Chapter 05 – Money Markets 6th Edition

d.Commercial Paper

Commercial paper is a short term unsecured promissory note issued by large,

creditworthy corporations and financial institutions. Because the notes are unsecured and

are not very liquid, commercial paper is rated by ratings agencies. The paper rating

strongly affects the cost of financing with commercial paper. Low quality paper is often

secured by bank lines of credit to obtain a better rating. In normal times the spread

between prime grade and medium grade paper averages about 22 basis points per year.

The maximum maturity is 270 days (most are less) because the SEC requires formal

registration of securities with maturities greater than 270 days. For this reason some of

the paper issued is commonly rolled over at maturity. Commercial paper comprised

about 20% of total money market securities in 2013, down from 26% in 2007, but

starting to recover from the crisis.

Commercial paper is a discount instrument and uses discount quotes similar to T–bills.

The commercial paper market has developed to provide corporations with an alternative

to short term bank loans. Commercial paper outstanding grew tremendously in the 1990s

because large, creditworthy paper issuers were able to obtain lower cost financing by

issuing paper rather than borrowing from banks. Commercial paper is issued in

denominations ranging from $100,000 to $1 million, with the most common maturities in

the 20 to 45 day range. About 22% of issuers directly market their own paper, but the

bulk is sold through brokers and dealers. Brokered paper is more expensive. There is no

active secondary market for commercial paper, partly because commercial paper dealers

will redeem paper from the buyers if the buyer needs the money prior to maturity. In

2007 the market for asset backed commercial paper seized up as lenders refused to roll

over maturing paper that was backed by mortgages. Asset backed commercial paper

(ABCP) is paper backed by assets of the issuing firms. This market grew dramatically

before the crisis, peaking at $2.16 trillion. Many of the assets backing the paper were

mortgage related however and when the crisis began liquidity dried up in the market and

it collapsed. Much of the investment in ABCP came from money market funds, which

were having their own problems and reduced investments in all risky assets including

ABCP. In June 2010 there were just $391 billion of ABCP outstanding even though the

Fed created a Commercial Paper Funding Facility to provide liquidity to borrowers in the

market.

As a result of problems in the paper market spreads between prime grade and medium

grade paper increased from only a few basis points to 160 basis points in 2007 and 395

basis points in 2008 before peaking at an incredible 615 basis points after the Lehman

collapse. Spreads have returned to more normal levels but the market has not yet

recovered its former size.

a. Negotiable Certificates of Deposit

5-1

Chapter 05 – Money Markets 6th Edition

A negotiable certificate of deposit (hereafter CD) is a bearer certificate indicating that a

time deposit has been made at the issuing bank which the bearer can collect at maturity.

Large CDs are negotiable instruments. Negotiable CDs have a minimum denomination

of $100,000, but denominations of $1 million are the most common. Typical maturities

range from 1, 2, 3 and 6 months out to 1 year. Negotiable CD rates are add on rates

(single-payment loans) quoted using the 360 day convention.1 They comprised about

27% of money market securities in 2013; the absolute amount of CDs outstanding fell

from 2007 to 2010 as bank credit deteriorated and has yet to recover. Normally, large

well known banks, particularly New York banks, often can pay lower interest rates on

their CDs than other lesser well known institutions. About 15 dealers make a secondary

market in CDs, although it is not very active. CDs are required to have ‘substantial

interest penalties for early withdrawal.’ The secondary market eliminates the problem of

the interest penalty, and has increased bank’s ability to draw funds that would otherwise

be invested in non-bank money market securities.

b. Banker’s Acceptances (BAs)

