1.1.1.1.1Chapter Nine

Foreign Exchange Markets

1.1.1.2 I. Chapter Outline

1. Foreign Exchange Markets and Risk: Chapter Overview

2. Background and History of Foreign Exchange Markets

3. Foreign Exchange Rates and Transactions

a. Foreign Exchange Rates

b. Foreign Exchange Transactions

c. Return and Risk of Foreign Exchange Transactions

d. Role of Financial Institutions in Foreign Exchange Transactions

4. Interaction of Interest Rates, Inflation, and Exchange Rates

a. Purchasing Power Parity

b. Interest Rate Parity

Appendix 9A: Balance of Payments Accounts (available on Connect or from your McGraw-Hill

representative)

Instructor’s Manual Appendix: Factors Affecting Exchange Rates (Not in text)

II. Learning Goals

1. Understand what foreign exchange markets and foreign exchange rates are.

2. Understand the history of and current trends in foreign exchange markets.

3. Identify the world’s largest foreign exchange markets.

4. Distinguish between a spot foreign exchange transaction and forward foreign exchange

transaction.

5. Calculate return and risk on foreign exchange transactions.

6. Describe the role of financial institutions in foreign exchange transactions.

7. Identify the relations among interest rates, inflation, and exchange rates.

1.1.1.3 III. Chapter in Perspective

This is the fifth chapter that covers securities markets. In this chapter, a very brief history of

foreign exchange systems (Bretton Woods, e.g.) is provided. The primary focus of the chapter is

to introduce readers to foreign exchange transactions and market terminology. Transaction

exposure and forward hedging are introduced with the emphasis on FI participation in foreign

exchange markets. The concept of translation exposure is introduced, although translation

details are not presented and FASB 52 is not discussed. Relative purchasing power parity and

interest rate parity are introduced and the approximate equations are presented. The two major

balance of payments accounts are explained and recent data are presented. The discussion omits

changes in official reserves and the statistical discrepancy. The appendix (not covered in the

text) outlines some of the major determinants of foreign exchange rate in a conceptual

framework.

1.1.1.4 IV. Key Concepts and Definitions to Communicate to Students

Foreign exchange markets Net long (short) in a currency

Foreign exchange rates Open position

Dollarization Safe haven

Foreign exchange risk Purchasing power parity

Currency appreciation Interest rate parity theorem (IRPT)

Currency depreciation Balance of payment accounts

Spot & forward foreign exchange transactions Net exposure

Currency options Law of one price

International Fisher Effect

1.1.1.5

1.1.1.6 V. Teaching Notes

1. Foreign Exchange Markets and Risk: Chapter Overview

In 2012 the U.S. imported $3.3 trillion in goods and services and exported about $3.0 trillion.

Capital markets, foreign exchange markets and derivatives markets all play a part in facilitating

such large amounts of international transactions.

There are two relevant prices involved in international trade. The first is the price of the good or

service purchased and the second is the price of the currency.1 In many transactions the first

price is fixed but the latter will normally fluctuate with changes in the foreign exchange rate.

Fluctuating exchange rates, like fluctuating prices, cause risk in international business

transactions. The foreign exchange rate is in a sense the ‘entry fee’ to purchase a country’s

financial and real goods and services. It is the link between economies, and the foreign

exchange rate reflects the value of the goods and services produced by a given country relative to

the value of goods and services produced in another country. Depreciating foreign currencies

hurt the home currency value of foreign assets, but also reduce the home currency value of

foreign liabilities. The converse is true for appreciating currencies. The recent drop in the value

of the dollar hurt firms that import goods and services into the U.S., but it helped firms that

exported goods and services overseas and improved the translated value of foreign currency

earnings for U.S. U.S. multinational firms.

1 It does not matter whether the good or service purchased is denominated in dollars or not.

Someone faces currency conversion costs and risk. For instance, from the U.S. perspective if the

good is non-dollar denominated the U.S. buyer faces the currency cost, if it is dollar denominated

the foreign seller bears the cost and risk.

Teaching Tip: In fixed or tightly managed floating systems currencies are said to be either

revalued (upward) or devalued (downward). In free floating systems, the terms are appreciation

and depreciation respectively.

