1. Primary and Secondary Stock Markets

a. Primary Markets

In the primary market, corporations obtain equity funds by creating and selling new issues of

stock. Investment bankers usually assist in this process. Sales may be on a fully underwritten

basis or may be via best efforts. Recall from Chapter 6 that with a fully underwritten offering

the investment banker buys the securities from the issuer at the bid price and resells them to the

public at the offer price. The gross proceeds on a fully underwritten offering are the offer price

times the number of shares bought. The net proceeds are the bid price times the number of

shares sold.1 The underwriter’s spread is the difference between the gross and net proceeds.

Investment bankers often form syndicates or coalitions of other investment banks to help market

an issue. Syndicates help spread the risk and increase the sales force available to market the

issue. The bank that is the primary negotiator in the deal is called the originating house. The

investment banks’ names are listed in tombstone ads, and they are normally arranged according

to the prestige of the bank and their importance in the deal. The originating house will normally

be the first bank listed and the position on the tombstone ad is jealousy guarded.2

An initial public offering (IPO) occurs the first time a corporation sells shares to the public.

Seasoned offerings are new issues of additional stock sold subsequent to the IPO.

Teaching Tip: Many of Wall Street’s elite investment banking firms have been fined for ethical

violations, including ‘spinning,’ ‘laddering’ and issuing overly optimistic research reports. Most

‘hot’ IPOs are oversubscribed, so the investment banker chooses which customers will receive

the IPO shares. Since IPOs are often issued at a discount, IPO buyers may receive an

abnormally high short term return. Spinning is allocating shares of a hot IPO to favored

customers in exchange for receiving investment banking business from the buyer’s firm later on.

Allocating disproportionate amounts of these shares to favored personal accounts in exchange for

receiving underwriting and consulting business in the future is unethical and a breach of the

public trust. Laddering (not in the text) is allocating IPO shares to firms who agree to buy more

in the aftermarket in an attempt to increase the price over the short run, increasing gains to

original purchasers. Investment banking firms operate underwriting divisions and employ

research analysts. Analysts have been issuing overly optimistic research reports to support the

underwriting business. At certain firms such as Merrill Lynch, internal memos indicated

analysts’ real opinions about the poor quality of certain stock investments, while the published

research reports were highly favorable. The research analysts have a potential conflict of interest

with the underwriting business. If analysts publish reports indicating a stock is a poor buy, the

firm’s underwriting and distribution arm is likely to have difficulty marketing a new issue. In

some firms, research analysts even earned bonuses based on the amount of underwriting business

the firm engaged in, an obvious violation of independence. Sarbanes-Oxley has increased the

independence of analysts from the underwriting business, but stopped short of requiring

divestiture of research analyst firms.

1The term net proceeds is misleading. It ignores other direct and indirect costs beyond the

bid-ask spread.

2Investment bankers have at times withdrawn from deals because of where their placement

would be on the tombstone ad.

Teaching Tip: A new seasoned stock issue will normally result in a small drop in price of the

existing stock (about 2-3%) upon the announcement of the new stock offering. In a perfect

world where firms always choose positive NPV projects this price drop should not occur. A

possible explanation of the price drop is that firms tend to issue equity only when the firm’s

management believes the shares are overvalued. As a result the markets drop their estimate of

the value of the shares when a new offering is announced. Other explanations are possible and

no one really knows why the price drop is of a fairly standard amount and does not appear to be

related to issue size. Smaller, but still statistically significant, price drops in the common stock

have been found to occur for straight debt offer announcements when the debt announcement

was a surprise to the market.3

1.1.1.1 Rights Offering

In some cases corporations that already have publicly traded stock may choose or be required to

use a rights offering. A rights offering allows existing shareholders to purchase a pro-rata

portion of the new issue at a slightly favorable price. This right is termed the preemptive right.

Essentially, the rights are warrants given to existing shareholders which can then be used to buy

the new issue.

