31. Coupon Bond: Par value = $1,000, Coupon rate = 10%, annual payments, rb = 8%, Maturity = 2 years

t CF CF/(1 + 0.08) t PV of CF x t

1 $100 $92.59 $92.59

If rb = 10%

t CF CF/(1 + 0.10) t PV of CF x t

1 $100 $90.91 $90.91

If rb = 12%

t CF CF/(1 + 0.12) t PV of CF x t

1 $100 $89.29 $89.23

c. Zero Coupon Bond: Par value = $1,000, Coupon rate = 0%, rb = 8%, Maturity = 2 years

t CF CF/(1 + 0.08) t PV of CF x t

If rb = 10%

t CF CF/(1 + 0.10) t PV of CF x t

If rb = 12%

t CF CF/(1 + 0.12) t PV of CF x t

d. Changing the yield to maturity does not affect the duration of the zero coupon bond.

32. Five-year Treasury Bond: Par value = $1,000, Coupon rate = 10%, semiannual payments, rb = 10%, Maturity = 5 years

t CF CF/(1 + 0.10/2) t(2) PV of CF x t

0.5 $50 $47.62 $23.81

1 $50 $45.35 $45.35

1.5 $50 $43.19 $64.79

2 $50 $41.14 $82.27

2.5 $50 $39.18 $97.94

3 $50 $37.31 $111.93

If rb = 12%

t CF CF/(1 + 0.12/2) t(2) PV of CF x t

0.5 $50 $47.17 $23.58

1 $50 $44.50 $44.50

1.5 $50 $41.98 $62.97

2 $50 $39.60 $79.21

2.5 $50 $37.36 $93.41

If rb = 14%

t CF CF/(1 + 0.14/2) t(2) PV of CF x t

0.5 $50 $46.73 $23.36

1 $50 $43.67 $43.67

1.5 $50 $40.81 $61.22

2 $50 $38.14 $76.29

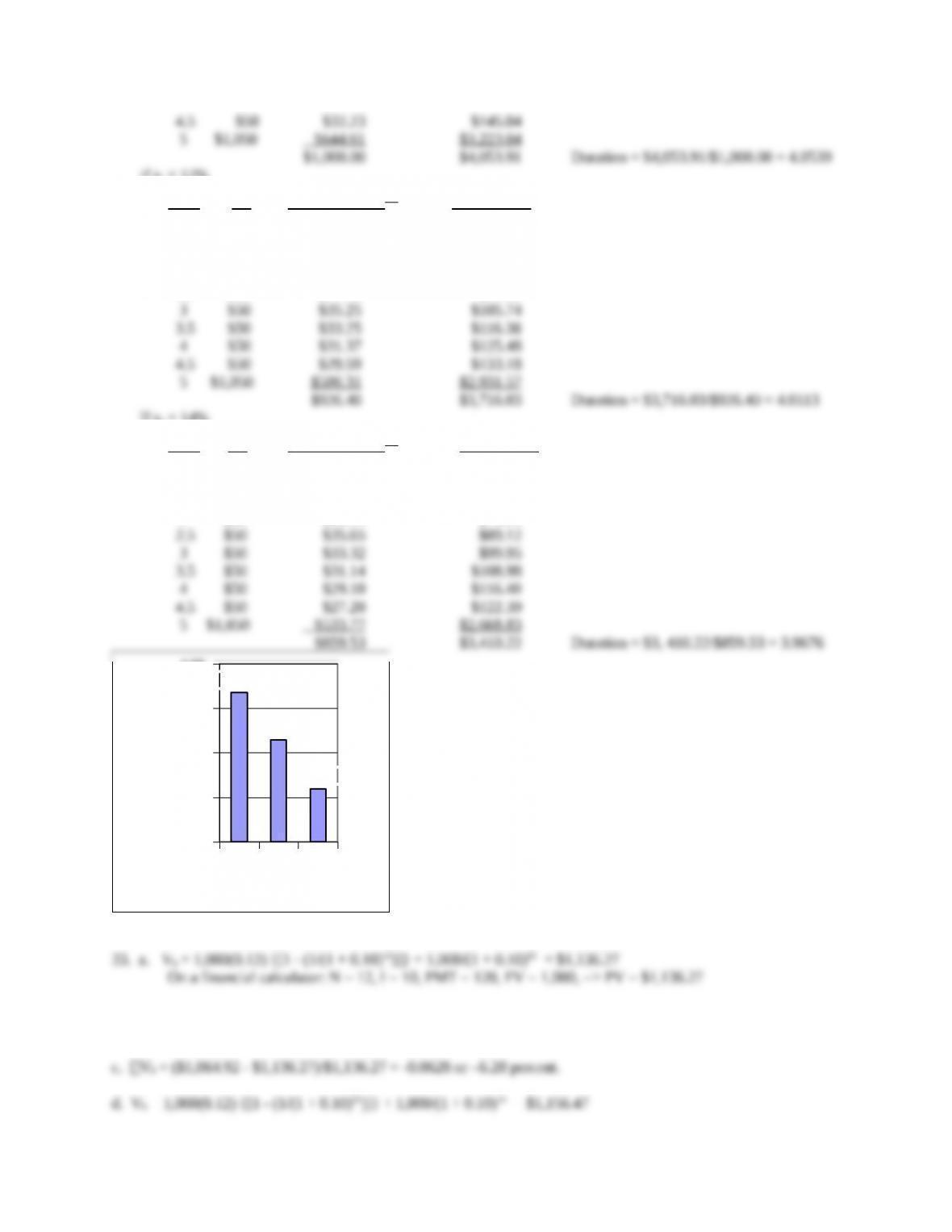

0.10.12 0000000000000020.14000000000000001

3.92

3.96

4.00

4.04

4.08

4.0539

4.0113

3.9676

Yield t o M a t urit y

Years

b. Vb = 1,000(0.12) {[1 – (1/(1 + 0.11)12)]} + 1,000/(1 + 0.11)12 = $1,064.92

On a financial calculator: N = 12, I = 11, PMT = 120, FV = 1,000, => PV = $1,064.92

Vb = ($1,073.79 – $1,156.47)/$1,156.47 = -0.0715 or –7.15 percent.

b. Vb = 1,000(0.15) {[1 – (1/(1 + 0.13)5)]} + 1,000/(1 + 0.13)12 = $1,070.34

