a. Mortgage Characteristics

Although mortgages can have unique terms, the demands of the secondary market increasingly

determine the guidelines for accepting or rejecting a mortgage application.

Collateral

All mortgage loans are backed by collateral that will have a lien placed against it. A lien is a

public record attached to the title of the property that gives the financial institution the right to

sell the property if the mortgage borrower defaults. A lien prevents sale of the property until the

mortgage is paid off and the lien removed.

1.1.1.1 Down Payment

In the absence of government insurance, a down payment is required to minimize default risk.

An 80% loan to value ratio is standard. If a borrower cannot pay the required 20% down

payment they may obtain FHA insurance. FHA insurance has a maximum borrowing amount

that varies according to regional housing costs. The borrower may instead apply for private

mortgage insurance (PMI). Most PMI requires a monthly payment that is added to the

principle and interest payment. Although it can vary from lender to lender, the typical monthly

mortgage insurance payment if the borrower pays only 10% down can be found by multiplying

the loan amount times a constant factor equal to 0.0051 and then dividing the result by 12. For

instance, on a $100,000 mortgage with 10% down, the monthly PMI premium would be

($100,000*0.0051)/12 = $42.50. If you finance 97% the constant is 0.0090 and the monthly PMI

payment would be $75.1

PMI does not usually provide complete insurance. PMI may pay between 12 and 35% of the

difference in the home value and the balance owed. As a homeowner pays the balance down they

can petition to have PMI removed to eliminate the payment. The home will have to be

reappraised and the homeowner must petition for the removal. Expect a lengthy process.

Teaching Tip: Once the homeowner reduces the principle amount to 80% or less of the house

value, either through payments and/or appreciation of the value of the home, the homeowner

may wish to have the house reappraised and apply for termination of the mortgage insurance.

The appraisal cost may be as low as $500-$600.

Insured vs Conventional Mortgages

Conventional mortgages are mortgages not insured by the Federal government. The term

insured mortgages refers to mortgages insured by the Federal government, not privately insured

mortgages.

Mortgage Maturities

1 Thanks to Chuck Schmautz, a mortgage broker at First Security Bank for providing this

information.

The two standard maturities are 15 year and 30 year, with 30 year mortgages predominating.

Some contracts call for balloon payments at the end of three to five years. These contracts may

require interest only payments during the interim period. Most borrowers will not be able to pay

off the balloon so the borrower is essentially agreeing to refinance the mortgage when the

balloon is due.

Teaching Tip: A balloon payment mortgage is riskier to the borrower because there is no

guarantee that refinancing will be granted. An injury or illness, a layoff, etc. can endanger an

individual’s primary asset, their home.

Interest Rates

Mortgage rates are a function of the fed funds rate, discount points paid, whether the loan is a

FHA or a conventional mortgage, maturity, whether the mortgage is fixed or adjustable rate,

regional demand for funds and the level of competition of suppliers of mortgage credit. Regional

credit availability is not an issue due to the national financing market.

1.1.1.2 Fixed versus Adjustable Rate Mortgages

Fixed rate mortgages (FRMs) remain the most popular mortgage type, although a significant

number of mortgages are adjustable rate. With the low rates of the early 2000s, adjustable rate

mortgages (ARMs) have not been as popular as in prior periods (at one point several years ago

50% of new originations were adjustable rate). The payment on ARMs can vary as the

applicable interest rate index changes. The index used cannot be the lender’s cost of funds and is

often an index of lenders’ fund costs (termed a COFI or cost of funds index). The rate change

per year and over the life of the mortgage is capped and prepayment penalties are not allowed

on ARMs. With a fixed rate mortgage the lender bears the interest rate risk, with an ARM the

borrower bears the interest rate risk.2 As we saw in 2007 and 2008 ARMs result in higher

default risk for lenders in periods of rising interest rates. When rates rise, borrowers have more

difficulty making the payments on their mortgage. The share of ARMs as a percentage of new

originations has fallen dramatically and is at about 5% in 2010 according to the MBA Mortgage

Finance Forecast.3

Teaching Tip: A home mortgage is usually the largest single monthly payout of the individual. It

may be prudent to know with certainty what this amount will be. If a borrower wishes to use an

