LG5 20-18 Calculation of Altman’s Z-Score: Use the following financial statements for

Garners’ Platoon Mental Health Care, Inc., to calculate and interpret the Altman’s Z-score for this

firm.

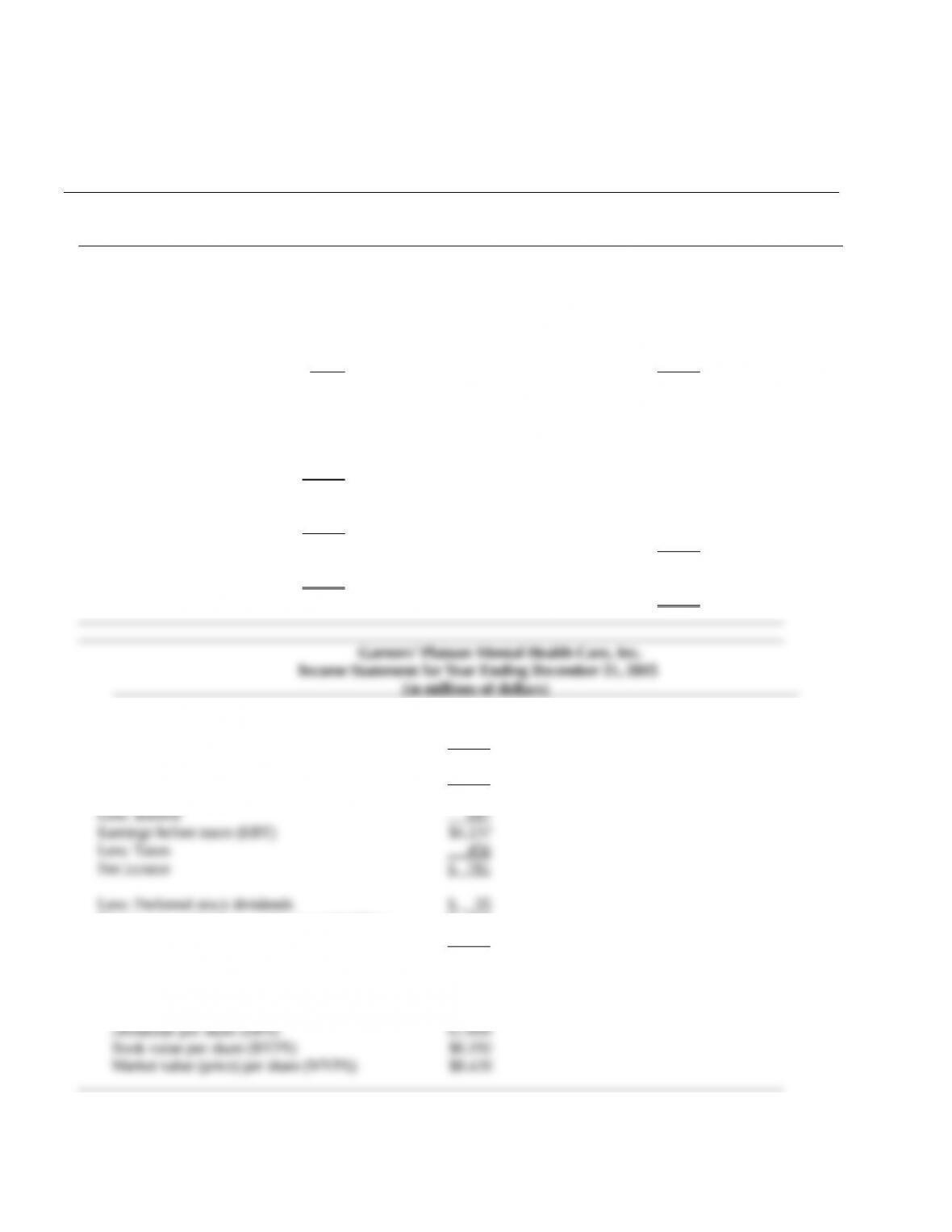

Garners’ Platoon Mental Health Care, Inc.

