1.1.1.1.1Chapter Four

The Federal Reserve System, Monetary

Policy, and Interest Rates

1.1.1.2 I. Chapter Outline

1. Major Duties and Responsibilities of the Federal Reserve System: Chapter Overview

2. Structure of the Federal Reserve System

a. Organization of the Federal Reserve System

b. Board of Governors of the Federal Reserve System

c. Federal Open Market Committee

d. Functions Performed by Federal Reserve Banks

e. Balance Sheet of the Federal Reserve

3. Monetary Policy Tools

a. Open Market Operations

b. The Discount Rate

c. Reserve Requirements (Reserve Ratios)

4. The Federal Reserve, the Money Supply, and Interest Rates

a. Effects of Monetary Tools on Various Economic Variables

b. Money Supply versus Interest Rate Targeting

5. International Monetary Policies and Strategies

a. Systemwide Rescue Programs Employed During the Financial Crisis

II. Learning Goals

1. Understand the major functions of the Federal Reserve System.

2. Identify the structure of the Federal Reserve System.

3. Identify the monetary policy tools used by the Federal Reserve.

4. Appreciate how monetary policy changes affect key economic variables.

5. Understand how central banks around the world adjusted their monetary policy during the

financial crisis.

1.1.1.3 III. Chapter in Perspective

This chapter presents an overview of the Federal Reserve System, including a brief look at its

history and structure. The major functions performed by the Fed are covered and the balance

sheet of the Fed is examined. The chapter provides the reader with a non-technical explanation

of the effects of monetary policy on interest rates and the economy. The deposit growth

multiplier concept is introduced and a simple ‘transmission mechanism’ depicting the effects of

a change in Fed policy on the economy is presented. Different monetary targets such as

borrowed and non-borrowed reserves and interest rate targets are also discussed.

Intervention into foreign exchange markets is also briefly covered. The new edition also

discusses the Fed’s rescue programs employed during the financial crisis.

1.1.1.4 IV. Key Concepts and Definitions to Communicate to Students

Discount rate FRB NY Trading Desk

Discount window Policy directive

Check clearing Repurchase agreement

ACH and Fed Wire Primary credit

Federal Open Market Committee Seasonal credit

Open market operations Secondary credit

Reserves Deposit growth multiplier

Monetary base M1 and M2

Required and excess reserves Foreign exchange intervention

Fed funds rate Borrowed and non-borrowed reserve

targets

Transmission mechanism

Policies of other major central banks

TALF

Quantitative easing

1.1.1.5 V. Teaching Notes

1. Major Duties and Responsibilities of the Federal Reserve System: Chapter Overview

The Federal Reserve was created in 1913 in response to a series of U.S. financial panics which

culminated in a particularly severe panic in 1907. The Fed was created to serve as a lender of

last resort, as a bank regulator and as a monitor of the money supply. Current objectives of the

Fed include stimulating sustainable non-inflationary economic growth while keeping

employment high. Not everyone agrees with the dual mandate of the Fed. Monetarists feel that

the Fed’s purpose should be to limit inflation. The Fed also assists in facilitating the nation’s

payment systems. The Fed operates the Fed Wire which facilitates trading of bank reserves and

an Automated Clearing House (ACH), which is a similar payments mechanism for debit and

credit transactions.1 The Fed is largely independent of Congress and the President, at least in the

short run. The Humphrey-Hawkins Act of 1978 however requires the Fed to present their

monetary policy goals and an assessment of how well they are meeting their goals to Congress

twice a year.

1The Clearing House Interbank Payments System (CHIPS) provides yet another payment mechanism. CHIPS is a

private sector electronic network operated by about 100 U.S. and foreign banks to facilitate correspondent services

and international transactions.

The four major functions of the Fed today include: a) conducting monetary policy, b) supervising

and regulating depository institutions, 3) maintaining the stability of the financial system and 4)

providing payment and other financial services to many institutions, including governments.