2. Background and History of Foreign Exchange Markets

Throughout much of the 1800s countries used a gold standard to back the value of their

currencies. Currency issuers agreed to redeem their notes for a certain amount of gold. Gold

thus became a fungible asset convertible to various currencies. The British pound was at the

center of the global system and the pound was the ‘reserve currency’ for the world. This reserve

currency status adds value to a currency beyond immediate supply demand conditions. The gold

standard with the pound at its center could not be maintained in the late 1930s and early 1940s as

Great Britain depleted its gold stocks to pay for war munitions. After World War II the prior gold

standard was replaced with the gold exchange standard, termed the Bretton Woods System

(1944-1971) after the town in New Hampshire where the agreement was crafted. Under Bretton

Woods, currencies were pegged to the U.S. dollar and the U.S. dollar was backed by gold. This

system worked well until the U.S. began to have higher inflation than other developed

economies, particularly Germany and Japan were willing to maintain. A run on gold ensued in

the early 1970s which led to Nixon closing the ‘gold window’ and led to the Smithsonian

Agreement I (1971). This agreement tried to prop up the system but failed, and the second

Smithsonian Agreement (1973) allowed freely floating exchange rates. The fixed exchange

rate system failed because U.S. inflation was greater than the rest of the developed world. The

system was based on the willingness of foreign countries to hold dollars and backed by the

willingness of the U.S. to exchange dollars for gold. At that time, the dollar’s value was fixed at

$35 per ounce of gold. As more and more market participants doubted that the value of the

dollar could be maintained, fewer participants were willing to hold dollars, preferring gold or

other currencies instead. The Treasury and foreign government authorities were unable to

maintain the value of the dollar as depletion of gold reserves ensued.

Bretton Woods arose because of the need to foster cooperation among countries and promote

trade instead of the competitive devaluations that had occurred during the Depression years. The

instructor should emphasize that all fixed exchange rate systems require cooperation among

member countries; otherwise, fixed exchange rates cannot be maintained because private sector

currency trading can dwarf the size of governments’ currency reserves. However, throughout

much of the Bretton Woods period, private currency market trading was quite low. As the

currency markets grew, governments found it increasingly difficult to maintain a fixed exchange

rate that was inconsistent with relative economic conditions among member countries.

Prior to 1972 all forward foreign exchange trading was over–the–counter trading involving

banks. The International Monetary Market (IMM) began trading foreign currency futures

contracts in 1972 although the OTC forward market still dominates trading activity. Advantages

of trading currency futures on an exchange include:

Anonymity of parties

No credit risk concerns because the exchange’s clearinghouse guarantees performance of

both parties

Standardized known terms of contracts

Liquidity: Most futures contracts do not result in making or taking delivery because

participants who are long (short) in a futures contract can easily go short (long) in the

same contract, netting their position to zero. There is a much lower likelihood of finding

a counterparty to offset a given OTC forward contract.

Disadvantages of using currency futures rather than forwards would include the difficulty in

obtaining the exact contract specifications desired, in particular, currency futures are actively

traded on only the major currencies and long–term contracts may not be available or may be

relatively illiquid. In addition, futures are cash settled daily, gains and losses on forwards are not

recognized until contract maturity, which makes forwards more suitable for hedging in many

cases. Currency options are traded on the Philadelphia Stock Exchange and provide yet another

way to speculate on foreign currency movements or hedge currency transactions.

On January 1, 1999, the euro was introduced to represent the currencies of the eleven

participating European Monetary Union (EMU) countries. The euro was initially used for

payments between nations, for currency speculation and for financial transactions. However, the

euro did not begin to replace domestic currencies in circulation until January 1, 2002 (among 12

European countries at the time, since expanded). The creation of the euro was the next step in

stages for monetary union outlined by the Maastricht Treaty of 1993. The euro declined in

value after its launch, probably partly due to the uncertainty whether the European Central Bank

could successfully manage a common currency for somewhat diverse economies. The

immediate impact of the euro was to reduce foreign currency transactions by consolidating

trading for the original currencies. Nevertheless, the euro was an immediate success in financial

transactions and growth in euro denominated debt instruments has been quite large. The euro

has become the world’s second most important currency (number one is the dollar, number three

is the yen).

