1.1.1.1.1Chapter Seven

Mortgage Markets

1.1.1.2 I. Chapter Outline

1. Mortgages and Mortgage-Backed Securities: Chapter Overview

2. The Primary Mortgage Market

a. Mortgage Characteristics

b. Mortgage Amortization

c. Other Types of Mortgages

3. The Secondary Mortgage Markets

a. History and Background of Secondary Mortgage Markets

b. Mortgage Sales

c. Mortgage-Backed Securities

4. Participants in the Mortgage Markets

5. International Trends in Securitization

Appendix 7a: Amortization Schedules for 30-year Mortgages in Example 7-1 and in Example

7-4, No Points versus Points, available on Connect or from your McGraw-Hill representative

II. Learning Goals

1. Distinguish between a mortgage and a mortgage-backed security.

2. Describe the main types of mortgages issued by financial institutions.

3. Identify the major characteristics of a mortgage.

4. Examine how a mortgage amortization schedule is determined.

5. Describe some of the new innovations in mortgage financing.

6. Define a mortgage sale.

7. Define a pass-through security.

8. Define a collateralized mortgage obligation.

9. List the major mortgage holders in the United States.

10. Describe the trends in the international securitization of mortgages.

1.1.1.3 III. Chapter in Perspective

This is the third chapter that covers securities markets and it has three major sections. The

primary characteristics of standard fixed and adjustable rate mortgages are covered first. The

second major topic is innovations in mortgage financing methods. Secondary mortgage markets,

government agency involvement in mortgage markets and securitization methods are presented

in the final major section. A brief discussion of international trends in securitization concludes

the chapter. The securitization material is conceptually much more difficult than the prior topics.

The purpose of the chapter is to give the student an understanding of the characteristics of

mortgages and mortgage terminology and alternative means of obtaining mortgage credit. The

reader should also understand the advantages and disadvantages of securitization for financial

intermediaries and the major features of different types of mortgage-backed securities.

1.1.1.4 IV. Key Concepts and Definitions to Communicate to Students

Mortgages Second mortgages

Securitization Home equity loan

Lien Reverse annuity mortgage

Down payment Sale with recourse

Private mortgage insurance Pass-through mortgage securities

Insured vs conventional mortgages Timing insurance

Fully amortized vs balloon payment mortgages CMO tranche

Fixed vs adjustable rate mortgages Subprime mortgage

Discount points Option ARMS

Amortization schedule Correspondent banking

Jumbo mortgages Single family mortgages

Alt-A mortgages Privately issued pass-throughs

Mortgage backed bonds (MBBs) Origination versus financing

Subprime mortgages Government agencies

Mortgage companies

1.1.1.5 V. Teaching Notes

1. Mortgages and Mortgage-Backed Securities: Chapter Overview

Mortgages are loans to purchase a home, land or other real property. Late in 2013 there were

$13.244 trillion of mortgages outstanding. About 74.5% of mortgages are single family (1-4

family) mortgages. The rest are divided between commercial mortgages (17.2%), multifamily

dwelling mortgages (6.9%) and a small amount of farm mortgages (under 1%). This chapter

covers the primary and secondary market characteristics of single family mortgages.

There is a well developed and active secondary market for mortgages, unlike many other loan

types. Government involvement in the single family secondary mortgage market through

insurance and promoting securitization has led to the active secondary market for mortgages.

Securitization is the process of transforming individual loan contracts into marketable securities.

About 50%-60% of single family mortgages are typically securitized, with about 60% in

2013. Mortgage contracts by themselves would not be particularly saleable because they have

nonstandard, fairly small denominations and unique, potentially substantial credit risk. A

saleable contract should have a standard, large denomination to appeal to institutional buyers, a

low cost method of assessment of credit risk, good collateral, a standard maturity, and a standard

interest rate.1 Mortgages have generally good collateral, standard lengthy maturities and

standard interest rates. The small and variable denomination of individual mortgages implies

that mortgages should be pooled to create a typical large denomination. Credit risk analysis of

the many individual borrowers in the pool would be quite costly and would severely limit the

usefulness of the securitization process if not alleviated. Thus, for most mortgages that are

securitized either the government provides insurance for mortgages, an 80% loan to value ratio

is required, or the mortgage must be privately insured perhaps by a firm such as CMG

Mortgage Insurance.

