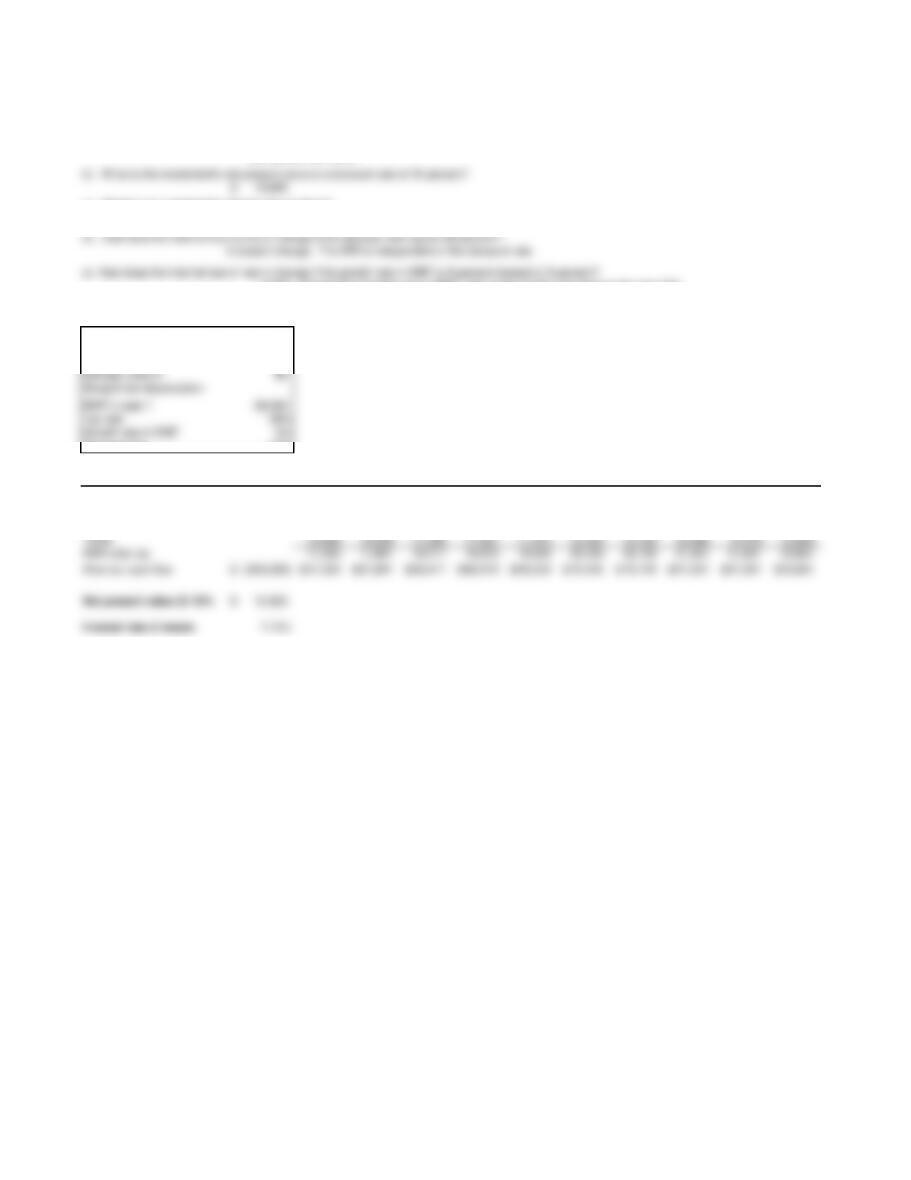

Chapter 7 Problem 12

a). Complete the spreadsheet below by estimating the project’s annual after tax cash flow.

b). What is the investment’s net present value at a discount rate of 10 percent?

c). What is the investment‘s internal rate of return?

d). How does the internal rate of return change if the discount rate equals 20 percent?

e). How does the internal rate of return change if the growth rate in EBIT is 8 percent instead of 3 percent?