Teaching Tip: A large number of rights expire unused. If the investor does not wish to use the

rights, they should sell them; an active market exists for rights. Letting the rights simply expire

is throwing away money. Rights offerings are not that commonly used. In many cases the

existing shareholders do not buy enough of the new issue to meet management’s funding targets.

When used, investment bankers are often hired to do a ‘standby and take-up’ of shares not sold.

When the cost of the standby and take-up arrangement is added, rights offerings may not a

cheaper method than an underwritten offering. Rights offerings also do not disperse ownership

whereas an underwritten offering probably will increase the number of new owners.

Registration

3 See “Common Stock Price Effects of Security Issues Conditioned by Earnings and Dividend

Announcements,” Manuel, Brooks and Schadler, October 1993, Journal of Business 66, No.4,

pp. 571-593.

A public issue of securities has to be approved by the Securities Exchange Commission (SEC).

Investment banks assist issuers with the registration process. The SEC requires the issuer to

disclose its line of business, current and projected financial position, the use of the proceeds,

major features of the issue and details about management. The SEC normally imposes a 20 day

waiting period after filing during which the SEC can request more information. Prospectuses

(abbreviated registration statements) circulated during this time are called ‘red herrings’ for the

red stamp on them indicating that the SEC has yet to approve the issue. The time period between

filing for registration and issuance of the shares is termed the quiet period. During this time,

management and bankers may conduct ‘road shows’ to solicit investor interest and help

determine the final price, but the firm may not engage in written communication to the public.4

In 2004 the SEC proposed removing the quiet period restriction as long as the information is first

filed with the SEC for firms with market capitalization of at least $700 million and $1 billion in

debt. The SEC is allowing Internet broadcasts of ‘road shows.’ For examples see

www.retailroadshow.com. These broadcasts are open to all investors and they allow more

investors to gain information about new issues. Currently, the bankers invite selected customers

to attend the presentations. Both of these changes appear to be good ideas that may broaden

investor participation in new offerings.

Once the SEC approves the issue the official prospectus is issued and securities are offered to the

public, usually within a day. The purpose of the SEC’s involvement is to ensure that the public

has enough information to evaluate the riskiness and the suitability of the investment for their

portfolio.

Teaching Tip: Investment banks are jointly liable with the issuers for any misstatements on the

registration statement. Lawsuits subsequent to an issue that does not perform well abound. To

help limit liability, investment bankers and issuers undergo a due diligence investigation to

ensure that all material facts are correct and are disclosed to the public.

To help speed up the process issuers sometimes pre-register securities using a procedure termed a

shelf registration. After the registration is approved the issuer may then market the issue at any

time within the subsequent two years after filing a short form with the SEC that is normally

approved within a day or two.

Teaching Tip: Under Regulation D, Rule 504, companies who wish to make a small public

offering of equity up to $1 million can file a brief registration statement called a Small Company

Offering Registration (SCOR) filing rather than the normal detailed registration statement. A

typical lawyer or an accountant can complete this form rather than an investment banking legal

expert. SCOR filings may be sold directly to individual investors and can be traded with brokers

who make a market in them. These stocks tend to be inactively traded. See Bruce G. Posner,

“How to Finance Anything,” Inc. (April 1992):50-62.

4 These rules were adopted in 1933. The SEC feared that not all investors would have timely

access to the information. Email and the Internet have reduced the problems with equal access to

information.

b. Secondary Markets

Secondary markets are the markets where existing securities are re-traded among investors. The

issuing corporation receives no proceeds from secondary market sales.

