Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Notes on Major Case 6

Waste Management

Ethical Issues:

The Principle of Due Care in the AICPA Code of Professional Conduct obligates a CPA

to perform services with competence and diligence and with concern for the best interest of

investors and creditors who provide the capital needed for operations. Due Care also implies that

the auditor is independent of management, objective in decision making, and maintains integrity.

Auditors must properly plan the audit and supervisor assistants and obtain sufficient relevant

data. The ability to obtain sufficient, competent evidential matter is the basis for making

professional judgments that help to determine whether Waste Management’s financial statements

accurately record, in all material respects, the client’s actual income, financial position, and cash

flows. For example, auditors fail to meet these requirements if they rely extensively on

information provided by the client, often in the form of oral representations of management, and

fail to obtain sufficient documentary and other evidence from independent sources to verify

management’s representations. Andersen heavily relied on management’s assurances that the

steps outlined to correct for past misstatements in the financial statements would not continue

into the future. Not only did they persist, but the company failed to spread out the effect of the

misstatements over future income as had been agreed to with management.

In addition to a lack of due care, Andersen was not independent of the client, at least in

appearance, because of managing partner on the Waste Management engagement, Robert

Allgyer, was a member of the Steering Committee that oversaw the Strategic Review and that

made a recommendation on implementing a new operating model to “increase shareholder

value.” Andersen Consulting billed Waste Management for Allgyer’s time for these services. In

setting Allgyer’s compensation, Andersen took into account, among other things, the firm’s

billings to Waste Management for audit and non-audit services

(http://www.sec.gov/litigation/litreleases/lr17435.htm). Allgyer’s relationship with Waste

Management impaired audit independence because the firm would eventually audit results based

on the new model recommended by Allgyer.

Audit independence is the cornerstone of the ethical obligations of auditors because it

creates a barrier between the clients’ interests and what is in the public interest. The public relies

on the auditor’s independence and ability to make objective judgments. Independence is both a

factual requirement and auditors must also appear to be independent to a reasonable observer.

The relationship between former Andersen professional staff that had gone to work for Waste

Management in key financial reporting positions created the appearance that independence might

be impaired. This relationship brought into question whether Andersen lacked the intellectual

honesty and objectivity that was necessary to make professional judgments about the GAAP

conformity of the financial statements.

CPAs are expected to approach an audit with professional skepticism; to have an attitude

that includes a questioning mind and a critical assessment of audit evidence. The auditor should

plan and perform the audit with professional skepticism recognizing that circumstances may

exist that cause the financial statements to be materially misstated. Andersen knew Waste

Management’s statements contained many misstatements in the application of GAAP but the

firm rationalized accepting the statements without correction or restatement of prior years’

statements based on erroneous materiality judgments.

Another indication of Andersen’s lack of independence was the level of its audit fees in

comparison to non-audit fees. The firm may have been concerned that if it would lose

lucrative consulting jobs if it had maintained its integrity and not given in to the pressures

placed on them by top management. As pointed out in the case, Andersen reported to

the audit committee that it had billed Waste Management approximately $7.5 million in

audit fees. Over the seven-year period, while Andersen’s corporate audit fees remained

capped, Andersen also billed the company $11.8 million in other fees. A related entity,

Andersen Consulting, also billed Waste Management approximately $6 million in

additional non-audit fees, $3.7 million of which related to a Strategic Review that

analyzed the company’s overall business structure.

SEC Litigation Release 17435 notes that until 1997, every CFO and CAO in Waste

Management’s history as a public company had previously worked as an auditor at Andersen.

During the 1990s, approximately 14 former Andersen employees worked for Waste

Management, most often in key financial and accounting positions

(http://www.sec.gov/litigation/litreleases/lr17435.htm).

Andersen allowed client management to dictate the direction that would be taken to deal

with audit issues raised in the PAJEs. It is highly unusual for an audit firm to enter into an

agreement with a client to adjust for past accounting mistakes in the future by spreading them out

over a number of years and simply promise never to do it again. Andersen relinquished its role as

the decider of what should be done based on audit and ethics standards and allowed the client to

make important professional decisions. In doing so, the firm knowingly went along with material

misstatements in the financial statements ostensibly to keep the client happy.

