Chapter 07 – Mortgage Markets 6th Edition

1. The Secondary Mortgage Markets

a. History And Background Of Secondary Mortgage Markets

In 2013 about 60% of all residential mortgages were securitized. Originators often keep

the servicing contract. Servicing fees range from ¼% to ½% of the loan amount.

Securitization also allows FIs to remove the mortgages from the balance sheet which

improves liquidity, reduces interest rate risk and reduces capital and other regulatory

costs. More details and calculations of savings are provided in Chapter 24.

b. Mortgage Sales

Traditionally, mortgage and loan sales were conducted between correspondent banks.

Correspondent banks are banks that have ongoing service, loan and deposit relationships

with each other. Prototypically, a small bank has a correspondent relationship with a

larger bank. The small bank keeps deposits at the larger bank and uses the larger bank to

clear checks, obtain loans and invest extra funds. Small banks often also create loans too

large for them to finance and they may sell all or part of the loan to their correspondent

bank. The large bank may also sell loan participations to the small bank if local loan

demand is weak at the smaller bank’s locale. This practice improves diversification at the

smaller bank. Mortgage (or other loan) sales may be with or without recourse, most are

without recourse and may or may not lead to securitization. If a loan is sold with

recourse the loan seller remains liable to the loan buyer if the borrower defaults. The five

primary buyers of mortgages are banks, insurance firms, pension funds, closed end bank

loan funds and nonfinancial corporations. A major advantage of selling the mortgages is

the reduction in capital required by the selling institution. A bank that finances a

mortgage must hold 2.8¢ in equity capital per dollar of mortgage loans. Selling the loan

reduces the required equity. The seller may keep the servicing contract or may not,

preferring to concentrate on earning origination fees on new mortgages.

Securitization and the crisis:

Securitization has allowed the creation of a national market for mortgages. The process

allows origination to be done locally, while the ultimate financing is on a national or even

an international scale. However, the originators are retaining the risk of a default, a

decline in the quality of originating procedures and documentation resulted.

Underwriting standards declined, there has allegedly been poor processing of loan

documents, failures to monitor the securitization process and to monitor borrowers along

with outright fraudulent activity.

Ethics Teaching Tip:

Many banks have paid very large fines related to selling poor quality mortgages to Fannie

Mae and Freddie Mac. Allegations of misrepresentation of prices of mortgage backed

securities sold during the crisis have also emerged. As of this writing Bank of America

(BofA) was in negotiations with the U.S. Justice Department to pay a $12 billion fine for

7-1

Chapter 07 – Mortgage Markets 6th Edition

mortgage related problems, $5 billion of which would go to consumer relief.1 If the bank

will write down principal on problem mortgages the fines will be reduced. BofA has

already been ordered to pay $6 billion to the FHFA. In all BofA may have paid as much

as $60 billion due to fines and civil suits. J.P. Morgan has payments of $13 billion.

Ethics Teaching Tip:

The experiences of Taylor, Bean & Whitaker Mortgage Corp (TBW) provide a case study

of the apparently corrupt interactions between the mortgage agencies and the industry.

Lee Farkas, former chairman of TBW has been accused of kiting checks, selling loans

that didn’t exist and using the same collateral to back multiple loans. TBW was doing

business with Fannie Mae but Fannie Mae refused to purchase any more mortgages in

2002. In 2001 Fannie Mae accounted for 80% of TBW’s business. Fannie Mae stopped

buying from TBW because they discovered that the firm had sold them six loans they had

previously rejected. This should have been the end of the story, but at this point Freddie

Mac, apparently aware of the problems with TBW, decided to begin purchasing its

mortgages. According to the Wall Street Journal this decision allowed a small $15

million fraud to blossom into a $1.9 billion fraud. Shortly thereafter a former executive

of Freddie Mac, Paul Allen, became the CEO of TBW even though Allen remained in

Virginia, far away from TBW’s corporate offices in Florida.2

c. Mortgage-Backed Securities

Securitization is the process of transforming individual loan contracts into marketable

securities. This is accomplished by depositing a pool of mortgages with a trustee and

then selling some type of marketable security to investors. It is a form of intermediation.

