Chapter 06 – Understanding Financial Markets and Institutions

CHAPTER 6 – UNDERSTANDING FINANCIAL MARKETS AND INSTITUTIONS

questions

LG1 1. Classify the following transactions as taking place in the primary or secondary markets:

LG2 2. Classify the following financial instruments as money market securities or capital market

LG3 3. What are the different types of financial institutions? Include a description of the main

services offered by each.

The different types of financial institutions are:

Chapter 06 – Understanding Financial Markets and Institutions

LG3 4. How would economic transactions between suppliers of funds (e.g., households) and users of

funds (e.g., corporations) occur in a world without FIs?

LG3 5. Why would a world limited to the direct transfer of funds from suppliers of funds to users of

funds likely result in quite low levels of fund flows?

In this economy without FIs, the amount of funds flowing between fund suppliers and fund users

Chapter 06 – Understanding Financial Markets and Institutions

Second, many financial claims feature a long-term commitment (e.g., mortgages, corporate

stock, and bonds) for fund suppliers, thus creating another disincentive for fund suppliers to hold

LG3 6. How do FIs reduce monitoring costs associated with the flow of funds from fund suppliers to

fund users?

Chapter 06 – Understanding Financial Markets and Institutions

LG3 7. How do FIs alleviate the problem of liquidity risk faced by investors wishing to invest in

securities of corporations?

LG4 8. What are six factors that determine the nominal interest rate on a security?

LG4 9. What should happen to a security’s equilibrium interest rate as the security’s liquidity risk

increases?

LG5 10. Discuss and compare the three explanations for the shape of the yield curve.

Explanations for the yield curve’s shape fall predominantly into three categories: the unbiased

expectations theory, the liquidity premium theory, and the market segmentation theory.

Chapter 06 – Understanding Financial Markets and Institutions

LG5 11. Are the unbiased expectations and liquidity premium theories explanations for the shape of

the yield curve completely independent theories? Explain why or why not.

LG6 12. What is a forward interest rate?

LG6 13. If we observe a 1-year Treasury security rate that is higher than the 2-year Treasury security

rate, what can we infer about the 1-year rate expected one year from now?

problems

LG4 6-2 Determinants of Interest Rate for Individual Securities You are considering an

investment in 30-year bonds issued by Moore Corporation. The bonds have no special covenants.

The Wall Street Journal reports that 1-year T-bills are currently earning 1.25 percent. Your broker

has determined the following information about economic activity and Moore Corporation

bonds:

a. What is the inflation premium?

Chapter 06 – Understanding Financial Markets and Institutions

b. What is the fair interest rate on Moore Corporation 30-year bonds?

LG4 6-3 Determinants of Interest Rates for Individual Securities Dakota Corporation 15-year

bonds have an equilibrium rate of return of 8 percent. For all securities, the inflation risk

premium is 1.75 percent and the real risk free rate is 3.50 percent. The security’s liquidity risk

premium is 0.25 percent and maturity risk premium is 0.85 percent. The security has no special

covenants. Calculate the bond’s default risk premium.

LG4 6-4 Determinants of Interest Rates for Individual Securities A 2-year Treasury security

currently earns 1.94 percent. Over the next two years, the real risk free rate is expected to be 1.00

percent per year and the inflation premium is expected to be 0.50 percent per year. Calculate the

maturity risk premium on the 2-year Treasury security.

LG5 6-5 Unbiased Expectations Theory Suppose that the current 1-year rate (1-year spot rate) and

expected 1-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively)

are as follows:

Using the unbiased expectations theory, calculate the current (long-term) rates for 1-, 2-, 3-, and

4-year-maturity Treasury securities. Plot the resulting yield curve.

Yield to

Maturity

6-6

LG5 6-6 Unbiased Expectations Theory Suppose that the current 1-year rate (1-year spot rate) and

expected 1-year T-bill rates over the following three years (i.e., years 2, 3, and 4, respectively)

Using the unbiased expectations theory, calculate the current (long-term) rates for 1-, 2-, 3-, and

4-year-maturity Treasury securities. Plot the resulting yield curve.

LG5 6-7 Unbiased Expectations Theory One-year Treasury bills currently earn 1.45 percent. You

expected that one year from now, 1-year Treasury bill rates will increase to 1.65 percent. If the

unbiased expectations theory is correct, what should the current rate be on 2-year Treasury

securities?

Chapter 06 – Understanding Financial Markets and Institutions

LG5 6-8 Unbiased Expectations Theory One-year Treasury bills currently earn 2.15 percent. You

expected that one year from now, 1-year Treasury bill rates will increase to 2.65 percent and that

two years from now, 1-year Treasury bill rates will increase to 3.05 percent. If the unbiased

expectations theory is correct, what should the current rate be on 3-year Treasury securities?