2. Structure of the Federal Reserve System

a. Organization of the Federal Reserve System

There are 12 Federal Reserve Banks (FRBs) located throughout the country. The structure was

originally intended to disperse power along regional lines throughout the country. To some

extent this dispersion still remains, but the major authority to promulgate and implement

monetary policy now lies in Washington, D.C. with the Board. Each FRB has a nine member

Board of Directors consisting as follows:

Six are elected by member banks in the district, of these six, three are non-bank business

people.

Three are appointed by the Board of Governors of the Federal Reserve System.

FRBs are nonprofit organizations, but they are owned by the member banks in their district. Part

of the independence of the Fed arises because the Fed generates positive net income from

interest and fees so it is not directly dependent on Congressional funding. The Fed now pays

interest on bank reserves and this reduces the profitability of the Fed. If the interest rate paid

increases with the Fed funds rate this could also create a perverse incentive that could

conceivably affect Fed policy because Fed profitability would be reduced if the Fed increased

interest rate targets. The Fed argues that paying interest minimizes reserve volatility.

Teaching Tip: In a bid to stave off negative inflation in Europe the ECB is considering charging

negative deposit rates on bank reserves. This should encourage banks to lend excess reserves

and stimulate the Eucopean economyrather than pay interest.

b. Board of Governors of the Federal Reserve System (BoGov)

The BoGov is comprised of seven members and each member is appointed to a non-renewable

14 year term by the President of the United States and confirmed by the Senate. Terms are

staggered so that one term expires every other January. The President appoints the chairman and

vice-chairman of the board from among BoGov members to four year terms that can be repeated.

The board has two major areas of responsibility; the formulation and conduct of monetary policy

through the FOMC (see below), and the promulgation of bank regulations. The board can

change the discount rate and bank reserve requirements.

c. Federal Open Market Committee (FOMC)

The 12 member FOMC is the body that formulates and conducts monetary policy. Seven of the

12 members are comprised by the BoGov; thus, the BoGov has a controlling vote on the FOMC.

The remaining members are 1) the President of the New York Federal Reserve Bank and 2) four

presidents of other Federal Reserve Banks, chosen on a rotating basis. The FOMC conducts

open market operations to implement monetary policy. Open market operations are the

purchase and sale of U.S. government securities to increase or decrease the level of bank

reserves (money supply) respectively. Open market operations are the most commonly used

policy tool to conduct monetary policy. The results of each FOMC meeting are compiled in the

so called “Beige Book,” which summarizes information on current economic conditions

compiled by the district banks, and from interviews with business leaders and economists, etc.

d. Functions Performed by Federal Reserve Banks

Functions include:

Assisting in the conduct of monetary policy and economic analysis

Supervision and regulation of banks and bank holding companies in their district

The new Wall Street Reform and Consumer Protection Act of July 2010 requires the Fed

to supervise complex financial institutions that could generate systemic risk to the

economy. The Fed (and others) has now been given broader powers to seize or break up

institutions whose actions could harm the economy.

The Fed is now also charged with implementing federal laws designed to protect

consumers in credit and other financial transactions. The Fed is charged with

implementing regulations to ensure compliance, investigating complaints, and ensuring

availability of services to low and moderate income groups and certain geographic

regions.

Provision of government services for the U.S. Treasury

Replacement of old currency and issuance of new currency

Providing check clearing services for a fee

The number of checks cleared peaked at 17 billion in 2000 and has since declined as

alternatives to checks have risen and industry consolidations. In October 2004 the Check

21 Act authorized the use of an electronic image rather than a paper check for settlement.2

This switch was expected to save the banking industry as much as $3 billion per year.