Mortgage backed bonds and CMOs (REMICs) are examples of asset transformations (see

Chapter 1). As of 2013, there were $7.85 trillion of mortgage securities outstanding. The

main types are illustrated below (many variations exist) and more detail in provided in

Chapter 24.

Pass-Through Securities

On a pass-through security, the pool organizer simply passes through all mortgage

payments made by the homeowners, including prepayments, to the holders of the

pass-through securities on a pro-rata basis. Payments are thus monthly, and are variable

based on how many homeowners pay off their mortgages early. The pool organizer or the

government usually provides insurance for the mortgages in the pool. Default risk is not

generally a worry for a government or agency backed pass-through security holder (such

as a GNMA pass-through). These securities carry substantial prepayment risk however.

1 BofA in Talks to Pay At Least $12 Billion to Settle Probes: At Least $5 Billion

Expected to Go to Consumer Relief, By Devlin Barrett, Dan Fitzpatrick and Christina

Rexrode, June 5, 2014,

http://online.wsj.com/articles/bofa-in-talks-to-pay-at-least-12-billion-to-settle-probes-140

2006948?mod=djemalertNEWS.

2 A Mortgage Big Fish Disappoints, Holman Jenkins, Jr. The Wall Street Journal Online,

April 27, 2011.

7-2

Chapter 07 – Mortgage Markets 6th Edition

Teaching Tip: Prepayment risk can be illustrated with a simple example. If an investor

holds a relatively high interest rate pass-through it will be priced above par. The investor

is willing to pay a premium above par because the claim pays a high level of interest

relative to current rates. If the mortgages are prepaid the investor will receive the par

amount but they will have paid a premium over par that will be lost because the investor

will be cashed out at par.

Mortgage Backed Pass Through Securities Outstanding (1st Qtr 2013)

Issuer Trillions $ %

GNMA $1.40 17.8%

FNMA $3.01 38.3%

FHLMC $1.75 22.3%

Privately Issued Pass-Throughs (PIPs) $1.69 21.5%

Total $7.85 100.0%

GNMA

The Government National Mortgage Association (GNMA) is a government agency that

was formed in 1968 to provide mortgage credit to veterans, farmers and lower income

individuals. Rather than provide direct financing for mortgages, GNMA will guarantee

payment on mortgage pools that are created by private pool organizers. Originators

submit a pool of mortgages for GNMA approval. All mortgages in the pool must have

the same interest rate and maturity and have FHA, FmHA or VA insurance so GNMA

insurance is really only timing insurance (ensures that the payments are made in a

timely fashion).3 GNMA does not form mortgage pools but allows pool organizers to sell

securities which use the pool as collateral and carry GNMA’s name. These are called

GNMA pass-throughs. These securities have minimum denominations of $25,000. The

pass-through holders receive the amounts paid in by the homeowners minus a 6 basis

point fee. GNMA and the mortgage servicers share those basis points. Mortgage

companies are the largest issuer of GNMA pass-throughs.

FNMA

Fannie Mae was formed in 1938 as a government agency and charged with creating a

secondary market for FHA and VA insured mortgages. FNMA did so by making and

honoring forward commitments to purchase mortgages from originators. FNMA raises

money by issuing its own securities to the public. FNMA has an emergency line of credit

with the Treasury if needed although FNMA was privatized in 1968. Privatization

occurred so that FNMA could expand into conventional mortgages and because they were

profitable on their own and no longer needed government agency status.

FHLMC

3 The government places caps on the insurable amount of an individual mortgage. These

caps vary according to the cost of housing in a given area and housing costs through time,

the maximum was $417,000 in 2014.

7-3

Chapter 07 – Mortgage Markets 6th Edition

Freddie Mac was created in 1970 as a private company with the purpose of improving the

liquidity of mortgages originated by thrifts. FHLMC buys both FHA, VA and

conventional mortgages, puts the mortgages into pools, and then sells claims (securities)

collateralized by the mortgage pool. Thus FHLMC does not provide the ultimate

financing for the bulk of their mortgages.

