Case 8-4

Royal Dutch Shell plc

From 1907 until 2005, Royal Dutch Petroleum Company, a Netherlands-based company, and the

Shell Transport and Trading Company, plc, a UK-based company, were the two public parent

companies of a group of companies known collectively as the Royal Dutch/Shell Group (Group).

Operating activities were conducted through the subsidiaries of Royal Dutch and Shell Transport.

In 2005, Royal Dutch Shell plc became the single parent company of Royal Dutch and Shell

Transport. Today, Shell is one of the world’s largest independent oil and gas companies in terms

of market capitalization, operating cash flow and oil and gas production.

Proved Reserves

Petroleum resources represent a significant part of the group’s upstream assets and are the

foundation of most of its current and future activities. The group’s exploration and production

business depends on its effectiveness in finding and maturing petroleum resources to sustain

itself and drive profitable production growth. The Group reports its reserves of oil and gas to the

SEC as part of its 20-F filing for a foreign company selling stock on the NYSE.

Reporting internal and external volumes properly is very important to Shell. This is based

on the SEC-compliant proved reserves estimation and reporting process that enables access to

funds needed for the group’s capital-intensive business. The SEC requirement of “reasonable

certainty” represents the high standard of evidence/confidence consistent with the meaning of the

word proved. Proved oil and gas reserves are the estimated quantities of crude oil, natural gas,

and natural gas liquids which geological and engineering data demonstrate with reasonable

certainty to be recoverable in future years from known reservoirs under existing economic and

operating conditions (i.e., prices and costs as of the date the estimate is made). Prices include

consideration of changes in existing prices provided by contractual arrangements, but not on

escalations based upon future conditions.

In 2004, Shell amended its Annual Report on Form 20-F/A for the calendar year 2003

financial statements following an agreement with the SEC reached on August 24, 2004, with

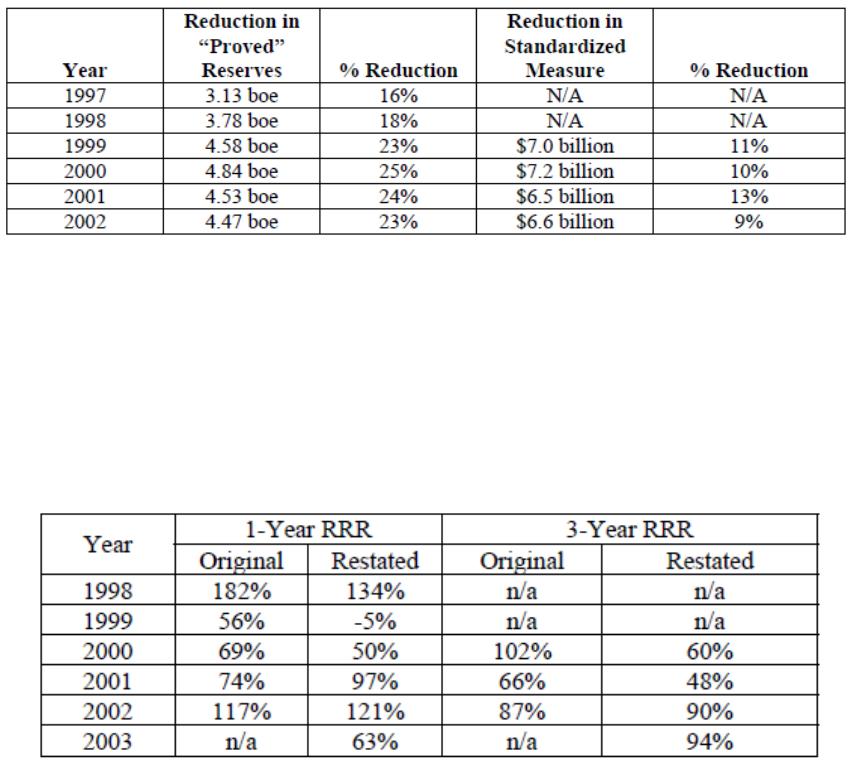

respect to the amount of proved reserves. The SEC had charged that 4.47 billion barrels of oil

equivalent (boe), or approximately 23 percent of previously reported proved reserves, did not

meet the standard set by law. Shell also reduced its reserves replacement ratio (RRR) — the rate

at which production was replaced by new oil discoveries. According to the SEC Complaint,

Shell’s overstatement of proved reserves, and its delay in correcting the overstatement, resulted

from (1) its desire to create and maintain the appearance of a strong RRR, a key performance

indicator in the oil and gas industry, (2) the failure of its internal reserves estimation and

reporting guidelines to conform to applicable regulations, and (3) the lack of effective internal

controls over the reserves estimation and reporting process.

Reduction of RRR

In a series of announcements between January 9 and May 24, 2004, Shell

disclosed that it had recategorized 4.47 billion boe, or approximately 23

percent, of the proved reserves it reported as of year-end 2002, because they

were not proved reserves as defined in Commission Rule 4-10 of Regulation S-X. This

recategorization reduced the standard measure of future cash flows by approximately $6.6 billion

as reported in Shell’s original 2002 Form 20-F, Supplemental Information under SFAS 69.

On July 2, 2004, Shell filed an amended 2002 Form 20-F reflecting the restatement of its

proved reserves and standard measure of future cash flows for the years 1999 to 2002 as follows:

As a result of the overstatement of proved reserves, Shell also announced a reduction in its RRR

for 1998 through 2002, from the previously reported 100 percent to approximately 80 percent.

