LG4 15-1 Suppose that Wall-E Corp. currently has the following balance sheet, and that sales for

the year just ended were $7 million. The firm also has a profit margin of 27 percent, a

retention ratio of 20 percent, and expects sales of $9 million next year. Fixed assets are

currently fully utilized, and the nature of Wall-E’s fixed assets is such that they must be

added in $1 million increments. If current assets and current liabilities are expected to

grow with sales, what amount of additional funds will Wall-E need from external sources

to fund the expected growth?

Assets Liabilities and Equity

Current

assets $2,000,000 Current

liabilities $2,500,000

Fixed

assets 5,000,000 Long-term

debt 1,500,000

Equity 3,000,000

Total

assets $7,000,000

Total

liabilities

and equity

$7,000,000

In this case, the necessary increase in assets will be:

( )

*

0

Necessary increase in current assets

$2,000,000 $9,000,000 $7, 000,000

$7,000,000

$571, 429

AS

S

= ´ D

= ´ –

=

0

*

Necessary increase in fixed assets

$5,000,000 ($9,000,000 $7,000,000)

$7,000,000

$1, 428,571

AS

S

= ´ D

= ´ –

=

The necessary increase in fixed assets is $1,428,571. However, fixed assets must be

added in $1 million increments. Thus, the asset need for fixed assets must be increased to

$2 million.

The spontaneous increase in liabilities will be:

( )

*

0

Spontaneous increase in liabilities

$2,500,000 $9,000,000 $7, 000,000

$7,000,000

$714, 286

LS

S

= ´ D

= ´ –

=

The projected increase in retained earnings will be:

1

Projected increase in retained earnings

0.27 $9,000,000 0.20

$486,000

M S RR= ´ ´

= ´ ´

=

So AFN will be = $571,429 + $2,000,000 – $714,286 – $486,000 = $1,371,143

advanced

problems

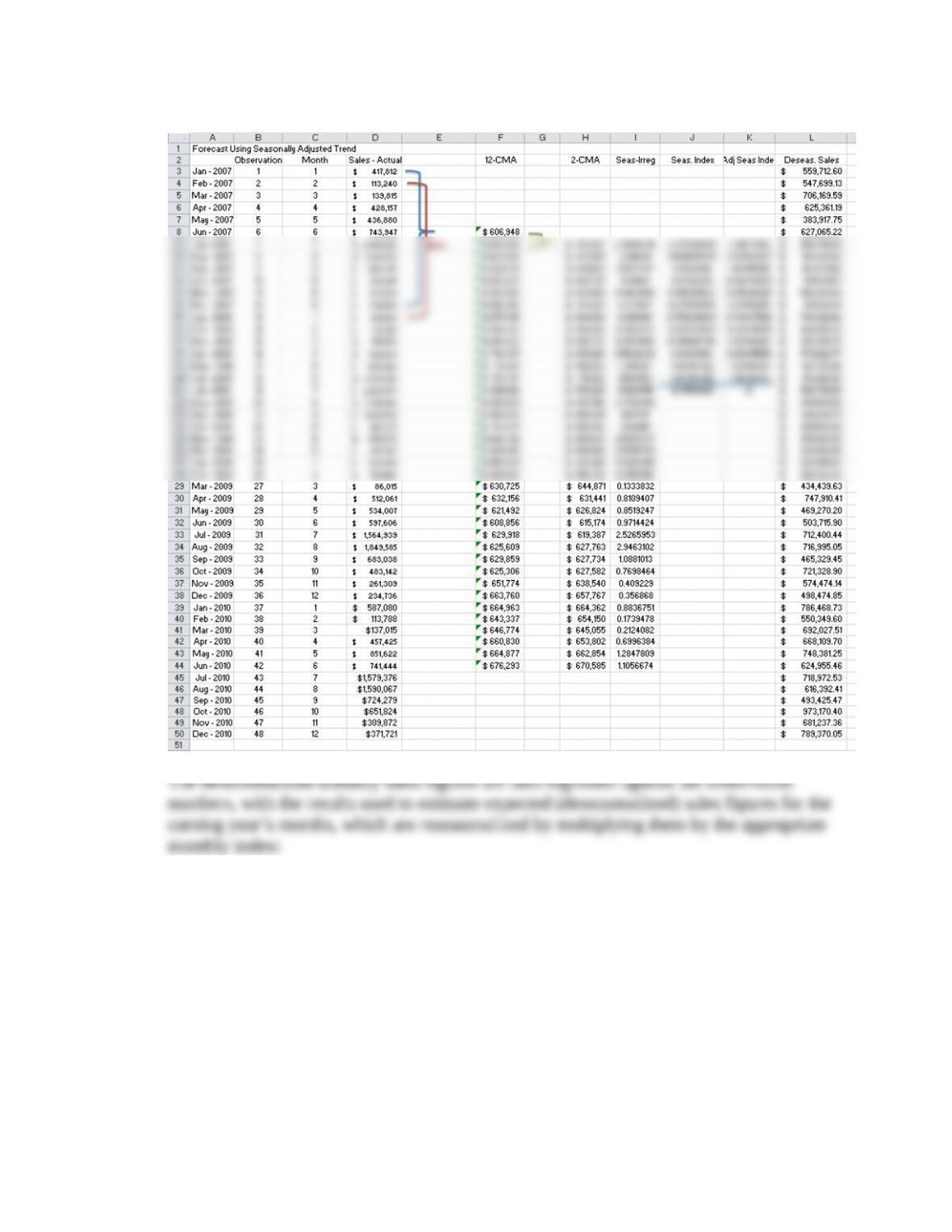

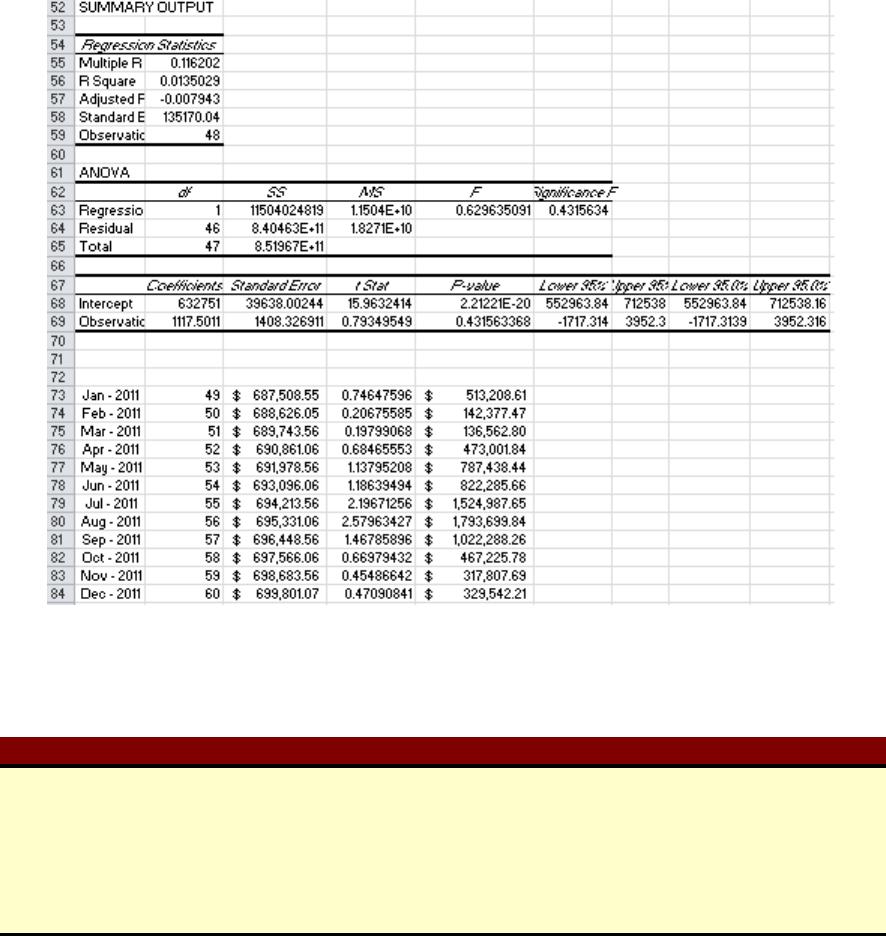

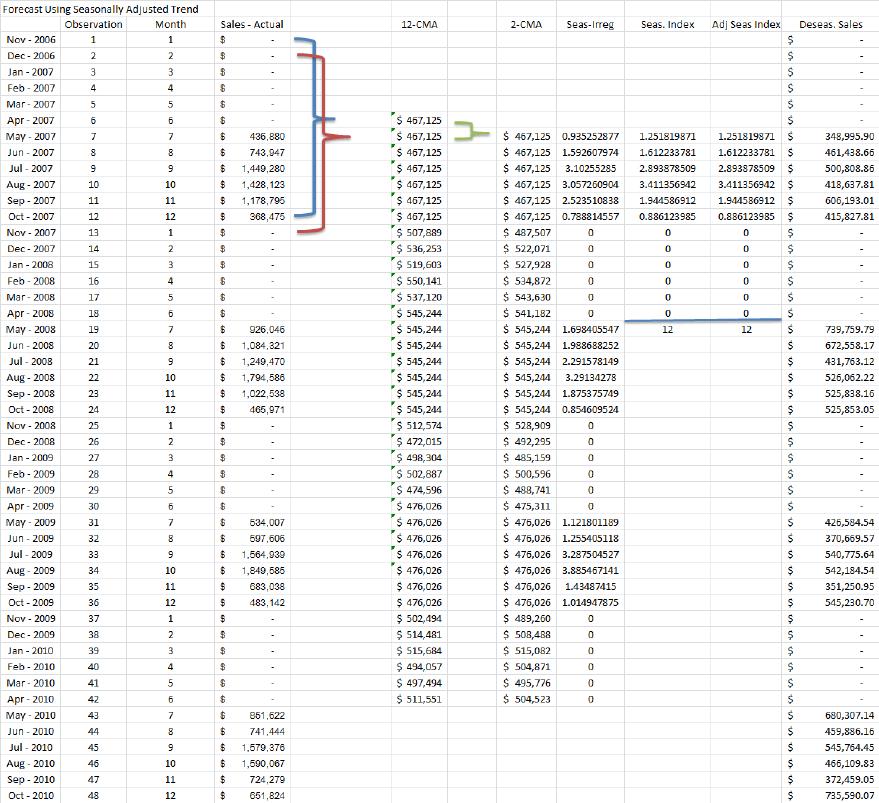

LG3 15-2John’s Bait and Fish shop has had the monthly sales amounts listed as follows for the last

four years. Assuming that there is both seasonality and a trend, estimate monthly sales

for each month of the coming year.

Year: 2010 2011 2012 2013

January $417,812 $585,558 $334,336 $587,080

February 113,240 138,414 165,492 113,788

March 139,815 177,676 86,015 137,015

April 428,157 392,734 512,061 457,425

May 436,880 926,046 534,007 851,622

June 743,947 1,084,321 597,606 741,444

July 1,449,280 1,249,470 1,564,939 1,579,376

August 1,428,123 1,794,586 1,849,585 1,590,067

September 1,178,795 1,022,538 683,038 724,279

October 368,475 465,971 483,142 651,824

November 257,638 389,276 261,309 309,872

December 321,208 386,377 234,736 371,721

LG3 15-3 Sara’s Ice Cream Shop is closed for six months out of the year, but has had the monthly

sales amounts listed as follows for the last four years. Assuming that there is both

seasonality and a trend, estimate monthly sales for each month of the coming year.

Year: 2010 2011 2012 2013

May $436,880 $926,046 $534,007 $851,622

June 743,947 1,084,321 597,606 741,444

July 1,449,280 1,249,470 1,564,939 1,579,376

August 1,428,123 1,794,586 1,849,585 1,590,067

September 1,178,795 1,022,538 683,038 724,279

October 368,475 465,971 483,142 651,824

LG3 15-4 Suppose that the 2013 actual and 2014 projected financial statements for Comfy Corners

Catbeds are initially shown as follows. In these tables, sales are projected to rise by 22

percent in the coming year, and the components of the income statement and balance

sheet that are expected to increase at the same 22 percent rate as sales are indicated by

green type. Assuming that Comfy Corners Catbeds wants to cover the AFN with half

equity, 25 percent long-term debt, and the remainder from notes payable, what amount of

additional funds will be needed if debt carries a 10 percent interest rate?

