Chapter 06 – Bond Markets 6th edition

d. Bond Ratings and Interest Rate Spreads

Most bonds are rated in terms of default risk by at least one of the major ratings agencies,

typically Moody’s and/or Standard and Poors. Many institutions can hold only limited

amounts of unrated or low rated debt, so a favorable rating lowers the interest yield

required and increases the amount of potential buyers. Junk bonds are bonds rated

below Baa by Moody’s or BBB by S&P. Higher ratings are termed investment grade

bonds. Explanations of the ratings may be found in the text. In general ratings agencies

evaluate the industry strength, the firm’s position in the industry, liquidity, profitability,

debt capacity and since Sarbanes-Oxley, corporate governance. Each specific rated issue

is also examined for protection provided to investors as well as the firm’s ability to pay.

According to Alamo Capital, in May 2014 the average yield on 10 year A rated bonds

was 3.31% while the average yield on the 10 year Treasury was 2.48% for a default yield

spread of 83 basis points. The average rate on high yield debt was 5.27% providing an

additional credit spread of 196 basis points. On a $50 million bond issue, having a junk

rating would add an additional $980,000 in pre-tax interest expense per year. As you can

see, the rating substantially affects bond financing costs. Ratings spreads tend to vary

inversely with the phase in the cycle of the economy. From 1980 to 2002 the cumulative

default rate (CDFs) on 10 year Aaa rated bonds was 0.03% and the CDF was 9.63% on

Baa rated bonds.

The CDF for any year t of an N year bond can be calculated as

t

j

jt SurvivalobPr1CDF

To find the CDF after two years for an N year bond that has a 98% chance of survival in

year 1 and a 97% chance of survival thereafter:

%94.4)97.0*98.0(1SurvivalobPr1CDF

2

j

jt

Survive

97%

Survive

Year 1 98% Year 2 CDF

Decision

3% Tree

2% Don’t Survive

Don’t

Survive

Ratings agencies have been criticized for failing to downgrade firms quickly when

6-1

Chapter 06 – Bond Markets 6th edition

conditions deteriorate.1 The Dodd-Frank bill allows investors to sue for ‘knowing or

reckless’ failure to properly rate certain risky securities. In hindsight, the ratings agencies

granted too high ratings to issuers of mortgage backed securities. The text discusses a

possible motivation for the ratings firms. The high ratings granted to certain tranches of

collateralized debt obligations (CDOs) allowed excessive issuance and excessive

leverage to be employed by hedge funds, banks and investment banks. This leverage

eventually led to the credit crunch and the demise of Bear Stearns.

As noted above, junk bonds (also called speculative grade or high yield bonds are those

rated below Baa3 or BBB-) carry considerably more risk and higher yields. The higher

yields may be necessary because many institutions are limited in the extent to which they

can hold junk debt. Junk bonds have often been used to finance takeovers, limiting the

amount of equity required by the acquirer. Junk issuance fell dramatically during the

crisis but rebounded on the low rates. Issuance was $2214 billion in 2011,$362.2 billion

in 2012 and $173.9 billion in the first half of 2013.

Bond Credit Ratings (Source: Text Table 6-10)

Explanation Moody’s S&P Fitch

Best quality; smallest degree of risk Aaa AAA AAA

High quality; slightly more long-term risk than

top rating

Aa1 AA+ AA+

Aa2 AA AA

Aa3 AA- AA-

Upper medium grade; possible impairment in the

future

A1 A+ A+

A2 A A

A3 A- A-

Medium grade; lacks outstanding investment

characteristics

Baa1 BBB+ BBB+

Baa2 BBB BBB

Baa3 BBB- BBB-

Speculative issues; protection may be very

moderate

Ba1 BB+ BB+

Ba2 BB BB

Ba3 BB- BB-

Very speculative; may have small assurance of

interest and principal payments

B1 B+ B+

B2 B B

B3 B- B-

Issues in poor standing; may be in default Caa CCC CCC

Speculative in a high degree; with marked

shortcomings Ca CC CC

Lowest quality; poor prospects of attaining real

investment standing CCC

Payment Default D D

1For more information see Frank Portnoy’s testimony before a U.S. Senate Committee on

January 24, 2002 on the Enron affair, available in Financial Engineering News June/July

2002, No. 26. Professor Portnoy is a law professor at the University Of San Diego

School Of Law.

6-2

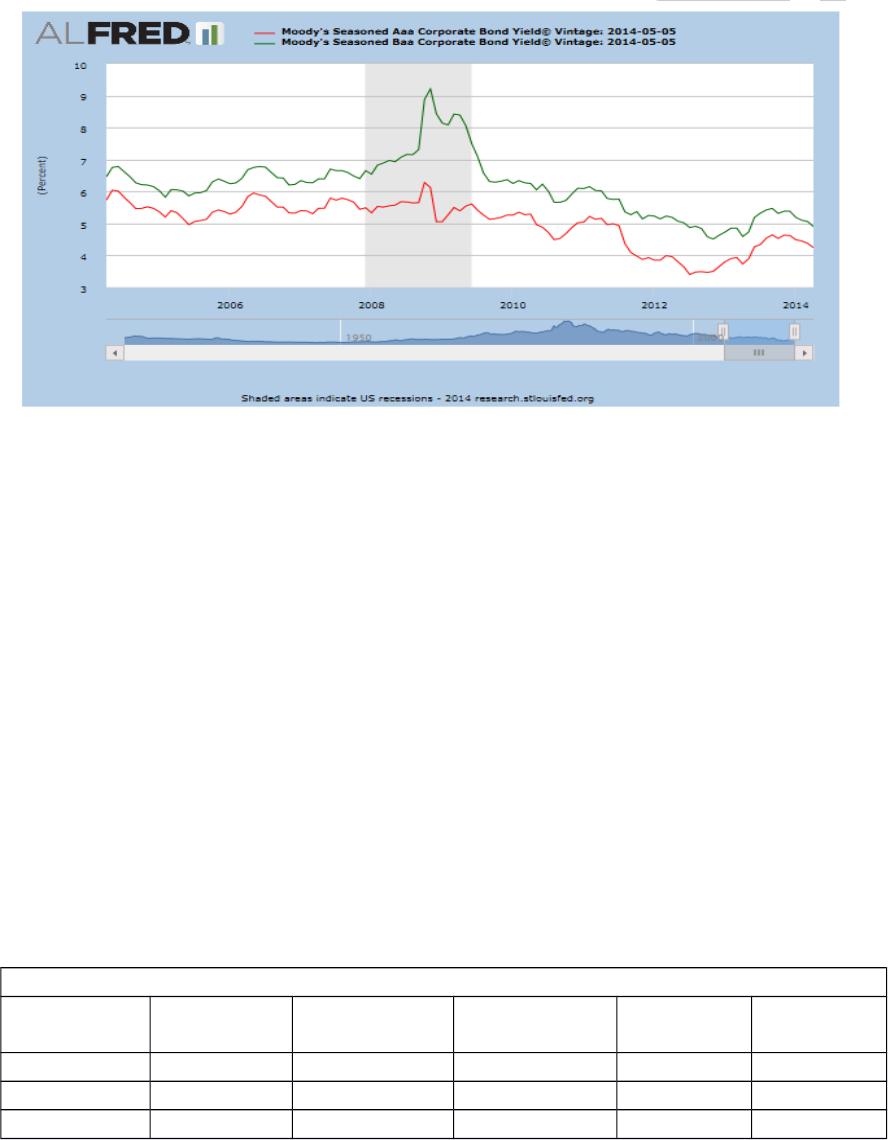

Source: alfred.stlouisfed.org

Chapter 06 – Bond Markets 6th edition

AAA and BAA yield spreads are shown in the graph below. Notice the increase in yield

spreads that occurred during the financial crisis.

Spreads contain more information than just default risk differences. For instance,

interest rate volatility is greater for lower rated bonds and riskier bonds often have

lower liquidity. Spreads will capture these differences whereas ratings only capture

the default risk differences.

Standard and Poors was sued by the U.S. government in 2013 for allegedly providing

optimistically biased ratings of mortgage backed securities. One wonders why S&P

was the only ratings agency sued. Pundits claim it is because only S&P lowered the

U.S. government’s debt rating.

a. Bond Market Indexes

Bond market indexes are published daily in the Wall Street Journal; indexes are available

for the major bond sectors. Table 6-11 in the text highlights the major indexes.

2. Bond Market Participants

Governments and foreign investors hold the bulk of Treasuries (see table below).

Municipal and corporate bonds are predominantly held by business financial institutions

although individuals hold % of municipals.

Bond market participants by type 2013 (See Text Figure 6–11)

Business

Financial

Business

Nonfinancial Governments

Household

s Foreign

Treasuries 21.83% 0.89% 19.07% 10.32% 47.89%

Municipals 52.58% 0.97% 0.28% 44.46% 1.71%

Corporate 59.33% <1% 1.01% 19.19% 20.47%

Percentage holdings of Treasuries by business financial entities doubled between 2007

and 2010 as safe investments were desired and the government increased the issuance of

Treasury debt.

6-3

Chapter 06 – Bond Markets 6th edition

3. Comparison of Bond Market Securities

Yield rates on the three major bond types are presented in Text Figure 6-12. Yield rates

are highly correlated among the three types, but default risk premiums on muni and

corporate bonds can vary over time. As noted default spreads increased dramatically

during the financial crisis.

4. International Aspects of Bond Markets

International bond markets include issues underwritten by multinational syndicates or

bonds issued outside the home country. New issuance in this market grew dramatically

before the financial crisis. From 1995 to 2007 the annual quantity of international debt

securities issued grew from about $254 billion to $3,002 billion before the crisis reduced

new issuance which fell to $705 billion in 2012. Nevertheless the amount of international

bonds and notes outstanding grew from $2,209.3 billion in 1995 to $20,672.3 in March

2013, an overall growth rate of 835.7% over the period.

In terms of currency, there are now more euro denominated floating rate and fixed rate

debt instruments outstanding than dollar denominated instruments.2 International bonds

are usually bearer bonds placed in multiple countries or in a country other than the

issuer’s home country. Financial institutions are the largest issuers of international bonds,

other than equity related bonds which are dominated by corporate issuers.

In 2013 China was holding an estimated $1.32 trillion in U.S. Treasuries. Ask your

students what the effect would be if China sold their Treasury holdings. Is China likely to

do so? Why has China acquired so many Treasuries? The Chinese central bank has

acquired the Treasuries as a result of their attempts to keep the yuan low relative to the

dollar, albeit at the cost of domestic inflation in China.

Adding international bonds to a portfolio can improve diversification as foreign bond

correlations are lower than for domestic securities. However, some countries’ markets

are subject to sudden shifts in capital flows and thus risk is higher for these investments.

In addition currency movements may have major impacts on investment returns.

a. Eurobonds, Foreign Bonds, and Sovereign Bonds

b. Eurobonds

Eurobonds are long-term bonds sold outside the country of the currency in which they

are denominated. This need not be in Europe. For instance Eurodollar bonds may be

dollar denominated bonds sold in Japan. They typically have denominations of $5,000

and $10,000 and are traded mostly OTC in London and Luxembourg. Eurobonds are

typically placed by an investment banking syndicate, traditionally the issue costs have

been higher than for domestic bonds.

2 In equity related bonds and notes the U.S. dollar still dominates.

6-4

Chapter 06 – Bond Markets 6th edition

Eurobond growth was hindered by the Euro/Greek crisis. New issuance fell from $1.5

trillion in 2007 to $947 billion in 2008 and falling all the way to $76 billion in 2012. The

International Swap Dealer’s Association (ISDA) ruled a restructuring of Greek debt a

‘credit event’ because investors were forced to accept a haircut. This resulted in required

payments on credit default swaps and panicked the markets. The ECB eventually

provided a $480 billion bailout. European growth in 2014 is increasing slightly but

deflationary pressures and subpar growth rates remain.

c. Foreign Bonds

Foreign bonds are bonds issued outside the home country and are denominated in the

host country’s currency. For example, Samurai bonds are dollar denominated bonds

issued by Japanese borrowers in the U.S.

d. Sovereign Bonds

Sovereign bonds are government issued debt. Most LDC sovereign debts are issued in a

strong currency such as the dollar or euro rather than in the issuing countries home

currency. Emerging market debt is often not rated investment grade and carries higher

interest rates. In this era of low rates, yields on these bonds can appear attractive,

offering spreads of between 400 and 1500 or more basis points over U.S. Treasuries.

Spreads increased dramatically during the financial crisis, in some cases tripling in a few

weeks. In 2009, Dubai World could not make its interest payment on its debt. In Europe,

Greece, Ireland and Portugal all required bailouts to avoid debt defaults. A private lender

cannot force a government to pay its debts. Argentina has defaulted three times. The

International Monetary Fund and other lending facilities usually assist in bailing out

sovereign debts, usually with certain conditions that the country must meet.

1.1.1.1 VI. Web Links

http://www.publicdebt.treas.gov Bureau of the Public Debt; this site has the current

amount of public debt.

http://www.nyse.com/ An excellent website of the New York Stock

Exchange.

http://www.ft.com/ Financial Times, won two Espy awards for best new

site and best non U.S. news site. Coverage of

global events and markets.

http://www.moodys.com/ A leading provider of independent credit ratings,

research and financial information to the capital

markets

http://www.standardandpoors.com/ A leading provider of independent credit ratings,

research and financial information to the capital

markets

6-5

Chapter 06 – Bond Markets 6th edition

http://www.fitchratings.com/ A leading provider of independent credit ratings,

research and financial information to the capital

markets

1.1.1.1.1.1 http://www.ny.frb.org/ Federal Reserve Bank of New York website, complete

with research, links to the Treasury Direct program

and job opportunities.

1.1.1.1.1.2 VII. Student Learning Activities

1. Go to the web page of the Bond Market Association:

http://www.investinginbonds.com and use their recommendations to ascertain what

percentage of your personal investment portfolio should currently be in bonds.

2. Go to http://www.marketwatch.com/tools/bonds/ and examine the average yield

spreads between the investment grade, high yield and convertible bonds. Explain the

differences you find.

3. Go to the SEC’s website and investigate ‘yield burning’ on municipal bonds. What is

yield burning? Who is concerned about this practice? Why?

4. Read the article, “Financial Contracting Under Extreme Uncertainty: An Analysis of

Brazilian Corporate Debentures,” Anderson, Journal of Financial Economics: 1999.

What additional factors must a bondholder consider in international investing? How

can the additional factors be handled?

5. Why did bond market activity boom immediately after the financial crisis of

2007-2008? How were large firms and small firms affected differently by the crisis?

Explain.

6-6