Stock Exchanges

The New York Stock Exchange Euronext (NYSE) is the most active U.S. secondary stock

market based on dollar volume traded.5 The NYSE trades over 2300 stocks with an average

daily trading volume of $50 billion dollars or 1.9 billion shares in 2010. The NYSE merged with

Euronext N.V. in 2007 and acquired the American Stock Exchange (AMEX) in 2008 and was

itself acquired by the Intercontintental Exchange (ICE) in November 2013 in a deal worth about

$11 billion. ICE/NYSE/Euronext is the world’s third largest exchange behind Hong Kong

Exchanes and Clearing and the CME Group. The NYSE went public in 2006 after merging with

Archipelago Holdings (Arca). NYSE Euronext operates four markets in the U.S., NYSE, NYSE

Arca, NYSE AMEX and ArcaEdge. NYSE Arca resulted from the merger with the Arca

electronic exchange and NYSE AMEX is the new name of the old AMEX. ArcaEdge trades over

the counter (OTC) stocks and low volume pink sheet stocks.

NASDAQ is now the third largest U.S. market since BATS and DirectEdge merged. In 1998 the

AMEX attempted to merge with NASDAQ but the two entities soon separated, citing

irreconcilable differences. The future of the remaining regional exchanges is doubtful.

Nevertheless, the regionals remain innovative. The idea for ETFs came from the regionals.

ETFs are index funds that are exchange listed and trade like stocks. The advantage of ETFs over

mutual funds is that ETFs can be traded throughout the day and can be sold short.

Teaching Tip: Deutsche Bourse made a takeover offer for the NYSE/Euronext. NASDAQ, in

combination with the Intercontinental Exchange (ICE), made a counter offer. The U.S.

Department of Justice moved to block the NASDAQ/ICE offer on anti-trust grounds. The DOJ

felt a merger with NASDAQ could limit competition and hurt investors.6 The merger was not

allowed by European antitrust authorities.

The NYSE is a continuous open outcry auction where the high bidder sets the price. The price

fluctuates throughout the day according to buying and selling pressure. Historically stocks

traded in minimum price increments of 1/8 or 1/16, but stock prices increments are now in

decimals with a maximum trade increment of five cents a share. The effect has been to reduce

spreads on stocks, and thereby reduce trading costs, increasing the markets’ operational

efficiency.

A customer will usually place a market order to buy or sell a stock either with their broker or

5The National Association of Securities Dealers Automated Quotations (NASDAQ) has at times

reported a higher volume of shares traded than the NYSE, but NASDAQ numbers apparently

overstate actual trading volume due to the method used in calculating the numbers so care must

be used in quoting their trading activity numbers.

6 See “Antitrust Objection Drives Nasdaq to Drop NYSE Bid, The Wall Street Journal Online,

by Jacob Bunge and William Launder, May 16, 2011.

online. In either case the exchange quickly receives and processes the order. A market order is

transacted at the prevailing price when the order reaches the floor, usually within a matter of

minutes of placing the order. Alternatively, a customer may place a limit order. A limit order is

an order to transact at a specified price or better. If the limit order is not immediately filled it

resides with the specialist on the NYSE (see below) or a NASDAQ dealer until the market

moves to the limit price or the order expires. Market microstructure deals with the details of

how orders are processed and securities are traded. Some markets trade through dealers, some

use brokers, or combinations of the two. The trend is towards electronic order processing.

Program trading is the simultaneous buying and selling 15 or more different stocks valued at $1

million or more using computer programs to initiate the trades. Program trading takes the form

of stock index futures arbitrage and portfolio insurance and is often criticized for generating

excess volatility in stock prices and transferring volatility from derivatives markets to the stock

market. As a result, the NYSE employs circuit breakers to halt program trading when the Dow

Jones Industrial Average (DJIA) moves sufficiently, see the table below:

Drop in DJIA* Impact

1,450 point drop before 2:00 pm Trading halted for one hour

1,450 point drop 2:00-2:30 pm Trading halted for 30 minutes

1,450 point drop after 2:30 pm No halt

2,900 point drop before 1:00 pm Trading halted for two hours

2,900 point drop 1:00-2:00 pm Trading halted for one hour

2,900 point drop after 2:30 pm Trading halted for the rest of the day

4,350 point drop anytime Trading halted for the rest of the day

Source: Text

* the point drops are approximately 10%, 20% and 30% respectively.