Facts and Assumptions

Equipment initial cost $ 350,000$

Depreciable life yrs. 7

Expected life yrs. 10

Salvage value $ $0

Straight line depreciation

EBIT in year 1 28,000

Tax rate 38%

Growth rate in EBIT 3%

Discount rate 10%

Year 0 1 2 3 4 5 6 7 8 9 10

Initial cost 350,000

Annual depreciation 50,000 50,000 50,000 50,000 50,000 50,000 50,000

EBIT 28,000 28,840 29,705 30,596 31,514 32,460 33,433 34,436 35,470 36,534

Net present value @ 10%

Internal rate of return

Chapter 7 Problem 12 Suggested Answers

a). Complete the spreadsheet below by estimating the project’s annual after tax cash flow.

See spreasheet below.

b). What is the investment’s net present value at a discount rate of 10 percent?

12,923$

c). What is the investment‘s internal rate of return?

11.0%

d). How does the internal rate of return change if the discount rate equals 20 percent?

It doesn’t change. The IRR is independent of the discount rate.

e). How does the internal rate of return change if the growth rate in EBIT is 8 percent instead of 3 percent?

12.8% Change the “Growth rate in EBIT” assumption to 8% and observe the new IRR.

Facts and Assumptions

Equipment initial cost $ 350,000$

Depreciable life yrs. 7

Expected life yrs. 10

Salvage value $ $0

Straight line depreciation

EBIT in year 1 28,000

Tax rate 38%

Growth rate in EBIT 3%

Discount rate 10%

Year 0 1 2 3 4 5 6 7 8 9 10

Initial cost 350,000

Annual depreciation 50,000 50,000 50,000 50,000 50,000 50,000 50,000

EBIT 28,000 28,840 29,705 30,596 31,514 32,460 33,433 34,436 35,470 36,534

Taxes 10,640 10,959 11,288 11,627 11,975 12,335 12,705 13,086 13,478 13,883

EBIT after tax 17,360 17,881 18,417 18,970 19,539 20,125 20,729 21,351 21,991 22,651

After tax cash flow (350,000)$ 67,360$ 67,881$ 68,417$ 68,970$ 69,539$ 70,125$ 70,729$ 21,351$ 21,991$ 22,651$

Net present value @ 10% 12,923$

Internal rate of return 11.0%

Chapter 7 Problem 13

Date

01-31 $100,000

02-28

03-31

04-30

05-31

06-30

F = $1,000(1.01)12 = $1,000(1.1268) = $1,126.80 This compares to F = $1,000(1+.12) =$1,120.00 for annual compounding.

Hence, the monthly compounding has the same effect on the year-end amount due as the charging of a rate of 12.68 percent compounded annually. 12.68

percent is referred to as the effective interest rate.

Clearly, it is desirable to recognize the difference between 1 percent per month compounded monthly and 12 percent per annum compounded annually. If

$1,000 is borrowed with interest at 1 percent per month compounded monthly, the amount due in one year is:

Consider a loan transaction in which interest is charged at the rate of 1 percent per month. Sometimes such a transaction is described as having an interest

rate of 12 percent per annum. More precisely, this rate should be described as a nominal 12 percent per annum coumpounded monthly.

In many financial transactions, interest is computed and charged more than once a year. Interest on corporate bonds, for example, is usually payable every

six months.

To generalize, if interest is compounded m times a year at an interest rate of r/m per compounding period. Then,

The nominal interest rate per annum, or the APR = m(r/m) = r .

Principal

payment

Outstanding

Balance End

of Month

The effective interest rate per annum,or the EAR = (1+r/m) m – 1 .

Consider a $100,000, 30 year, fixed-rate, 9 percent, home mortgage requiring monthly payments.

a. The monthly interest rate on the mortgage is 9%/12 months = .75%. What is the APRon the mortgage?

b. What is the EAR on the mortgage?

c. The borrower’s payment book will look something like the following. Complete the entries for the first 6 months.

