Chapter 8

2. The numerator of Stock A’s beta = 22.9% (0.62 × 37%). The same quantity for Stock B =

32.0% (0.94 × 34%). Because all betas share the same denominator, the stock with the lower

4. If the investment is above the company’s average risk, then the company’s cost of capital is not

an appropriate benchmark. Equivalently, the high risk of the investment places it below the

6. When an investment lies below the market line it is possible to make equal-risk investments

8. a. Using the perpetuity equation, IRR = 6.4/40=16%

b. Kw = [(1–.35)(7.5%)(290) + 14%(20 × 40)]/(290 + 20 × 40) = 11.6%. As long as the

10. Divide the cash flows into two periods: A 15-year annuity of $1,000, and a growing perpetuity

beginning in the 15th year. The value of the 15-year annuity is $6,462.38.

The value of the growing perpetuity at time 15 is $1,000(1 + 0.04)/(0.13 – 0.04) = $11,555.56.

=PV(.13,15,1000) = ($6,462.38)

PV(rate, nper, pmt, [fv], [type])

12. A standard way to estimate an asset’s beta is to regress its returns against those of a well–

14. See Excel solutions at mhhe.com/higgins11e. .

16. a. Voice Division EVA = $220 × (1 – 40%) – 10% × $1,000 = $32 million. Data Division

b. The fact that the Data Division’s EVA is negative should be a source of concern but not

justification for immediately eliminating the division. Here are some reasons EVA

numbers should be treated cautiously in strategic decision making.

number can be used to represent capital employed in an EVA calculation.

In my opinion divisional EVAs can yield useful information but should never be used

name a date by which division EVA will be positive, and then hold him to this projection.

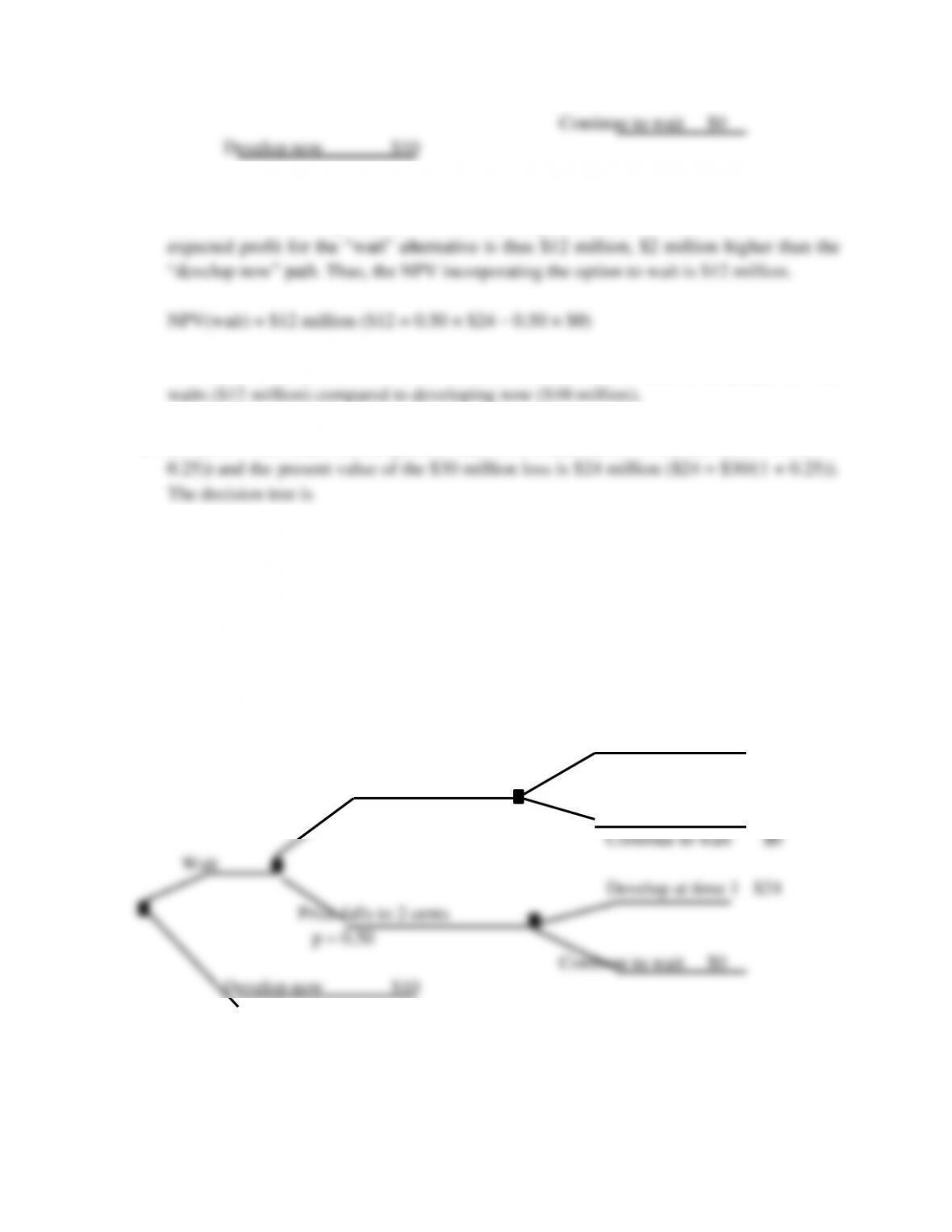

18. a. At the 25% discount rate, the present value of $30 million is $24 million ($24 =

$30/(1+.25)) and the present value of the $10 million loss is $8 million ($8 = $10/(+.25)).

The decision tree is

Develop at time 1 $24

Price rises to 8 cents

p = 0.50

b. If gas prices rise, WRI will develop the wind farm in one year at a present value profit of

$24 million, but if they fall, it will defer development to a future date at no cost. The

c. The value of the option to wait is $2 million, the difference in value of the project if WRI

d. At the 25% discount rate, the present value of $60 million is $48 million ($48 = $60/(1 +

Develop at time 1 $48

Price rises to 12 cents

p = 0.50

If gas prices rise, WRI will develop the wind farm in one year at a present value profit of

The value of the option to wait is $14 million, the difference in value of the project if WRI

20. See Excel solutions at www.mhhe.com/higgins11e.

22. a. Asset beta = (E/V) × Equity beta = (1 – 0.60) × 1.20 = 0.48

d. Relevant cash flows are:

Year

1

2

3

4

5

Principal

$320

$240

$160

$80

$0

Interest at 8% beginning balance

32

26

19

13

6

Tax shields (Tax rate × interest

expense)

13

10

8

5

3

PV of tax shields at KA = $34.04 million

f. The answer in (e) above ignores expected financial distress costs and is thus surely an

24. a. Following the approach described in Table 8A.1, an average asset beta, weighted by

relative market values of equity, appears below. Other weighting schemes, or a simple

unweighted average, are also defensible.

Firm

Equity

Beta

Debt

MVE

E/V

Asset beta

% total

MVE

Weighted

Asset

beta

Black & Decker

1.19

$4,100

$6,300

0.606

0.721

38.78%

0.280

Fedders Corp.

1.20

5

200

0.976

1.171

1.23%

0.014

Helen of Troy

Corp.

2.14

380

530

0.582

1.246

3.26%

0.041

Salton, Inc.

3.25

375

115

0.235

0.763

0.71%

0.005

Whirlpool

1.83

10,600

9,100

0.462

0.845

56.02%

0.474

Industry

Asset

Beta

0.814

b. The asset betas of the companies above vary within a reasonably narrow range, providing

some comfort that our calculated asset beta reflects the business risk of the home appliance