On May 6, 2010, the financial markets experienced what has come to be termed, the ‘flash

crash.’ Markets fell about 5% in a very brief time, only to just as quickly recover most of the

loss. Some well known stocks such as Accenture, BostonBeer and Exelon even briefly traded at

1 cent per share. Although many rumors as to the cause of the crash abounded, an investigation

eventually stated that trades of $4.1 billion S&P500 futures contracts by a Kansas City based

mutual fund, Asset Strategy Fund, triggered the crash. The fund used a computer algorithm to

sell on increased trading volume. Other program traders used algorithms to trade when market

declined, further increasing sell pressure. Regulators have now suggested limiting use of trade

orders that do not contain a specific price.

In so called flash trading, traders are allowed to see incoming buy or sell orders milliseconds

earlier than general market traders. Flash traders then use computerized statistical analysis to

generate high frequency trading strategies that are executed by computer as well. Proponents

claim that allowing flash trading creates more liquidity and the possibility of price improvement

for regular customers who may be able to trade inside posted bid-ask quotes. The problem with

flash trading is twofold. First, it creates a disadvantage for regular traders and investors who are

not allowed to view incoming orders. Second, the high volume of trading generated by multiple

computers can lead to events like the so called flash crash. In 2009 the SEC proposed banning

flash trading, but as of 2014 it had not been banned. In June 2014 the SEC is considering

requiring high frequency traders (HFTs) to register as broker dealers to improve regulation. The

SEC also wants greater exposure of dark pool trading (see below).7 The SEC has missed about

70% of implementation deadlines imposed by the 2,319 page Dodd-Frank bill. Among other

items, the bill requires the SEC to review and strengthen the fiduciary duty of broker dealers,

ensure the fairness of investment recommendations by brokers who sell proprietary products,

require disclosure of relationships between investment advisors and broker dealers.

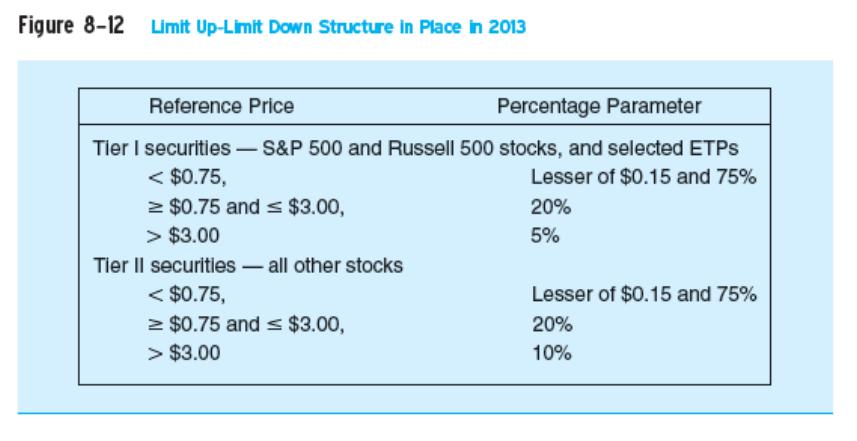

As a result of the flash crash the SEC imposed circuit breaker rules for individual stocks.

Trading is halted if the price breaks the price band calculated as price band = (Reference Price) ±

[(Reference price) × (Percentage parameter)]. The parameter is a function of the reference price,

which is the median over the last 5 minutes of trading, as delineated in Text Figure 8-12

reproduced below:

7 SEC Chairman Targets Dark Pools, High-Speed Trading; Chairman White Suggests

High-Speed Firms Register With Regulators, by Scott Patterson, The Wall Street Journal Online,

6/6/14.

ETPs are exchange traded products. If a stock moves out of the bounds, termed ‘limit up or limit

down (LULD), trading is initially halted for 15 seconds. If the limit orders are filled or canceled

within the trading halt time, trading resumes, otherwise a further 5 minute trading halt is

imposed. During this pause no trades are executed but quotes are displayed. The boundaries for

trading halts are wider at the open and close.

