Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

CHAPTER 16 – ASSESSING LONG-TERM DEBT, EQUITY, AND CAPITAL

STRUCTURE

Questions

LG1 1. How will passive and active capital structure changes differ?

Active capital structure changes will be initiated immediately, regardless of whether

LG2 2. Why is debt often referred to as leverage in finance?

LG3 3. In M&M’s perfect world, will the debt holders ever bear any of the risk of the firm?

LG4 4. Why does allowing for the existence of corporate taxation cause firms to prefer the

maximum amount of debt possible?

LG5 5. If a firm increased the amount of debt in its capital structure, but a shareholder

wanted to switch back to the mixture of expected return and risk she had before the

LG5 6. If an investor wanted to reduce the risk of a levered stock in their portfolio, how

LG6 7. Suppose you were the financial manager for a firm and were considering a

proposed increase in the amount of debt in the firm’s capital structure. If you thought the

firm was going to consistently earn a level of EBIT above its break-even level of EBIT

16-1

Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

LG7 8. Explain why, in a world with both corporate taxes and the chance of bankruptcy, a

LG7 9. If the U.S. government completely eliminated taxation at the corporate level, how

LG8 10. Would you expect a utility company to have high or low debt levels? Why?

problems

basic problems

LG3 0-1 Capital Structure Weights Suppose that Lil John Industries’ equity is currently

selling for $37 per share and that there are 2 million shares outstanding. If the firm also

has 30 thousand bonds outstanding, which are selling at 103 percent of par, what are the

firm’s current capital structure weights?

2,000, 000 $37 70.54%

2,000, 000 $37 30, 000 $1,000 1.03

30, 000 $1,000 1.03 29.46%

2,000, 000 $37 30, 000 $1,000 1.03

E

E D

D

E D

´

= =

+ ´ + ´ ´

´ ´

= =

+ ´ + ´ ´

LG3 0-2 Capital Structure Weights Suppose that Papa Bell, Inc.’s, equity is currently

selling for $55 per share, with 4 million shares outstanding. If the firm also has 17

thousand bonds outstanding, which are selling at 94 percent of par, what are the firm’s

current capital structure weights?

16-2

Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

4,000,000 $55 93.23%

4,000,000 $55 17,000 $1,000 0.94

17,000 $1,000 0.94 6.77%

4,000,000 $55 17,000 $1,000 0.94

E

E D

D

E D

´

= =

+ ´ + ´ ´

´ ´

= =

+ ´ + ´ ´

LG1 0-3 Restructuring Strategy Suppose that Lil John Industries’ equity is currently selling

for $27 per share and that there are 2 million shares outstanding. The firm also has 50

thousand bonds outstanding, which are selling at 103 percent of par. If Lil John was

considering an active change to their capital structure so that the firm would have a D/E of

1.4, which type of security (stocks or bonds) would they need to sell to accomplish this,

and how much would they have to sell?

Using the capital structure weights formulas from Chapter 11, the current capital weights

are:

2,000, 000 $27 0.5118 or 51.18%

2,000,000 $27 50,000 $1,000 1.03

50,000 $1,000 1.03 0.4882 or 48.82%

2,000,000 $27 50,000 $1,000 1.03

E

E D

D

E D

´

= =

+ ´ + ´ ´

´ ´

= =

+ ´ + ´ ´

The current D/E ratio is 0.4882 / 0.5118 = 0.9537, so Lil John would be contemplating

increasing the D/E ratio. To do so, they would have to change their debt ratio to 1.4 / 2.4 =

0.5833, which would require issuing (0.5833 – 0.4882) × [($2,000,000 × $27) + (50,000 ×

LG1 0-4 Capital Structure Weights Suppose that Papa Bell, Inc.’s, equity is currently

selling for $45 per share, with 4 million shares outstanding. The firm also has seven

thousand bonds outstanding, which are selling at 94 percent of par. If Papa Bell was

considering an active change to their capital structure so as to have a D/E of 0.4, which

type of security (stocks or bonds) would they need to sell to accomplish this, and how

much would they have to sell?

