhibit C.4 shows the two stage activity-based cost allocation

method

4. First Stage

a. Identify activities involved in processing the product or

service and then form activity cost pools by combining

activities into homogenous groups called cost pools.

b. A homogenous cost pools consists of activities that belong

to the same process and/or are caused by the same cost

driver

c. A cost driver (activity cost driver) is a factor that causes the

cost of an activity to go up or go down.

d. An activity cost pool is a temporary account used to

accumulate the costs a company incurs to support an

identified set of activities. It is handled like a factory

overhead account.

5. Second stage

a. Compute predetermined overhead cost allocation rates for

each cost pool

b. Allocate costs to cost objects based on cost drivers

(allocation bases)

c. Cost objectsusers of the activity (such as jobs or products).

Notes

C-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Appendix C – Activity-Based Costing

C. Advantages and Disadvantages of Activity Based Costing

1. Traditional cost systems:

a. Capture overhead costs by individual department (or

function) in one or more overhead accounts.

b. Assign overhead costs using a single allocation base such as

direct labor or multiple allocation bases.

c. Allocation bases are often not closely related to the actual

way costs are incurred.

2. Activity-based cost systems:

a. Capture costs by individual activity. Activities and their

costs are accumulated into activity cost pools.

b. Select a cost driver (allocation base) for each activity pool;

use this cost driver to assign accumulated activity costs to

cost objects (such as jobs or products) benefiting from the

activity.

c. Generally ABC uses more allocation bases than a traditional

plantwide system

d. Especially effective when the same department or

departments produce many different kinds of products;

complex products are assigned greater portion of overhead.

e. Encourages managers to focus on activities as well as the

use of those activities.

f. Requires managers to look at each item and encourages

them to manage each cost to increase the benefit from each

dollar spent.

g. Encourages managers to cooperate because it shows how

their efforts are interrelated—results in activity-based

management.

h. ABC requires more effort to implement than a traditional

cost system. It doesn’t always conform to GAAP so it can’t

readily be used for external reporting.

i. The cost sometimes outweighs its value.

C-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Appendix C – Activity-Based Costing

DEMO PROBLEM

Plata Company manufacturers 2 printer models: Deluxe and Cheapie. A single

plantwide cost driver (150% of direct labor cost) is used to apply the $24,000 of

overhead costs to the products. The following information is available:

Deluxe Cheapie

quantity to be produced 100 1,000

Selling price per unit $ 300 $ 100

Direct Materials cost per unit 100 40

Direct Labor cost per unit 20 14

1. Using the plantwide overhead rate method, compute the cost per unit, the

gross profit per unit and gross profit rate per unit.

The company decided to apply the activity based costing (ABC) method to see if they

can get a be2er allocation of overhead costs. The following data was collected:

activity Name activity Cost Driver Deluxe Cheapie Total

Setups $ 4,000 Setup hours 600 200 800

Machining 20,000 Machine hours 2,000 3,000 5,000

Total overhead costs $ 24,000

2. Using the activity Based costing (ABC) method:

a. Compute the activity rate for each of the identified ac)vi)es

b. Compute the amount of overhead assigned to the Deluxe and Cheapie

printers

c. Compute the cost per unit, the gross profit per unit and gross profit rate

per unit.

C-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Appendix C – Activity-Based Costing

SOLUTION

1. Using the plantwide overhead rate method, compute the cost per unit, the gross

profit per unit and gross profit rate per unit.

Deluxe Cheapie

Sales per unit $ 300 $ 100

direct materials per unit $ 100 $ 40

direct labor per unit 20 14

overhead per unit (150% X DL cost) 30 21

cost per unit 150 75

gross profit ($) per unit $ 150 $ 25

Gross profit rate (%) (Gross Pro0t/Sales) 50.0% 25.0%

2. Using the activity Based costing (ABC) method:

a. Compute the activity rate for each of the identified ac)vi)es

Ac)vi)es activity Costs Driver quantity Rate __________

Setups $4,000 / 800 setup hours = $5 per setup hour

Machining $20,000 / 5,000 machine hours = $4 per machine hour

b. Compute the amount of overhead assigned to the Deluxe and Cheapie

printers

Ac)vi)es Deluxe

Rate x Act. activity Cost

Setups $5 per setup hr. x 600 setup hrs. $3,000

Machining $4 per machine hr. x 2,000 machine hrs. 8,000

Total costs allocated $11,000

Overhead Cost per Unit ($11,000 / 100 units) $110

Ac)vi)es Cheapie

Rate x Act. activity Cost

Setups $5 per setup hr. x 200 setup hrs. $ 1,000

Machining $4 per machine hr. x 3,000 machine hrs. 12,000

Total costs allocated $13,000

Overhead Cost per Unit ($13,000 / 1,000 units) $13

C-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Appendix C – Activity-Based Costing

c. Compute the Unit cost, the gross profit per unit and gross profit %

per unit

Deluxe Cheapie

Sales per unit $ 300 $ 100

direct materials per unit

$

100

$

40

direct labor per unit 20 14

overhead per unit (150% X DL cost) 110 13

cost per unit 230 67

gross profit ($) per unit $ 70 $ 33

Gross profit rate (%) (Gross Pro0t/Sales) 23.3% 33.0%

C-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.