Brokers and exchanges are allowing some traders to engage in high frequency trades

anonymously using the broker’s access code. This is termed ‘naked access.’ Reportedly, 36% of

all U.S. stock trading is occurring this way. Finally, dark pools are trades that occur on

alternative trading platforms (such as electronic communication networks) that do not report the

details of the trade on order books. Detailed information such as the name of the buyer or seller

and the volume traded may be kept private. This would seem to be in violation of earlier

National Market System regulations that required disclosure of trades across markets. About

15% of daily trading in 2013 may have been in dark pools.

The SEC has prohibited the use of ‘stub quotes.’ Stub quotes are quotes that are far away from

the market that dealers sometimes use because they are required to post both buy and sell quotes.

Some of these quotes were enacted when the markets crashed so quickly. Nevertheless fears of

another flash crash remain and the NYSE and NASDAQ await final rulings from the SEC. See

for instance, “Fears Linger of New ‘Flash Crash,’” by Michael Mackenzie and Tels Demos,

Financial Times, May 5, 2011.

The NYSE annually auctions off trading licenses through a Dutch auction process. A trading

license is needed to trade on the floor of the exchange. Trading licenses are good for one year

and only members of the NYSE are eligible.

The NYSE employs specialists, or designated market makers (DMMs) to help ensure

continuous trading with orderly price transitions. At the DMM trading post brokers fill

customer’s orders with each other or against the specialist’s limit order book. DMMs are

exchange employees who serve as both brokers and dealers. A trade on the floor of the NYSE

may or may not involve a specialist. When an order arrives on the floor it is transferred to the

specialist post (all orders are now transmitted electronically). The order may be filled by another

broker at the post, may be filled by the specialist, or may be filled against the specialist’s limit

order book. DMMs are involved in about 10% of all trades. Unlike NASDAQ which may have

as many as 15 to 20 dealers in a given stock, there is only one specialist assigned to a stock on

the NYSE. DMM firms include Dermott Clancy., Speer Leeds and Kellogg, Bear Wagner

Specialists, SIG Specialists, SLK Specialists and Van Der Moolen.8 Firms may cover more than

one stock. Investment bankers are generally not allowed to be specialists because of potential

conflicts of interest. These DMMs covered more than 90% of shares traded on the NYSE.9

Specialists had allegedly engaged in front running customers. In front running, the specialists

place their own orders ahead of the public. The move to decimalization and increasing

competition from other markets has eroded specialists’ profits, increasing the temptation to act

unethically.

In October 2006 the NYSE expanded its electronic trading capabilities for certain stocks. This

reduced order execution time from 9 seconds to under one second and removed certain prior

electronic trading restrictions.

Teaching Tip: A specialist or DMM may have to trade against a market trend. For instance, if the

majority of orders are buy orders, the DMM will usually fill the orders by selling from their own

inventory. Likewise they will buy when everyone else is selling, although in either case they

may petition the exchange to suspend trading in that security. The majority of DMM profits

come from the brokerage function. On a very bad day however, a DMM may have to endure

large dollar losses.

The NASDAQ is not a physical location, but a computerized network of dealers who make a

market in a given security. The number of dealers for one security ranges from over 20 to only

one or two. In 2001 the largest NASDAQ market makers were Knight Securities, Salomon

Smith Barney, Morgan Stanley, Schwab Capital Markets and Merrill Lynch.10

Teaching Tip: Although the computer network allows brokers to check for the best quotes, there

is no guarantee that brokers will obtain or transact at the best quotes (the lowest ask for a buy

order or the highest bid for a sell order). Brokers have directed order flow to certain dealers in

exchange for lower commissions on other orders, free research, or other advantages. The NASD

has tightened rules and enforcement on unethical practices. This is a problem with a

self-regulated industry. There are no self-regulated industries that I know of that have not had

breaches of ethics at some point.