Some countries have dollarized their economies, meaning they now use the U.S. dollar as their

currency. A strong stable currency attracts foreign capital, which some emerging markets need to

generate growth. If a country dollarizes they give up the ability to engage in independent

domestic monetary policy in a countercyclical fashion. A dollarized economy is also at risk of a

dollar appreciation, which may make the country’s good and services overpriced or a declining

dollar may generate inflation in the dollarized economy. Dollarization removes the temptation to

monetize public debt and thus may require fiscal discipline. Dollarization may make sense for

countries that can’t provide fiscal discipline any other way.

In 2013 the foreign exchange markets were the largest markets in the world with $5.34 trillion of

daily trading activity in essentially a 24-hour market.

Teaching Tip:

Selected foreign currency reserves 1/2013:

Country Foreign Currency Reserves

(all in $ in billions)

China $3,317

Saudi Arabia 643

Russia 538

Taiwan 398

S. Korea 327

(all U.S. $ value but only an estimated 60% are in U.S. $)

Sources: Economist, ECB and IMF

These reserves are built up when foreign central banks intervene in the currency markets to

acquire dollars or require local firms to exchange foreign currency earnings for the local

currency. Foreign central banks may engage in these operations to suppress or peg the value of

their local currency in order to help stimulate their export sector. Without these interventions the

local currency should rise as local firms that export to the U.S. acquire too many dollars and

begin to sell their dollar holdings in the currency markets. The dropping dollar may them make

the imports too expensive in the U.S or erode foreign profit margins. China in particular has

accumulated huge dollar holdings. China maintains capital controls that regulate private capital

flows in and out of the country. The currency reserves are typically invested in U.S. Treasuries,

keeping U.S. interest rates lower than they would be otherwise and probably allowing the U.S.

government and U.S. private borrowers to accumulate more debt than they could otherwise.

However, accumulation of foreign currency reserves can be inflationary as the process involves

creating extra local currency. Eventually China will have to allow the yuan to float to limit

inflationary pressures in China.

China is now allowing limited fluctuation in the value of the Chinese currency, the yuan, against

the dollar. The yuan is officially valued against a basket of currencies and allowed to fluctuate in

a narrow range although in reality the yuan is managed relative to the euro and the dollar. The

yuan was mostly pegged from 2001-2005 and from 2008-2010. In September 2010 the U.S.

House of Representatives passed a bill allowing the U.S. to institute tariffs or other sanctions

against countries determined to be ‘currency manipulators’ to bolster their export sectors. The

U.S. has considered naming China as a currency manipulator. Note that the U.S.’ QE program

could be considered to be a currency manipulation designed in part to stimulate growth in the

U.S. export sector. In June 2010 China promised to allow the yuan to float more freely.

In 2009 Hong Kong was allowed to begin trading the yuan offshore and offshore deposits grew

from 100 billion yuan in 2010 to 600 billion in 2013. In January 2011 Chinese based companies

use the yuan off the mainland and America was allowed to begin yuan trading. As of October

2011 foreign companies can settle direct investment accounts on the mainland in yuan. China

widened the trading band against the dollar and in February 2013 the CME Group initiated

trading in yuan or renminbi futures.

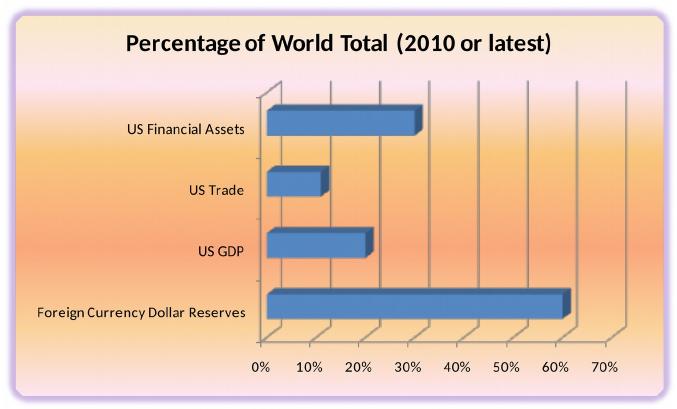

Will the U.S. dollar remain the world’s reserve currency?