Using the capital structure weights formulas from Chapter 11, the current capital weights

are:

4, 000, 000 $45 96.47%

4,000, 000 $45 7, 000 $1, 000 0.94

7,000 $1,000 0.94 3.53%

4,000, 000 $45 7, 000 $1, 000 0.94

E

E D

D

E D

´

= =

+ ´ + ´ ´

´ ´

= =

+ ´ + ´ ´

The current D/E ratio is 0.0353 / 0.9647 = 0.0366, so Lil John would be contemplating

increasing the D/E ratio. To do so, they would have to change their debt ratio to 0.4 / 1.4 =

16-3

intermediate problems

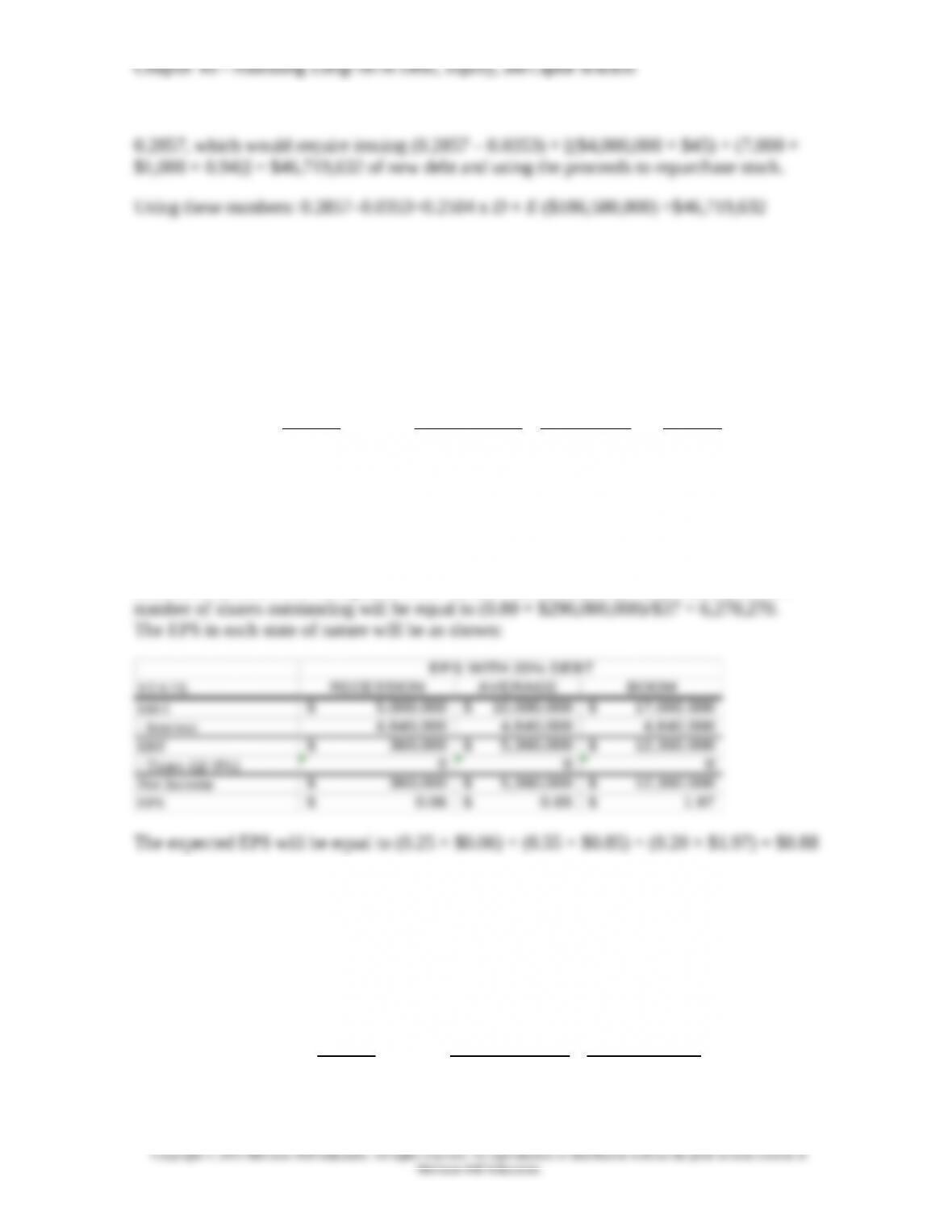

LG3 0-5 Expected EPS after Leveraging Daddi Mac, Inc., doesn’t face any taxes and has

