LG5 13-19 IRR Use the IRR decision rule to evaluate this project; should it be accepted or rejected?

The IRR for this project will be the solution to:

LG5 13-20 MIRR Use the MIRR decision rule to evaluate this project; should it be accepted or

rejected? Cash flows will be moved asfollows:

Year 0 1 2 3 4 5 6

Cash

Flow

–

$5,0

00

$1,200 $2,400 $1,600 $1,600 $1,400 $1,200

LG2 13-21 NPV Use the NPV decision rule to evaluate this project; should it be accepted or

rejected?

( ) ( ) ( ) ( ) ( ) ( )

1 2 3 4 5 6

$1, 200 $2, 400 $1, 600 $1, 600 $1, 400 $1, 200

$5,000 1.08 1.08 1.08 1.08 1.08 1.08

$2,323.92

NPV =– + + + + + +

=

LG7 13-22 PI Use the PI decision rule to evaluate this project; should it be accepted or rejected?

( ) ( ) ( ) ( ) ( ) ( )

1 1 1 1 1 1

$1, 200 $1, 400 $1,600 $1, 600 $1, 400 $1, 200

$5,000

1.08 1.08 1.08 1.08 1.08 1.08

$2,323.92

$2,323.92 $5,000 1.46

$5, 000

NPV

PI

=– + + + + + +

=

+

= =

Since PI > 1, the project should be accepted.

Use this information to answer the next six questions. If you should not use a

particular decision technique, indicate why.

Suppose your firm is considering investing in a project with the cash flows shown as

follows, that the required rate of return on projects of this risk class is 11 percent, and that

the maximum allowable payback and discounted payback statistics for your company are

3 and 3.5 years, respectively.