Presumably competition forces banks to pass on the cost savings to customers in the form

of reduced checking fees. Customers will lose the ability to play the float (which can be

several days) as checks may now be very quickly cleared (as soon as deposited), making

them more similar to most debit cards. Customers must take care that sufficient funds are

available at the time the check is spent with most retailers or they could overdraw. For

instance a customer could no longer write a check in the afternoon the day before payday,

knowing that the check will not clear before the payroll deposit the next day. This is a

dubious practice anyway (technically it is kiting, an illegal activity). Customers who run

low balances would be advised to apply for overdraft protection. Banks can no longer

automatically cover overdrafts without written permission of the bank customer.

The Fed ACH (the Fed’s automated clearing house) is now offering same day check

clearing for certain checks converted to electronic images rather than next day settlement.

Providing wire transfer services through the Fed Wire

Providing district economic analysis and research

According to the Financial Services Policy Committee of the Federal Reserve’s 2012 report,

in 2011 more than 85% of noncash payments were electronic. The breakdown was as

follows:

47 billion debit transactions

26 billion credit

22 billion ACH

2 The grounding of cargo aircraft after the September 11, 2001 terrorist attacks also ‘grounded’ millions of checks

waiting to be flown around the country in the clearing and settlement process. This spurred Congress on to passing

the Check 21 law.

9 billion prepaid cards

e. Balance Sheet of the Federal Reserve & Growth due to Financial Crisis

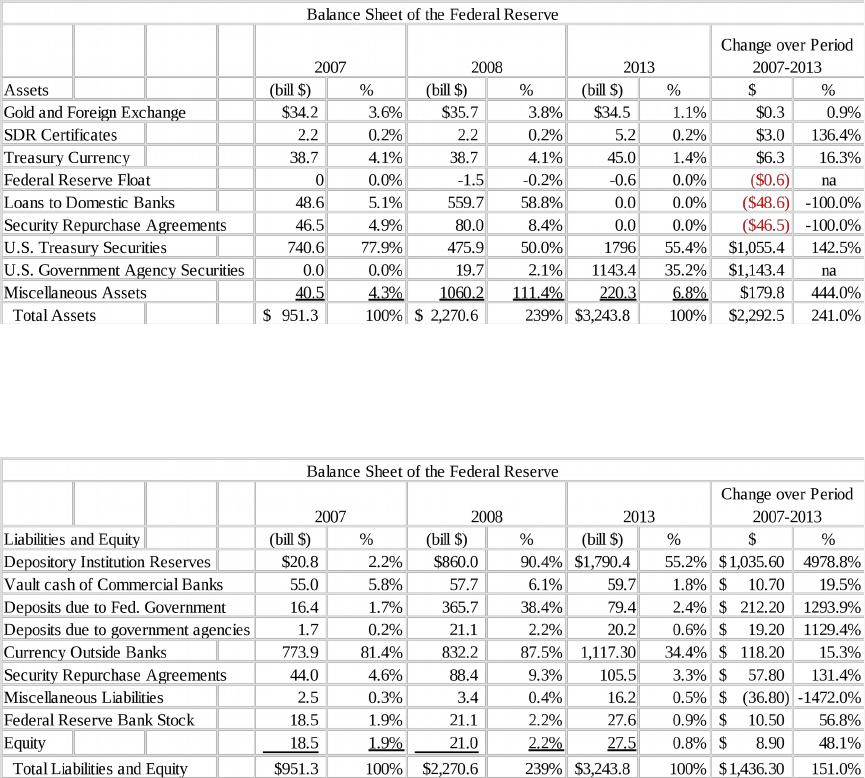

The Federal Reserve’s balance sheet grew 241% from 2007 to 2013 due to the ongoing financial

crisis. Much of the extraordinary growth is due to the Fed’s usage of quantitative easing in an

attempt to support mortgage markets and stimulate growth.

Notice the extraordinary growth in depository institution reserves. Banks have not lent anywhere

near their available capital. Some have argued that this is because the Fed began paying interest

on reserves in October 2008 although this is unlikely to be the main cause. The interest rate is

set to equal the target Fed Funds rate. This may reduce the incentive for banks to lend excess

reserves in the Fed Funds market. Of course loan rates (and thus profits) are higher than the Fed

Funds rate. Nevertheless this is posited as one problem with the effectiveness of Fed policy in

stimulating growth in the economy. The Fed’s lending facilities created more bank reserves, but

did not result in greater lending. Total bank lending turned up in 2013.