ARM he or she should ensure they fully understand all the details, indeed, having a lawyer

review the loan contract is an excellent idea. An ARM borrower should determine the maximum

monthly payment and ensure that they can comfortably handle that amount. The two most

common types ARMs are fixed for 5 years, then floating and adjustable every year. The

borrower must take care when purchasing an ARM that is fixed for 5 years to ensure that they

can handle the maximum payments when the mortgage is recast and to be aware of any

possibility of negative amortization. ARMs offer teaser rates to entice borrowers to purchase

them. The size of the rate difference between an ARM and a FRM varies between rate

environments. Recently the fixed for 5 year ARM offered a 50-75 basis point advantage over 30

year FRM rates. The annual adjustment ARM usually offers a much larger advantage,

sometimes as high as 200 basis points over 30 year FRMs. These spreads vary as rate

2 The cap implies that even in an ARM the lender still bears some interest rate risk.

3 See the Mortgage Bankers Association website at www.mbaa.org.

expectations change however.

The FHFA publishes the National Average Contract Mortgage Rate for the Purchase of

Previously Occupied Homes by Combined Lenders. Some lenders use this rate for setting

interest rates on ARMs. Federally chartered savings associations must use this rate. It can be

found at www.fhfa.gov and as of May 2014 the rate was 4.53%.

Teaching Tip: A buyer should ascertain the type of home that is easily saleable in their area.

They should not be in a hurry when purchasing a home. “Shop till you drop” is good advice in a

major, often illiquid investment. Typically, a home buyer should not buy a home where the total

monthly payment will be more than 25%-35% of their current take home pay. One won’t enjoy a

home that one can never afford to leave, and financial frictions are a major source of stress on

relationships.

Teaching Tip: The borrower can often obtain a conversion option which allows the borrower to

convert the ARM to a fixed rate mortgage. This option is usually granted within a narrow time

window, say from year 3 to year 5. It is usually not a good deal because the conversion will

typically occur at a markup over fixed rates at the time of the conversion, not at today’s fixed

rates.

Teaching Tip: Because of the annual caps ARMs can be good deals if you believe you will either

move or refinance in 3 to 5 years as long as the borrower is aware that there is a possibility of not

being able to refinance due to changes in the borrower’s condition or changes in the housing and

mortgage markets.

1.1.1.3 Discount Points

A borrower can buy a lower interest rate by paying points up front. A discount point is 1% of

the loan amount. Lenders periodically establish point schedules that show what interest rate they

are willing to offer if the borrower pays a certain amount of points. A simple breakeven analysis

can be used to determine whether the borrower should pay the points. The dollar value of the

points / monthly payment savings = number of months required to recoup the points. If the

borrower expects to live in the house for the breakeven number of months or longer, it is

worthwhile to pay the points. This example ignores taxes.

When should you pay points? You are thinking of purchasing a $100,000 home and making a

20% down payment. The 30 year mortgage rate is 8 1/4% at par, but you can get an 8% rate by

paying 5/8s of a point. What should you do if you are not going to prepay the mortgage?

(Ignore taxes)

If you don’t pay the points (r = 8 1/4% / 12 = 0.6875%):

$80,000 = $PMT * [1 – 1.006875-360] / 0.006875

$PMT = $601.01

If you pay the points (r = 8% / 12 = .6667%)

$80,000 = $PMT * [1 – 1.006667-360] / 0.006667

$PMT = $587.01

Payment Savings = $601.01 – $587.01 = $14 / month

Cost: 5/8s of a point = 0.625% * $80,000 = $500

Would you pay $500 today to save $14 a month?

What is the breakeven?

W/ Payments

$500 = $14 * [1 – 1.006667–N ] / 0.006667]

Reinvested4Solve for N (r = 8%/12)

N = 40.93 months or 3.4 years

W/O Payments Easy way: $500 / $14 = 35.71 months or 2.98 years

Reinvested

Pay the points if you believe you will keep the mortgage for at least as long as the breakeven

time period.

The refinancing decision is similar, instead of the points cost the refinancing (refi) cost will be

the present value and the payment savings will be payment. One can also calculate the net

present value of paying the points or of the refi decision.

Teaching Tip: You might wish to advise your students that if the breakeven is 5 years or longer,

it is probably not worth paying the points because most people’s life circumstances are likely to

have changed by 5 years, and one cannot tell whether one will still wish to remain in the same

house after that time.