Outstanding

Balance

Beginning of

Month

Monthly

payment

Interest

due

e. Suppose after 15 years the borrower has the opportunity to refinance the remaining principal on the mortgage with a new 15-year mortgage

carrying an interest rate of 7 1/8%. Refinancing will involve $250 in costs and “points” equal to 1.5 percent of the amount borrowed. If the

borrower plans to live in the house for 15 more years, does it make economic sense to refinance? Does your answer change if the borrower only

intends to live in the house for 5 more years and will pay off any loans outstanding at that time? You may ignore taxes and may assume there are

no prepayment penalties on either mortgage.

d. After paying on this mortgage for 15 years, what will be the remaining principal outstanding?

Chapter 7 Problem 13 Suggested Answers

Data:

Principal: $ 100,000.00

Term: 30 years 360 months

Rate: 9.000% per annum 0.750% per month

APR = m(r/m) = 9 percent.

EAR = (1+r/m)m – 1 = 9.38%

Date

01-31 $ 100,000.00 $ 804.62 $ 750.00 $ 54.62 $ 99,945.38

02-28 99,945.38 804.62 749.59 55.03 99,890.35

03-31 99,890.35 804.62 749.18 55.45 99,834.90

04-30 99,834.90 804.62 748.76 55.86 99,779.04

05-31 99,779.04 804.62 748.34 56.28 99,722.76

06-30 99,722.76 804.62 747.92 56.70 99,666.06

The remaining principal due equals the present value of the remaining payments.

Using Excel:

$79,330.23 =-PV(9%/12, 15*12, 804.62, 0)

Option 1: Keep the exisiting mortgage. At an opportunity cost of 7 1/8%, the remaining payments on the current loan have a present value of

PV(7.125%/12,15*12,804.62,0) = $88,826.71

Option 2: Refinance.

Amount to be refinanced 79,330.23$

Fees 250.00$

Points 1,189.95$

Total cost 80,770.18$

There is over a $8,000 benefit to refinancing. $8,056.53

If homeowner plans to stay only 5 more years:

Option 1: Keep the existing mortgage. Pay $804.62 for 60 months. Present value at 7 1/8% = $40,514.14

-PV(9%/12, 10*12, $804.62) =

$63,518.27

The present value of this liability discounted at 7 1/8 percent over 5 years equals $44,528.57

-PV(71/8/12, 5*12, 0, $63,518.27) =

$44,528.57

Hence, the total cost of this option equals $85,042.71 ($40,514.14 + $44,528.57)

Option 2: Refinance. Pay $718.60 for 60 months. Present value = $36,182.77. Payment: Present Value:

$718.60 $36,182.77

At the end of 60 months the principal value on the loan equals the present value at 7 1/8 percent interest of the remaining 120 payments, which equals $61,548.17

PV(.07125/12, 10*12, 718.60) = $61,548.17

Comparing total costs, option 2 is still $4,272.53 cheaper, the advantage to refinancing is much less.

Outstanding

Balance End

of Month

d. After paying on this mortgage for 15 years, what will be the remaining principal outstanding?

e. Suppose after 15 years the borrower has the opportunity to refinance the remaining principal on the mortgage with a new 15-year mortgage carrying an

interest rate of 7 1/8%. Refinancing will involve $250 in costs and “points” equal to 1.5 percent of the amount borrowed. If the borrower plans to live in

the house for 15 more years, does it make economic sense to refinance? Does your answer change if the borrower only intends to live in the house for 5

more years and will pay off any loans outstanding at that time? You may ignore taxes and may assume there are no prepayment penalties on either

mortgage.

At the end of 60 months the principal value still to be paid on the loan equals the present value at 9 percent interest of the remaining 10 years of payments. Using

the present value of an annuity formula for 120 monthly periods, this amount is $63,518.06.

Outstanding

Balance Beginning

of Month

Monthly

payment

Interest due

Principal

payment

Consider a $100,000, 30 year, fixed-rate, 9 percent, home mortgage requiring monthly payments.

a. The monthly interest rate on the mortgage is 9%/12 months = .75%. What is the annual nominal interest rate on the mortgage?

b. What is the annual effective interest rate on the mortgage?

c. The borrower’s payment book will look something like the following. Complete the entries for the first 6 months.