Government Sponsorship of FNMA and Freddie Mac and the history of problems at

both

Both FNMA and FHLMC are implicitly backed by the U.S. government, indeed both

have a credit line with the Treasury. The government backing reduces FNMA’s and

FHLMC’s borrowing costs and both companies have been consistently profitable.

Because the government backing lowers these government sponsored enterprises’ (GSEs)

funding costs, either the GSEs can consistently generate monopoly profits and/or more

funds are channeled into mortgage investments that otherwise would have gone

elsewhere, probably to corporate bond or equity investments. A second concern is the

government’s liability that would occur if these GSEs experienced financial difficulties,

as both organizations are quite large. Other problems that have recently arisen include:

(source: Text)

Problems with derivatives positions: The Office of Federal Housing Enterprise

Oversight (OFHEO) indicated that both organizations were at risk from large

positions in derivatives, supposedly designed to hedge their interest rate risk. If these

institutions are hedging appropriately, then the derivatives positions should not add to

bankruptcy risk to the organizations. However, hedging reduces both return and risk

and few hedgers can resist the temptation to use derivatives to try to increase return

rather than to reduce risk. In 2003, Freddie Mac experienced a 52% drop in income

due to derivatives losses.

Both institutions have been accused of overcharging lenders for mortgage insurance.

Freddie and Fannie constitute an oligopoly. Oligopolistic competition should prevent

the firms from earning monopoly rents unless implicit or explicit price fixing is

occurring. Because these are GSEs and have subsidized funds costs, they may not be

aggressively pricing their services.

In 2003 both institutions restated earnings or equity. Fannie Mae restated equity by

$1.1 billion. Freddie Mac restated earnings by $4.5 billion. Both were claimed to be

computational errors. Both have since been found to have been manipulating

accounts to smooth earnings and in one case increase a bonus to an executive.

In February 2004, Alan Greenspan stated that both institutions posed serious risks to

the U.S. financial system. His concern was that their status as GSEs allowed Fannie

and Freddie to borrow excessively. The result was a new regulator for the industry,

the Federal Housing Finance Agency or FHFA.

In early 2007 Freddie Mac and Fannie Mae proposed buying billions of dollars of

subprime mortgages to ease credit problems in that sector. However, their public

statements may have only encouraged originators to increase lending into this sector,

perhaps worsening the subprime problems experienced since.

7-4

Chapter 07 – Mortgage Markets 6th Edition

On September 7, 2008 the Federal Housing Finance Agency (FHFA) placed both

Fannie Mae and Freddie Mac in government conservatorship. The FHFA suspended

dividend payments to both common and preferred stockholders and U.S. Treasury

began financing the two firms. As of April 2011, the taxpayers were out about $132

billion on the two mortgage agencies with more losses expected.

Private Mortgage Pass-Throughs

A limited number of private mortgage pass-through issuers deal with nonconforming

mortgages that do not qualify for government insurance. Prudential Home, Residential

Funding Corporation, GE Capital Mortgages, Countrywide, and a few other companies

create private mortgage pass-throughs. The acronym for private mortgage pass-throughs

is Privately Issued Pass-Throughs or PIPs. PIPs must be registered with the SEC and

normally are rated by one or more of the ratings agencies.

