LG3 10-25 Risk Premiums You own $10,000 of Denny’s Corp stock that has a beta of 2.9. You also

own $15,000 of Qwest Communications (beta = 1.5) and $5,000 of Southwest Airlines (beta =

0.7). Assume that the market return will be 11.5 percent and the risk-free rate is 4.5 percent.

What is the market risk premium? What is the risk premium of each stock? What is the risk

premium of the portfolio?

Market risk premium = 11.5% − 4.5% = 7%

LG3 10-26 Risk Premiums You own $15,000 of Opsware, Inc. stock that has a beta of 3.8. You also

own $10,000 of Lowe’s Companies (beta = 1.6) and $10,000 of New York Times (beta = 0.8).

Assume that the market return will be 12 percent and the risk-free rate is 6 percent. What is the

market risk premium? What is the risk premium of each stock? What is the risk premium of the

portfolio?

Market risk premium = 12% − 6% = 6%

Opsware’s risk premium = 3.8 × (12% − 6%) = 22.8%

LG3 10-27 Portfolio Beta and Required Return You hold the positions in the following table.

What is the beta of your portfolio? If you expect the market to earn 12 percent and the risk-free

rate is 3.5 percent, what is the required return of the portfolio?

Price Shares Beta

Now compute the portfolio beta: (0.2310 × 3.8) + (0.2557 × 1.2) + (0.2438 × 0.4) + (0.2695 ×

0.5) = 1.42. So, the portfolio’s required return = 3.5% + 1.42 × (12% − 3.5%) = 15.57%

LG3 10-28 Portfolio Beta and Required Return You hold the positions in the following table. What

is the beta of your portfolio? If you expect the market to earn 12 percent and the risk-free rate is

3.5 percent, what is the required return of the portfolio?

