Chapter 10 – Estimating Risk and Return

CHAPTER 10 – ESTIMATING RISK AND RETURN

questions

LG1 1. Consider an asset that provides the same return no matter what economic state occurs.

What would be the standard deviation (or risk) of this asset? Explain.

LG1 2. Why is expected return considered “forward-looking”? What are the challenges for

practitioners to utilize expected return?

LG2 3. In 2000, the S&P 500 Index earned -9.1 percent while the T-bill yield was 5.9 percent.

Does this mean the market risk premium was negative? Explain.

LG2 4. How might the magnitude of the market risk premium impact people’s desire to buy

stocks?

LG3 5. Describe how adding a risk-free security to modern portfolio theory allows investors to do

better than the efficient frontier.

10-1

a

3

Chapter 10 – Estimating Risk and Return

can find a portfolio with the same level of risk as an efficient portfolio but with a higher

expected return.

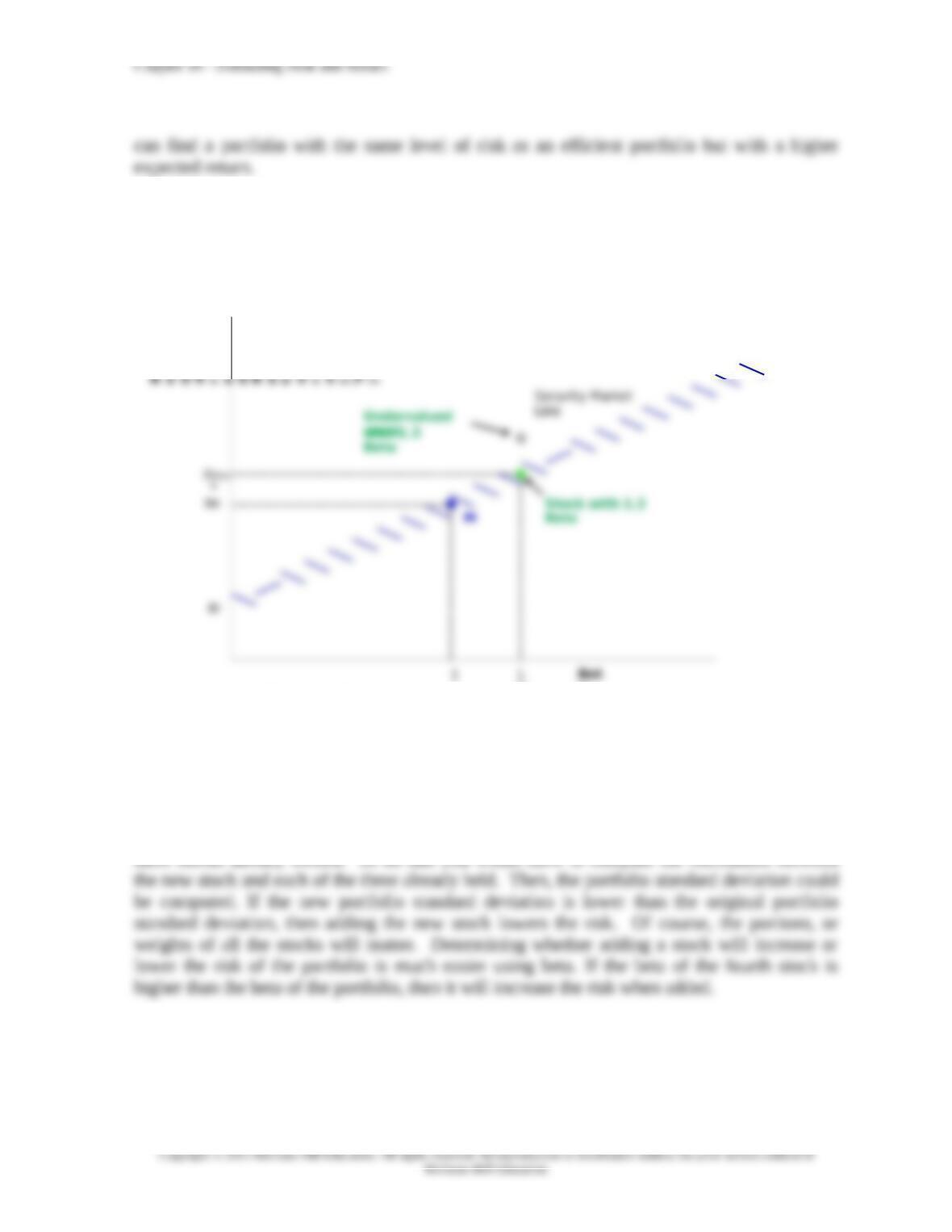

LG3 6. Show on a graph like Figure 10-2 where a stock with a beta of 1.3 would be located on the

security market line. Then show where that stock would be located if it is undervalued.

Figure shown:

LG3 7. Consider that you have three stocks in your portfolio and wish to add a fourth. You want to

know if the fourth stock will make the portfolio riskier or less risky. Compare and contrast

how this would be assessed using standard deviation versus market risk (beta) as the measure

of risk.

Using standard deviation, you would need to determine how the fourth stock interacts with the

LG3 8. Describe how different allocations between the risk-free security and the market portfolio

can achieve any level of market risk desired. Give examples of a portfolio from a person who

is very risk averse and a portfolio for someone who is not so averse to taking risk.

10-2

Chapter 10 – Estimating Risk and Return

100 percent into the market portfolio, an investor can achieve any level of market risk desired.

LG4 9. Cisco Systems has a beta of 1.25. Does this mean that you should expect Cisco to earn a

return 25 percent higher than the S&P 500 Index return? Explain.