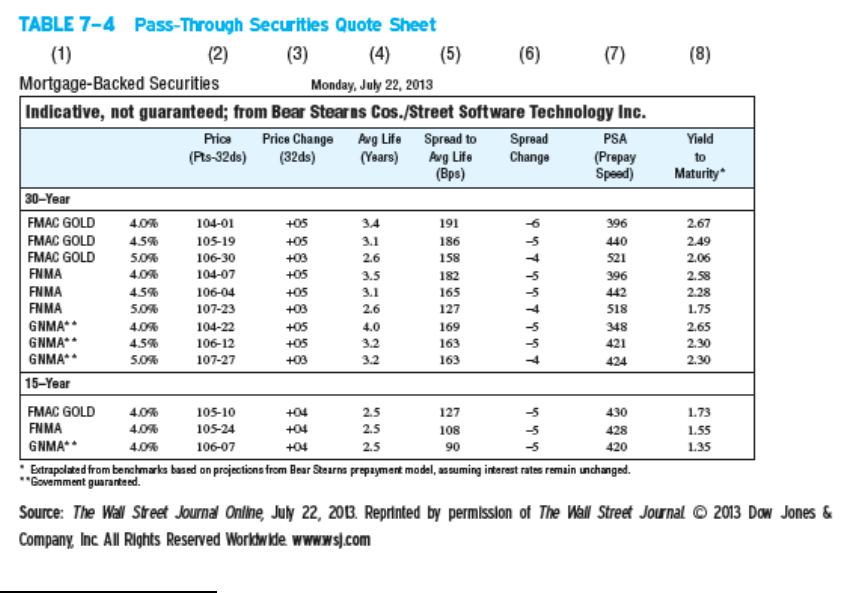

Mortgage Backed Pass-Through Quotes

Mortgage instruments are priced according to some assumed level of prepayments. The

SIFMA (formerly known as the Public Securities Association has developed what is

known as the “Standard Prepayment Model:” The SIFMA model of prepayments on

home mortgages is 0.2% initially with prepayments rising at 0.2% per month until month

30, after which prepayments remain at 6% per year.4 If 25% higher prepayments than the

standard are expected (usually due to falling interest rates) the mortgage instrument may

be priced with expected prepayments of “125% of SIFMA.”

Text Table 7-4 includes a quote sheet for various mortgage backed securities from July

2010. A portion of the table is reproduced and explained below:

4 There is a 30 month ‘ramp’ of increasing prepayments using the industry vernacular.

7-5

Chapter 07 – Mortgage Markets 6th Edition

FMAC is Freddie Mac, the term “Gold” indicates that the maximum delay from

receipt of payments by the fund sponsor and payment made to the investor is 55 days.

The percentages after the issuer or backer name are the coupon rates.

Price quotes are in 32nds as a percentage of par, akin to Treasury Bond quotes.

Average life is not the same as duration, rather it is the weighted average time in

which principal payments are received based on the given level of prepayments. Note

the association between SIFMA (or PSA) prepay speed and average life. Also note

the low expected average life even though the mortgages backing the securities are 30

year mortgages.

The spread to average life in basis points is the spread over a Treasury bond with the

same maturity as the average life.

PSA or SIFMA (Prepay speed) refers to whether the securities are expected to have

prepayments faster than the normal (>100%) or slower (<100%) than the standard

PSA prepayment levels. Standard PSA assumes that after a low amount of

prepayments over the first 30 months life of the pool, prepayments will average about

6% of the pool each year. 200% PSA would then represent 2 x 6% or 12%

prepayments per year after the initial 30 month ramp up in prepayments.

The yield to maturity is an estimated yield rate based on the expected level of

prepayments. Prepayment levels vary with interest rates and the yield rate will vary

as interest rates move.

Note the variation in prepayment rates in the expanded text table, ranging from 396% of

PSA to 521% of PSA. All of the prepay speeds are high because of generally low rates.

If rates rise, prepay speeds will fall.

Teaching Tip: It is important to understand that with a pass-through the investor bears all

the prepayment risk and the pool organizer has no prepayment risk. GNMA pass-through

securities are often sold as ‘guaranteed’ because of the government backing but investors

should understand that the rate of return on the pass-through is not guaranteed and can

vary widely with different prepayment patterns.

Collateralized Mortgage Obligations (CMOs)

7-6

Chapter 07 – Mortgage Markets 6th Edition

CMOs were created to allow investors to better choose and control the level of

prepayment risk they face. CMOs are a hybrid between a pass-through and a bond.

CMOs have different payment classes called tranches.5 Suppose the CMO has three

classes, A, B and C. The Class A CMO holder would receive all the initial principal

payments (on the entire pool), including all prepayments, whenever they occur, until all

the Class A holders have been paid off.6 Buyers of Class A CMOs are interested in short

duration investments. Initially, Class B and C holders would receive no principle, just

interest payments until all of the principle of Class A holders has been paid off.