The Small Order Execution System (SOES) was developed on NASDAQ to help ensure that

customer orders are executed at the best price. Details can be found on the NASDAQ website or

8 Source: NYSE Euronext website and text

9 Market Mechanics: A Guide to U.S. Stock Markets, NASDAQ Educational Foundation

10 Ibid, Also note that NASDAQ allows bankers to be dealers.

from the free publication cited in footnote 7. NASDAQ provides an electronic OTC Bulletin

Board to assist in trading of stocks with low volume and interest. Trades are executed by

contacting a broker/dealer who has posted quotes. There is no membership or listing

requirements for these stocks. Stocks with even smaller trading volume are traded by circulating

‘pink sheets’ among NASD dealers containing quotes to buy and sell.

ECNS are computerized trading systems that match buy and sell orders automatically.

According to Robert Greifeld, President and CEO of NASDAQ, ECNs represent a lower cost

model of order execution and potentially faster execution.11 The former ECN, Better Alternative

Trading System, or BATS, is now the second largest exchange in the U.S. .its merger with

another former ECN, DirectEdge. after. Institutional traders are the primary users of ECNs with

institutions posting quotes to buy and sell, often for large blocks of shares. ECNs had been

eroding both NASDAQ’s and the NYSE’s market share. There has been less trading of NYSE

listed stocks on ECNs due to regulatory requirements, although these requirements have been

circumvented or weakened lately. Increasing competition with NYSE stocks and the new rules

on best price execution in multiple markets were clearly part of the reason for the earlier mergers

of NYSE and Archipelago and the NASDAQ and Instinet.

Teaching Tip: Many securities trade on multiple markets. All markets now have quotations on

securities in other markets to either take advantage of or limit arbitrage possibilities. SEC rules

require market makers to post more than the inside quotes on public quotation systems. This

helps ensure that buyers and sellers can transact at the best price because they can see more

quotes from different markets. This particularly assists block traders who place orders for

10,000 shares or more. The end result is more trades executed in multiple markets; many of

which would have occurred on the NYSE floor before the change. The term is to conduct an

‘intermarket sweep,’ transacting at best prices in multiple markets. The rules changes prompted

the NYSE to move further toward electronic trading.

Teaching Tip: When the NYSE proposed to merge with Archipelago, an electronic

communication network or ECN, seat prices rose dramatically, probably because the NYSE had

suffered from increasing competition from ECNs and from its own ethical problems.

Incidentally, this merger probably means the end of the specialist or DMM system in the long

run. Not surprisingly, shortly after the announced merger of the NYSE and Archipelago,

NASDAQ and Instinet announced a merger. These mergers are also probably another blow to

the survival chances of the regional exchanges.

Teaching Tip: Will an auction style market like the NYSE continue to exist in the future?

Internationally, markets are moving to electronic trading platforms. What is the competitive

advantage of the NYSE? Is it having a set location where trades can be monitored? Can’t

technology do this? Is it having a specialist to trade against the market when prices are on a

trend? Can’t market makers in a NASDAQ style system or dealers in an ECN be given the same

charge?

11 From Greifeld’s lecture, Gilkey Executive Lecture Series, University of Montana, Spring

2005.

Stock Quotes

Stock quotes are available from many websites and the form of the quotes may vary. The text

covers a Wall Street Journal Online quote sheet.

The WSJ quotes include the company name and ticker symbol, the daily open, high, low and

closing price in dollars and cents, the net change from the prior close in dollars and as a percent.

The volume of shares traded, the 52 week high and low price (excluding the current day) are also

included. The annualized dividend and dividend yield (found by taking the latest quarterly

dividend x 4), the P/E ratio and year to date percentage change in the stock’s price are also

provided.

Day Trading and Online Trading:

The tech boom and the Internet fueled much speculative fever (that hopefully is now over).