Drafts are often used to facilitate international trade in goods and services. The seller of

the goods writes either a time draft or a sight draft payable by the buyer of the goods or

services. A sight draft is a claim that becomes due and payable upon presentation to the

purchaser. A time draft is a claim that becomes due and payable at a certain future date

specified on the draft. Because the seller normally will not know the creditworthiness of

the buyer (and credit investigation costs can be quite high), the seller may be reluctant to

ship the goods unless payment can be guaranteed by a third party. Banker’s acceptances

are a certain kind of time draft where a bank has agreed to pay the seller of the goods the

amount owed if the buyer cannot or will not pay on the date due. The draft is backed by

a letter of credit drawn on the buyer’s bank, ensuring that the bank will “accept” the draft

drawn up by the seller. Once the seller can prove that the goods have been shipped in

accordance with the contract and the proper paperwork has been presented to the buyer,

the time draft can be sold as a discount instrument. The seller of the goods can wait until

maturity to receive payment, or can discount the note to the bank and receive the

discounted face amount immediately. The bank can then hold the acceptance or sell it.

BAs are bearer instruments and are fairly actively traded. Maturities range from 30 to

270 days and BAs are bundled into round lots of $100,000 and $500,000.

The amount of BAs outstanding is quite small compared to the other money market

instruments (less than 1% of the total money market securities outstanding) and has been

steadily declining. Users of BAs are primarily firms involved in export and import and

foreign banks financing non-U.S. international trade.2 Commercial paper

(non-collateralized and asset backed), Euro CP and bank loans compete with BAs. Thus

BAs continue to decline in relative importance due to growth in the asset backed

commercial paper and Euro commercial paper markets and because spreads between

1CDs with maturity greater than one year are not bullet or single payment loans, rather

they usually pay interest semiannually.

2See for instance, LaRoche, R. Bankers Acceptances, Federal Reserve Bank of

Richmond, Economic Quarterly, (79) 1, Winter 1993.

5-2

Chapter 05 – Money Markets 6th Edition

Eurodollar deposits and BAs have fallen. Acceptances actually began declining in 1990

when the Fed removed reserve requirements on non-personal time deposits. As a result

the favorable treatment of BAs, (certain BAs have no reserve requirements) no longer

existed. A schematic of how a BA is created is provided in Appendix 5B available on

Connect.

c. Comparison of Money Market Securities

Most money market securities have high denominations, or high round lots, low default

risk, low interest rates and short maturities. The different instruments have evolved to fill

certain niches or needs. The securities’ secondary markets show more variation. T-bills

are the most actively traded money market security. CDs and BAs are less actively

traded, in part because money market mutual funds and other buyers have been using a

buy and hold strategy for these securities. Commercial paper is usually redeemed by the

seller upon the buyer’s request so no secondary market is needed. Fed funds and repos

tend to be short term so no secondary market has developed for these instruments.

2. Money Market Participants

a. The U.S. Treasury

The Treasury issues T-bills to provide funds throughout the year. The bulk of individual

income tax receipts occur in the spring and corporations and self-employed individuals

generally pay taxes quarterly. Government expenditures however occur throughout the

year and the Treasury uses T-bills to provide financing over the intervening periods when

income is not received.

b. The Federal Reserve

The Fed is a major participant in the money market. The Fed’s open market operations

are conducted using T-bills, T-notes and T-bonds, and Fed policy often involves

repurchase agreements. Moreover, the Fed currently targets the fed funds rate and

actively intervenes in money markets to manipulate this rate.

c. Commercial Banks

Banks both issue and invest in CDs, fed funds, BAs and repos. Banks use the money

markets to manage and minimize their excess reserves position and to meet short term

deficits in reserves.

d. Money Market Mutual Funds

Money market mutual funds (MMMFs) pool investors’ funds and purchase money

market securities. Because most money market securities are high denomination, the

MMMFs allow the small investor to participate in a variety of money market securities

that would otherwise be too expensive for the typical individual. Investors in MMMFs

may earn slightly higher rates than on bank accounts but must forego bank deposit

insurance. Most MMMFs allow limited check writing, low cost investment and free

movement of funds between funds in the same family. There are many different funds

with differing investment strategies. Some are only available for institutional investors

and some are available for individual investors.

