Answers to Chapter 4

Questions:

1. As part of the Federal Reserve System, Federal Reserve Banks perform multiple functions. These include

assistance in the conduct of monetary policy, supervision and regulation of member banks and other large financial

institutions, consumer protection, and the provision of services, such as new currency issue, check clearing, wire

transfer services, and research services to either the federal government or member banks. We summarize each

function as follows.

Assistance in the Conduct of Monetary Policy: Federal Reserve Bank (FRB) presidents serve on the Federal

Open Market Committee (FOMC). FRBs set and change discount rates.

2. The discount rate (the interest rate on “lender of last resort” loans made by Federal Reserve Banks to depository

3. The Federal Reserve System is divided into 12 Federal Reserve districts as shown in Figure 4-1. Each district has

one main Federal Reserve Bank, some of which also have branches in other cities within the district. In terms of

total assets, the three largest Federal Reserve Banks are the New York, Chicago, and San Francisco banks. Together

Federal Reserve Banks operate under the general supervision of the Board of Governors of the Federal

Reserve based in Washington D.C. Each Federal Reserve Bank has its own nine-member Board of Directors that

4. The primary responsibilities of the Federal Reserve Board are the formulation and conduct of monetary policy

and the supervision and regulation of banks. All seven Board members sit on the Federal Open Market Committee

which makes key decisions affecting the availability of money and credit in the economy. The Federal Reserve

Board also has primary responsibility for the supervision and regulation of i) all bank holding companies (their

holding companies. The Board is also responsible for the development and administration of regulations governing

the fair provision of consumer credit (e.g., the Truth in Lending Act, the Equal Credit Opportunity Act, etc.).

5. The main responsibilities of the FOMC are to formulate policies to promote full employment, economic growth,

price stability, and a sustainable pattern of international trade. The FOMC seeks to accomplish this by setting

guidelines regarding open market operations. Open market operations−the purchase and sale of U.S. government

6. The major liabilities on the Fed’s balance sheet are currency in circulation and reserves (depository institution

reserve balances in accounts at Federal Reserve Banks plus vault cash on hand of commercial banks). Their sum is

Reserve Deposits. The largest liability on the Federal Reserve’s balance sheet is depository institution reserves. All

depository institutions hold reserve accounts at their local Federal Reserve Bank. These reserve holdings are used to

Currency Outside Banks. The second largest liability, in terms of percent of total liabilities and equity, of the

Federal Reserve System is notes (bills) in circulation. At the top of each Federal Reserve note ($1 bill, $5 bill, $10

7. In the fall of 2008, the Federal Reserve implemented several measures to provide liquidity to financial markets

that had frozen up as a result of the financial crisis. The liquidity facilities introduced by the Federal Reserve in

response to the crisis created a large quantity of excess reserves at DIs. For example, in October 2008 the Federal

Reserve began paying interest on excess reserves, for the first time. Further, during the financial crisis, the Fed set

Some observers claim that the large increase in excess reserves implied that many of the policies introduced

by the Federal Reserve in response to the financial crisis were ineffective. Rather than promoting the flow of credit

to firms and households, it was argued that the increase in excess reserves indicated that the money lent to banks and

other FIs by the Federal Reserve in late 2008 and 2009 was simply sitting idle in banks’ reserve accounts. Many

8. The major assets on the Federal Reserve’s balance sheet are Treasury securities, Treasury currency, and gold and

foreign exchange. While interbank loans (loans to domestic banks) are quite a small portion of the Federal Reserve’s

assets, they play an important role in implementing monetary policy.