Price Shares Beta

Advanced Micro

Devices

$14.70 300 4.2

0.5) = 1.79

So, the portfolio’s required return = 3.5% + 1.79 × (12% − 3.5%) = 18.72%

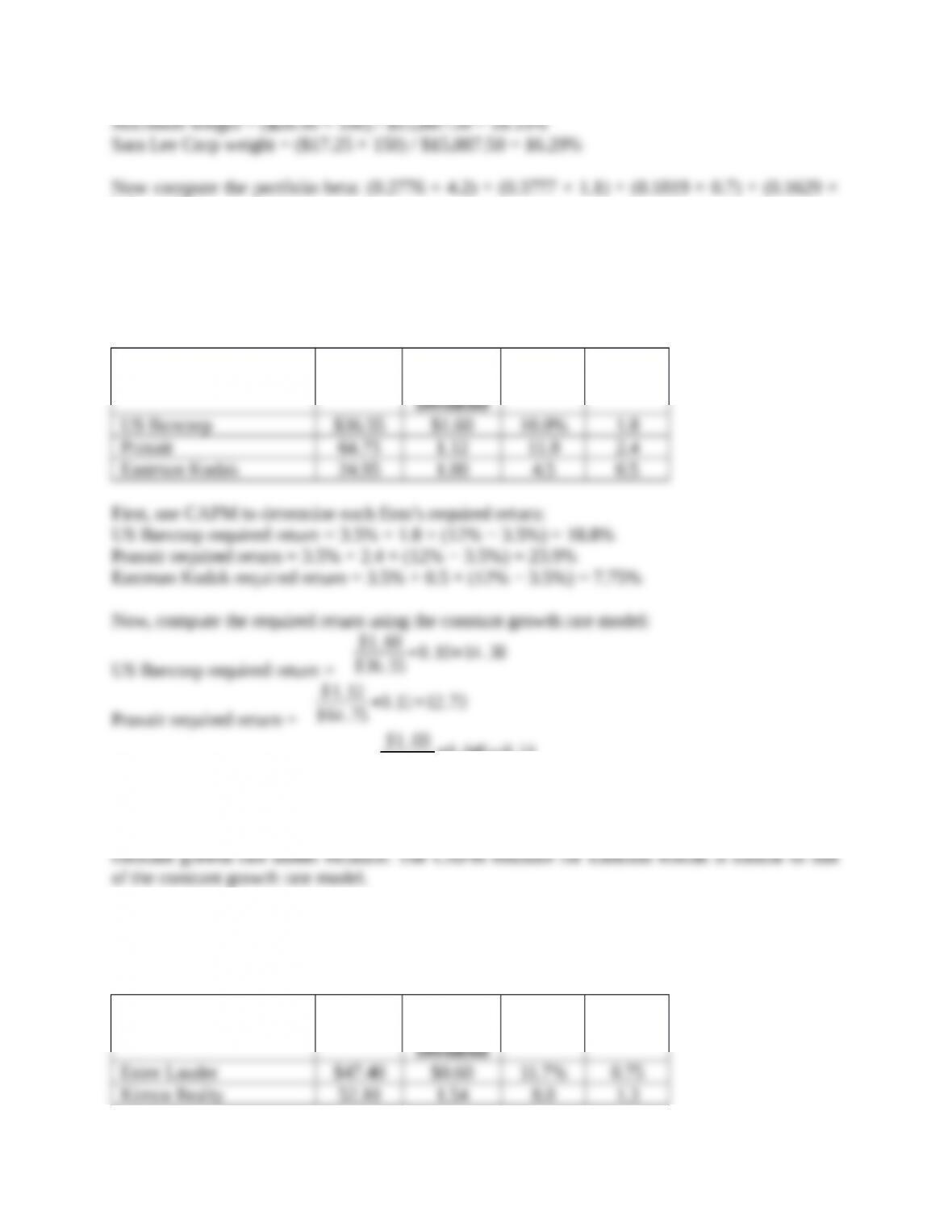

LG3&7 10-29 Required Return Using the information in the table, compute the required return for each

company using both CAPM and the constant growth model. Compare and discuss the results.

Assume that the market portfolio will earn 12 percent and the risk-free rate is 3.5 percent.

Price Upcomin

g

Growth Beta

Apr 2012 -8.23% -6.27% -7.19% Jan 2011 -3.57% 3.20% 3.04% Oct 2009 6.53% 5.74% 4.86%

Mar 2012 -0.73% -0.75% -1.46% Dec 2010 -0.65% 2.26% 1.78% Sep 2009 7.81% -1.98% -3.64%

Feb 2012 1.62% 3.13% 4.20% Nov 2010 10.49% 6.53% 6.19% Aug 2009 4.34% 3.57% 5.64%

Jan 2012 8.22% 4.06% 5.44% Oct 2010 -4.70% -0.23% -0.37% Jul 2009 5.41% 3.36% 1.54%

c. Estimate Microsoft’s beta using the following quarterly data returns. Compare the estimate to

the ones from parts (a) and (b).

Date MSFT S&P500

Q1 2013 8.00% 10.03%

Q4 2012 -9.53% -1.01%

Q3 2012 -2.04% 5.76%

Q2 2012 -4.57% -3.29%

Q1 2012 25.08% 12.00%

Q4 2011 5.08% 11.15%

Q3 2011 -3.64%

–

14.33%

Q2 2011 3.04% -0.39%

Q1 2011 -8.47% 5.42%

Q4 2010 14.65% 10.20%

Q3 2010 7.02% 10.72%

Q2 2010

–

21.09%

–

11.86%

Q1 2010 -3.46% 4.87%

Q4 2009 19.01% 5.49%

Q3 2009 8.82% 14.98%

A. Beta estimates using different market proxies and 45 months. The estimate is from the Excel

Microsoft’s beta is 15 percent higher when using the S&P 500 versus the NASDAQ as the

market proxies.

B. Beta estimate using 30 months.

C. Beta estimate using quarterly returns.

research it!

