Chapter 06 – Understanding Financial Markets and Institutions

LG5 6-12 Liquidity Premium Theory Based on economists’ forecasts and analysis, 1-year Treasury

bill rates and liquidity premiums for the next four years are expected to be as follows:

R1 = 1.25%

E(2r1) = 2.15% L2 = 0.08%

E(3r1) = 2.55% L3 = 0.10%

E(4r1) = 3.00% L4 = 0.15%

Chapter 06 – Understanding Financial Markets and Institutions

Yield to

Maturity

intermediate 6-13 Determinants of Interest Rates for Individual Securities Tom and Sue’s Flowers,

LG4 6-14 Determinants of Interest Rates for Individual Securities Nikki G’s Corporation’s 10-

LG4 6-15 Unbiased Expectations Theory Suppose we observe the following rates: 1R1 = 8 percent,

1R2 = 10 percent. If the unbiased expectations theory of the term structure of interest rates holds,

Chapter 06 – Understanding Financial Markets and Institutions

LG5 6-16 Unbiased Expectations Theory The Wall Street Journal reports that the rate on 4-year

Treasury securities is 1.60 percent and the rate on 5-year Treasury securities is 2.15 percent.

According to the unbiased expectations theories, what does the market expect the 1-year

Treasury rate to be four years from today, E(5r1)?

LG5 6-17 Liquidity Premium Theory The Wall Street Journal reports that the rate on 3-year

Treasury securities is 5.25 percent and the rate on 4-year Treasury securities is 5.50 percent. The

1-year interest rate expected in three years is, E(4r1), 6.10 percent. According to the liquidity

premium theories, what is the liquidity premium on the 4-year Treasury security, L4?

LG5 6-18 Liquidity Premium Theory Suppose we observe the following rates: 1R1 = 0.75 percent,

1R2 = 1.20 percent, and E(2r1) = 0.907 percent. If the liquidity premium theory of the term

structure of interest rates holds, what is the liquidity premium for year 2, L2?

LG6 6-19 Forecasting Interest Rates You note the following yield curve in The Wall Street Journal.

According to the unbiased expectations theory, what is the 1-year forward rate for the period

beginning one year from today, 2f1?

6-3

Chapter 06 – Understanding Financial Markets and Institutions

LG6 6-20 Forecasting Interest Rates On March 11, 20XX, the existing or current (spot) 1-, 2-, 3-,

and 4-year zero-coupon Treasury security rates were as follows:

advanced 6-21 Determinants of Interest Rates for Individual Securities The Wall Street Journal reports

problems that the current rate on 10-year Treasury bonds is 7.25 percent, on 20-year Treasury

LG4 6-22 Determinants of Interest Rates for Individual Securities The Wall Street Journal reports

that the current rate on 8-year Treasury bonds is 5.85 percent, on 15-year Treasury

LG4 6-23 Determinants of Interest Rates for Individual Securities The Wall Street Journal reports

LG4 6-24 Determinants of Interest Rates for Individual Securities The Wall Street Journal reports

Chapter 06 – Understanding Financial Markets and Institutions

LG5 6-25 Unbiased Expectations Theory Suppose we observe the 3-year Treasury security rate (1R3)

to be 8 percent, the expected 1-year rate next year,(E(2r1), to be 4 percent, and the expected 1-

year rate the following year, E(3r1), to be 6 percent. If the unbiased expectations theory of the

term structure of interest rates holds, what is the 1-year Treasury security rate, 1R1?

LG5 6-26 Unbiased Expectations Theory The Wall Street Journal reports that the rate on 3-year

Treasury securities is 1.20 percent and the rate on 5-year Treasury securities is 2.15 percent.

According to the unbiased expectations theories, what does the market expect the 2-year

Treasury rate to be three years from today, E(3r2)?

LG6 6-27 Forecasting Interest Rates Assume the current interest rate on a 1-year Treasury bond

(1R1) is 4.50 percent, the current rate on a 2-year Treasury bond (1R2) is 5.25 percent, and the

current rate on a 3-year Treasury bond (1R3) is 6.50 percent. If the unbiased expectations theory

of the term structure of interest rates is correct, what is the 1-year forward rate expected on

Treasury bills during year 3, 3f1?

LG6 6-28 Forecasting Interest Rates A recent edition of The Wall Street Journal reported interest

rates of 1.25 percent, 1.60 percent, 1.98 percent, and 2.25 percent for three-year, four-year, five-

year, and six-year Treasury security yields, respectively, According to the unbiased expectation

theory of the term structure of interest rates, what are the expected one-year forward rates for

years 4, 5, and 6?

Chapter 06 – Understanding Financial Markets and Institutions

research it! Spreads

Go to the Federal Reserve Board’s Web site at www.federalreserve.gov and get the latest rates

on 10-year T-bills and Aaa- and Baa-rated corporate bonds using the following steps.