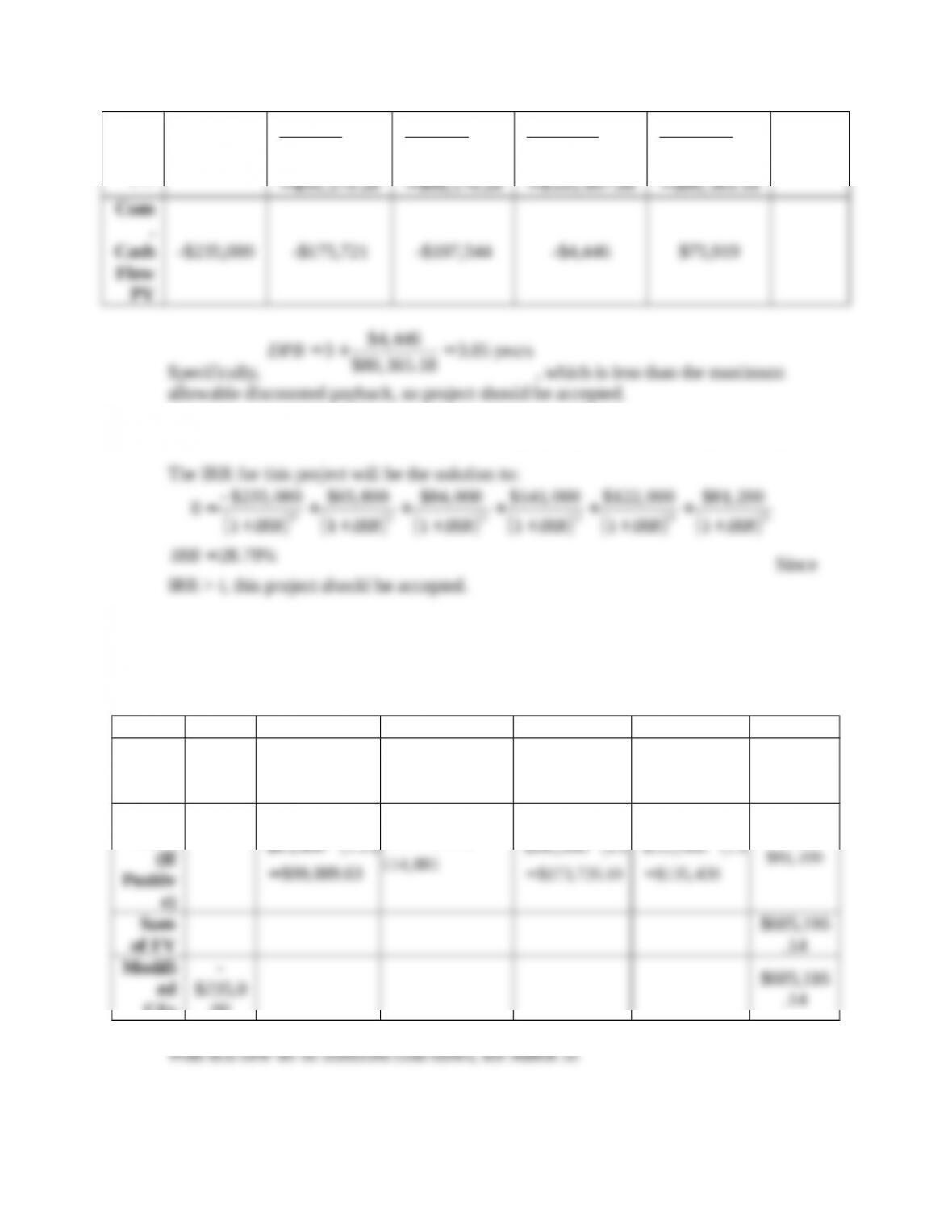

Time 0 1 2 3 4 5

Cash

Flow

–

$235,000

$65,80

0

$84,00

0

$141,00

0

$122,00

0

$81,20

0

LG3 13-23 Payback Use the payback decision rule to evaluate this project; should it be accepted or

rejected?

Cumulative cash flow will switch from negative a positive between years 2 and 3:

LG3 13-24 Discounted Payback Use the discounted payback decision rule to evaluate this project;

should it be accepted or rejected?

Cumulative PV of cash flow will switch from negative and positive between years 3 and

4:

Flow

Cash

Flow

-$235,000

( )

1

$65,800

1.11

$59, 279.28=

( )

2

$84, 000

1.11

$68,176.28=

( )

3

$141,000

1.11

$103, 097.98=

( )

4

$122, 000

1.11

$80, 365.18=

Cum

.

Cash

Flow

PV

-$235,000 -$175,721 -$107,544 -$4,446 $75,919

Specifically,

$4, 446

3 3.05 years

$80,365.18

DPB = + =

, which is less than the maximum

allowable discounted payback, so project should be accepted.

LG5 13-25 IRR Use the IRR decision rule to evaluate this project; should it be accepted or rejected?

LG5 13-26 MIRR Use the MIRR decision rule to evaluate this project; should it be accepted or

rejected?

Cash flows will be moved as follows:

Year 0 1 2 3 4 5

Cash

Flow

–

$235,0

00

$65,800 $84,000 $141,000 $122,000 $81,200

Future

Value

( )

4

$65,800 1.11

´

( )

3

$84, 000 1.11

´

( )

2

$141, 000 1.11

´

( )

1

$122,000 1.11

´

( ) ( )

0 5

$235, 000 $605,116.14

01 1

20.82%

IRR IRR

IRR

–

= +

+ +

=

LG2 13-27 NPV Use the NPV decision rule to evaluate this project; should it be accepted or

rejected?

( ) ( ) ( ) ( ) ( )

1 2 3 4 5

$65,800 $84, 000 $141, 000 $122, 000 $81, 200

$235,000 1.11 1.11 1.11 1.11 1.11

$124,106.98

NPV =- + + + + +

=

Since NPV > 0, the project should be accepted.

LG7 13-28 PI Use the PI decision rule to evaluate this project; should it be accepted or rejected?