$4,880,00

Costs $2,600,000

0 A/R $137,000 $167,140

Depreciati

on $1,000,000

$1,220,00

0 Inv $1,013,000

$1,235,86

0

EBIT $400,000 $488,000

Current

Assets $1,750,000

$2,135,00

0

$6,100,00

(40%) $80,800 $101,021

Net

Income $121,200 $151,531 A/P $179,000 $218,380

N/P $980,000

$1,298,04

7

Dividends $60,600 $60,600 Accruals $375,000 $457,500

Current

$1,973,92

Debt $2,534,000

5

Inc in Liab

$121,880.0

0

RE change $90,930.89

AFN

$1,272,189

.11

LG3 15-5 Suppose that the 2013 actual and 2014 projected financial statements for AFS are initially

shown as follows. In these tables, sales are projected to rise by 14 percent in the coming

year, and the components of the income statement and balance sheet that are expected to

increase at the same 14 percent rate as sales are indicated by green type. Assuming that

AFS wants to cover the AFN with half equity and half long-term debt, what amount of

additional funds will be needed if debt carries a 9 percent interest rate?

$855,000.0

Depreciation $1,200,000 $1,368,000 Inv $800,000

$912,000.0

0

EBIT $1,300,000 $1,482,000

Current

Assets $1,690,000

$1,926,600

.00

$5,700,000

N/P $500,000 $500,000

Dividends $344,100 $344,100 Accruals $375,000 $427,500

Retained $344,100 $442,705

Current

Liab $1,225,000 $1,326,500

LTD $1,200,000 $1,396,197

Equity $4,265,000 $4,903,903

TD +E $6,690,000 $7,626,600

integrated mini-case

Effect of Capital Structure on AFN

Suppose that the 2013 actual and 2014 projected financial statements for your firm are initially

shown as follows. In these tables, sales are projected to rise by 18 percent in the coming year,

and the components of the income statement and balance sheet that are expected to increase at

the same 18 percent rate as sales are indicated by green type. Assuming that your firm has to pay

9 percent interest on debt, what would the AFN be if needed capital was to be raised entirely

from equity?

How would your answer change if the entire AFN was to be raised from long-term debt? And

what does this imply about the relationship between the sources of funding and the amount

needed?

Income Statement Balance Sheet

2013 Actual 2014 Forecast 2013 actual 2014 Forecast

Sales $10,000,000 $11,800,000 Assets

Costs except depreciation 5,200,000 6,136,000 Cash $ 540,000 $ 637,200

Depreciation 800,000 944,000 Accounts receivable 800,000 944,000

EBIT $ 4,000,000 $ 4,720,000 Inventories 1,600,000 1,888,000

Interest 181,530 181,530 Total current assets $ 2,940,000 $ 3,469,200

EBT $ 3,818,470 $ 4,538,470 Net plant and equipment 7,500,000 8,850,000

Taxes (40%) 1,527,388 1,815,388 Total assets $10,440,000 $12,319,200

Net income $ 2,291,082 $ 2,723,082

Liabilities and Equity

Common dividends $2,000,000 $2,000,000 Accounts payable $ 557,000 $ 657,260

Addition to retained earnings $ 291,082 $ 723,082 Notes payable 750,000 750,000

Accruals 1,200,000 1,416,000

Total current liabilities $ 2,507,000 $ 2,823,260

Long-term debt 2,017,000 2,017,000

Total debt $ 4,524,000 $ 4,840,260

Common stock $ 5,250,000 $ 5,250,000

Retained earnings 666,000 1,389,082

Total common equity $ 5,916,000 $ 6,639,082

Total liabilities and equity $10,440,000 $11,479,342

If the ANF is funded entirely with equity, the financial statements will be:

Income Statement Balance Sheet

2013 Actual 2014 Forecast 2013 Actual 2014 Forecast

Accruals 1,200,000 1,416,000

Total current liabilities $ 2,507,000 $ 2,823,260

Long-term debt 2,017,000 2,017,000

Total debt $ 4,524,000 $ 4,840,260

Common stock $ 5,250,000 $ 6,089,858

Retained earnings 666,000 1,389,082

Total common equity $ 5,916,000 $ 7,478,940

Total liabilities and equity $10,440,000 $12,319,200

Common stock = $5,250,000 + $839,858 = $6,089,858

If the AFN is funded entirely with debt:

Income Statement Balance Sheet

2013 Actual 2014 Forecast 2013 Actual 2014 Forecast

Sales $10,000,000 $11,800,000 Assets

Costs except depreciation 5,200,000 6,136,000 Cash $ 540,000 $ 637,200

Depreciation 800,000 944,000 Accounts receivable 800,000 944,000