Go to the Federal Reserve’s Web site at www.federalreserve.gov . Click on “Economic Research

and Data,” then click on “Selected Interest Rates – H.15.” Click on the most recent date. This

will bring the file onto your computer that contains the relevant data. Click on “Historical Data”

and then “10-year” under “Treasury constant maturities,” or “Aaa” and “Baa” under “Corporate

bonds” to get past data. Calculate the current spread of Aaa- and Baa-rated bonds over the 10-

year Treasury-bond rate. How have these spreads changed over the last two years?

integrated mini-case: Calculating Interest Rates

From discussions with your broker, you have determined that the expected inflation premium is

Further, the maturity risk premium on PeeWee bonds is 0.1875 percent per year starting in year

2. PeeWee’s default risk premium and liquidity risk premium do not change with bond maturity.

Chapter 06 – Understanding Financial Markets and Institutions

a. What is the fair interest rate on 5-year Treasury securities?

b. What is the fair interest rate on PeeWee Corporation 5-year bonds?

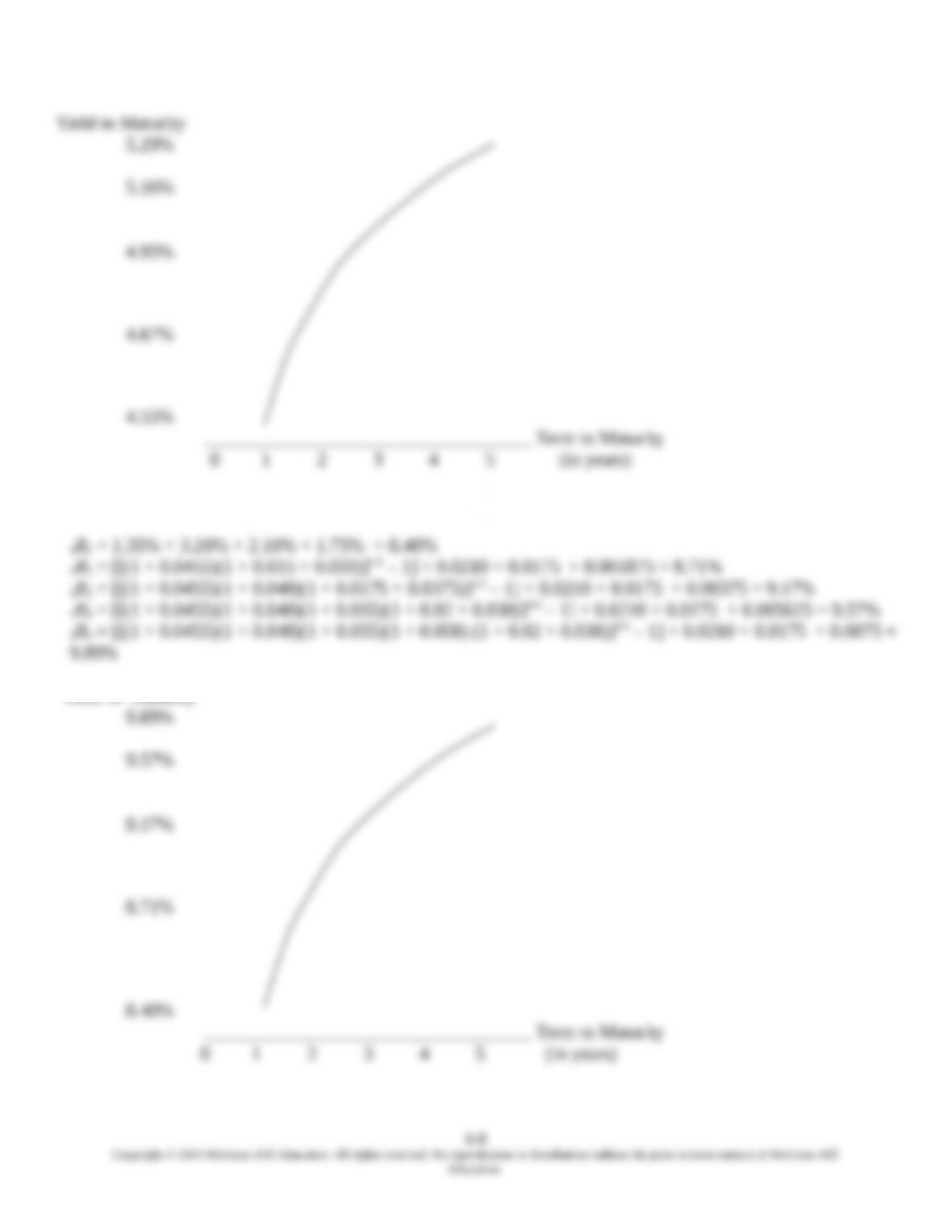

c. Plot the 5-year yield curve for the Treasury securities.

d. Plot the 5-year yield curve for the PeeWee Corporation bonds.

SOLUTION:

a. What is the fair interest rate on 5-year Treasury securities?

c. Plot the 5-year yield curve for the Treasury securities.

Chapter 06 – Understanding Financial Markets and Institutions

d. Plot the 5-year yield curve for the PeeWee Corporation bonds.