5-3

Chapter 05 – Money Markets 6th Edition

e. Brokers and Dealers

Major brokers and dealers include:

The twenty–one government securities dealers who make a market in T-bills assist the

Treasury by purchasing its securities and assist the Fed in implementing open market

operations.

Cantor, Fitzgerald Securities, Garban-Intercapital or ICAP, Liberty, Prebon, and

Hilliard Farber are money and security brokers. They are major players in the

secondary market for government securities and they serve as brokers in the fed funds

market. They do not trade for their own account and maintain anonymity of the

principals in trades they broker.

Thousands of brokers and dealers who link buyers and sellers.

f. Corporations

Non-financial corporations raise large amounts of money in the commercial paper

markets and invest in other money market securities.

g. Other Financial Institutions

Insurance firms, particularly property and casualty insurers, maintain large liquidity

balances. Money market mutual funds invest in these securities and finance companies

must raise large amounts of funds in the commercial paper market because they cannot

accept deposits.

3. International Aspects of Money Markets

Text Table 5-7 indicates the level of foreign investment in U.S. money market securities

by type of instrument. Investments in Treasury securities comprise the largest segment.

Text Figure 5-8 shows money market instruments outstanding in selected

countries/regions for selected instruments. Notice the growing prevalence of the euro as

the currency of denomination. During the financial crisis, foreign investment in money

markets grew only in Treasury investments (recall that Treasuries are a safe haven

investment). U.S. rates were increasingly unfavorable in comparison to foreign interest

rates so investors seeking yield invested elsewhere. In particular the Fed kept the fed

funds rate low while LIBOR jumped and Euro CD rates also rose well above U.S. rates.

a. Euro Money Markets

Eurocurrency deposits are deposits of currency held outside the home country. Hence,

Eurodollar deposits are dollar denominated deposits held outside the United States.3

Eurodollar deposits are not subject to U.S. bank regulations. The Eurodollar market has

evolved as a source of overnight funding for international banks, and plays a role similar

to fed funds loans in the U.S. The rate offered to lend these funds is the London

InterBank Offer Rate (LIBOR).4 The LIBOR rate is closely related to the U.S. fed funds

rate and the two rates appear to be converging more closely in recent years, but LIBOR

tends to be slightly higher because regulatory costs on Eurodollar accounts are lower than

on domestic deposits. LIBOR also tends to be higher because international bank deposits

3In reality, the money may never leave the country, but for accounting purposes the

money is considered ‘offshore.’

5-4

Chapter 05 – Money Markets 6th Edition

are perceived as slightly riskier than U.S. deposits, perhaps in part because the U.S. has

not allowed its large banks to fail. During the crisis LIBOR rose from 2.57% in

September 2008 to an all-time high of 6.88% in September 2009. Because the Fed kept

the fed funds rate low LIBOR and the fed funds rate diverged.

Teaching Tip: Until recently the British Banker’s Association (BBA) published daily

estimates of LIBOR based on loan rate data supplied by participating banks. In early

2008 some banks indicated to the BBA a concern that the reported LIBOR did not truly

represent bank borrowing costs. LIBOR had increased sharply with the credit crunch;

nevertheless, some banks apparently felt that others were underreporting true borrowing

costs, fearing that higher LIBOR would indicate a potential problem obtaining funding.

This eventually blew up into the LIBOR manipulation scandal as it was revealed that

banks manipulated LIBOR to profit on derivatives positions and/or to appear less risky

during the crisis. Bank profits from misquoting LIBOR may have exceeded $75 billion.

Details of how this was accomplished may be found in the Wall Street Journal Online

article of 5/2/13: Clubby London Trading Scene Fostered Libor Rate-Fixing Scandal

http://online.wsj.com/article/SB10001424127887323296504578396670651342096.html?

mod=WSJ_hp_LEFTWhatsNewsCollection.