$290 million in assets, currently financed entirely with equity. Equity is worth $37 per

share, and book value of equity is equal to market value of equity. Also, let’s assume that

the firm’s expected values for EBIT depend upon which state of the economy occurs this

year, with the possible values of EBIT and their associated probabilities shown as follows:

STATE RECESSION AVERAGE BOOM

Probability of state 0.25 0.55 0.20

Expected EBIT in state $5 million $10 million $17 million

The firm is considering switching to a 20 percent debt capital structure, and has determined

that they would have to pay an 8 percent yield on perpetual debt in either event. What will

be the level of expected EPS if they switch to the proposed capital structure?

Interest in all states will be equal to 0.08 × (0.20 × $290,000,000) = $4,640,000, and the

LG3 0-6 Expected EPS after Leveraging HiLo, Inc., doesn’t face any taxes and has $150

million in assets, currently financed entirely with equity. Equity is worth $7 per share, and

book value of equity is equal to market value of equity. Also, let’s assume that the firm’s

expected values for EBIT depend upon which state of the economy occurs this year, with

the possible values of EBIT and their associated probabilities shown as follows:

STATE PESSIMISTIC OPTIMISTIC

Probability of state 0.45 0.55

16-4

Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

Expected EBIT in state $5 million $19 million

The firm is considering switching to a 40 percent debt capital structure, and has determined

that they would have to pay a 12 percent yield on perpetual debt in either event. What will

be the level of expected EPS if they switch to the proposed capital structure?

Interest in all states will be equal to 0.12 × (0.40 × $150,000,000) = $7,200,000, and the