Balance Sheet as of December 31, 2015

(in millions of dollars)

Assets Liabilities and Equity

Current assets: Current liabilities :

Cash and marketable Accrued wages and

securities $ 247 taxes $ 186

Accounts receivable 652 Accounts payable 510

Inventory 1,035 Notes payable 513

Total $1,934 Total $1,209

Fixed assets: Long-term debt: $1,818

Gross plant and

equipment $3,419 Stockholders’ equity:

Less: Depreciation 494 Preferred stock (35 million shares) $ 35

Net plant and Common stock and

equipment $2,925 paid-in surplus 375

Other long-term assets 525 (375 million shares)

Total $3,450 Retained earnings 1,947

Total $2,357

Total assets $5,384

Total liabilities and equity $5,384

Net sales (all credit) $2,964

Less: Cost of goods sold 1,420

Gross profits $1,544

Less: Depreciation and other operating expenses 120

Earnings before interest and taxes (EBIT) $1,424

Net income available to common stockholders $ 746

Less: Common stock dividends $ 375

Addition to retained earnings $ 371

Per (common) share data:

Earnings per share (EPS) $1.989

X1 = Net working capital/Total assets = ($1,934m – $1,209m) / $5,384m = 0.1347

LG5 20-19 Calculation of Bankruptcy Probability Suppose a linear probability model you have

developed finds there are two factors influencing the past bankruptcy behavior of firms: the debt

ratio and the profit margin. Based on past bankruptcy experience, the linear probability model is

estimated as:

LG5 20-20 Calculation of Bankruptcy Probability A linear probability model you have developed

finds there are two factors influencing the past bankruptcy behavior of firms: the equity

multiplier and the total asset turnover ratio. Based on past bankruptcy experience, the linear

probability model is estimated as:

advanced

problems

LG1 20-21 Economies of Scope A survey of a local market has provided the following average cost data:

Johnson Construction Corp. (JCC) has assets of $3 million and an average cost of 20 percent.

Anderson Architects (AA) has assets of $4 million and an average cost of 30 percent. Cole Home

Builders (CHB) has assets of $4 million and an average cost of 25 percent. For each firm, average

costs are measured as a proportion of assets. JCC is planning to acquire AA and CHB with the

expectation of reducing overall average costs by eliminating the duplication of services.

a. What should the average cost after the acquisition be for JCC to justify this merger?

b. If JCC plans to reduce operating costs by $500,000 after the merger, what will the average cost be

for the new firm?

LG1 20-22 Economies of Scope A survey of a national market has provided the following average cost

data: Jackson County Construction (JCC) has assets of $2.55 million and an average cost of 30

percent. Arkansas Architects (AA) has assets of $1.7 million and an average cost of 25 percent.

Colorado Home Builders (CHB) has assets of $1 million and an average cost of 15 percent. For each

firm, average costs are measured as a proportion of assets. JCC is planning to acquire AA and CHB

with the expectation of reducing overall average costs by eliminating the duplication of services.

a. What should the average cost after the acquisition be for JCC to justify this merger?

b. If JCC plans to reduce operating costs by $425,000 after the merger, what will the average cost be

for the new firm?

Average cost:

The average cost after merger = $0.915m / $5.250m = 17.43 percent

LG2 20-23 Calculation of Change in the HHI Associated with a Merger Cakes, Corp. currently

has a 60 percent market share in banking services, followed by Cookies, Inc., with 20 percent

and Dippen Dough with 20 percent.

a. What is the concentration ratio as measured by the Herfindahl-Hirschman Index (HHI)?

b. If Cakes, Corp. acquires Cookies, Inc., what will be the new HHI?

c. Assume the Justice department will allow mergers as long as the changes in HHI do not

exceed 1,400. What is the minimum amount of assets that Cakes, Corp will have to divest after it

merges with Cookies, Inc.?