In Excel the monthly loan payment can be calculated using the PMT financial function (Formulas > Financial > PMT). The entry is

=PMT(.09/12, 12*30, 100000,0). The monthly interest rate is .09/12, and the number of periods is 12*30, or 360. The monthly payment is

$804.62

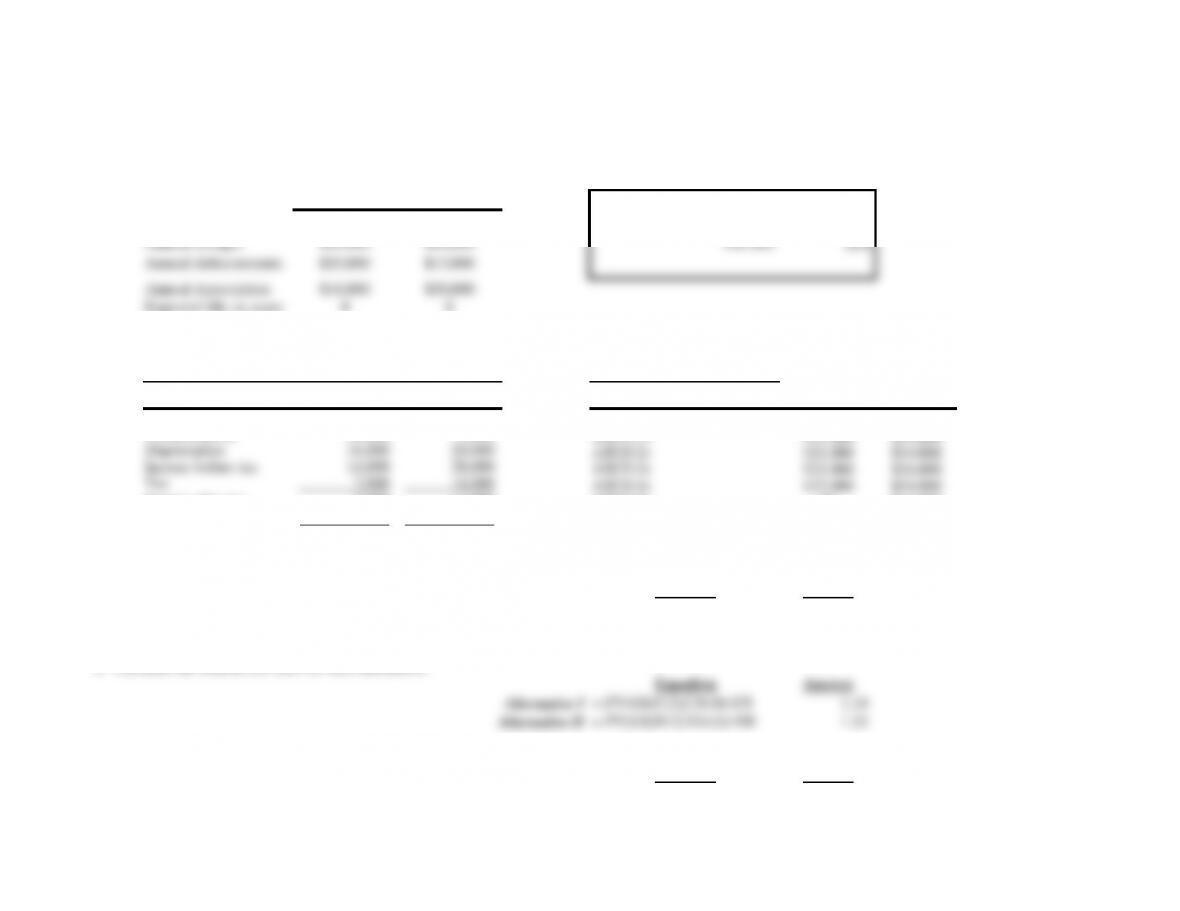

Chapter 7 Problem 14

Alternative Alternative

III

Initial investment $64,000 $120,000

Annual receipts $50,000 $60,000

Annual disbursements $20,000 $12,000

Annual depreciation $16,000 $20,000

Expected life 4 yrs 6 yrs

Salvage value 0 0

a. Calculate the net present value of each alternative.

b. Calculate the benefit cost ratio for each alternative.

c. Calculate the internal rate of return for each alternative.

d. If the company is not under capital rationing which alternative should be chosen? Why?