No one know for sure but notice that in the chart below that uses data from the Economist the

disproportionate size of the foreign currency dollar reserves in relation to the proportion of U.S.

financial assets, trade and GDP. The point the Economist Magazine is making is that dollar

currency reserves are too high for the relative size of the U.S. economy, and this may not be

sustainable if foreign investors lose faith in the value of the U.S. economy and its currency. If

other alternatives emerge, such as a more stable European economy and a maturing China, it is

possible and maybe even likely that the reserve currency status of the U.S. dollar will be slowly

eroded over time. This may make it more difficult for the U.S. government to finance its large

deficits and debt levels but the timing of such changes is highly uncertain.

U.S. percentage of the world total in the given category:

Data Source: www.economist.com, China’s Currency, The Rise of the Redback, Jan 20, 2011

3. Foreign Exchange Rates and Transactions

a. Foreign Exchange Rates

Currency quotes are often very confusing to students. Rates can be quoted two ways:

1. Dollar value of one unit of foreign currency: £1 = $1.60

2. Foreign currency value of the dollar: $1 = £0.625

These two quotes are inverses.

Teaching Tip: When discussing percentage changes in the value of a currency one must pay

careful attention to the form of the quote. For example if in the above quote we say the pound

appreciated 10%, how is the new value of the pound calculated?

£1 = $1.60 initially so the new value of the pound is $1.60 1.1 = $1.76. The value of the dollar

did not drop 10% however. The inverse of $1.76 is 0.5682 so the $1 = £0.5682, a 9.09% drop.

Teaching Tip: If the dollar appreciates, the foreign currency value of the dollar rises but the

dollar value of the foreign currency falls.

b. Foreign Exchange Transactions

Spot or immediate transactions are normally settled within two to three business days, but

currencies may be bought or sold forward for one or more months (transaction dates beyond 1

year are less common). As a country’s exchange rate increases, its exports may become more

expensive and imports may be relatively cheaper. A strong currency can contribute to a current

account deficit. Conversely, a weaker currency may improve the current account deficit. The

dollar has gone through wide swings in value in recent years. The dollar fell 33% against the

euro from 2002 to 2004, regained much of the loss in 2005 but fell again in 2007 and 2008

reaching record lows.

The dollar regained much of its losses in 2005. The resounding ‘no’ vote on the European

constitution by the French and Dutch constituencies dampened prospects for continuing reforms

needed to stimulate European growth (the so called “Lisbon Reforms”). Concerns about the

expansion of the EU coupled with the no vote raised doubts about the long term viability of the

euro and of the move toward political and economic convergence that some economists feel are

needed to promote European growth.

The dollar’s drop continued in 2007 and in early 2008, hitting record lows against the euro and

declining against the yen. In February 2008 the dollar stood at its weakest in 12 years on a trade

weighted basis. The dollar weakness was due to labor market prospects, the housing problems

and poorer U.S. growth prospects.2

From September 2008 to March 2009 the dollar increased in value against the major currencies

as investor sought safety in U.S. Treasury investments. From March to November 2009 the

dollar began to fall as investors again sought out higher yields as fears of economic collapse

subsided. Subsequent to this time period the dollar strengthened against the euro because of the

European sovereign debt problems in Portugal, Ireland, Iceland, Greece and Spain. About 42%

of all foreign exchange trading involves the dollar and the second largest currency traded is the

euro involved in about 20% of trading. The euro strengthened against the dollar in 2010 and

through August 2011, but in September of 2011 fears of more European problems caused the

dollar to strengthen despite a downgrade of the U.S. credit rating by S&P, particularly after the

U.S. passed a debt ceiling increase.

What lies in store for the dollar in the future? No one knows for sure but the long term trend in

the value of the dollar on a trade weighted basis is down and is likely to continue downward for

the following reasons.

The size of the U.S. current account deficit which was reaching record levels in absolute

terms and as a percent of GDP before the crisis remains large. This deficit may not be

ultimately sustainable because it requires foreigners to be willing to hold large quantities

of dollars (dollar assets).

Europe has had higher interest rates than the U.S, although the European Central Bank

recently dropped its benchmark interest rate and began charging negative deposit rates on

bank reserves. Nevertheless, higher interest rates in Europe puts pressure on the dollar to

fall against the euro through carry trades.3

Asian central banks continue to acquire dollars to keep their currencies from rising.

Europe did not follow suit and the result has been a stronger euro, ceteris paribus.