If the merger stands with no adjustment, then X = 80 and Y = 0. But some portion of X must be

Using the formula: Q =

2a

4ac) –

b

( b–

2/1

2

, we get Q = 73.1662 percent, which means Cakes,

LG2 20-24 Calculation of Change in the HHI Associated with a Merger Tractor Supply, Corp.

currently has a 50 percent market share in banking services, followed by Farm Equipment, Inc.,

with 30 percent and Plow Mart with 20 percent.

a. What is the concentration ratio as measured by the Herfindahl-Hirschman Index (HHI)?

b. If Tractor Supply, Corp. acquires Plow Mart, Inc., what will be the new HHI?

c. Assume the Justice department will allow mergers as long as the changes in HHI do not

exceed 1,500. What is the minimum amount of assets that Tractor, Corp will have to divest after

it merges with Plow Mart, Inc.?

If the merger stands with no adjustment, then X = 70 and Z = 0. But some portion of X must be

LG3 20-25 Valuation of a Merger The managers of BSW, Inc. have approached KCMP Corp. about a

possible merger. KCMP Corp. is asking a price of $72 million to be purchased by BSW, Inc. KCMP

Corp. currently has total cash flows of $6 million that are expected to grow at two percent annually

$7.12m $7.27m ?

Present value of cash flows = ———- + ———— + ————- + $54.09m = $72m

from the merger (1.10)1 (1.10)2 (1.10)3

LG3 20-26 Valuation of a Merger The managers of State Bank have been approached by City Bank about

a possible merger. State Bank is asking a price of $205 million to be purchased by City Bank. State

Bank currently has total cash flows of $15 million that are expected to grow at 1 percent annually for

the next two years. Managers are uncertain of the growth in State Bank’s cash flows in year 3.

Managers estimate that because of synergies the merged firm’s cash flows will increase by an

additional $1.5 million in the first year after the merger and these cash flows will grow by 5 percent

in years 2 and 3 following the merger. Managers have estimated that the present value of any

incremental cash flows received after year three is $158.75 million. The WACC for the merged firms

is 8 percent. Calculate State Bank’s minimum incremental cash flow needed in year 3 after the

merger such that City Bank would see this merger as a positive NPV project.

The incremental cash flows for the first three years after the merger are:

Year after merger 1 2 3

Cash flow from State Bank $15m(1.01) $15m(1.01)2 ?

This merger would be beneficial for the stockholders of the bidder firm if, in year 3 after the

merger, State Bank’s incremental cash flows in year 3 were $18.96 million.

LG5 20-27 Calculating the Probability of Bankruptcy A linear probability model you have

developed finds there are two factors influencing the past bankruptcy behavior of firms: the debt-

to-equity ratio and the sales-to-total assets ratio. Based on past bankruptcy experience, the linear

probability model is estimated as:

LG5 20-28 Calculating the Probability of Bankruptcy A linear probability model you have

developed finds there are two factors influencing the past bankruptcy behavior of firms: the debt-

to-equity ratio and the profit margin. Based on past bankruptcy experience, the linear probability

model is estimated as:

research it! Mergers and Acquisitions

Go to the Thomson Financial—Investment Banking and Capital Markets Group website at

http://dmi.thomsonreuters.com/DealsIntelligence and find the latest information available for

the dollar value of mergers and acquisition activity using the following steps. Click on

“QUARTERLY REVIEWS.” Under “MERGERS & ACQUISITIONS,” click on “Global M&A

Financial Advisory,” the most recent quarter. This will download a file on to your computer that

will contain the most recent information on merger and acquisition activity. What is the most

recent dollar value of global merger and acquisition activity undertaken? Who are the top

advisors on these merger and acquisition deals? How has the top advisor market share changed in

the last year?