A company is considering two alternative methods of producing a new product. The relevant data concerning the alternatives appear

below:

e. Again assuming no capital rationing, suppose the company plans to produce the product indefinitely rather than quit when the

equipment wears out. Which alternative should the company select? Why?

At the end of the useful life of whatever equipment is chosen the product will be discontinued. The company’s tax rate is 50 percent

and the discount rate is 10 percent.

f. If the company is experiencing severe capital rationing, and plans to terminate production when the equipment wears out, would

any of your answers above change?

Chapter 7 Problem 14 Suggested Answers

Alternative Alternative

III

Initial investment ($64,000) ($120,000) Discount rate: 10%

Annual receipts $50,000 $60,000 Tax rate: 50%

Annual disbursements $20,000 $12,000

Annual depreciation $16,000 $20,000

Expected life, in years 4 6

Salvage value 0 0

Table to calculate after tax cash flows: Table to use IRR:

Alternative

III Alternative III

Receipts 50,000$ 60,000$ Initial investment ($64,000) ($120,000)

Disbursements 20,000 12,000 ATCF(1) $23,000 $34,000

Depreciation 16,000 20,000 ATCF(2) $23,000 $34,000

Income before tax 14,000 28,000 ATCF(3) $23,000 $34,000

Tax 7,000 14,000 ATCF(4) $23,000 $34,000

Income after tax 7,000 14,000 ATCF(5) $0 $34,000

+ Depreciation 16,000 20,000 ATCF(6) $0 $34,000

After tax cash flow 23,000$ 34,000$

a. Calculate the net present value of each alternative.

Equation Answer

Alternative I =-PV(G8,C12,C24,0)+C8 $8,906.91

Alternative II =-PV(G8,D12,D24,0)+D8 $28,078.86

or =NPV(G8,H18:H23)+H17 $28,078.86

b. Calculate the benefit cost ratio for each alternative.

Equation Answer

Alternative I =-PV(G8,C12,C24,0)/-C8 1.14

Alternative II =-PV(G8,D12,D24,0)/-D8 1.23

c. Calculate the internal rate of return for each alternative.

Equation Answer

Alternative I =IRR(G17:G23,.10) 16.3%

Additional Data:

A company is considering two alternative methods of producing a new product. The relevant data concerning the alternatives are presented below:

d. If the company is not under capital rationing which alternative should be chosen? Why?

It should choose II because II has the higher NPV and NPV is a direct measure of increase in wealth.

UEAB(I) = =-PMT(G8,C12,G28,C13)

$2,809.87

UEAB(II) = =-PMT(G8,D12,G29,D13)

$6,447.11

Asset II continues to be the preferred choice, delivering the highest benefit on an equivalent annual basis.

Under capital rationing one is interested in bang per buck. This suggests using the benefit cost ratio to rank alternatives. Looking at these indices again

suggests that II is the superior alternative. This is just a provisional decision because one would need to know the BCRs of other unmentioned investments

before concluding that either of these should be undertaken.

e. Again assuming no capital rationing, suppose the company plans to produce the product indefinitely rather than quit when the equipment wears out.

Which alternative should the company select? Why?

f. If the company is experiencing severe capital rationing, and plans to terminate production when the equipment wears out, would any of your answers

above change?

There are several ways to approach this question. One of the easier is to calculate the uniform equivalent annual cost or benefit for each. This is the annuity

over the asset’s life that has the same present value as the asset. The uniform equivalent annual cost or benefit is the annual cost or benefit that would accrue

if the asset were replaced every time it wore out with an identical asset at the same cost and benefits continued indefinitely.

This approach is inappropriate under inflation or technological changes affecting the assets. But the problem does not mention these possibilities.