UBS was fined $1.52 billion, RBS $612 million and Barclays $450 million. J. P. Morgan

and Deutsche-Bank are now facing fines from European Union regulators. As a result of

the scandal the BBA is no longer allowed to publish LIBOR. ICE now publishes LIBOR.

LIBOR is available in various maturities for the following currencies: USD, CHF (Swiss

franc), GBP, JPY, CAD, Euro, AUD, DKK (Danish krone), NZD, and the SEK (Swedish

krona). More disturbingly, The Federal Reserve Bank of New York and the Bank of

England may have known of the manipulation as early as 2007 and a trader alleges that

manipulation has occurred since 1991. This is one more instance of the need to

emphasize ethics in business. LIBOR is the base rate on literally trillions of dollars of

derivatives. LIBOR also is the base rate for many loans, including adjustable rate loans.

Some of the major euro securities include:

Eurodollar CDs: Dollar denominated deposits held outside the U.S. The maturity is

typically less than one year. Rates on Eurodollar CDs are sometimes higher than

domestic CD rates because of the lack of explicit deposit insurance and lower

regulatory costs.

4The rate at which a bank will pay to obtain these funds is called, not surprisingly,

LIBID. According to the text the spread between LIBOR and LIBID is narrow, usually

no more than 12.5 basis points.

5-5

Chapter 05 – Money Markets 6th Edition

Eurocommercial paper issued by commercial paper dealers: Technically, the term

means commercial paper issued outside the borrower’s country of origin, but in their

home currency. The term is coming to mean securities issued in Europe without

involving a bank.

With the introduction of the euro currency net issuance of international debt denominated

in euros has grown rapidly. It is likely that money markets denominated in euros will

continue to grow in importance.

Euro money markets were strongly affected by the 2013 debt crisis in Cypress. Short

term euro market activity declined rapidly as fears of contagion spread. The European

Central Bank was forced to lend over $1 trillion to prevent a banking crisis in the EU. As

a result Euro commercial paper rates climbed significantly above U.S. commercial paper

rates and dollar denominated paper was substituted for euro commercial paper.

Appendix 5A: Single versus Discriminating Price Auctions (available in Connect or

from your McGraw-Hill representative)

In the Treasury single price auction the lowest bid price accepted becomes the price that

all winning bidders pay. There are two purported advantages of a single price auction

over a discriminating auction:

1. A greater number of bidders have their bids filled and

2. More aggressive bidding occurs under the single price format resulting in a higher

average price paid by investors.

5-6

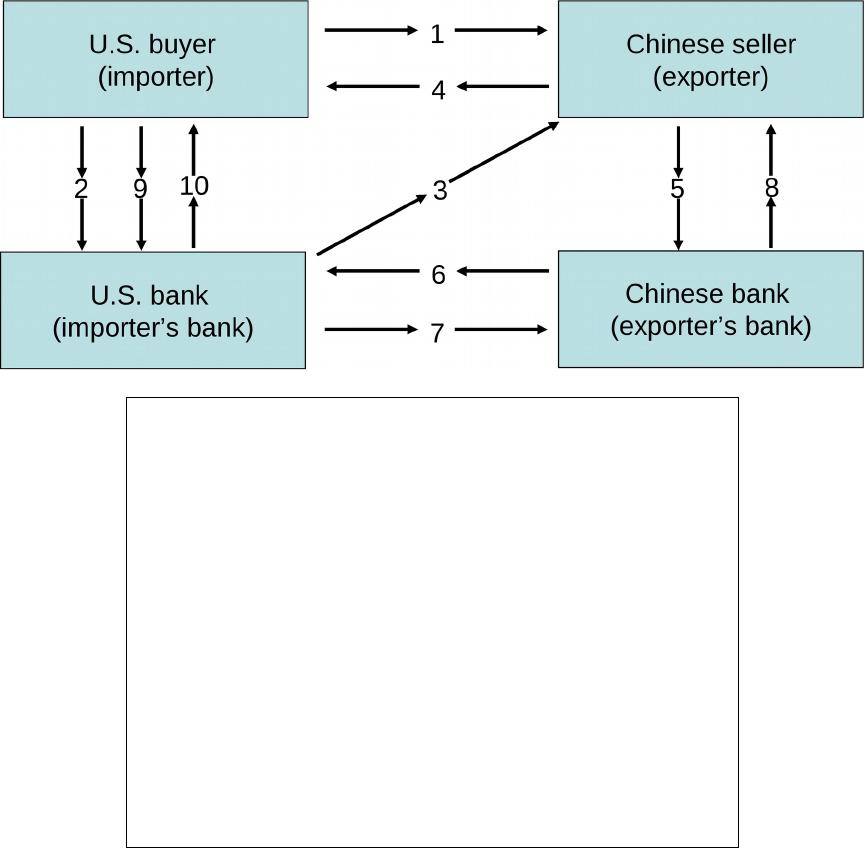

Purchase order sent by U.S. buyer to Chinese seller

Chinese seller requests a leer of credit

Nocaon of leer of credit and dra authorizaon

Order shipped

Time dra and shipping papers sent to Chinese seller’s bank

Time dra and shipping papers sent to U.S. bank; banker’s

acceptance created

Payments sent to foreign bank (immediately if Chinese

seller wishes to discount the dra and collect immediately,

at maturity if not)

Payments sent to Chinese seller (see #7)

Payment to U.S. bank by U.S. buyer at maturity, paid in full

Shipping papers delivered

Chapter 05 – Money Markets 6th Edition

Appendix 5B: Creation of a Banker’s Acceptance ((available in Connect or from

your McGraw-Hill representative)

A schematic of the creation of a Banker’s Acceptance (BA) with a brief explanation is

provided at the website. A slightly modified copy is reproduced below:

5-7

Chapter 05 – Money Markets 6th Edition

1.1.1.1 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal

Reserve

http://www.americanbanker.com/ American Banker’s Association Website

http://www.ustreas.gov/ Website of the U.S. Treasury.

http://www.ft.com/ Financial Times, won two Espy awards for best new

site and best non U.S. news site. Coverage of

global events and markets.

http://www.moodys.com/ A leading provider of independent credit ratings,

research and financial information to the capital

markets.

http://www.standardandpoors.com/ A leading provider of independent credit ratings,

research and financial information to the capital

markets, although little of the information is free.

1.1.1.1.1.1 http://www.ny.frb.org/ Federal Reserve Bank of New York website, complete

with research, links to the Treasury Direct program

and job opportunities.

http://www.bloomberg.com/ The website provides current market data on many

instruments, including stocks, bonds and money

market securities.

1.1.1.1.1.2 VII. Student Learning Activities

1. Go to the Treasury Direct webpage:

http://www.treasurydirect.gov/indiv/myaccount/myaccount.htm and read about the

Treasury Direct program. What is the program for and how can it benefit investors?

Describe the three ways that individuals can buy Treasury securities. Which one is

being phased out? What are the advantages and disadvantages of each?

2. Compare current rates on fed funds loans, T-bills, commercial paper and banker’s

acceptances. Are the rates similar? Why do they differ? Calculate the effective

annual rates for each type instrument. Keep the terms as similar as possible.

5-8

Chapter 05 – Money Markets 6th Edition

3. Using the Web, find the highest three or four negotiable CD rates in the country

offered by banks for a one year maturity. (Hint: The Wall Street Journal or BankRate

websites can help.) Why do the rates differ? Should an investor automatically

choose the highest rate? Why or why not?

4. You are the Assistant Treasurer for ABC Corporation. Your firm has $10 million in

excess cash it does not plan on needing for the next three months. These funds

however do include some contingency funds that are kept if unexpected funds needs

arise. Your boss has asked you to recommend a money market investment for the

firm. Prepare a two page memo to your boss explaining the different types of money

market investments available and the pros and cons of investing in each.

5-9