Likewise, Class C is not affected by any prepayments until Class B holders have been

paid off. The multiple classes allow investors to better choose the level of prepayment

risk desired. CMOS can be used for other purposes such as credit enhancement as well.

The REMIC (Real Estate Mortgage Investment Conduit) is essentially a legal form of

CMO that avoids tax complications. The IRS normally does not allow an intermediary to

transform cash flows without taxing the activity. In 1986 Congress set up the REMIC as

a trust form that is exempt from IRS taxation.

Mortgage Backed Bonds (MBBs)

With MBBs, mortgages are pledged as collateral backing the bond issue. The MBB is in

all other respects similar to standard corporate bonds. In this case the bond issuer bears

the prepayment risk, and as a result the bonds normally have to be significantly

overcollateralized to obtain a favorable bond rating. MBBs are not technically a method

of securitization in that the bond issuer does not remove the mortgages from their balance

sheet; thus, issuing MBBs does not provide some of the aforementioned benefits of

securitization to the FI.

2. Participants in the Mortgage Markets

Who originates single family mortgages?

Banks

Thrifts

Mortgage companies

Other

Who finances mortgages? (Source Text)

Depository Institutions 33.25%

Govt Agency Holdings & Held in Pools 60.01%

Mortgage Companies 1.33%

Life Insurers 2.63%

Other FIs 0.55%

Other 2.23%

5 According to the Bond Market Association, now SIFMA, tranche is the French word for

slice.

6 This discussion applies to ‘sequential pay’ CMOS; other types exist. Two other

common types are ‘planned amortization classes’ or PACs and ‘tactical amortization

classes or TACs.

7-7

Chapter 07 – Mortgage Markets 6th Edition

There is a very large difference in the amount of mortgages originated by mortgage

companies and the amount financed. Most mortgage companies quickly sell the

mortgages they originate.

3. International Trends in Securitization

Outside the U.S., Europe has engaged in the most securitization. The conversion to the

Euro has increased the growth of securitization in Euroland. The United Kingdom has

more securitization than any other European country. France and Germany have not

progressed in securitization to the same degree.

Europe and Asian real estate markets have not been as hard hit as the U.S. because they

lacked substantial subprime lending. Great Britain and Ireland have experienced similar

problems, resulting in the bailout of Northern Rock, a large British mortgage lender and a

bailout of the six major Irish banks. The biggest banks in the Netherlands, Switzerland,

Iceland and Spain recorded annual losses during the crisis.

In October 2008 the German government guaranteed all consumer bank deposits and

arranged a bailout of Hypo Real Estate, the country’s second largest commercial property

lender. The Netherlands, Belgium and Luxembourg put together a $16.37 billion bailout

of Fortis NV. Many European and Asian countries quickly passes stimulus packages to

offset the problems in the U.S. and their own economies.

Securitization may take a different form overseas. So called ‘synthetic’ securitization is

more common where originators retain ownership of the mortgages. Global

securitization by region as a percent of global total is presented below:

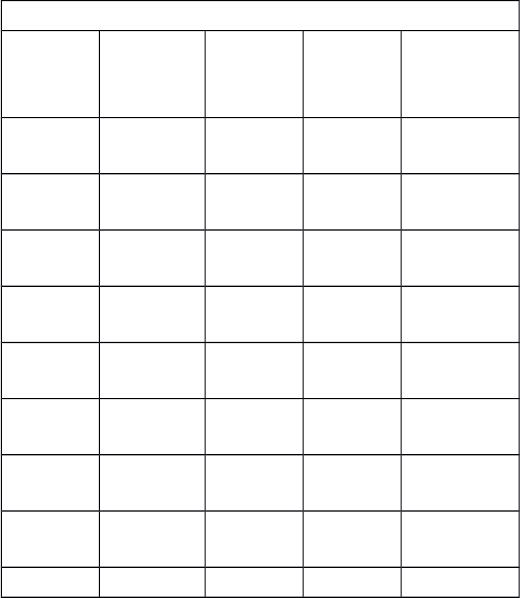

Global MBS issuance over time by region, Bill $

Year U.S. Europe Rest of

the

World

World

Total

2002 94.6% 3.7% 1.7% $2,470.8

0

2003 93.4% 4.9% 1.7% $3,396.3

0

2004 87.1% 9.2% 3.6% $2,199.8

0

2005 84.8% 11.5% 3.7% $2,629.2

0

2006 78.7% 16.7% 4.5% $2,680.5

0

2007 72.6% 23.0% 4.4% $3,035.6

0

2008 56.3% 38.9% 4.8% $2,493.0

0

2009 79.4% 16.8% 3.7% $2,569.8

0

2010 79.5% 17.0% 3.5% $2,484.0

7-8

Chapter 07 – Mortgage Markets 6th Edition

0

2011 77.3% 18.3% 4.4% $2,148.2

0

2012 84.7% 11.8% 3.5% $2,426.3

0

2013* 79.6% 8.5% 11.9% $731.90

* Through March 2013

Source: Text data

Appendix 7a: Amortization Schedules for 30-year Mortgages in Example 7-1 and in

Example 7-4, No Points versus Points, available on Connect or from your

McGraw-Hill representative

The appendix has amortization schedules to illustrate Text Examples 7-1 and 7-4. The

schedules show the remaining balance on two mortgages, one where the borrower pays

points, and one where they do not.

1.1.1.1 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal

Reserve

http://mortgage-x.com/x/rates.asp Website providing mortgage rates that can be parsed

by state and loan type.

http://www.mbaa.org Website of the Mortgage Bankers Association, a

trade group that provides research and forecasts

about the mortgage finance industry.

http://www.fanniemae.com/ Website of the Federal National Mortgage

Association

http://www.freddiemac.com/ Website of the Federal National Mortgage

Association

http://www.va.gov/ Website of the Veteran’s Administration

http://www.wsj.com/ Website of the Wall Street Journal Interactive

edition. The Online Journal frequently contains

updates on mortgage markets and home sales.

https://entp.hud.gov/idapp/html/hicost1.cfm HUD site containing FHA mortgage

limits (can search by state)

http://www.ginniemae.gov/ GNMA’s website, here the browser can learn about

GNMA pass-throughs and REMICs.

7-9

Chapter 07 – Mortgage Markets 6th Edition

http://www.fhfa.gov Federal Housing Finance Agency website, overseer

of mortgage markets and FNMA and FHLMC.

1.1.1.1.1.1 VII. Student Learning Activities

1. Go to the FHFA’s website and find the Housing Mission and Goals Statement. Read

and comment on the appropriateness of the statement in light of the recent financial

crisis.

2. Go to FNMA’s website and find a REMIC (CMO) prospectus. Read the section that

discusses the risk factors and discuss what affects the rate of return to a REMIC

investor.

3. Procure estimates of current mortgage rates, including discount points, on 30 year

fixed rate mortgage payments for a $200,000 conventional mortgage from four

mortgage lenders. Is it worth it to pay any of the required points if you can only

count on being in the house 4 to 5 years? Explain.

4. Go to the FHLMC website and read about career opportunities with this company.

Give a 10 minute oral report to your class discussing what you found.

Set up an amortization schedule in a spreadsheet for a 30 year fixed rate mortgage

with a 6% annual interest rate. Calculate the present value of the payments at a 5.5%

discount rate. Now suppose that the 6% mortgage is paid off in full after 10 years.

Find the required payoff in ten years. Now find the present value at 5.5% with the 10

year payoff. What happens to the present value of the cash flows with the

prepayment? Explain.

5. Go to the HUD site of the FHA that contains information on insurance limits

(https://entp.hud.gov/idapp/html/hicost1.cfm). Find the insurance limit in your area.

What are your options if you wish to have a larger mortgage than the insurance limit?

Explain.

7-10