integrated mini-case: Capital Funding in a Public Firm

Disaster Airlines is a firm in severe financial distress. The firm can no longer pay its bills on time

and it is far behind on payments to its banks and long-term debt holders. The firm has decided to

ether be purchased by another air carrier or liquidate its assets and close. The managers have

approached Altruistic Airlines about being acquired. After examining Disaster’s

financial statements, looking at the routes owned by Disaster, and looking at the condition of the

fixed assets, Altruistic Airlines has offered to pay the stockholders of Disaster Airlines $8 million

to be acquired. Disaster Airlines covers flights to both areas in which Altruistic already flies, but

also has routes in areas into which Altruistic is interested in expanding. As part of the analysis,

Altruistic determined that the additional cash flows resulting from the acquisition would total

$500,000 this year and would grow at a rate of 4 percent for the next three years. After this time

the cash flows would grow at a rate of two percent annually. The WACC of Altruistic Airlines

would be 8 percent after the merger.

If, instead, Disaster Airlines decides to liquidate its assets, it will pay off its debt and give

any remaining funds to the firm’s stockholders. Disaster Airlines’ balance sheet is listed as

follows.

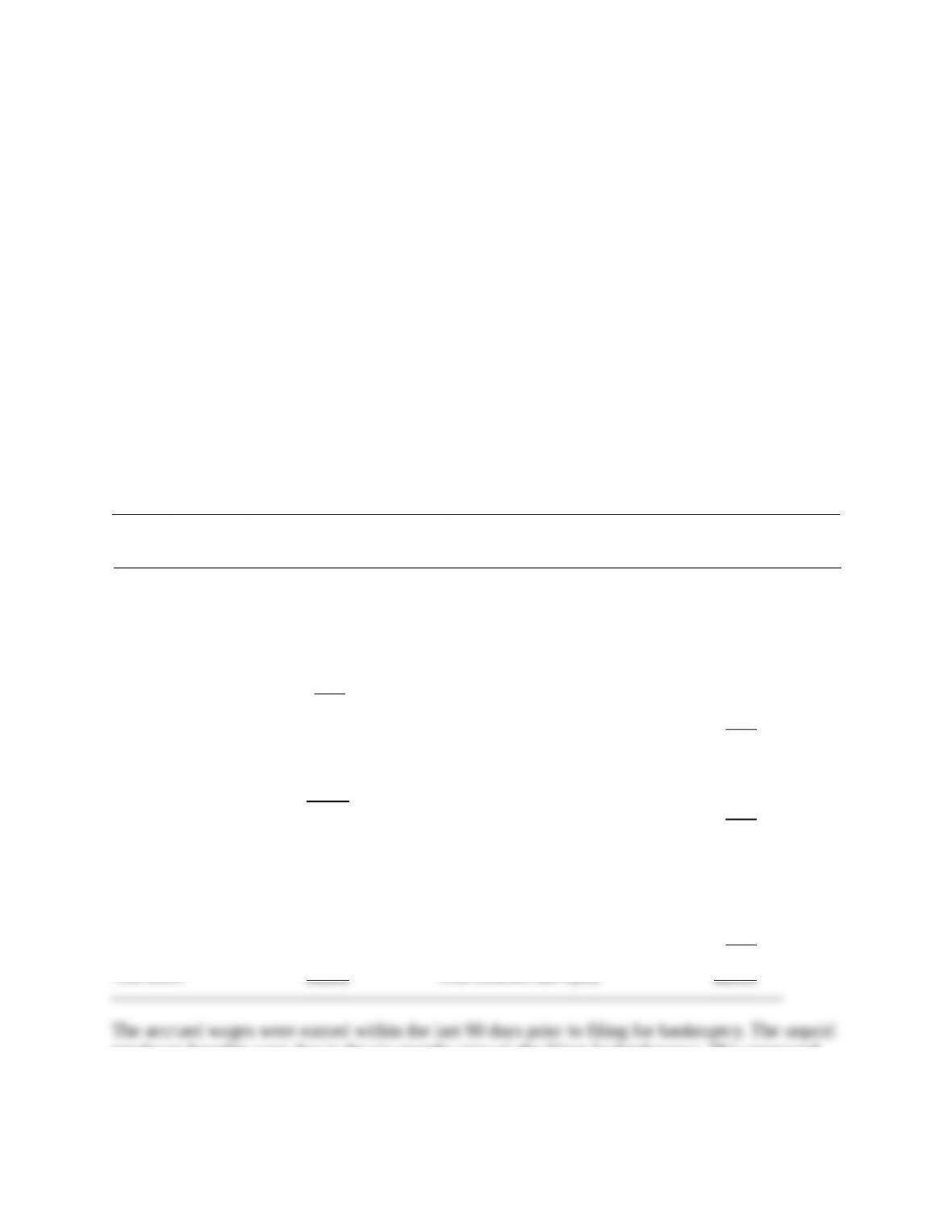

Disaster Airlines, Inc.

Balance Sheet as of June 25, 2015

(in millions of dollars)

Assets Liabilities and Equity

Current assets: Current liabilities:

Cash and marketable Accrued wages (2,500 employees) $ 4

securities $ 63 Unpaid employee benefits 3

Accounts receivable 28 Unsecured customer deposits 6

Inventory 100 Accrued taxes 22

Total $ 191 Accounts payable 157

Notes payable to banks 211

Fixed assets: Total $ 403

Gross plant and

equipment $1,152 Long-term Debt:

Less: Depreciation 248 First mortgage $ 160

Net plant and Subordinate debentures 412

equipment $ 904 Total $ 572

Stockholders’ equity:

Common stock and

paid-in surplus $ 100

(100 million shares)

Retained earnings 20

Total $ 120

employee benefits were due in the six months prior to the filing for bankruptcy. The unsecured

customer deposits are for less than $900 each. Disaster Airlines has no property taxes past due.

The first mortgage is secured against the fixed assets of the firm. The debentures are subordinate