Questions

1. The SEC charged Andersen with failing to quantify and estimate all known and

likely misstatements due to non-GAAP practices. What is the purpose of doing

this from an auditing perspective?

Auditors quantify all known and likely misstatements to evaluate the audit findings and

determine the appropriate audit opinion. To issue an unmodified opinion the auditors must

conclude that there is a low level of risk of material misstatement of the financial statements.

Known misstatements are specific misstatements identified during the course of the audit (i.e., a

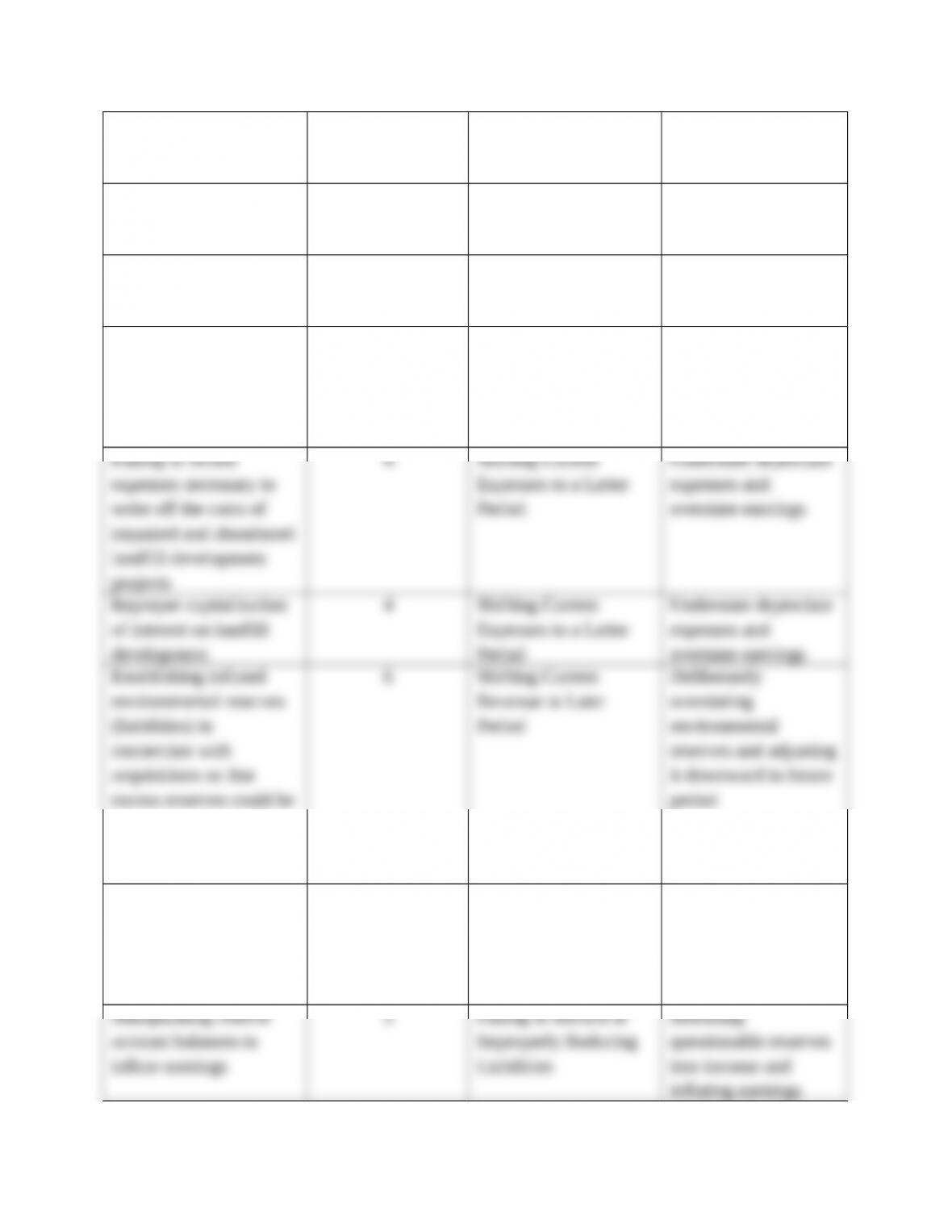

2. Classify each of the accounting techniques described in the case that contributed

to the fraud into one of Schilit’s accounting shenanigans. Include a brief

discussion on how each technique violated GAAP.

Waste Management used the following improper accounting practices paired with Schilit’s

shenanigans:

Description of

Improper Accounting

Practice

Schilit’s

Shenanigan

Number

Description of

Shenanigan

Effect on Financial

Statements

Improperly eliminating

or deferring current

period expenses

4 Shifting Current

Expenses to a Latter

Period

Understate depreciate

expenses and

overstate earnings

Making unsupported

changes in depreciation

estimates

4 Shifting Current

Expenses to a Latter

Period

Understate depreciate

expenses and

overstate earnings

Failing to record

expenses for decreases

in the value of landfills

as they were filled with

waste

4 Shifting Current

Expenses to a Latter

Period

Understate depreciate

expenses and

overstate earnings

used to avoid recording

unrelated environmental

and other expenses

Netting one-time gains

against operating

expenses

3,5 Boosting Income with

a One-time Gain Offset

by Offsetting Expenses

Reducing current

revenue and reducing

current expenses; net

effect of inflating

earnings

3. Review the facts of the case with respect to Andersen’s role in the fraud and

describe the provisions of the AICPA Code of Professional Conduct that you

believe were violated by the firm. Comment on Andersen’s risk assessment as

part of its audit procedures.

Andersen audited and issued an unqualified (i.e., unmodified) report on each of Waste

Management’s original financial statements and on the financial statements in the restatement. In

The SEC complaint against Andersen charged that the firm knew of Waste Management’s