Teaching Tip:

FHA insurance cost is two-fold, and some costs vary with down payment & mortgage amount

but there is generally an upfront cost of 1.75% of total loan amount, which can be financed, and

an annual premium that varies with the loan to value (LTV) ratio and mortgage maturity. For a

30 year mortgage with a LTV ratio of 95% or more the annual premium is 1.30% of the loan

amount (paid monthly).

Securitization brings many benefits to FIs. Securitization allows FIs to a) become more liquid,

b) reduce interest rate and credit risk, c) reduce capital and reserve requirements, and d) generate

fee income from servicing more mortgages than they could otherwise.

The mortgage markets are huge (they are larger than the corporate debt market), rapidly growing

(from 2001 through 2013 the amount of single family home mortgages grew by about 73%) and

have become increasingly sophisticated. Even with the downturn in mortgages in the late 2000s,

mortgage markets are likely to generate long term growth. In some areas home prices have

advanced more rapidly than income growth, leading to slowed growth in housing prices and even

declines in some markets such as Florida. In other countries and in our own past, severe

collapses in housing prices have presaged protracted periods of low economic growth or even a

prolonged recession, so over the short to intermediate term, the housing market may remain a

drag on growth.

In 2006, 2007 and 2008 problems in the subprime mortgage market led to the credit crunch of

2007 and 2008. A subprime mortgage is a mortgage made to a borrower with a below normal

credit rating. Credit problems in the sector eventually bankrupted Countrywide Financial, the

largest mortgage issuer, in the summer of 2007. The subprime problems spread to the broader

mortgage markets and resulted in a weakening of stock markets throughout 2007 and on into

2008. According to the Mortgage Bankers Association (MBAA) delinquency rates for

mortgages in the second quarter of 2007 were at 5.12% of all loans, up from prior quarters and

the prior year. The percentage of loans in foreclosures in the same time period was 1.40%, also

up. The rate of loans entering the foreclosure process was 0.65%, also an increase. Interestingly

however, these numbers were driven by mortgage markets in a relatively small number of states.

1 Standardization improves salability. Standard terms improve the ability to market an issue to

buyers because they are more familiar with the terms and risks of the investment.

National foreclosure rates would have fallen if one excluded California, Florida, Nevada and

Arizona. Delinquencies and foreclosures in mortgages and falling home prices were also

problems in Ohio, Michigan, Indiana, Illinois, Kentucky, Tennessee and Pennsylvania.

Delinquencies and foreclosure rates were higher for ARMs than for fixed rate mortgages.2

According to the Office of the Comptroller of the Currency (OCC) as of the end of 2013 about

92% of mortgages in their sample were current and performing. About 3.5% of mortgage

holders were at least 60 days behind on their payments or in the foreclosure process. Census