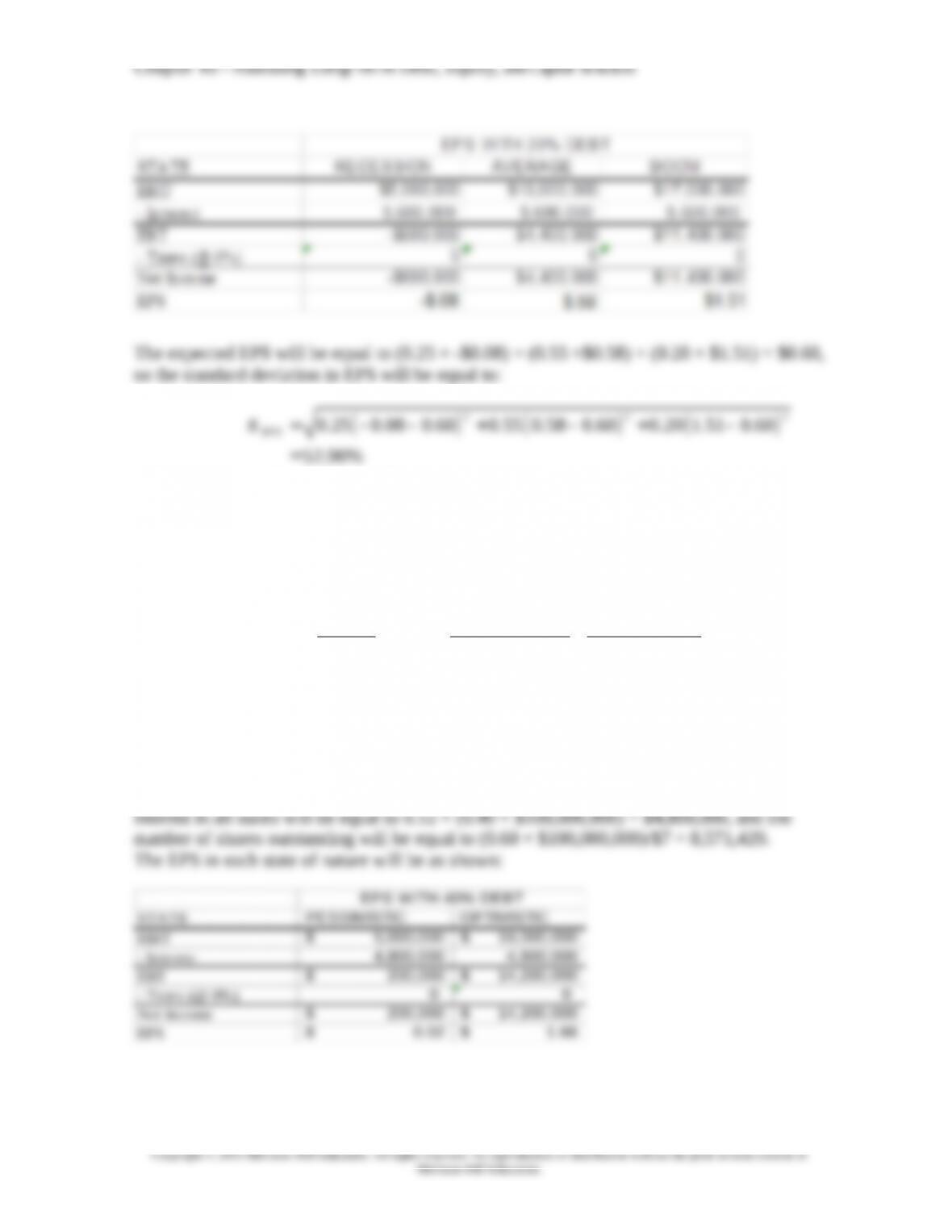

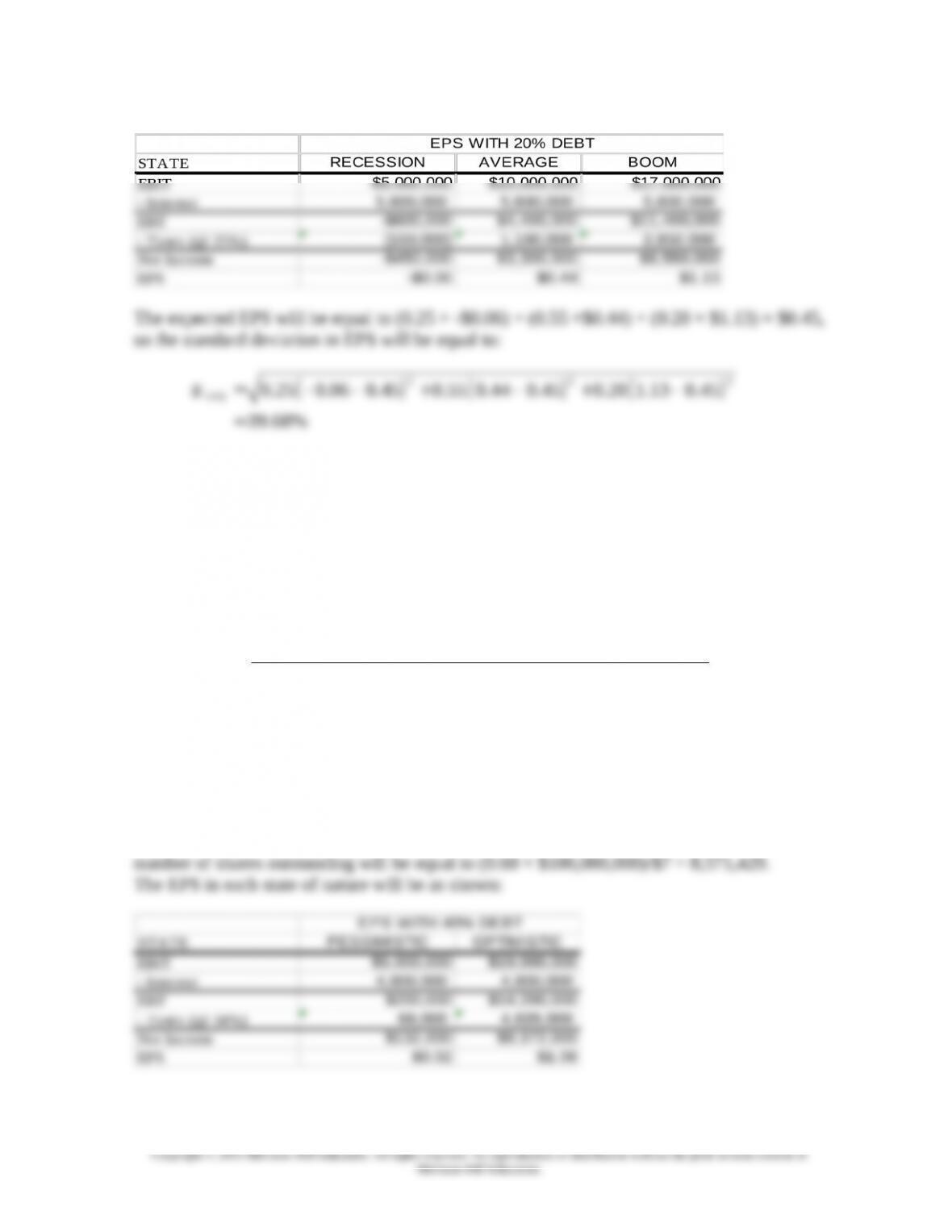

LG3 0-7 Standard Deviation in EPS after Leveraging Daddi Mac, Inc., doesn’t face any

taxes and has $350 million in assets, currently financed entirely with equity. Equity is

worth $37 per share, and book value of equity is equal to market value of equity. Also, let’s

assume that the firm’s expected values for EBIT are dependent upon which state of the

economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

STATE RECESSION AVERAGE BOOM

Probability of state 0.25 0.55 0.20

Expected EBIT in state $5 million $10 million $17 million

The firm is considering switching to a 20 percent debt capital structure, and has determined

that they would have to pay an 8 percent yield on perpetual debt regardless of whether they

change their capital structure. What will be the standard deviation in EPS if they switch to

the proposed capital structure?