( ) ( ) ( ) ( ) ( )

1 2 3 4 5

$6,580 $84, 000 $141,000 $122,000 $81, 200

$235,000

1.11 1.11 1.11 1.11 1.11

$124,106.98

$124,106.98 $235,000 1.53

$235, 000

NPV

PI

=– + + + + +

=

+

= =

Since PI > 1, the project should be accepted.

advanced problems

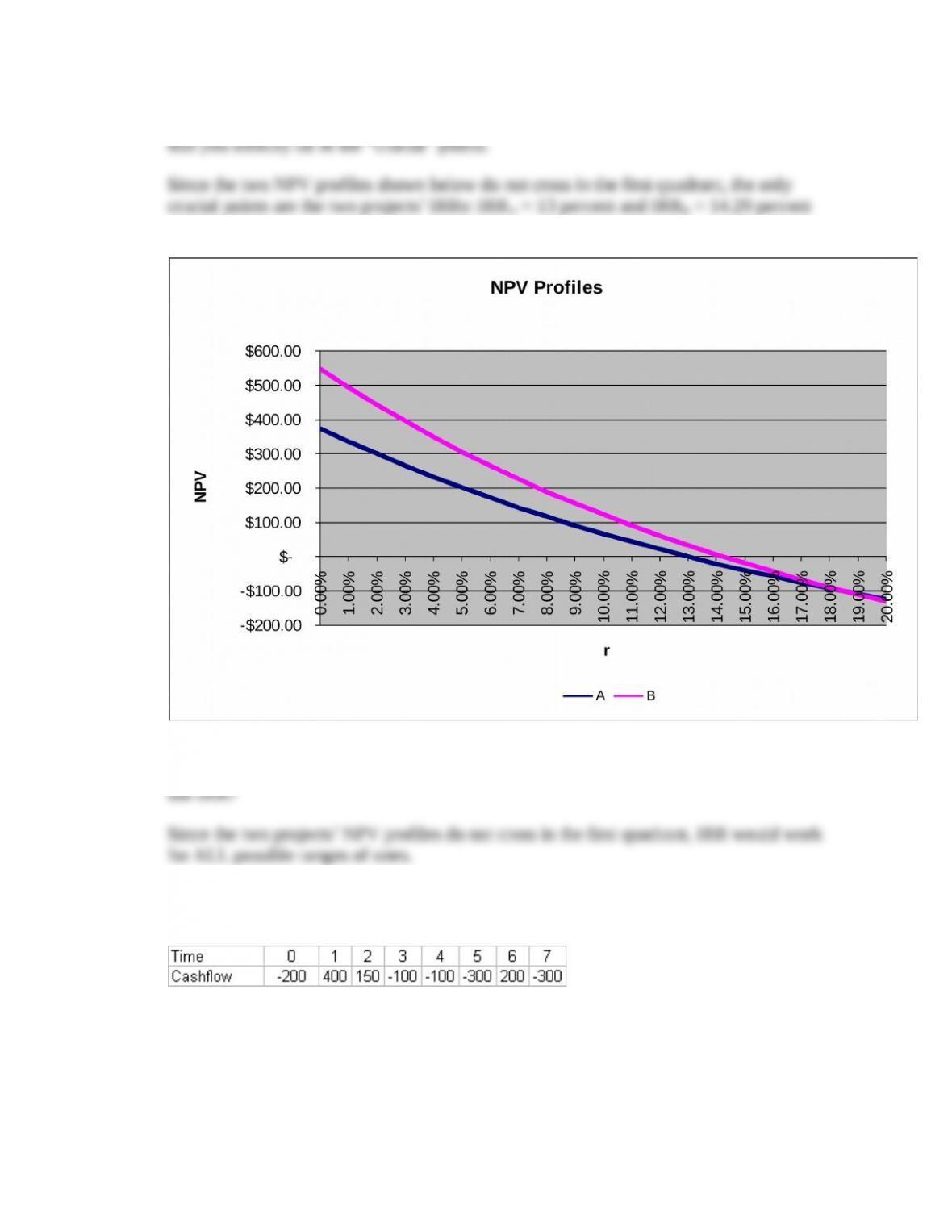

Use the project cash flows for the two mutually exclusive projects shown below to

answer the following two questions.