Had Shell reported proved reserves properly, its annual and three-year RRR over this span would

have been as follows:

According to the SEC complaint, these failures led Shell to record and maintain proved reserves

it knew, or was reckless in not knowing, did not satisfy applicable regulations and to report for

certain years a stronger RRR than it actually had achieved in supplemental information filed

along with its 10-K report. The SEC had warned about the proved reserves but Shell either

rejected the warnings as immaterial or unduly pessimistic, or attempted to manage the potential

exposure by, for example, delaying debooking of improperly recorded proved reserves until new,

offsetting proved reserves bookings materialized.

Failure to Maintain Adequate Internal Controls

The charges against Shell include the failure to implement and maintain internal controls

sufficient to provide reasonable assurance that it was estimating and reporting proved reserves

accurately and in compliance with applicable requirements. These failures arose from

inadequate training and supervision of the operating unit personnel responsible for estimating

and reporting proved reserves and deficiencies in the internal reserves audit function. Shell’s

decentralized system required an effective internal reserves audit function.

To perform this function, Shell historically had engaged as Group

reserves auditor a retired Shell petroleum engineer who worked only part-

time and was provided limited resources and no sta( to audit its vast

worldwide operations. Although the Group reserves auditor was an

experienced reservoir engineer, he received little, if any, training on such

critical matters as how he should conduct his work and the rules and

standards on which his opinions should be based. He also lacked authority to

require operating unit compliance with either commission rules or group

reserves guidelines. Moreover, he reported to the management of Shell’s

exploration and production division, which were the same people he audited.

The Group reserves auditor visited each operating unit only once every

four or more years. Subsequent to his visits, he issued reports rating the

operating unit’s systems, compliance with Group guidelines and audit

response as “good,” “satisfactory” or “unsatisfactory,” opining whether the

operating unit’s reported reserves met Group guidelines. From the start of his

tenure in January 1999 until September 2003, the Group reserves auditor did

not issue a single “unsatisfactory” rating. The Group reserves auditor also

issued an annual report on the reasonableness of Shell’s year-end total

reserves summary. Until his February 2004 report on Shell’s 2003 proved

reserves, the Group reserve auditor focused as much on whether Group

proved reserves complied with group guidelines as he did on whether they

complied with SEC requirements.

Further, the group reserves auditor failed to act independently in

several respects. At times, he allowed proved reserves associated with a

project to remain booked because he was more “bullish” on its prospects

than the local management responsible for the project. At other times, solely

to support booking proved reserves for otherwise uneconomic projects, he

advised local management to submit development plans that were unlikely

ever to be executed. This lack of independence facilitated the booking of

questionable reserves well after they should have been debooked.

Finally, the nonexecutive directors of Royal Dutch and Shell Transport, including the

members of the Group audit committee, were not provided with the information necessary for the

boards of the two companies to ensure that timely and appropriate action was taken with respect

to the proved reserves estimation and reporting practices.

Group Reserve Auditor’s Report

In January 2002, the Group reserves auditor’s report on Shell’s 2001 proved

reserves stated that “recent clari6cations of FASB reserves guidelines by the

SEC have shown that current Group reserves practice regarding the first time

booking of Proved reserves in new 6elds is in some cases too lenient.” The

auditor stated that the “g[G]roup guidelines should be reviewed [and] first-

time bookings should be aligned closer with SEC guidance and industry

practice and they should be allowed only for 6rm projects with technical

maturity and full economic viability.”

On February 11, 2002, an internal note addressed the divergence

between Shell’s guidelines and the Commission’s rules and estimated the

possible impact of this divergence on Shell’s reported proved reserves. The

note explicitly stated that “recently the SEC issued clari6cations that make it

apparent that the Group guidelines for booking Proved Reserves are no

longer fully aligned with the SEC rules.” Potential exposures identified in the

note included approximately 1 billion boe of proved reserves relating to

projects. The note failed to recommend debookings, and Shell did not take

action to debook any of these proved reserves at that time.

By September 2002, the CEO of EP internally spoke in blunt terms of

his perception of the operational and performance problems facing EP,

noting to his colleagues that “we are struggling on all key criteria” and that

“RRR remains below 100% mainly due to aggressive booking in 1997-2000.”

He further observed that “we have tried to adhere to a bunch of criteria that

can only be managed successfully for so long” and admonished that “given

the external visibility of our issues…, the market can only be ‘fooled’ if: (1)

credibility of the company is high; (2) medium and long-term portfolio

refreshment is real; and/or (3) positive trends can be shown on key

indicators.”

A month later, the group chair emailed the EP CEO that he was “not

contemplating a change in the external promise . . . .” The next day, the EP

CEO responded, stating “I must admit that I become sick and tired about

arguing about the hard facts and also cannot perform miracles given where

we are today. If I was interpreting the disclosure requirements literally under

the Sarbanes-Oxley Act and legal requirements we would have a real

problem.”

None of these events prompted Shell to debook signiticant volumes. To

the contrary, Shell continued to make large, questionable proved reserves

bookings during this period. By the summer of 2003, Shell’s analysis of

reserves exposures had progressed, but still no debookings were

recommended even though internal information indicated that “some 1040

million boe (5%) is considered to be potentially at risk.” The note concluded,

however, that “at this stage, no action in relation to entries in the [proved

reserves exposure] Catalogue is recommended… It should be noted that the

total potential exposure is broadly o(set by the potential to include gas fuel

and Gare volumes in external reserves disclosures.” The note apprised the

committee of steps taken to address possible noncompliance with the SEC’s

regulations. However, management was advised that “much, if not all, of the

potential exposure is o(set by Shell’s practice of not disclosing reserves in

relation to gas production that is consumed on site as fuel or (incidental)

Garing and venting.”

According to the SEC complaint, Shell has undertaken substantial

remedial effort in connection with the reserves recategorization and had

cooperated with the Commission in its investigation.