U.S. Government Agency Securities. U.S. government agency securities are the second largest asset account on

the Fed’s balance sheet in 2013 (35.2 percent of total assets). However, in 2007, this account was 0.0 percent of total

Gold and Foreign Exchange and Treasury Currency. The Federal Reserve holds Treasury gold certificates that are

Interbank Loans. As mentioned earlier, in a liquidity emergency depository institutions in need of additional funds

Miscellaneous assets. Generally, miscellaneous assets are a small portion of the Fed’s total assets (e.g., 6.8 percent

in 2013). However, during the financial crisis, the Fed undertook a number of measures to support various sectors of

9. This account grew as the Fed took steps to improve credit market liquidity and support the mortgage and housing

markets during the financial crisis by buying mortgage-backed securities backed by Fannie Mae, Freddie Mac, and

10. The tools used by the Federal Reserve to implement its monetary policy include open market operations, the

discount rate, and reserve requirements. Open market operations are the Federal Reserves’ purchases or sales of

11. Changing the discount rate signals to the market and the economy that the Federal Reserve would like to see

higher or lower rates in the economy. Thus, the discount rate is like a signal of the FOMC’s intention regarding the

12. For two reasons, the Federal Reserve rarely uses the discount rate as a monetary policy tool. First, it is difficult

13. Historically, discount window lending was limited only to depository institutions (DIs) with severe liquidity

needs. The discount window rate, which was set below the fed funds rate, was charged on loans to depository

generally sound financial condition that cannot obtain temporary funds in the financial markets at reasonable terms.

Secondary credit is available to depository institutions that are not eligible for primary credit. It is extended on a

very short-term basis, typically overnight, at a rate that is above the primary credit rate. Secondary credit is available

to meet backup liquidity needs when its use is consistent with a timely return to a reliance on market sources of

With the change, discount window loans to healthy banks would be priced at 1 percent above the fed funds

rate rather than below as it generally was in the period preceding January 2003. Loans to troubled banks would cost

1.5 percent above the fed funds rate. The changes were not intended to change the Fed’s use of the discount window

The Fed took additional unprecedented steps, expanding the usual function of the discount window, to

address the financial crisis. While the discount window had traditionally been available only to DIs, in the spring of

2008 (as Bears Stearns nearly failed) investment banks gained access to the discount window through the Primary

During the financial crisis, the Fed also significantly reduced the spread (premium) between the discount

rate and the federal funds target to just a quarter of a point, bringing the discount rate down to a half percent. With

lower rates at the Fed’s discount window and inter-bank liquidity scarce as many lenders cut back their lending,

14. The Federal Reserve uses mainly open market operations to implement its monetary policy. As mentioned in

question 12, adjustments to the discount rate are rarely used because it is difficult for the Fed to predict changes in

reserves held by banks and the willingness of the public to redeposit funds at banks instead of holding cash (i.e.,

they have a preferred cash-deposit ratio)), the reserve requirement is rarely used by the Federal Reserve as a

15. Expansionary Activities: The chapter discusses three monetary policy tools that the Fed can use to increase the

money supply. These include open market purchases of securities, discount rate decreases, and reserve requirement

that interest rates fall and security prices to rise. In the third case (a discount rate change), the impact of a lowering

of interest rates is more direct. Lower interest rates encourage borrowing. Economic agents spend more when they

can get cheaper funds. Households, business, and governments are more likely to invest in fixed assets (e.g.,

cheaper compared to foreign goods. Eventually, U.S. exports increase. The increase in spending from all of these

market participants results in economic expansion, stimulates additional real production, and may cause inflation to

Contractionary Activities: To decrease the money supply the Fed can undertake open market sales, discount rate

increases, and reserve requirement increases. All else constant, when the Federal Reserve sells securities in the open

market, reserve accounts of banks (and the money base) decrease. When the Fed raises the discount rate, interest

relative to foreign rates may result in an increase in the (foreign) exchange value (rate) of the dollar. As the dollar’s

exchange rate increases, U.S. goods become relatively expensive compared to foreign goods. Eventually, U.S.

16. The programs can be categorized into four general areas: expansion of retail deposit insurance, capital

injections, debt guarantees, and asset purchases/guarantees.