The Fed expanded availability of Discount Window borrowing to investment banks in order to

encourage liquidity in the financial system at the start of the financial crisis. Liquidity had been

impaired by the credit crunch spurred by the fallout in the subprime mortgage markets. The Fed

and the Treasury helped arrange a bailout of Bear Stearns by J.P. Morgan Chase. Bear Stearns

was a failing investment bank heavily involved in the mortgage markets and was on the brink of

defaulting on many of its repo arrangements. The Fed took the unprecedented step of

guaranteeing $30 billion of Bear Stearns’ illiquid mortgage assets.3 Even before the bailout of

Bear Stearns the Fed had agreed to swap up to $200 billion of Treasuries it holds for illiquid

mortgage backed securities in an effort to restore liquidity to the markets.4 In particular the short

term repo markets had stopped functioning on worries about failures of underlying mortgages

backing securities, many through CDO structures.

The growth in the balance sheet reflects the Fed’s responses to the financial crisis. At the end of

2007 the Fed created a Term Auction Facility (TAF) extended discount window borrowing on an

auction basis. In March 2008 the Fed facilitated the J.P. Morgan Chase purchase of Bear Stearns

that took some of Bear’s risky assets off their books (and onto the Fed’s). The Fed also created

the Term Securities Lending Facility (TSLF) which swapped Treasury securities for less liquid

and riskier securities and the Primary Dealer Credit Facility (PDCF) which expanded discount

window loans to non-banks. In the fall of 2008 with the collapse of Lehman Brothers and

Goldman-Sachs and Morgan Stanley becoming commercial banks, the Fed created additional

facilities to assist in credit flows. The Fed created the Asset-Backed Commercial Paper Money

Market Mutual Fund Liquidity Facility (AMLF), the Commercial Paper Funding Facility

(CPFF), the Money Market Investor Funding Facility (MMIFF), and the Term Asset-Backed

Securities Loan Facility (TALF). The AMLF and the CPFF were created because liquidity

collapsed in the commercial paper market. The MMIFF was created to help stem liquidity

problems in money market mutual funds that resulted when one fund failed. The TALF was

designed to encourage securitization to continue. Slowdowns in securitization reduced the

amount of credit available to borrowers in certain markets. Average weekly lending from the

Fed grew from about $59 million in 2006 to almost $850 billion in late 2008.

3. Monetary Policy Tools

The major process by which the Fed normally impacts the economy is through influencing the

market for bank reserves. Banks trade excess reserves among themselves at the interest rate

called the fed funds rate. The Fed attempts to influence the fed funds rate by either affecting

demand or supply of funds available for lending between banks. Targeting the level of reserves

in the economy is tantamount to targeting the supply of funds available for bank to bank lending

(and by inference, the amount of funds available for lending to non-bank customers). Targeting

interest rates, as the Fed has done since 1993, is the same as influencing the demand for bank

reserves. The Fed cut interest rates 11 times in 2001 to stimulate the weakening economy. The

fed funds target rate was increased 5 times in 2004 from a low of 1% to a year ending high of

3 “The Week That Shook Wall Street: Inside the Demise of Bear Stearns,” by Robin Sidel, Greg Ip, Michael Phillips

and Kate Kelly, The Wall Street Journal Online, March 18, 2008 Page A1.

4 “Fed Offers Lifeline for Spurned Debt,” by Greg Ip, The Wall Street Journal Online, March 12, 2008, Page A1.