LG4 10. Note from Table 10-2 that some technology-oriented firms (Intel) in the Dow Jones

Industrial Average have high market risk while others (AT&T and Verizon) have low market

LG4 11. Find a beta estimate from three different sources for General Electric (GE). Compare

these three values. Why might they be different?

LG4 12. If you were to compute beta yourself, what choices would you make regarding the market

portfolio, the holding period for the returns (daily, weekly, etc.), and the number of returns?

Justify your choices.

LG5 13. Explain how the concept of a positive risk-return relationship breaks down if you can

systematically find stocks that are overvalued and undervalued.

10-3

LG5 14. Determine what level of market efficiency each event is consistent with:

a. Immediately after an earnings announcement the stock price jumps and then stays

at the new level.

b. The CEO buys 50,000 shares of his company and the stock price does not change.

c. The stock price immediately jumps when a stock split is announced, but then

retraces half of the gain over the next day.

d. An investor analyzes company quarterly and annual balance sheets and income

statements looking for undervalued stocks. The investor earns about the same

return as the S&P 500 Index.

LG5 15. Why do most investment scams conducted over the Internet and e-mail involve penny

stocks instead of S&P 500 Index stocks?

LG5 16. Describe a stock market bubble. Can a bubble occur in a single stock?

Bubbles are initially started with an increase in price that is typically justified by the

LG6 17. If stock prices are not strong-form efficient, then what might be the price reaction to a

firm announcing a stock buyback? Explain.

10-4

LG7 18. Compare and contrast the assumptions that need to be made to compute a required return

using CAPM and the constant growth rate model.

When using the CAPM to compute required return, you need to make assumptions about what

LG7 19. How should you handle a case where required return computations from CAPM and the

constant growth rate model are very different?

LG1 10-1 Expected Return Compute the expected return given these three economic states, their

likelihoods, and the potential returns:

LG1 10-2 Expected Return Compute the expected return given these three economic

states, their likelihoods, and the potential returns:

10-5

LG2 10-3 Required Return If the risk-free rate is 3 percent and the risk premium is 5 percent,

LG2 10-4 Required Return If the risk-free rate is 4 percent and the risk premium is 6 percent,

LG2 10-5 Risk Premium The average annual return on the S&P 500 Index from 1986 to 1995 was

15.8 percent. The average annual T-bill yield during the same period was 5.6 percent. What

LG2 10-6 Risk Premium The average annual return on the S&P 500 Index from 1996 to 2005 was

10.8 percent. The average annual T-bill yield during the same period was 3.6 percent. What

LG3 10-7 CAPM Required Return Hastings Entertainment has a beta of 0.65. If the market

return is expected to be 11 percent and the risk-free rate is 4 percent, what is Hastings’

required return?

LG3 10-8 CAPM Required Return Nanometrics, Inc. has a beta of 3.15. If the market return is

expected to be 10 percent and the risk-free rate is 3.5 percent, what is Nanometrics’ required

return?

LG3 10-9 Company Risk Premium Netflix, Inc. has a beta of 3.61. If the market return is

LG3 10-10 Company Risk Premium Paycheck, Inc. has a beta of 0.94. If the market return is

10-6

LG3 10-11 Portfolio Beta You have a portfolio with a beta of 1.35. What will be the new portfolio

beta if you keep 85 percent of your money in the old portfolio and 15 percent in a stock with a

beta of 0.78?

LG3 10-12 Portfolio Beta You have a portfolio with a beta of 1.1. What will be the new portfolio

beta if you keep 85 percent of your money in the old portfolio and 15 percent in a stock with a

beta of 0.5?

LG5 10-13 Stock Market Bubble The Nasdaq stock market bubble peaked at 4,816 in 2000. Two

LG5 10-14 Stock Market Bubble The Japanese stock market bubble peaked at 38,916 in 1989.

LG7 10-15 Required Return Paccar’s current stock price is $48.20 and it is likely to pay a $0.80

dividend next year. Since analysts estimate Paccar will have an 8.8 percent growth rate, what

is its required return?

Use equation 10.6:

i=D1

P0

+g=$0. 80

$48 .20 +0 . 088=10 . 46

LG7 10-16 Required Return Universal Forest’s current stock price is $57.50 and it is likely to pay

a $0.26 dividend next year. Since analysts estimate Universal Forest will have a 9.5 percent

growth rate, what is its required return?

i=D1

P0

+g=$0 . 26

$57 . 50 +0 .095=9 . 95

LG1 10-17 Expected Return Risk For the same economic state probability distribution in

Problem 10-1, determine the standard deviation of the expected return.

10-7

Chapter 10 – Estimating Risk and Return

Economic

Probability Retur

Use equation 10-2 and expected return from Problem 10-1 of 8.5 percent:

Standard Deviation=

√

0 . 3×

(

40%−8 .5

)

2+0 . 4×

(

10%−8 . 5

)

2+0 .3×(−25 −8 . 5 )2

=

√

297 . 7+0 . 9+336 .7=25 . 21

LG1 10-18 Expected Return Risk For the same economic state probability distribution in

Problem 10-2, determine the standard deviation of the expected return.

LG3 10-21 Portfolio Beta You own $10,000 of Olympic Steel stock that has a beta of 2.2. You

also own $7,000 of Rent-a-Center (beta = 1.5) and $8,000 of Lincoln Educational (beta = 0.5).

What is the beta of your portfolio?

LG3 10-22 Portfolio Beta You own $7,000 of Human Genome stock that has a beta of 3.5. You

also own $8,000 of Frozen Food Express (beta = 1.6) and $10,000 of Molecular Devices (beta

= 0.4). What is the beta of your portfolio?

LG1 10-23 Expected Return and Risk Compute the expected return and standard deviation given

these four economic states, their likelihoods, and the potential returns:

Economic

Probability Retur