Historically most speculators lose, usually spectacularly; even renowned speculator Keynes

reputedly died penniless. Recent studies show that most day traders lose money. Day trading is

akin to gambling and we probably should not encourage this activity among students by

glamorizing it. The boom in online trading is probably over and a shakeout in this industry can

be expected, but online trading is too cost effective to fade away. Long term prospects for this

industry remain good although the activity moves up and down with the stock market. As

always, in tougher markets investors desire and value the opportunity to obtain advice from

professionals.

c. Stock Market Indexes

A few years ago the Dow Jones Corporation changed some of the components of its popular

Dow Jones Industrial Average (DJIA or Dow), including NASDAQ firms for the first time.

Several old line NYSE firms were replaced with Microsoft, Intel, and Home Depot. The Dow is

a price weighted average of 30 stocks chosen to represent the major industries of the day.

The NYSE composite and the S&P500 are value weighted indexes. The NASDAQ Composite

consists of industrials, banks and insurance firms but it contains more tech firms than the other

indexes.

Major Index12 # Stocks Weighting

DJIA 30 Price Weighted

NYSE Composite All NYSE Value Weighted

NASDAQ All NASDAQ Value Weighted

Standard & Poor’s 500 Value Weighted

Wilshire 5000 3,562 Value Weighted

The Wilshire 5000 is the broadest index. This index seeks to include all stocks that are 1)

headquartered in the U.S., 2) actively traded in the U.S. and 3) has widely available price

information. There are only 3,562 stocks now due to delistings, privatization and acquisitions.

12 There are many subindices available designed to focus on specific part of the market.

Teaching Tip: The late 1990s and early 2000s provided a roller coaster experience for investors.

From 1995 through the market peak in 2000 the Dow tripled in value. Within two years, half

that gain was lost. Over the same time period the NASDAQ Composite rose 571% to its peak in

2000, and as of the end of the third quarter of 2002 was only up 56% over its 1995 level. The

more stable S&P500 gained 233%, but by 2002 had lost two thirds of the gains.13 The financial

crisis only added to the volatility. The Dow peaked at 14,164.53 in October 2007 and by

mid-March 2008 the Dow had fallen 53.8%. The other indexes also fell over 50%. Prices did

recover somewhat, (up 70% from the lows by April 2010) but didn’t reach pre-crisis peaks until

March 2013.

Stock Market Index Calculations

A price weighted (PW) index assumes an equal number of shares are purchased for every stock

in the index. A value weighted (VW) index assumes that the dollar amount invested in each

stock in the index is proportional to the market value of the stock divided by the total market

value of all stocks in the index. Simple examples of price weighted and value weighted index

value calculations are given below:

Stock P0 Q0 P1 Q1

A $12 40 $15 40

B $50 80 $25 160

C $125 50 $140 50

P and Q are price per share and total number of shares outstanding respectively.

The PW index is found as:

PW Index 0 = ($12 + $50 + $125) / 3 = 62.33. Notice that Stock B has a 2 for 1 split, halving the

price and doubling the number of shares outstanding. When a stock in the index splits the

denominator in the index calculation must be adjusted to maintain a proper interpretation of the

PW index. The denominator will no longer be three and the new denominator is calculated as

follows using the time zero prices for A and C and the post split price for B: Denominator =

($12 + $25 + $125) / 62.33 = 2.60. Using a denominator of 2.60 eliminates the effect of the

stock split for B. PW Index 1 = ($15 + $25 + $140) / 2.60 = 69.26.

The VW index in time 1 is found as:

11108100

5012518504012

50140160254015 .

($)($)($

)($)($)($

VWindex

The VW index value in time 0 is 100.

In comparing the two, similar % change movements in higher price stocks in the PW index cause

proportionately larger changes in the index. Stock splits arbitrarily reduce the weights of stocks

that split in the PW index. The VW index avoids these problems.

13 “Investors Brace for Declines As Myriad of Concerns Linger,” Wall Street Journal, 10/1/02.