The above analysis assumes the homeowner does not prepay the mortgage. Paying the points

results in a lower interest rate and thus more of each payment goes to principal with the lower

rate. This will yield a slightly lower required payout in the event the mortgage is prepaid. The

present value of this amount will be small if the mortgage holder remains in the home for a long

time. The text provides an example of finding the approximate breakeven time to prepay for the

decision of when to pay points. The text breakeven example ignores taxes and is an

approximation only because it appears to ignore the difference in the balance from the two loans

over time.

Other Fees

A homebuyer will normally face a host of fees (payable at closing or before) including:

Application fee

Title search fee

Title insurance fee

Appraisal fee

Loan origination fee (usually 1% of the loan amount)

Closing agent/review fee

Costs to obtain mortgage insurance (FHA, VA or private) if needed

Teaching Tip: Closing costs average from 3%-5% of the mortgage amount (excluding points),

with 3% the most common.

4 This method assumes the $14 per month savings is invested at the monthly rate of .6667% per

month. If the money is not reinvested, the ‘without payments reinvested’ method is correct.

Mortgage Refinancing

Due to low interest rates in the 2000s, mortgage refinancing business boomed. In the early

2000s refinancings comprised 70% of all originations, but more recently have comprised

between 40% and 60%. Refinancings are expected to fall in 2014 as interest rates are projected

to increase. A typical rule of thumb is that the new mortgage rate should be 200 basis points

below the old rate, but with ARMs and reduced refinancing costs refinancings can be worthwhile

at smaller rate reductions. A breakeven similar to that mentioned above can be used to determine

if refinancing is worthwhile.

Teaching Tip: According to Corelogic home prices increased 11.2% in Q3 2013 from the same

quarter in 2012 and are predicted to increase 3.1% per year for next 5 years.

b. Mortgage Amortization

The typical mortgage is fully amortized at the original maturity so that the principle is reduced

with each payment and no balloon remains at maturity. Amortizing payments are calculated

using the present value of annuity formula. An amortization schedule depicts the amount of

each payment that goes to principle and to interest.

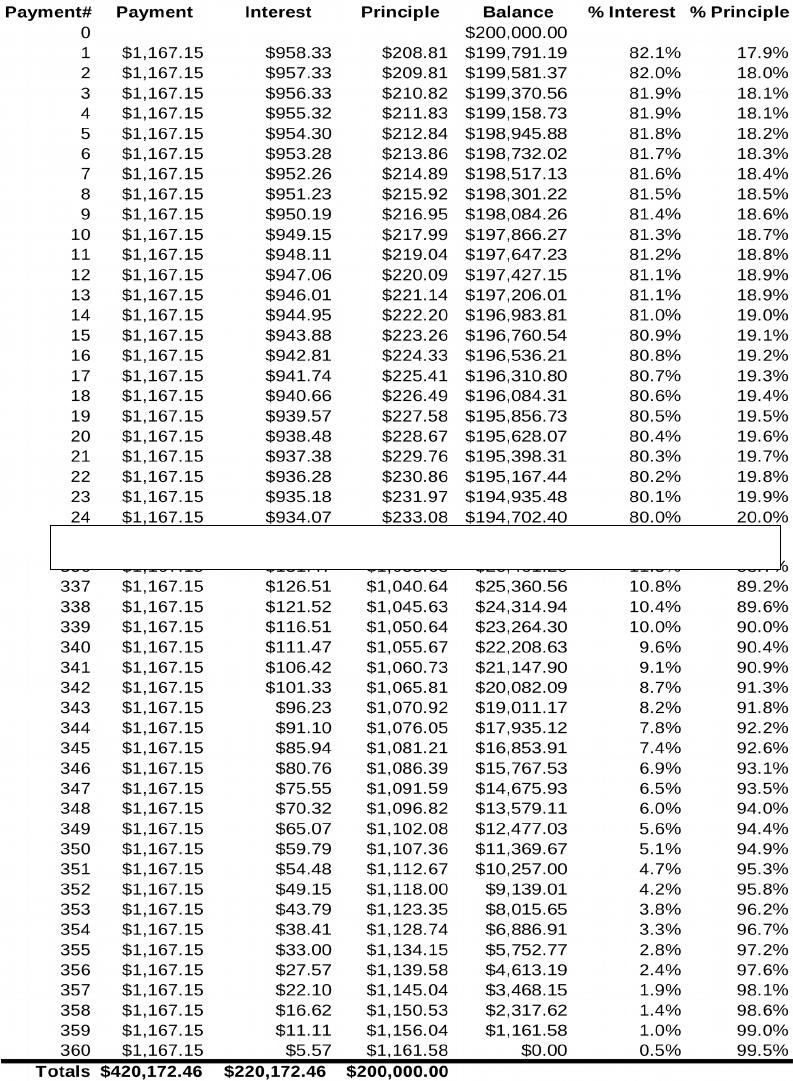

Example 1:

A borrower agrees to a $200,000, thirty year fixed rate mortgage with a 5.75% (or 0.4792% per

month) quoted interest rate. What is the payment amount and how much of each payment goes

to principle and interest?

Payment = $200,000 / (1-1.004792-360)/0.004792 = $1,167.15. The amortization schedule below

provides the breakdown of each payment into principle and interest on a dollar and a percentage

basis. The first 24 and the last 25 months of payments are shown.

Notice that the total interest paid on the mortgage ($220,172.46) is greater than the original

balance.

….………………

…

Example 2: Recent sample of rates on a $244,000 Mortgage (current quotes are available at

BankRate or at http://mortgage-x.com/x/rates.asp and are searchable by state)5

15 yr FRM 3.125% Par

30 yr FRM 4.25% Par; 4.125% 1.00 pt

P&I Payment on the 30 year (Par): ($244,000 mortg.) $1,200.33

P&I Payment on the 15 year (Par): ($244,000 mortg.) $1,699.73

Payment Difference – $ 499.39

Total Interest paid on the 30 yr FRM: $ 188,120

Total Interest paid on the 15 yr FRM: $ 61,951

Interest Difference $ 126,169

Teaching Tip: Be sure that students understand that their total monthly payment will normally be

about $100-$200 higher than the principle and interest payment due to insurance and taxes.

c. Other Types of Mortgages

Jumbo Mortgages

Jumbo mortgages are mortgages for loan amounts that exceed the maximum ‘conforming’ limits

allowed by the mortgage agencies Fannie Mae and Freddie Mac. Congress actually can specify

these maximums. In 2014 the maximum amount was $417,000, although there have been

exceptions due to the crisis.6 Jumbo mortgage interest rates have a 25 to 50 basis point spread

over conforming mortgages and may require a higher down payment.

Subprime Mortgages

Subprime mortgages are mortgages where the borrowers do not qualify for a ‘prime’ credit rating

because of a low credit score arising from prior credit problems such as delinquencies and

defaults. Or they may simply lack sufficient credit history or have insufficient income.

Subprime originations were about 9% of the total between 1996 and 2004 but increased to 21%

in the 2004 to 2006 time period. Originators weakened their credit standards and quickly sold

the mortgages. Congress encouraged this, particularly after the Democratic takeover of

Congress. ARMs and Interest Only mortgages were also used to make initial payments low to

encourage more home buyers. Both of these mortgages are likely to force homeowners to make

higher payments if interest rates rise over the life of the loan. When credit problems emerged in

this sector it led to a correction of housing prices in the broader market in part because of

securitization of mortgages which included the subprimes. Sharp declines in subprime backed

mortgage securities quickly led to the financial crisis.

Alt-A Mortgages

Alt-A is short for Alternative A- Paper. This term is used for mortgages that are riskier than

prime but not as risky as subprime. They may represent borrowers who have incomplete

documentation, poorer credit scores, higher loan to value ratios, etc. than prime mortgages.

Interest rates on Alt-A loans are usually between prime and subprime rates. Alt-A loans do not

conform to Fannie Mae and Freddie Mac standards.

5 Rates are higher on ‘jumbo’ mortgages.

6 https://www.fanniemae.com/singlefamily/loan-limits

Option ARMs

Option ARMS may also be called ‘pick-n-pay’ mortgages. These loans allow the borrower to

choose between various payment options. The four main types are

a) Minimum payment

This version provides the lowest initial payment, usually at a1% rate. The initial payment

is set for 12 months and after that it varies. A payment cap limits how much the payment

can vary. The text quotes a 7.5% cap. Continuing to make minimum payments will

result in capitalization of unpaid interest which will add to the loan amount, resulting in

negative amortization. A borrower is allowed to pay the minimum until the loan balance

reaches 110% to 115% of the original loan balance. After this maximum is reached the

borrower loses this option and must go with one of the other three. This alternative is

very risk for the borrower and should be discouraged.

b) Interest only payment (IO)

An IO mortgage allows the borrower to pay interest only (at an adjustable rate) initially.