c. Vb = ($1,070.34 – $1,108.14)/$1,108.14 = -0.0341 or –3.41 percent.

35. a. D = 4.05 years

time cash flow (1 + 0.10/2) t(2) CF/(1 + 0.10/2) t(2) PV of CF x t

0.5 50 0.9524 47.620 23.810

1.0 50 0.9070 45.350 45.350

1.5 50 0.8638 43.190 64.785

2.0 50 0.8227 41.135 82.270

b. Duration for a 14% yield to maturity = 3409.95/859.53 = 3.97 years

36. a. D = 3,393.18/1,000 = 3.39 years

Time Cash Flow 1/(1 + 0.10/2) t(2) CF/(1 + 0.10/2) t(2) PV of CF x t

0.5 50 0.9524 47.62 23.81

1.0 50 0.9070 45.35 45.35

1.5 50 0.8638 43.19 64.79

d. As maturity increases, duration increases but at a decreasing rate.

37. D = 8 years;

D = 10 years;

D = 12 years.

38. a.

time cash flow (1 + 0.10) t CF/(1 + 0.10) t PV of CF x t

1.0 137.6 0.9091 125.091 125.091

2.0 137.6 0.8264 113.719 227.438

b. The cash flows from this investment during the four-year investment horizon will be

39. a.

time cash flow (1 + 0.10) t CF/(1 + 0.10) t PV of CF x t

1.0 800 0.9091 727.27 727.27

2.0 800 0.8264 661.16 1322.31

b. Duration on 10% coupon bond = 4.17 years

At –0.10%: Pb = 1,000(0.08) {[1 – (1/(1 + 0.079)30)]} + 1,000/(1 + 0.079)30 = $1,011.36

On a financial calculator: N = 30, I = 7.9, PMT = 80, FV = 1,000, => PV = $1,011.36

At –2.0%: Pb = 1,000(0.08) {[1 – (1/(1 + 0.06)30)]} + 1,000/(1 + 0.06)30 = $1,275.30

On a financial calculator: N = 30, I = 10, PMT = 80, FV = 1,000, => PV = $1,275.30

b. Pb = -D x [rb/(1+ rb)] x Pb

At +0.10%: Pb = -12.1608 x 0.001/1.08 x $1,000 = -$11.26 => Pb = $988.74

Price – market Price – duration Amount

determined estimation of error

At +0.10%: $988.85 $988.74 $0.11

At -0.10%: $1,011.36 $1,011.26 $0.10

41. We know -D = [Pb/Pb]/[rb/(1+ rb)], so -D = (20/975)/(-0.005/1.0975) =- 4.5 years; D = 4.5 years.