Chapter 7 Problem 15

Marketing Research Costs, to date 20,000$

Initial cost of new equipment 300,000$

Licensing rights to use images (To be expensed for tax purposes at time 0) 350,000$

Expected life 5 yrs

Salvage value 0

Depreciation method Straight-line over 5 years to 0 salvage value

Selling price of new equipment in 3 years* 130,000$

Incremental annual sales 800,000$

Incremental annual production costs 200,000$

Incremental annual selling

and administrative costs 80,000$

Current annual overhead costs 200,000$

Immediate advertising expenses for launch (To be expensed for tax purposes at tme 0) 190,000$

Tax rate 40%

Working capital required, as a % of production costs 7.50% (Needed at time 0.)

Minimum required rate of return 10%

*The company must pay a 40% tax on the difference between the selling price and the asset’s book value at time of sale.

($ in thousands)

You work for Mattel, a profitable toy manufacturer, and you are negotiating with Warner Brothers for the rights to manufacture and sell Harry Potter lunchboxes (you already

sell related action figures). Your marketing department estimates that you can sell $800 million worth of lunchboxes per year for 3 years, starting next year. At the end of year

3, you will liquidate the assets of the business.

Given the following information about this new product investment, identify the relevant cash flows, and calculate the investment’s net present value, benefit-cost ratio, and

internal rate of return. Make whatever assumptions you feel necessary and explain them briefly.

Chapter 7 Problem 15 Suggested Answers

Given Data:

Marketing Research Costs, to date 20,000$

Initial cost of new equipment 300,000$

Licensing rights to use images (To be expensed for tax purposes at time 0) 350,000$

Expected life 5 yrs

Salvage value 0

Depreciation method Straight-line over 5 years to 0 salvage value

Selling price of new equipment in 3 years* 130,000$

Incremental annual sales 800,000$

Incremental annual production costs 200,000$

Incremental annual selling

and administrative costs 80,000$

Current annual overhead costs 200,000$

Immediate advertising expenses for launch (To be expensed for tax purposes at tme 0) 190,000$

Tax rate 40%

Working capital required, as a % of production costs 7.50%

Minimum required rate of return 10%

*The company must pay a 40% tax on the difference between the selling price and the asset’s book value at time of sale.

Assumptions and calculations:

Change in Net Working Capital Table: End of Year

0 1 2 3

NWC 15,000 15,000 15,000 0

Change in NWC 15,000 0 0 (15,000)

Using the information above, the cash flows from this project appear in the table below:

0 1 2 3

Plant and equipment (300,000)$ 126,000$

Initial cost of licensing rights after taxes (210,000)

Immediate advertising expenses after taxes (114,000)

Subtract increases in net working capital (15,000) – – 15,000

Total costs (639,000)$ 0 0

Total salvage value 141,000$

Sales 800,000$ 800,000$ 800,000$

Cost of sales (200,000) (200,000) (200,000)

Gross Profit 600,000 600,000 600,000

Selling and administrative expenses (80,000) (80,000) (80,000)

Operating Income 520,000 520,000 520,000

Depreciation (60,000) (60,000) (60,000)

EBIT 460,000 460,000 460,000

Tax at 40% (184,000) (184,000) (184,000)

Net Income 276,000 276,000 276,000

Add back depreciation 60,000 60,000 60,000

After-tax cash flow 336,000$ 336,000$ 336,000$

Free Cash Flow (639,000)$ 336,000$ 336,000$ 477,000$

Net Present Value 10% 302.52$ million

Benefit-cost ratio 1.47

Internal rate of return 33.7%

Year

($ in thousands)

The marketing research costs are sunk and therefore not incremental.

The current overhead is not incremental (it is incurred even without the project).

Straight-line depreciation of the equipment over five years = $300,000 / 5 = $60,000 per year. The sale of the equipment at the end of the 3rd year involves a profit equal to the selling price minus

the book value (130,000 – 120,000, where book value = 300,000 – 3*60,000). This profit is taxed at 40%, meaning the company pays $4,000 on sale, leaving a net cash receipt of $126,000.

Working capital of (.075)*(200,000)=15,000 must be invested immediately. Working capital levels do not change until liquidation of the business at the end of the third year, when the investment

is recouped in full.

($ in thousands)