Continuing problems with Europe’s economies and growing disillusionment with the

2 “Dollar’s Dive Deepens as Oil Soars: Power of Greenback Faces Severe Test, But No Rivals

Loom, by Craig Karmin and Joanna Slater, The Wall Street Journal Online, February 29, 2008,

Page A1.

3 In carry trades the investor borrows in the low interest rate currency, sells the currency and

invests in the high interest rate currency. This puts pressure on the dollar to fall if our rates are

lower than in Europe.

euro may limit the extent of euro appreciation against the dollar. Weaker Chinese growth

may limit dollar appreciation against the yuan.

The administration has not seemed to mind having the dollar drop. A falling dollar can

help the export sector of the U.S. economy. It seems likely that the U.S. will pursue an

easy monetary policy for some time to come and this will continue to put pressure on the

dollar to fall and stress the world’s willingness to absorb dollars.

As a result of the subprime crisis, high government debt levels and the credit crunch the

U.S. continues on a slower growth path than many other countries potential growth. This

may imply poorer investment opportunities and returns than can be found elsewhere but

the safe haven status of the dollar continues to outweigh the desire for higher returns that

should be available elsewhere.

Teaching Tip: The classical economic treatment of a dropping dollar improving the current

account deficit is true but the effects of devaluation are more complex than may first be realized.

As explained in Determinants of the Balance of Trade and Payments, 1997: Published in

International Money and Finance, by Michael Melvin, the elasticity of demand for U.S. goods

and services and the elasticity of supply of U.S. imports are crucial factors in how quickly a

devaluation leads to an improvement in the current account. For instance, if a depreciation leads

to import price increases to maintain foreign profit margins, more money may be spent on

imports, not less, at least in the short run. This is the basis for the so called “J” curve where a

current account deficit first gets worse with devaluation (the downward part of the J) and

eventually improves (the upward movement along the J).

Teaching Tip: As indicated above the Fed (U.S. Treasury) has had to allow the dollar to drop in

order to stimulate the economy with lower interest rates due to the ongoing anemic U.S. job

growth. Not all economists agreed on this policy, worrying that the dollar’s slide could become

precipitous and difficult to stop although this fear is probably overblown. The drop in value of

the dollar also exacerbates recessionary and inflationary pressures on the U.S. economy. Many

commodities are dollar priced, including oil and gold. If the dollar drops in value, eventually

oil prices may increase, because foreign oil sellers want to maintain their home currency profit

margins and because demand increases for buyers whose currency has appreciated against the

dollar, reducing the effective cost of the higher dollar price. The increased supply from fracking

has dampened these price pressures however.

All this adds to longer term inflationary risk which, if it occurs, will likely result in less

consumer spending on other items. Consumer spending has been a major driver of U.S. growth.

Subsidies for alternative biofuels have also created inflation in food prices. People forget how

regressive inflation actually is, hurting poorer people far more than those in higher income

brackets. The Fed has a difficult task managing the multiple risks now facing the U.S. economy.

Not all currencies declined against the dollar. Some countries that also had current account

deficits saw their currencies decline against the dollar, including South Korea, South Africa,

Indonesia, India and Turkey. These countries have had difficulties financing their deficits,

leading to drops in currency values. See the appendix for further discussion or see the cites

below:4

c. Return and Risk of Foreign Exchange Transactions

For a U.S. firm, transaction exposure (exposure to a change in the value of a foreign currency for

a given transaction) arises whenever foreign currency assets or liabilities are acquired, or when

commitments to buy or sell in a foreign currency are made. Commitments to purchase goods or

services in a foreign currency are at risk from rising foreign exchange rates (falling dollar) and

may be hedged by buying the foreign currency forward. Commitments to sell in a foreign

currency are at risk from falling foreign currency values and may be hedged by selling the

currency forward.

Teaching Tip: Any event that will lead to the receipt of foreign currency may be hedged by

selling the currency forward. Any event that requires payment of foreign currency in the future

may be hedged by buying the currency forward. Hedgers may have difficulty hedging beyond

one year with forwards; this is one reason for the creation of longer term swaps.

4 “Weak Dollar Feels New Stress,” by Joanna Slater, The Wall Street Journal Online, March 11,

2008, Page A1, and “The Yen and Euro May Grab the Headlines, But Not All Currencies Are

Beating the Buck,” by Evan Ramstad, The Wall Street Journal Online, March 18, 2008, Page C2.