2.5% (each increase was 25 basis points). In June 2005 the target fed funds rate was 3.25% but

by August 2006 the target rate had been increased to 5.25% due to inflation fears. In 2007 the

Fed reversed its interest rate policy and began to decrease the Fed funds target. In April 2008 the

Fed funds target was 2.00% and the discount rate was 2.25%. By year end 2008 the Fed funds

target was reduced to between 0 and 0.25% and the discount rate was 0.5%. These rates were

maintained throughout 2009. In Feb 2010 the Fed kept the target Fed funds rate at 0 to 0.25%

but raised the discount rate to 0.75% where both rates remain as of this writing. In November of

2008 the Fed announced it would engage in up to $600 billion of purchases of Treasuries and

mortgage backed securities, a process termed quantitative easing in order to encourage the flow

of credit in the economy. This amount was increased in March 2009 to $1.7 trillion. From the

end of 2008 through the first quarter of 2010 the Fed bought $1.7 trillion of securities. In

November 2010 the Fed announced a new series of bond buying of up to $600 billion in what

has been termed QE2. QE3 began in September of 2012 with the Fed announcing the purchase of

$40 billion Treasuries and $40 billion mortgage backed securities per month. The Fed began

tapering (gradually reducing) the monthly purchases in 2013 and on into 2014 even though the

Fed has repeatedly reiterated that short term interest rates would remain low on into 2015 unless

conditions improved rapidly. The Fed backed away from switching policy when unemployment

fell to or below 6.5% because of slow economic growth and declines in the labor force

participation rate. The Fed also has a target inflation rate of 2%.

The text mentions that Fed policy appears to follow a Taylor rule. A Taylor rule suggest the Fed

should increase interest rates when inflation is above target or if employment is above full

employment and decrease rates when inflation is below target or if the economy is at less than

full employment. Because of expectations and external shocks monetary policy rules must be

applied with discretion.

Ben Bernanke’s term ended in January 2014 and Janet Yellen became the new chairman of the

Fed. Chair Yellen has not changed the policy course set by Bernanke’s board although she is

considered to be ‘doveish’ or more likely to pursue a loose monetary policy for longer than

inflation hawks would.

Current rates & risks over the year, with links to meeting minutes can quickly be found at the

Federal Reserve Monitor of the Wall Street Journal Online website. Levels of M1 and M2 can

be found on the same website under Federal Reserve Data.

a. Open Market Operations

Open market operations are the buying and selling of U.S. government securities by the Fed.

The FOMC drafts a policy directive to change a targeted monetary aggregate such as M1, M2,

M3 or an interest rate target such as the fed funds rate and sends it to the N.Y. Federal Reserve

Bank Trading Desk.5 If the FOMC wishes to increase the money supply the directive will

specify that the Trading Desk is to buy U.S. government securities and credit the seller with

additional reserves at the Fed. In this manner new money is created. If the FOMC wishes to

decrease the money supply, securities will be sold and the buyer will pay for them by having

bank reserves removed from their account. Temporary changes in the money supply can be

enacted by using repurchase agreements. Fed use of a repo will temporarily increase the

money supply; a reverse repo could be used to temporarily reduce bank reserves and the money

supply.

As noted in the text, in March 2009 the Fed announced it would buy $300 billion of long-term

Treasury securities in what would become known as quantitative easing 1. This is unusual in the

size of the announced purchase and in purchasing long term securities. This was the first time

the Fed had done so since the 1960s. The Fed wanted to add liquidity and to keep long term

interest rates down. The Fed also wished to signal that they would do whatever it took to

stabilize the economy.

Teaching Tip: Many students think that the primary method of increasing the money supply is by

printing new money. In actuality, increases in the money supply are usually accomplished by

increasing bank reserves.

Teaching Tip: The U.S. Treasury operates the mints for coins.