The IO option is eliminated at some point in the mortgage, usually 5 to 10 years from the

start. At that point the payment will increase, usually substantially as the principal must

now be amortized over the remaining life of the mortgage. Payments can thus increase

due to higher interest rates and due to the switch to amortization. Before the crisis, these

options were sold to naïve borrowers, but they are obviously very risky. The borrowers

were apparently told they were not risky, or the risk was downplayed because the

homebuyers were told they could refinance when the payments increased. The financial

crisis eliminated this option however. At the end of the IO period the borrower must

choose between the remaining two options below.

c) A 15 year fully amortizing payment

At this point the payment is the same as a 15 year ARM with monthly payment

fluctuations, although the payments are likely to be higher than if a 15 year ARM had

been originally if the minimum payment or IO options were used.

d) A 30 year fully amortizing payment

At this point the payment is the same as a 30 year ARM with monthly payment

fluctuations, although the payments are likely to be higher than if a 15 year ARM had

been originally if the minimum payment or IO options were used.

Second Mortgages

Second mortgages are subordinated claims to senior mortgages. About 15% of primary mortgage

holders have a second mortgage. Seconds totaled about $1.09 trillion in 2007. Home equity

loans allow customers to borrow on a line of credit secured with a second mortgage. Interest on

home equity loans is normally tax deductible whereas credit card interest is not.

Teaching Tip: Be careful advising individuals to use a home equity loan to pay off credit card

debt. Theoretically, an expensive vacation or even a shopping spree could endanger your home

ownership if the buyer cannot manage credit properly. Under today’s bankruptcy laws, unpaid

credit card debts will not normally result in the loss of home ownership, whereas default on a

home equity loan will cause the loss of the home.

Teaching Tip: Citigroup and Household International came under fire in 2002 for their aggressive

marketing tactics used in selling mortgages to subprime borrowers.

Reverse Annuity Mortgages (RAMs)

RAMs are for homeowners with a substantial amount of equity in their home who wish to

supplement their income, usually retirees. Note that RAMs are sometimes called REMs

(Reverse Equity Mortgages). With a RAM the FI makes a monthly payment to the homeowner.

The FI is in effect buying out the homeowner’s equity over time. At maturity the house is sold

and the proceeds are used to pay off the FI. RAM maturities are usually set up so that the

homeowner will die before maturity. As the population ages and health care costs increase

RAMs are likely to grow in popularity. In the short term the housing market continues to soften

and home prices fall, RAMS may not be attractive to lenders.

The OTS provides an information packet on RAM with the following information:

•The homeowner can choose from various payout methods. The payout can be 1) lump

sum, 2) monthly payment for tenure (as long as the homeowner lives in the house), or a

fixed term and 3) credit line or combo of 2) and 3).

•REM Costs are higher than for standard mortgages:

Higher origination fees, closing costs and servicing fees

Most (90%) are FHA insured and so have 2% mort. insurance premium plus ongoing fee

for a rising loan amount

Origination fees are based on the home value, not loan amount, and home value is greater

than loan amount

Closing costs run between $7,000 and $15,000. If the owner moves or dies quickly, they

may not recover those costs.

•Financial counseling is required because these are complex instruments.

Teaching Tip: Don’t want to leave anything to the kids? They never visit anyway? Use a RAM

and enjoy your retirement!

Teaching Tip: New Types of Mortgages (from Smart Money Column: Mortgages Get More

Exotic, by Stacey Bradford, Wall Street Journal Online, July 25, 2004)

40 year mortgages

Negative Amortization Mortgage

Flex-ARM mortgage

Piggyback Mortgage or Combo loan

103s and 107s

Details are available from the article. Most of these alternative mortgage types are riskier for

home buyers and many are no longer available after the financial crisis; most are generally

methods to buy more house than you could otherwise afford.

The following website has spreadsheets depicting how negative amortization of ARMs can affect

payments. The results are surprising.

http://www.decisionaide.com/mpcalculators/NegativeARMS/NegativeARM.asp