16-5

advanced problems

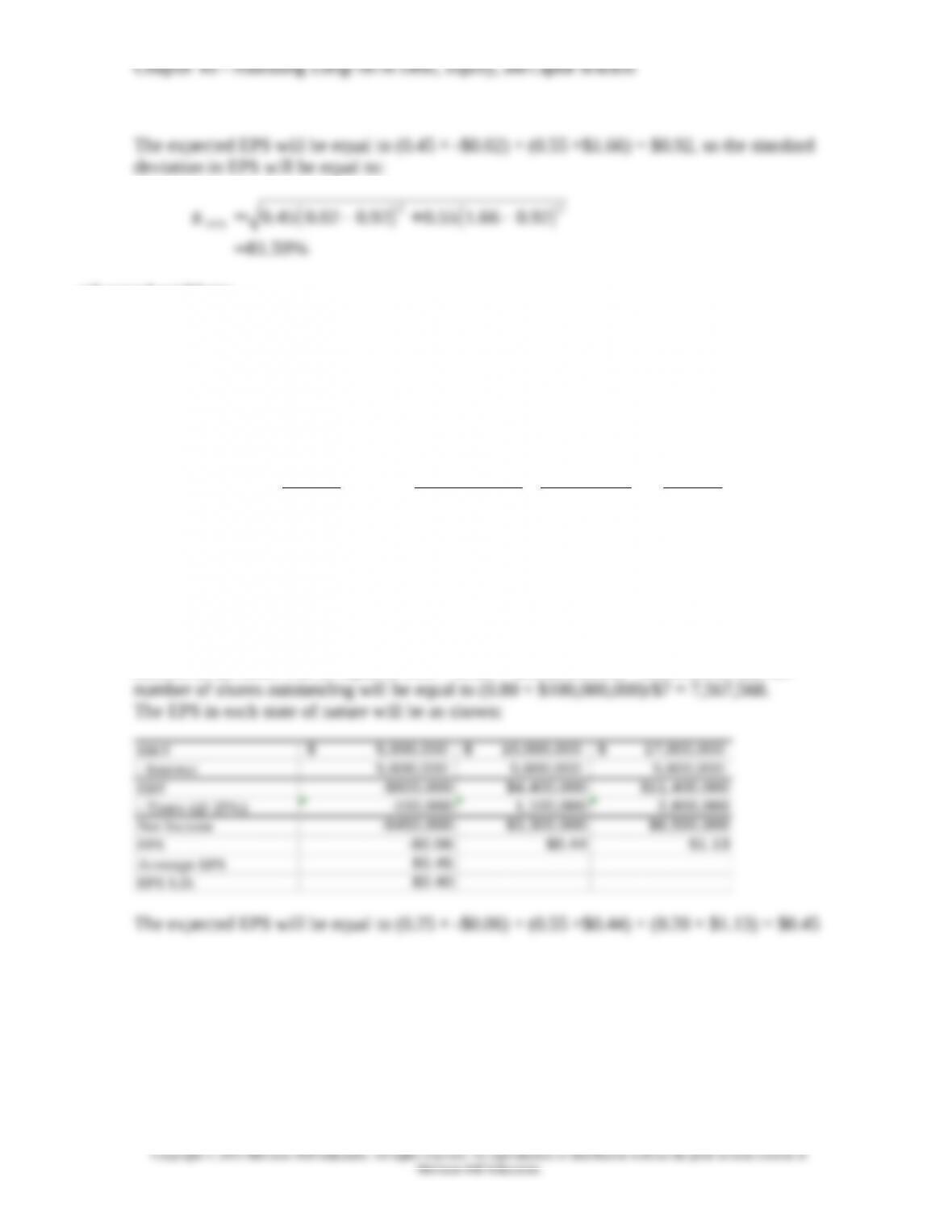

LG4 0-9 Expected EPS after Leveraging with Taxes NoNuns Cos. has a 25 percent tax rate

and has $350 million in assets, currently financed entirely with equity. Equity is worth $37

per share, and book value of equity is equal to market value of equity. Also, let’s assume

that the firm’s expected values for EBIT depend upon which state of the economy occurs

this year, with the possible values of EBIT and their associated probabilities shown as

follows:

STATE RECESSION AVERAGE BOOM

Probability of state 0.25 0.55 0.20

Expected EBIT in state $5 million $10 million $17 million

The firm is considering switching to a 20 percent debt capital structure, and has determined

that they would have to pay an 8 percent yield on perpetual debt in either event. What will

be the level of expected EPS if they switch to the proposed capital structure?

Interest in all states will be equal to 0.08 × (0.20 × $350,000,000) = $5,600,000, and the