Find a Beta

company from several different websites. Are the values you obtain similar? If they are not, why

might they be different?

(moneycentral.msn.com, finance.yahoo.com, http://www.zacks.com)

SOLUTION: For General Electric (GE), I found:

integrated mini-case: AT&T’s Beta

When you go on the Web to find a firm’s beta, you do not know how recently it was computed,

what index was used as a proxy for the market portfolio, or which time series of returns the

calculations used. Earlier in this chapter, it was shown that when we went on the Web to find a

beta for AT&T, we found the following: MSN Money (0.53), Yahoo! Finance (0.38), and Zacks

(0.54).

An alternative is to compute beta yourself. A common estimation procedure is to use 60 months

of return data and to use the S&P 500 Index as the market portfolio. You can obtain price data

for a company and for the S&P 500 Index for free from websites like Yahoo! Finance. Using

monthly prices, you can compute the monthly returns, as (Pn − Pn-1) / Pn-1. Following are 60

monthly returns for AT&T and the S&P 500 Index. You can use these returns to compute AT&T’s

beta. A spreadsheet, like Excel, can run a regression (go to Tool menu, select Data Analysis, and

then Regression). Select AT&T returns as the y variable and S&P 500 Index return as the x

Apr 13 3.62% -1.01% Aug 11 -2.67% -5.68% Dec 09 4.02% 1.78%

Mar 13 2.17% 3.60% Jul 11 -5.56% -2.15% Nov 09 4.97% 5.74%

Feb 13 3.22% 1.11% Jun 11 -0.49% -1.83% Oct 09 -3.53% -1.98%

Jan 13 4.54% 5.04% May 11 1.41% -1.35% Sep 09 3.71% 3.57%

Dec 12 -1.25% 0.71% Apr 11 3.13% 2.85% Aug 09 -0.70% 3.36%

Nov 12 -1.32% 0.28% Mar 11 7.86% -0.10% Jul 09 7.41% 7.41%

Oct 12 -7.18% -1.98% Feb 11 3.12% 3.20% Jun 09 0.20% 0.02%

Sep 12 2.88% 2.42% Jan 11 -4.97% 2.26% May 09 -3.25% 5.31%

Aug 12 -3.38% 1.98% Dec 10 5.70% 6.53% Apr 09 3.26% 9.39%

Jul 12 7.68% 1.26% Nov 10 -2.54% -0.23% Mar 09 6.06% 8.54%

Jun 12 4.34% 3.96% Oct 10 1.16% 3.69% Feb 09 -3.49% -10.99%

May 12 3.85% -6.27% Sep 10 5.81% 8.76% Jan 09 -12.32% -8.57%

Apr 12 6.87% -0.75% Aug 10 4.20% -4.74% Dec 08 -0.22% 0.78%

Mar 12 2.06% 3.13% Jul 10 9.12% 6.88% Nov 08 6.70% –7.48%

Feb 12 4.04% 4.06% Jun 10 -0.48% -5.39% Oct 08 -2.61% -16.94%

Jan 12 -1.34% 4.36% May 10 -6.76% -8.20% Sep 08 -12.73% –9.08%

Dec 11 4.35% 0.85% Apr 10 2.53% 1.48% Aug 08 3.84% 1.22%

Nov 11 -1.13% -0.51% Mar 10 4.11% 5.88% Jul 08 -7.43% -0.99%

Oct 11 4.37% 10.77% Feb 10 -2.15% 2.85% Jun 08 -15.55% -8.60%

Sep 11 0.15% -7.18% Jan 10 -8.16% -3.70% May 08 3.06% 1.07%

a. Compute AT&T’s beta using the returns listed.

b. Compare your estimate with the ones found on the Web as listed.

c. How different are the required returns using these betas? Compute required return using

each beta (assume that the risk-free rate is 5 percent and the market return will be 13

percent).