Teaching Tip: Part of the importance of the target fed funds rate is that this rate affects other rates

because this interest rate reflects the bank’s cost of short term funds. In particular, the prime rate

usually changes after a change in the fed funds rate.

b. The Discount Rate

Historically, the discount rate is the rate the Federal Reserve Banks charge to make emergency

loans to DIs in fulfilling its role as lender of last resort. The Fed implemented changes in its

discount window policy in January 2003. The changes did two things, 1) raise the cost of

borrowing from the Fed and 2) make it easier for banks to borrow from the Fed. There are now

three lending programs available from the discount window:

1. Primary credit – Primary credit is available to healthy depository institutions (DIs) on a

short term basis. The borrowed funds are not restricted in their use. The rate paid is

typically 1% above the fed funds target rate. As of June 2005, the discount rate was

4.25%. Traditionally the discount rate was kept below the fed funds rate, but banks were

limited to borrowing from the Fed only if they could show they could not borrow from

the private markets (such as the fed funds market).

2. Secondary credit – Short term secondary credit is available to troubled institutions. The

interest rate charged is higher than the rate on primary credit. Secondary credit is

restricted in how the funds may be used. The borrowing bank cannot use secondary

credit to expand the bank’s assets.

5 This is why the President of the N.Y. Fed always sits on the FOMC.

3. Seasonal credit – Seasonal credit is available for institutions that can demonstrate a

pattern of intra-year changes in borrowing needs, usually due to seasonal deposit changes

and loan demand as occurs in agricultural or tourist dependent areas. Seasonal credit is

available on a longer term basis and allows the borrowing institution to carry less liquid

assets which are low earning to meet funds needs.

The discount rate is not usually a direct monetary policy tool and it would be very difficult to

predict the change in borrowing that would result from a change in the discount rate. Changes in

the discount rate have at times however signaled the Fed’s intentions to allow interest rates to

move in one direction or the other. As mentioned earlier, the Fed has now opened up the

discount window to securities brokers and dealers and has decreased the spread between the Fed

funds target rate and the Discount Rate to 25 basis points.

As discussed above with the Fed’s balance sheet, in 2008 the Fed broadened access to the

Discount Window facility through the PDCF. The move was welcomed by securities dealers

whose average daily borrowing was over $30 billion initially. The Fed also lowered the spread

between the discount rate and the target fed funds rate during the crisis to only a quarter of a

point. This move, along with a slowdown in lending in private bank funding markets encouraged

additional borrowing from the discount window. These moves provided liquidity to institutions

but it is less clear that the ultimate goal of stimulating private sector credit growth was achieved.

c. Reserve Requirements (Reserve Ratios)

The third, and least used, monetary policy tool is changes to the reserve requirement ratios.

Banks are required to maintain reserves on deposit at the Fed to back a certain percentage

(basically 10%) of transaction deposits. If this ratio is increased, or if it is imposed on more

types of accounts, banks will have to hold more reserves at the Fed and less money will be

available to flow through the economy. The change in bank deposits is (1 / New reserve

requirement) New excess reserves, assuming no drains.6

If reserves are $2 billion and the Fed increases reserves by 1% or $20 million when banks have a

10% reserve requirement then the predicted increase in bank deposits would equal:

1/0.10 * $20 million = $200 million increase in bank deposits.

If the Fed reduced the reserve requirement to 9% instead then the new level of excess reserves

would be 1% of $2 billion or $20 million. The predicted increase in bank deposits would then

equal:

1/0.09 * $20 million = $222 million

The amount of drains is not very predictable. For instance, decreases in reserve requirements

cannot be guaranteed to lead to increases in the money available for lending if banks choose to

hold higher amounts of excess reserves at the Fed (as they did in the early 1990s and again in

2008.) Changes in the reserve requirement are rarely used as a monetary policy tool. This is

perhaps because it is difficult to predict the effect of changes in the reserve ratio on the money

supply. Changing the ratio frequently would likely impose additional costs on the banking

system which attempts to manage and minimize its excess reserves.

6 The multiplier used assumes that all possible amounts of money (subject to reserve requirements) loaned out are

re-deposited into banks and then re-lent and re-deposited, ad infinitum.