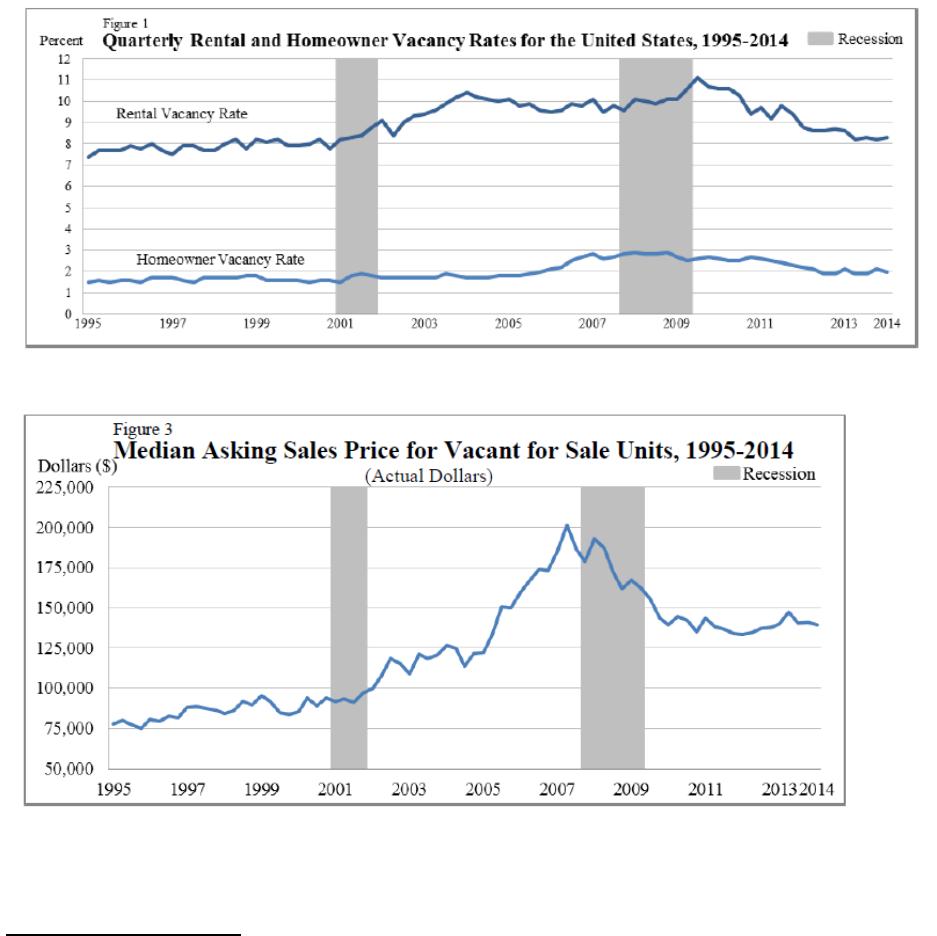

Bureau housing vacancy rates over time are presented below:

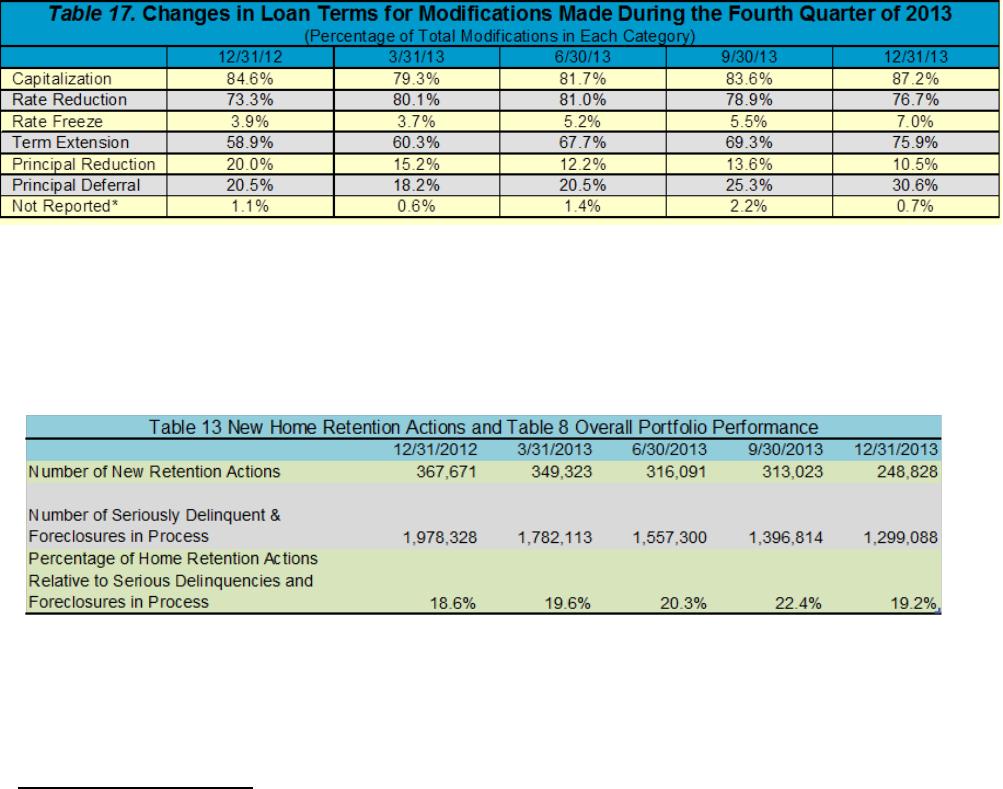

The median asked sales price in the first quarter of 2014 was $139,200 according to the BEA.

The OCC suggests standardized definitions for categories of mortgage creditworthiness based on

the following ranges of borrowers’ credit scores at the time of origination:3

Prime: 660 and above 75% of mortgages

2 “Delinquencies Increase in Latest MBA Delinquency Survey,” by Angela Waugaman,

Mortgage Bankers Association website, 9/6/07 Press releases,

http://www.mbaa.org/NewsandMedia/PressCenter/56555.htm

Alt-A: 620 to 659 10%

Subprime: < 620 6%

Unknown 9%

The percentages are the proportion of the mortgage portfolio held in OTS supervised institutions.

The loans in the data that were not accompanied by credit scores are classified as “other.”

Between May 2005 and February 2007 subprime mortgage default rates increased from 5.37% to

10.09%. Subprime mortgage holders 60 days or more behind in their payments hit 17.1% in

June 2007 and was over 20% in August of the same year. Problems in the subprime market

spilled over to the broader mortgage markets and helped fuel nationwide declines in home prices

which put many homeowners underwater. These mortgage types are also discussed under

mortgage types below.

The Obama administration has employed the Home Affordable Modification Program (HAMP)

to encourage and subsidize lenders to change mortgage terms for homeowners who are

delinquent in their payments.

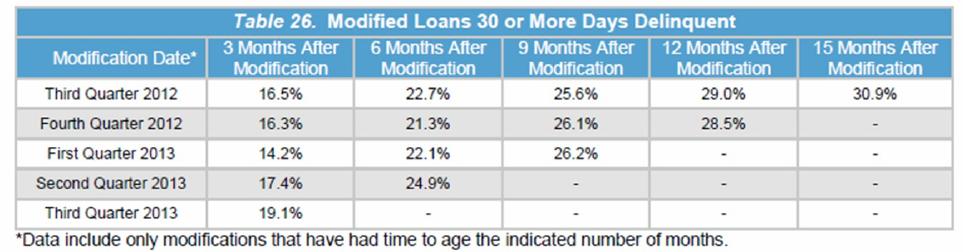

Source: OCC Mortgage Metrics report

Capitalization is adding missed payments to the loan amount. Note the low number of principal

reduction modifications. Principal reduction is probably the most effective method of ensuring

homeowners do not default given the declines in home prices, but lenders do not like principal

reduction, presumably because they must immediately mark down the value of the loans.

Source: Adapted from OCC Mortgage Metrics report

Not all of these are permanent loan modifications, many are trial period plans and temporary

payment reduction plans. Not all are HAMP plans; some were done independently by private

lenders. Notice that the number of modifications is small relative to the number of seriously

3 Unless noted otherwise all data in this section, including the tables, are from OTS Mortgage

Metrics.

delinquent (60 days or more past due) and foreclosures.

After modification, substantial numbers of home owners continue to have trouble making

payments as data in the following table indicate.

Source: OCC Mortgage Metrics report

Ethics Teaching Tip: The ability to sell and securitize mortgages coupled with a lack of

regulation of mortgage originators, particularly mortgage companies, helped create the subprime

crisis. An extended period of low interest rates in the 2000s helped contribute to rising home

prices, which then gave the appearance of low risk in mortgages. Mortgage originators knew

they would quickly sell the loans and pocket the origination fee. They may or may not retain the

servicing contract which would generate more fee income. Nevertheless, since the mortgages

were sold without recourse to the originator, increasingly lax credit standards were applied. Lax

standards led to poor lending practices such as ‘Low Doc” or “No Doc” loans referring to either

low or no documentation required demonstrating the borrower’s ability to repay the mortgage.

These loans were even given the appellation “Liar’s Loans” because allegedly mortgage lenders

coached applicants to fill out applications to ensure the mortgage would be approved and could

be resold with little regard to the veracity of the statements made. As long as the borrower made

three payments on the mortgage after origination, the originator was free and clear from

recourse. Hence, there was little reason to apply tight credit standards.

What hindsight reveals as excessive risk taking has happened over and over in periods of

booming markets. In these cases participants underestimate risk and reduce risk aversion to the

point where excessive risks are engendered. Whether this results from hubris, its twin,

overconfidence, a lack of economic training and experience, or just poor ethics no one knows for

sure. Undoubtedly it is a result of all these elements combined. The laws of financial gravity,

particularly with respect to long periods of price increases, have not been repealed by financial

innovation and the many risk sharing contracts now being promulgated. For all our

sophistication in finance we should remember two things: 1) It is impossible to eliminate

systemic risk in the aggregate, although you can share it among an increasing number of

participants with the many derivatives we now have; and 2) Policies promoting both solid

ethics and conservative financing principles are always needed. The more ethics failures we

endure, the tighter regulations will have to become, with all the inefficiencies and increase in

regulatory burdens this entails. It is also becoming increasingly obvious to me that

regulations/regulators have not kept up with financial innovation. Whether this is due to inherent

conflicts of interest, lack of funding or training or other reasons cannot be determined. When

you include overseas markets it becomes apparent that we have been moving from one crisis to

another every few years as capital markets have grown at such a rapid pace with extensive

innovation. Perhaps this is nothing new, the capital markets have always operated under the

premise of “caveat emptor.”

2. The Primary Mortgage Market

The origination and financing of mortgages are now largely separate functions. One of the

primary purposes of the government’s presence in the mortgage markets is to ensure the

availability of mortgage credit wherever it is demanded. Government mortgage insurance and

the securitization process have created a national market for financing mortgages. Thus, the

financing of mortgages is national, or even international, in scope. The origination (creation) of

mortgages is still primarily a local market, for instance, typically one does not go to another state

to obtain a mortgage. The originators, however often sell the mortgage (individually or in a

pool).4 Electronic mortgage origination has not grown as dramatically as predicted. Applying

for a mortgage online remains a cumbersome task, hurting this area of business.

Teaching Tip: Government involvement has accomplished at least two socially desirable

outcomes. One, it has allowed younger, less wealthy people to own homes by eliminating the

large down payment, thus facilitating a part of the “American dream” of home ownership.

Second, it has helped poorer regions of the country such as West Virginia, Montana, etc that

would not have had enough mortgage credit available to meet the demand for funds.

Teaching Tip: For many people, home ownership is one of the most satisfying assets they obtain.

It is a person’s major hedge against personal disasters and inflation. Even in low inflation times

it is usually (but not always) an appreciating asset and, unlike automobiles, should be considered

an investment. Homes are an illiquid investment and living in the wrong house for you in the

wrong area can make you miserable for a long time, so please advise students to shop wisely.

4The origination market is itself however becoming increasingly national because mortgage

companies (a local originating institution) often obtain mortgage financing from institutions

around the country.