LG6 13-29 NPV Profiles Graph the NPV profiles for both projects on a common chart, making sure

LG6 13-30 IRR Applicability For what range of possible interest rates would you want to use IRR

to choose between these two projects? For what range of rates would you NOT want to

LG6 13-31 Multiple IRRs Construct an NPV profile and determine EXACTLY how many

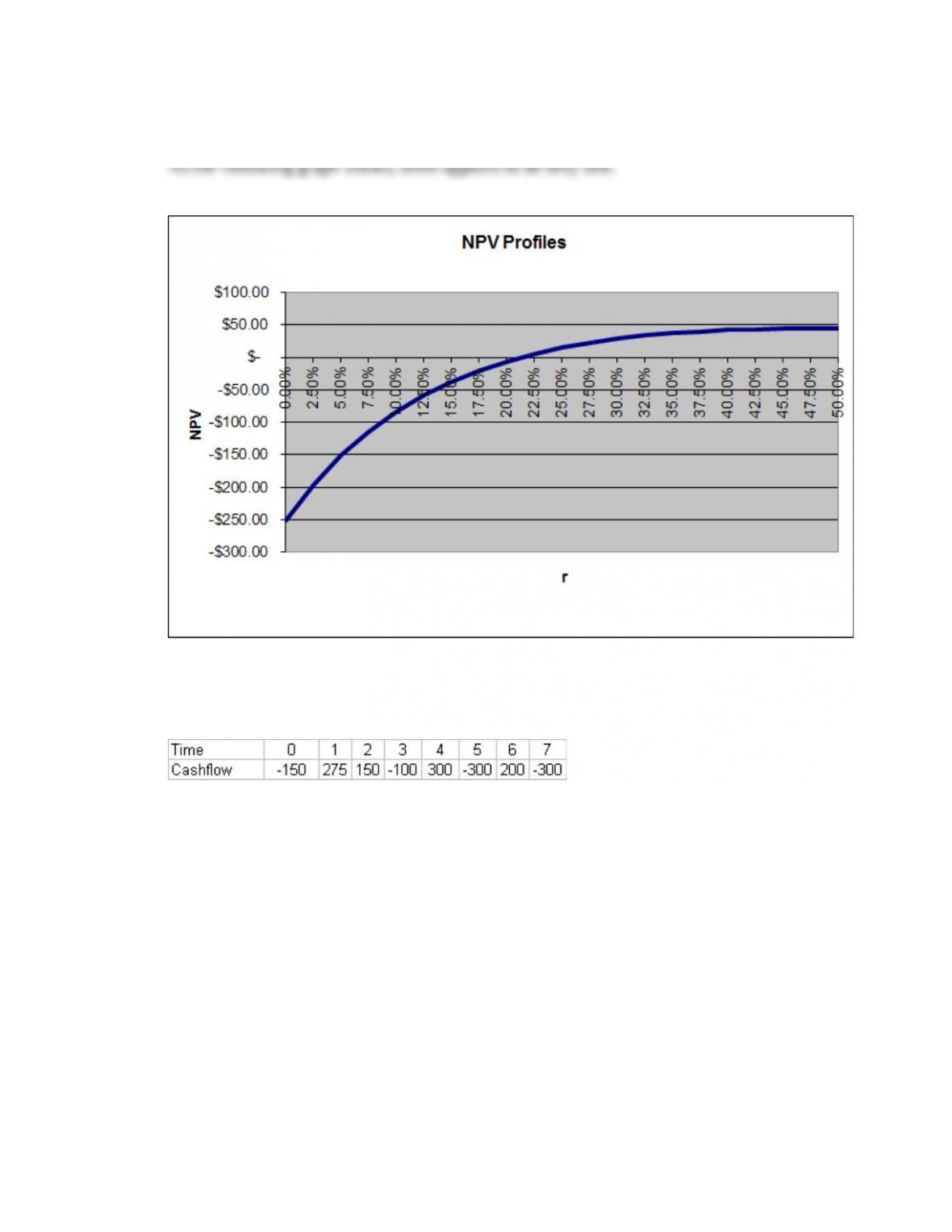

nonnegative IRRs you can find for the following set of cash flows:

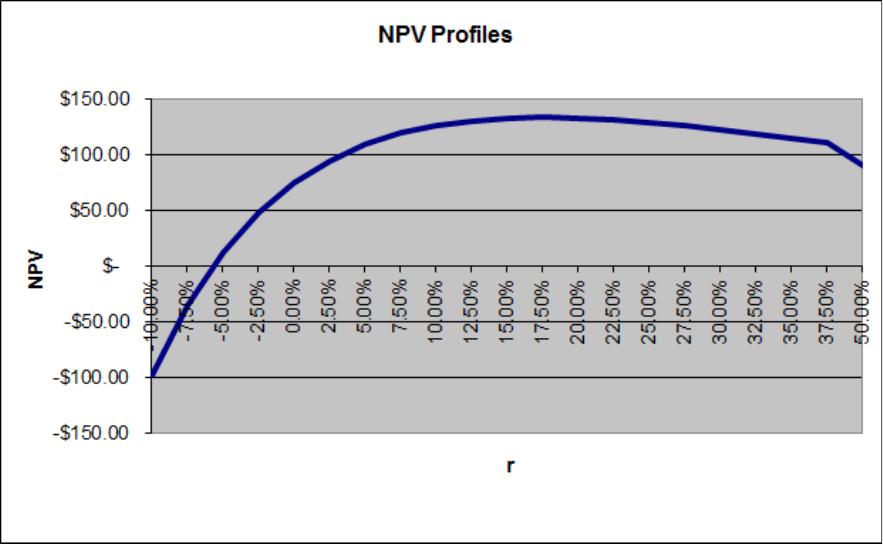

LG6 13-32 Multiple IRRs Construct an NPV profile and determine EXACTLY how many

nonnegative IRRs you can find for the following set of cash flows:

As shown, there appears to be only one.

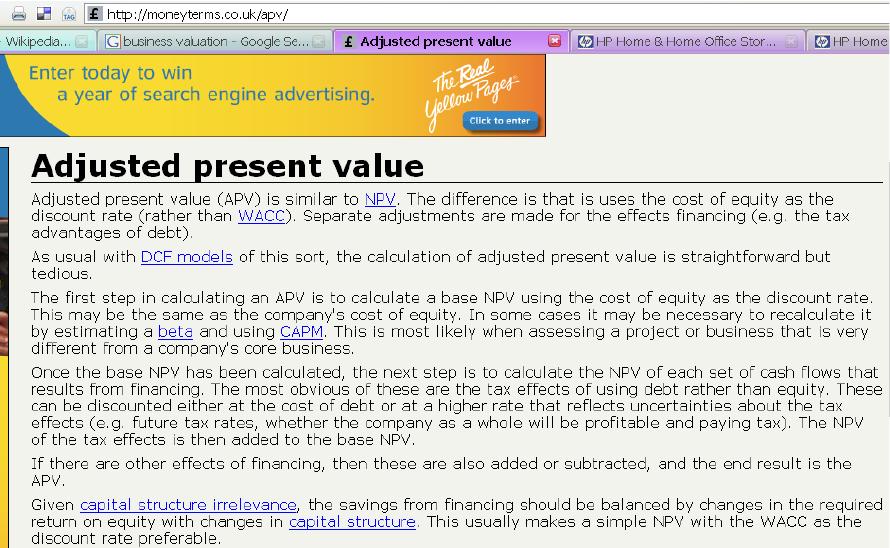

research it! Business Valuation

The capital budgeting decision techniques that we’ve discussed all have strengths and

weaknesses, but they do comprise the most popular rules for valuing projects. Valuing entire

businesses, on the other hand, requires that some adjustments be made to various pieces of these

methodologies. For example, one alternative to NPV used quite frequently for valuing firms is

called Adjusted Present Value (APV).

To explore these alternative decision rules, do a Web search for APV and answer the following

questions:

1. What is APV, and how does it differ from NPV?

2. What other business valuation models seem to be popular?

integrated mini-case

Suppose your firm is considering investing in a project with the cash flows shown as follows,

that the required rate of return on projects of this risk class is 11 percent, and that the maximum

allowable payback and discounted payback statistics for your company are 3 and 3.5 years,

respectively.

Time 0 1 2 3 4 5

Cash

Flow

-$175,000 -$65,800 $94,000 $41,000 $122,000 $81,200

Using every one of the capital budgeting decision methods discussed in this chapter, evaluate this

project, indicating whether each decision rule would call for acceptance or rejection of the

project.

Solution: The decision statistics and the appropriate accept/reject decisions are shown as follows: