1.1.1.1.1Part Two

1.1.1.1.1.1.1.1 Securities Markets

1.1.1.1.2Chapter Five

Money Markets

1.1.1.2 I. Chapter Outline

1. Definition of Money Markets: Chapter Overview

2. Money Markets

3. Yields on Money Market Securities

a. Bond Equivalent Yields

b. Equivalent Annual Return

c. Discount Yields

d. Single-Payment Yields

4. Money Market Securities

a. Treasury Bills

b. Federal Funds

c. Repurchase Agreements

d. Commercial Paper

e. Negotiable Certificates of Deposit

f. Banker’s Acceptances

g. Comparison of Money Market Securities

5. Money Market Participants

a. The U.S. Treasury

b. The Federal Reserve

c. Commercial Banks

d. Money Market Mutual Funds

e. Brokers and Dealers

f. Corporations

g. Other Financial Institutions

6. International Aspects of Money Markets

a. Euro Money Markets

Appendix 5A: Single versus Discriminating Price Auctions (available on Connect or from your

McGraw-Hill representative)

Appendix 5B: Creation of a Banker’s Acceptance (available on Connect or from your

McGraw-Hill representative)

1.1.1.3 II. Learning Goals

1. Define money markets.

2. Identify the major types of money market securities.

3. Examine the process used to issue Treasury securities.

4. List the main participants in money markets.

5. Examine the extent to which foreign investors participate in U.S. money markets.

6. Understand the major developments in Euro money markets.

1.1.1.4

1.1.1.5 III. Chapter in Perspective

This is the first of six chapters that cover different securities markets. Most students will have

some familiarity with stock and bond markets (Chapters 9 and 6), but little knowledge of money

markets (Chapter 5), mortgage markets (Chapter 7), foreign exchange markets (Chapter 8) and

markets for derivatives (Chapter 10). Chapter 5 initially covers the purpose and major features

of the money markets. Next, the characteristics of the major money market securities and their

primary and secondary markets are presented. The pricing conventions of money market

securities are reviewed, along with the predominant participants and their use of these markets.

The chapter concludes with a discussion of international money markets with a particular focus

on the Euro money markets.

1.1.1.6 IV. Key Concepts and Definitions to Communicate to Students

Money markets Negotiable CD

Bond equivalent yield Discount yield

Single payment yield Money market mutual funds

Opportunity cost Liquidity

Treasury Bills Bearer instrument

Default risk free Banker’s acceptance

Federal funds Eurodollar deposits

Correspondent banks LIBOR

Repo and reverse repurchase agreement Euronotes

Commercial paper Eurocommercial paper

Asset backed commercial paper

1.1.1.7 V. Teaching Notes

1. Definition of Money Markets: Chapter Overview

Money market securities are generally fixed income securities that have an original issue

maturity of one year or less, thus they have little price risk. Money markets primarily exist to

minimize the cost of maintaining liquidity for financial, non-financial and government

institutions and to provide borrowers with low cost, short term sources of funds. Money market

securities should thus provide safety of principal, liquidity and a predictable, albeit typically

modest, yield. Nevertheless, the money markets were rocked by the financial crisis. The

commercial paper market froze up, declining in value from $1.7 trillion to $1.6479 trillion (a

drop of $52.1 billion or 3%) in less than one week in September 2008. A money market mutual

fund, Primary Fund, one of the original money funds, ‘broke the buck’ when its net asset value

fell below $1 as announced on September 17, 2008 due to losses on its Lehman holdings. Fund

asset holdings immediately fell from $62.6 billion to $40 billion. The size and speed of

withdrawals forced the fund to withhold redemptions for seven days after request.1,2 The Fed

guaranteed all money market funds to prevent further fund withdrawals.

As bank lending also seized up the Fed expanded currency swap lines with the ECB and the

Swiss central bank to give European banks access to dollars since traditional sources of dollar

loans dried up.

2. Money Markets

Money markets exist because rarely do required cash disbursements occur at the same time and

in the same amounts as cash inflows for corporations and institutions. At times units will have

excess cash that is not immediately needed, and other economic units will need to borrow cash

for a short period of time. In addition, precautionary amounts of funds beyond planned liquidity

needs must be maintained because expected cash inflows and required cash disbursements

cannot be predicted with perfect accuracy. The opportunity cost of keeping cash on hand can be

quite high. The opportunity cost is the rate of return that could be earned in the highest valued

alternative if liquidity balances did not have to be maintained. Money markets have developed

to provide corporations, governments and institutions with safe, liquid investments (or sources of

funds for borrowers) that minimize the opportunity cost of maintaining liquidity.

Money market securities also have little or no default risk. With the focus on liquidity and

safety, the rate of return on money market securities is expected to be significantly less than

promised yields on capital market instruments.

1 www.marketwatch.com: FundWatch, Sept. 17, 2008, 9:11 a.m. Money market breaks the buck, freezes redemptions Reserve Primary Fund stung by Lehman

collapse, investor withdrawals, Sam Mamudi and Jonathan Burton

2 This was only the second money fund to ever break the buck. In 1994, Community Bankers

U.S. Government Money Market net asset value fell to 96 cents due to derivatives losses.

3. Yields on Money Market Securities

a. Bond Equivalent Yields

b. Equivalent Annual Return

c. Discount Yields

d. Single-Payment Yields

Many money market securities use special quoting conventions. Discount rates (or discount

yields) quote the interest rate as an annualized percentage of the sale (redemption) price of the

security assuming there are only 360 days in a year. Even if the security matures in 90 days for

example, the rate quote is as if the security matured in one year. Single payment securities or

loans (also called add ons) quote the rate as an annualized percentage of the purchase price of

the security, assuming there are only 360 days in a year. The two are not directly comparable.

For instance, one cannot directly compare the rate on a 60 day $10,000 CD (add on) quoted at

6% interest and a 180 day $10,000 T-bill (discount) quoted at 5.9%. One can calculate the initial

price (P0) and face value (Pf) of the two instruments and then calculate a bond equivalent yield

for each in order to see which pays the higher rate.

Single payment (add ons) Pf = P0 (1 + (an/360)) a = add on rate, n = days to maturity

Discount instruments P0 = Pf (1 – (dn /360)) where d = discount, n = days to maturity

For the CD: P0 = $10,000; Pf = $10,000 (1+(0.0660/360)) = $10,100

The bond equivalent yield for the CD is ($10,100/$10,000) –1) (365/60) = 6.08%

For the T-bill: Pf = $10,000; P0 = $10,000 (1 – (0.059180/360) = $9,705

The bond equivalent yield for the T-bill is ($10,000/$9,705) –1) (365/180) = 6.16%

The T-bill pays the higher bond equivalent yield or APR.

If the securities have equivalent maturities the two quotes can be directly compared using the

following:

a = d / (1 – (dn/360))

d = a / (1 + (an/360))

Bond equivalent yield BE = a (365/360)

The equivalent annual rate or EAR is the annual rate of return with annual compounding. The

EAR may be found two ways:

EAR = (Pf / P0)365/ n –1 or

EAR = (1 + (BEY / m))m – 1 ; where m = 365/n

A complete discussion of money market rates can be found in Stigum, M. The Money Market, 3rd

ed. Homewood, Ill.: Dow-Jones Irwin 1990.

4. Money Market Securities

The total amount of money market securities outstanding in 2007 in the major money markets

was about $8 trillion and in 2013 was about $5.1 trillion. The decline occurred due to the

financial crisis and the very low interest rates that have prevailed since. Real yields on many

money market securities have been negative over the period as can be seen by comparing the

rates with inflation in the table below. Market rates as of May 2014 are as shown below. Updates

may be easily obtained from the Wall Street Journal Online, Money Rates section. Rates are for

maturities of 3 months except as noted.

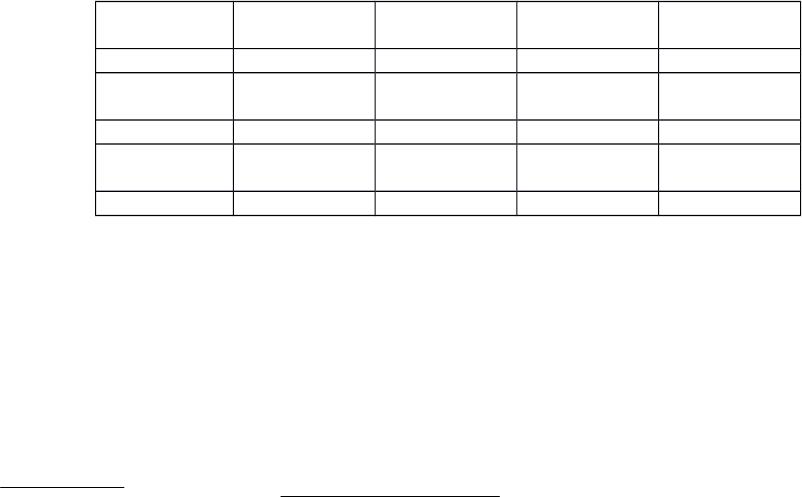

Instrument

Federal

Funds*

Commercial

Paper Jumbo CDs+ Euro CP

Rate 0.10% 0.11% 0.10% 0.23%

Instrument LIBOR

Banker’s

Acceptances Euro$ Repo*

Rate 0.2274% 0.23% 0.15% 0.14%

Instrument Treasury

Bills** Inflation***

Rate 0.030 2.0%

Data from Wall Street Journal Online Money Rates Section May 2014

* Overnight; +MMA, Savings and CD rates section of the WSJ, ** 13 week, *** Year over year,

all items as measured by the CPI

Teaching Tip:

Ask students to find the real after-tax rate of return on a CD. Using the 0.10% CD rate and the

2.0% inflation rate above and assuming the investor is in a 21% federal plus state tax bracket the

real after-tax rate of return is -1.88% as shown below:

The repo rate is typically lower than the Fed funds rate because repos are collateralized loans.

The commercial paper rate is lower than the banker’s acceptance rate. This is likely because

bank default risk is higher than many commercial paper issuers.

The table below provides outstanding dollar and percentage amounts of some of the major

money market investments.

0188.01

0200.1

)]21.01(0010.0[1

real

TnomA r1

inflation1

r1

Money market securities outstanding in 1990, 2004, 2007, 2010 and 2013

Billions $

Instrument 1990 2004 2007 2010 2013

Treasury Bills $ 527 $ 982 $1,010 $1,856 $1,607

Fed funds & Repos 372 1,585 2,731 1,656 1,097

Commercial Paper 538 1,310 2,109 1.083 1,001

Negotiable CDs 547 1,379 2,149 1,822 1,491

Banker’s Acceptances 52 4 1 1 0

Total $2,036 $5,260 $8,000 $6,418 $5,196

% of Total in Given Year

Instrument 1990 2004 2007 2010 2013

Treasury Bills 26% 19% 13% 29% 31%

Fed funds & Repos 18% 30% 34% 26% 21%

Commercial Paper 26% 25% 26% 17% 19%

Negotiable CDs 27% 26% 27% 28% 29%

Banker’s Acceptances 3% 0.1% 0.0% 0.0% 0%

100% 100% 100% 100% 100%

Source: Text

The increase in Treasury Bills is due to increased government borrowing during and after the

financial crisis. The decline in Fed funds and repos coincides with the growth of excess reserves

held by banks and a decline in unsecured lending during the crisis. Many banks borrowed at the

Federal Reserve’s discount window for funding needs during the crisis. Commercial paper

amounts declined with the financial crisis due to default risk concerns (as did the quantity of

negotiable CDs), weaker borrowing demand and lower long term funding costs.

a. Treasury Bills

T-bills are short term obligations of the U.S. government used to finance government spending

needs. In 2013 there was $1,607 billion outstanding comprising about 31% of total money

market securities. Original issue maturities are 4, 13, 26 or 52 weeks. The minimum

denomination is $100 but a round lot is $5 million. T-bills are thought to be free of default risk

and the T-Bill rate is often used as a measure of the short term ‘risk free rate.’ Each week new 13

and 26 week T-bills are offered for sale at competitive auction. T-bills are sold to the highest

bidder at auction, but no one bidder can purchase more than 35% of the total amount in any one

auction. Noncompetitive bids of up to $5 million can be made. The Treasury is using a single

price auction to determine the price all bidders pay.

Treasury securities used to be sold at a discriminating auction where high bidders paid higher

prices, and lower bidders paid lower prices. At that time noncompetitive bidders paid the average

price of the accepted bids. The text appendix discusses reasons for the change in bid process.

Today, competitive bidders submit a discount bid quote and the Treasury determines the price by

calculating the funds needed less the amount of noncompetitive bids and then chooses the ‘stop

out yield’ which is the maximum bid yield accepted.

In the event of an oversubscription, competitive bidders who bid lower yields receive their full

bid amount and bidders at the stop out yield receive a prorated amount of their quantity desired.

Noncompetitive bidders’ demand is met in full. All successful bidders pay the price associated

with the stop out yield.3

The secondary market for T-bills is the largest of any money market security. There are 21

primary government security dealers who purchase the new issues and about 500 smaller dealers

who actively participate in trading T-bills. The FedWire is often used for trades between dealers

and other institutions.

Teaching Tip: In violation of regulations, Salomon Brothers, bought about 80% of one Treasury

auction in an attempt to squeeze the market. Many T-bills are sold on a ‘when issued’ basis by

dealers who anticipate obtaining them at auction (i.e. T-bills are often sold short before they are

issued). Since Salomon obtained so much of the auction, other dealers could not meet their prior

short sale obligations and had to pay a premium price to Salomon to obtain the bills which the

dealers had already agreed to deliver to customers. The government forced Salomon to give up

their profits from the squeeze and pay fines. The biggest loss was to Salomon’s reputation and

they were eventually bought out.

T-bills are discount instruments. T-bill prices (P0) are calculated as P0 = PF (1 – (iT-billd*n/360))

where iT-billd is the discount quote, n is the maturity in days and PF is the face value of the bill.

One should calculate the bond equivalent yield in order to compare rate quotes on different

instruments that use different quoting conventions. The bond equivalent yield for a T–bill can be

calculated as (PF–P0)/P0 * (365/n).

During the financial crisis, not only did the supply of T-bills increase, but demand for Treasuries

as a safe haven investment soared. Demand increased so much that for the first time ever, yields

on 3 month bills fell below zero. In essence, investors paid the U.S. government to take their

money.

b. Federal Funds

Fed funds, together with repurchase agreements, comprise about 26% of total money market

securities. Federal funds, or fed funds, are short term unsecured loans of deposits held at the

Federal Reserve (i.e. loans of excess reserves, see Chapter 4). These loans occur largely between

institutions. Small banks often make loans to their correspondent banks when local loan

demand is insufficient. The majority of fed funds are overnight loans, although many are made

on ‘continuing contract.’4

3 In the unlikely event that noncompetitive bids are sufficiently large to meet all the funding

needs of the current auction the Treasury will allocate the entire issue to these bidders at a zero

discount and they will have to pay face value.

4Continuing contract (not in text) means that unless the borrower or lender notifies the other

party the loan will automatically be renewed daily.

Fed funds are add on loan contracts (single payment or ‘bullet’ loans) and follow the convention

of quoting all rates on an annual basis assuming a 360 day year. To convert a fed funds rate

quote to a bond equivalent yield take the rate quote and multiplied it by 365/360. Many fed fund

loans are arranged through correspondent banks or through brokers such as Garban-Intercapital

Ltd. (now named ICAP) and Prebon. The typical brokerage fee may be as small as 50 cents per

million dollars.

Funds transfers occur over the FedWire and transactions can be completed very quickly (in a

matter of minutes). A FI is not required to hold reserves at the Fed to participate in the fed funds

market; deposits at banks are often used in place of deposits at the Federal Reserve. Typical

transactions are $5 million and up.

c. Repurchase Agreements

A repurchase agreement (repo or RP) is an agreement where the seller of securities agrees to

repurchase the securities at a preset price at a preset time (typically from 1 to 14 days). Repos

are in effect, collateralized loans akin to fed funds loans. The seller is borrowing money and

pledging the securities as collateral and the buyer (who is said to be engaging in a reverse repo)

is lending money. The interest rate is determined by setting the buy and sell price of the

securities. The rate of interest paid on the repo is not a function of the rate of return on the

underlying securities. If risky securities are pledged as collateral, the fund’s lender may require a

larger ‘haircut,’ i.e. repos normally have to be slightly overcollateralized. For instance, to

borrow $100 the repo seller would have to sell securities currently worth $102, for a $2 haircut.

The repo is a ‘real’ sale in the sense that title to the securities passes to the lender of funds for the

term of the agreement. Transfers may occur over the FedWire system. Typical denominations

on repos of one week or less are $25 million and longer term repos usually have $10 million

denominations. Repos are add on instruments (single payment loans) with yields that average

about 25 basis points less than fed funds loans due to the repo collateral. Repos take longer to

arrange than fed funds, and fed funds loans are more likely to be used when funds are needed

immediately.

Bank of America (BOA) used repos to hide about $10.7 billion of debt from the public from

2007 to 2009. Under accounting rules if the value of the securities pledged on the repo are worth

105% of the cash received the borrowing firm (BOA) can book the transaction as an asset sale

rather than as a loan. So for the term of the repo the borrower can report lower leverage ratios

(i.e., it will have a higher equity to asset ratio). If these transactions occur a few days before a

financial report date such as the end of a quarter, the firm can appear to be safer than it actually

is. The strategy is called a ‘Repo 105’ strategy because of the 105% collateral requirement. It is

actually not allowed under U.S. law, but may be allowed for European subsidiaries under British

laws. Lehman Brothers used a similar strategy to hide debt amounts of between $8 billion and

$15 billion in 2007 and 2008.5

5 Merced, M and J. Werdigier. The Origins of Lehman’s ‘Repo 105.’ Investment Banking, NY

Times Dealbook, March 12, 2010.

Teaching Tip: The repo market was at the center of the credit crunch during early 2008. Wall

Street firms finance much of their security holdings with short term repos. As the subprime

mortgage problems began to spread lenders required greater haircuts to lend. Haircuts of $2 per

hundred on safe mortgages rose to $5 in February 2008 and haircuts on so called ‘Alt-A’ loans,

which are loans between prime and subprime credit, haircuts became as high as $30 per hundred.

Some lenders refused to engage in repo loans except with the safest collateral. Inability to roll

over their repo financing of their extensive mortgage holdings was one factor that led to the

collapse of Bear Stearns.6 Problems in the repo and commercial paper markets (see below) led to

the Fed’s actions in assisting in the bailout of Bear Stearns and opening up the Discount Window

to non-banks for the first time.7

6 Data from “Another Source of Quick Cash Dries Up, Firms Rethink Reliance on ‘Repo’

Financing as Conditions Tighten,” by Serena Ng and Randall Smith, The Wall Street Journal

Online, March 17, 2008, Page C1.

7 “Fed Offers Lifeline for Spurned Debt: New Tack on Bonds Tied to Mortgages Sends Dow Up

3.6%,” by Greg Ip, The Wall Street Journal Online, March 12, 2008, Page A1.