exaggerated profits during its audits of the financial statements from 1992 through 1996 and

repeatedly pleaded with the company to make changes. Each year, Andersen gave in and issued

• Determining the materiality of misstatements improperly; failing to record or disclose

information about such transactions; issuing an unqualified audit report.

• Written recognition in a memorandum prepared by Andersen of the company’s improper

netting practices and identification of SEC exposure; monitored continuing practice but

failed to adequately disclose the effect on current earnings.

At the outset of the fraud, management capped Andersen’s audit fees and advised the

Andersen engagement partner that the firm could earn additional fees through “special work.”

Andersen nevertheless identified the company’s improper accounting practices and quantified

The SEC was very critical of Andersen’s relationship with Waste Management. Litigation

Release 17039 notes that the firm had audited Waste Management since before it became a

public company in 1971 and considered the client its “crown jewel.” Until 1997, every CFO and

chief accounting officer (CAO) in Waste Management’s history as a public company had

previously worked as an auditor at Andersen. During the 1990s, approximately 14 former

Andersen employees worked for Waste Management, most often in key financial and accounting

positions. Andersen selected Allgyer to be the managing partner of the Waste Management

audit because he had demonstrated a “devotion to client service” and had a personal style that

“fit well with Waste Management officers.” During the time of the audit, Allgyer held the title of

The SEC found that Andersen and four of its auditors violated the anti-fraud provisions of

Rule 10b-5 of the Securities Exchange Act of 1934. These provisions make it unlawful for a CPA

The commission had alleged that Andersen and its partners failed to stand up to company

management and betrayed their ultimate allegiance to Waste Management’s shareholders and the

investing public by sanctioning false and misleading audit reports. Thus, the firm violated its

Andersen knew that Waste Management was not in compliance with GAAP. In planning and

performing the audit each year, Andersen should have assessed risks of material misstatements

by area, account, and overall. Andersen should have planned and performed the audit to detect