LG5 6-9 Liquidity Premium Theory One-year Treasury bills currently earn 3.45 percent. You

expected that one year from now, 1-year Treasury bill rates will increase to 3.65 percent. The

liquidity premium on 2-year securities is 0.05 percent. If the liquidity premium theory is correct,

what should the current rate be on 2-year Treasury securities?

LG5 6-10 Liquidity Premium Theory One-year Treasury bills currently earn 2.25 percent. You

expected that one year from now, 1-year Treasury bill rates will increase to 2.45 percent and that

two years from now, 1-year Treasury bill rates will increase to 2.95 percent. The liquidity

premium on 2-year securities is 0.05 percent and on 3-year securities is 0.15 percent. If the

liquidity premium theory is correct, what should the current rate be on 3-year Treasury

securities?

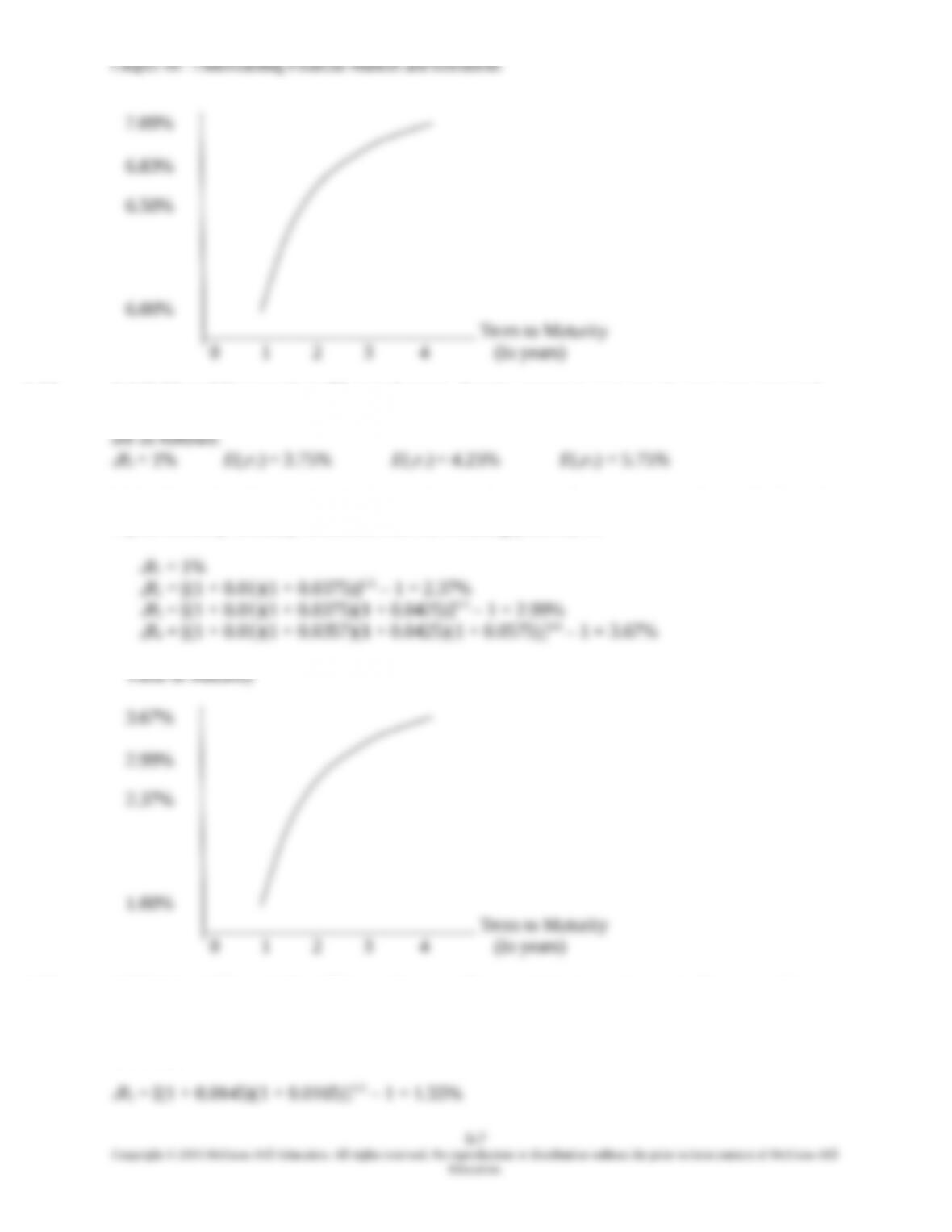

LG5 6-11 Liquidity Premium Theory Based on economists’ forecasts and analysis, 1-year Treasury

bill rates and liquidity premiums for the next four years are expected to be as follows:

R1 = 0.65%

E(2r1) = 1.75% L2 = 0.05%

E(3r1) = 1.85% L3 = 0.10%

E(4r1) = 2.15% L4 = 0.12%

Chapter 06 – Understanding Financial Markets and Institutions