to the notes payable to banks. The liquidation of the firm’s current assets produced $186 million

and of the firm’s fixed assets produced $800 million for a total of only $986 million in funds to

distribute to the creditors and stockholders of the firm.

The administrative expenses associated with the bankruptcy totaled $1 million and

unpaid expenses incurred after the filing of the bankruptcy petition but before the trustee was

appointed totaled $5 million.

Show which method of dissolution, an acquisition by Altruistic Airlines or a liquidation

of assets, is more beneficial for the creditors and stockholders of Disaster Airlines and the

stockholders of Altruistic Airlines.

SOLUTION: The distribution of the $986 million of funds is as follows:

Proceeds from liquidation of assets: $986m

Administrative expenses associated with the bankruptcy proceedings 1m

Unpaid expenses incurred after the filing of the bankruptcy petition but

before the trustee is appointed 5m

Wages due to employees (2,500 employees) 4m

Unpaid employee benefit plan contributions 3m

Unsecured customer claims 6m

Taxes due to federal, state, and other governmental agencies 22m

Funds available for secured creditors: $945m

First mortgage 160m

Funds available for unsecured creditors: $785m

The remaining $785 million is distributed to the unsecured creditors on a pro rata basis, with

senior creditors paid in full before subordinate creditors. Thus,

Settlement Percent of claim

Unsecured Creditors Amount at 100% a

received

Accounts payable $157m $157m 100%

Notes payable to banks 211m 211m 100

Subordinate debentures 412m 412m 100

Total $780m $780m

a $785 million is available to pay $780 million in unsecured creditors. Thus, the pro rata settlement rate is $780m/

$780m = 100%.

The remaining $5 million ($785m – $780m) goes to the firm’s common stockholders.

Altruistic Airlines has offered the shareholders of Disaster Airlines $8 million to be acquired.

Thus, the shareholders of Disaster Airlines would be better to take this offer to be acquired rather

than liquidate the firm’s assets. The shareholders of Disaster would receive an additional $3

million ($8m – $5m) with the acquisition compared to the liquidation of assets.

The incremental cash flows for the first three years after the merger are:

Year after merger 1 2 3

Cash flows $0.50m(1.04)1 $0.50m(1.04)2