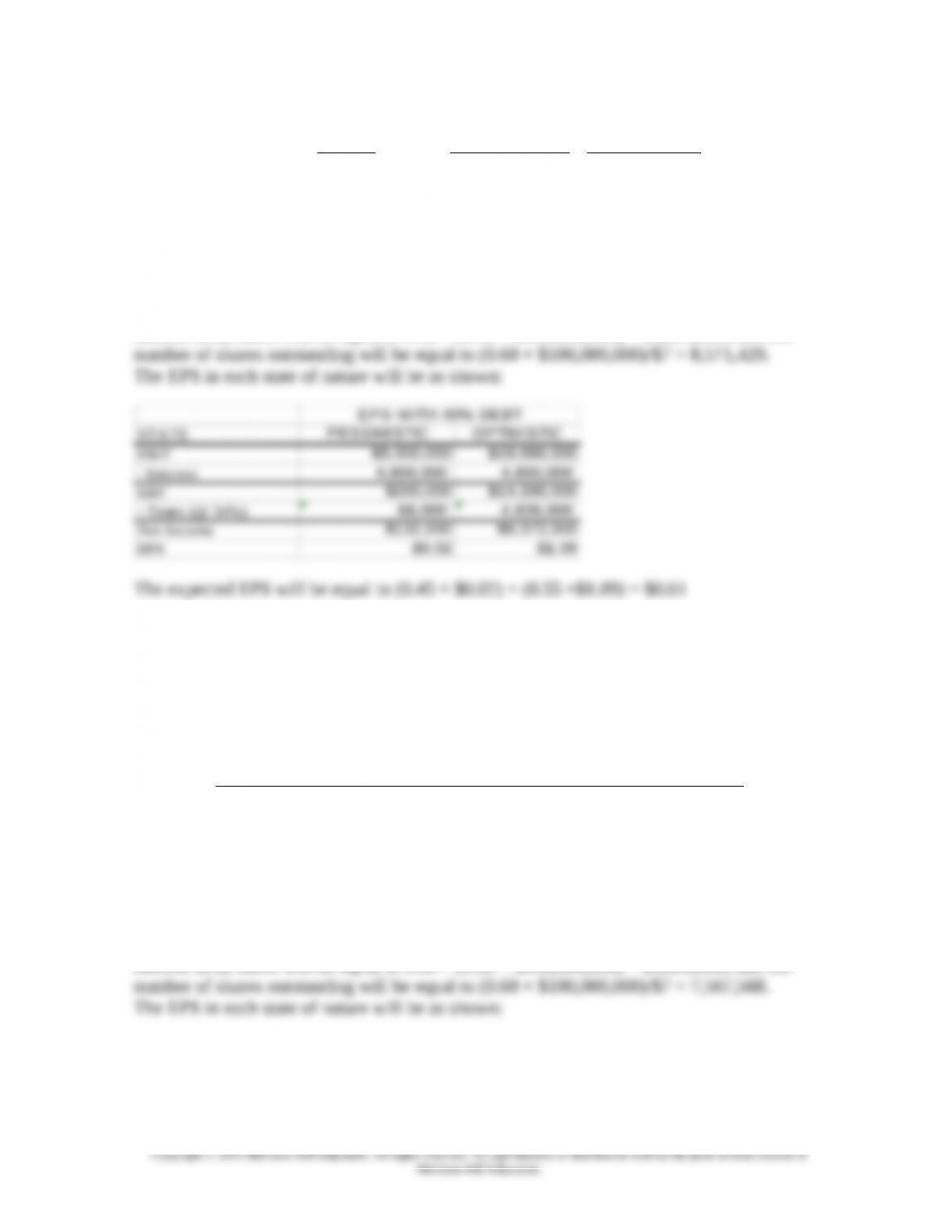

LG4 0-10 Expected EPS after Leveraging with Taxes GTB, Inc., has a 34 percent tax rate

and has $100 million in assets, currently financed entirely with equity. Equity is worth $7

per share, and book value of equity is equal to market value of equity. Also, let’s assume

that the firm’s expected values for EBIT depend upon which state of the economy occurs

this year, with the possible values of EBIT and their associated probabilities shown as

follows:

16-7

Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

STATE PESSIMISTIC OPTIMISTIC

Probability of state 0.45 0.55

Expected EBIT in state $5 million $19 million

The firm is considering switching to a 40 percent debt capital structure, and has determined

that they would have to pay a 12 percent yield on perpetual debt in either event. What will

be the level of expected EPS if they switch to the proposed capital structure?

LG4 0-11 Standard Deviation in EPS after Leveraging with Taxes NoNuns Cos. has

a 25 percent tax rate and has $350 million in assets, currently financed entirely with equity.

Equity is worth $37 per share, and book value of equity is equal to market value of equity.

Also, let’s assume that the firm’s expected values for EBIT depend upon which state of the

economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

STATE RECESSION AVERAGE BOOM

Probability of state 0.25 0.55 0.20

Expected EBIT in state $5 million $10 million $17 million

The firm is considering switching to a 20 percent debt capital structure, and has determined

that they would have to pay an 8 percent yield on perpetual debt in either event. What will

be the standard deviation in EPS if they switch to the proposed capital structure?

16-8

Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

Chapter 16 – Assessing Long-Term Debt, Equity, and Capital Structure

Expected EBIT in state $5 million $19 million

The firm is considering switching to a 40 percent debt capital structure, and has determined

that they would have to pay a 12 percent yield on perpetual debt in either event. What will

be the break-even level of EBIT?