Expansion of retail deposit insurance. Increased retail bank deposit insurance coverage was widely used during

Capital Injections. Direct injections of capital by central governments were the main mechanism used to directly

Countries varied in the capital instruments used and the conditions of capital injections. Some countries

(e.g., the U.S.) also imposed restrictions on executive compensation and/or dividend payments to common

stockholders. As seen in Table 4-9, countries also varied in the amounts of capital injected into the banking system.

allowed banks to maintain access to reasonably priced, medium-term funding. They also reduced liquidity risk and

lowered overall borrowing costs for banks.

Countries varied in the range of liabilities covered and fee structures associated with these programs, e.g.,

Asset purchases or guarantees. Asset purchase programs removed distressed assets from bank balance sheets.

Thus, bank liquidity was improved and capital relief was provided (particularly if purchase prices were higher than

amounted to a covert recapitalization of the bank. Further, there was a debate regarding the range of eligible assets.

To have a significant and immediate impact on market confidence, the programs would have to cover all distressed

assets, which would require large programs. As seen in Table 4-9, the U.K. used asset guarantees extensively

(commitments amounted to 33.4 percent of the country’s GDP). Beyond this, Germany committed an unspecified

Problems:

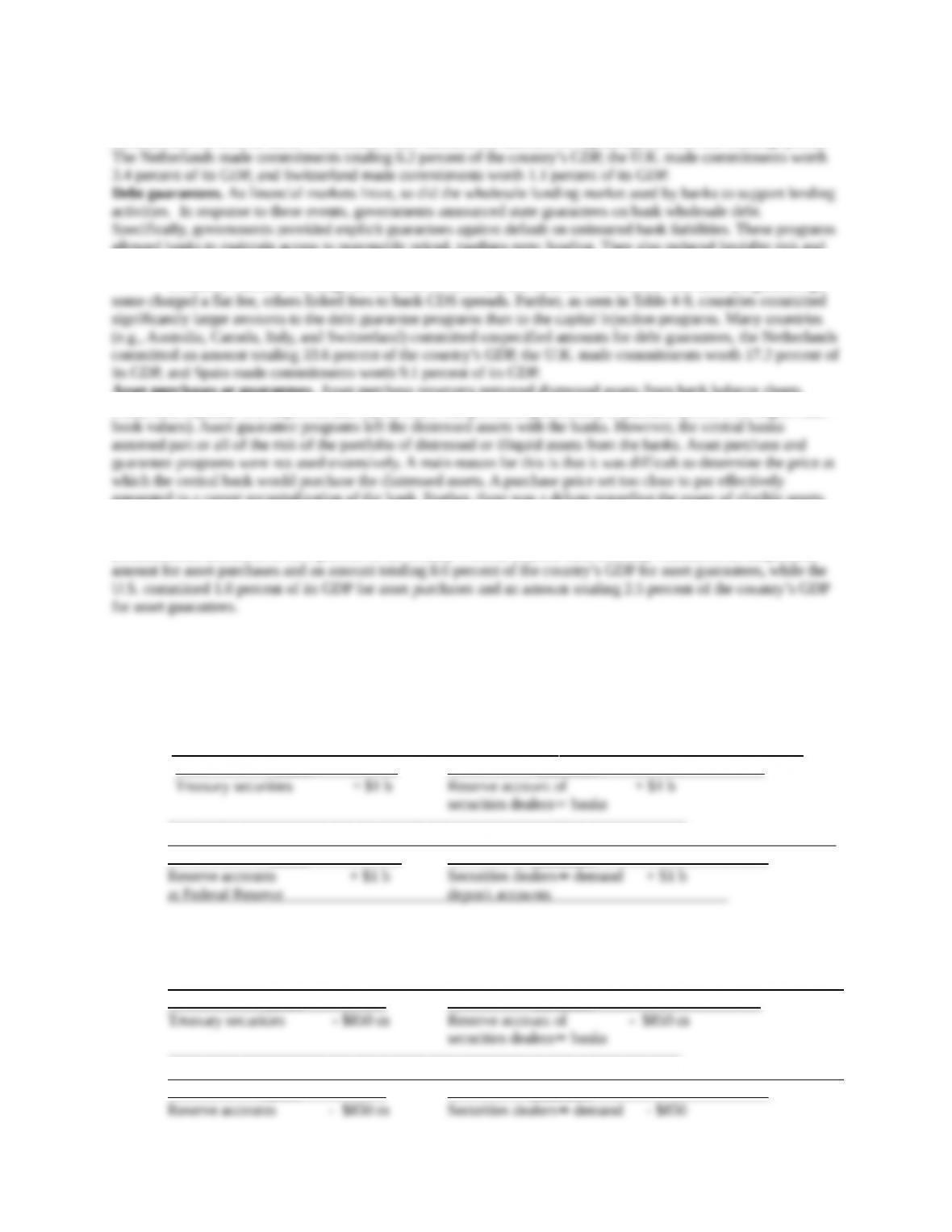

1. For the purchase of $1 billion in securities, the balance sheet of the Federal Reserve System and commercial

banks is shown below.

Change in Federal Reserve’s Balance Sheet

Assets Liabilities

—————————————————————————————————-

Change in Commercial Bank Balance Sheets

Assets Liabilities

2. For the sale of $850 million in securities, the balance sheet of the Federal Reserve System and commercial banks

is shown below.

Change in Federal Reserve’s Balance Sheet

Assets Liabilities

—————————————————————————————————

Change in Commercial Bank Balance Sheets

Assets Liabilities

at Federal Reserve deposit accounts

3.

a. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

———————————————————————————————

Bank Three

Assets Liabilities

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

New initial required reserves = 0.08 x $600m = $48m

Change in bank deposits = (1/0.08) x ($60m – $48m) = $150m

Federal Reserve Bank

Assets Liabilities

—————————————————————————————————

Bank Three

Assets Liabilities

b. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

———————————————————————————————

Bank Three

Assets Liabilities

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

Federal Reserve Bank

Assets Liabilities

—————————————————————————————————

Bank Three

Assets Liabilities

4.

a. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

———————————————————————————————

BSW Bank

Assets Liabilities

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

New initial required reserves = 0.06 x $150m = $9m

Change in bank deposits = (1/0.06) x ($15m – $9m) = $100m

Federal Reserve Bank

Assets Liabilities

—————————————————————————————————

BSW Bank

Assets Liabilities

b. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

———————————————————————————————

BSW Bank

Assets Liabilities

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

Federal Reserve Bank

Assets Liabilities

—————————————————————————————————

BSW Bank

Assets Liabilities

5.

a. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

———————————————————————————————

National Bank

Assets Liabilities

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

Federal Reserve Bank

Assets Liabilities

Securities $41.379m Reserve accounts $41.379m

—————————————————————————————————

National Bank

Assets Liabilities

b. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

Securities $50m Reserve accounts $50m

——————————————————————————————————————

National Bank

Assets Liabilities

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

Federal Reserve Bank

Assets Liabilities

—————————————————————————————————

National Bank

Assets Liabilities

6.

a. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

———————————————————————————————

MHM Bank

Assets Liabilities

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

New initial required reserves = 0.12 x $250m = $30m

Change in bank deposits = (1/(0.12 + (1 – 0.8))) x ($30m – $25m) = $15.625m

Federal Reserve Bank

Assets Liabilities

—————————————————————————————————

MHM Bank

Assets Liabilities

b. Panel A: Initial Balance Sheets

Federal Reserve Bank

Assets Liabilities

Securities $25m Reserve accounts $25m

————————————————————————————————————

MHM Bank

Assets Liabilities

Loans $225m Transaction deposits $250m

Reserve deposits 25m

at Fed

Panel B: Balance Sheet after All Changes Resulting from Decrease in Reserve Requirement

Federal Reserve Bank

Assets Liabilities

Securities $32.318m Reserve accounts $32.318m

—————————————————————————————————

MHM Bank

Assets Liabilities

7. a. Increase in bank deposits and money supply = (1/0.05) x $500m = $10 billion