Chapter 03 – Security Valuation 6th Edition

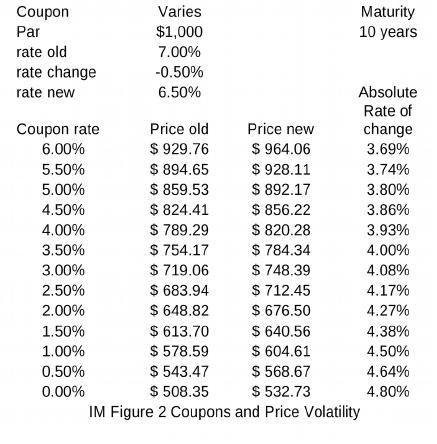

1. Impact of Coupon Rates on Security Values

a. Coupon Rate and Security Price

Ceteris paribus, the higher the coupon rate the higher the bond’s price. See the Teaching

Tip in 3a for an explanation.

b. Coupon Rate and Security Price Sensitivity to Changes in Interest Rates

A higher coupon results in lower bond price sensitivity to interest rate changes, ceteris

paribus. The bigger the coupon the greater the percentage of your initial investment that

is recovered in the near term (see the last Teaching Tip in 5.b.), or the bigger the coupon

the sooner you recover the investment. Suppose you are comparing two five year bonds,

one with a zero coupon and one with a 15% coupon. If interest rates rise the 15% coupon

bond pays you a much larger sum of money quickly with which you can reinvest and earn

the new higher interest rate. The zero coupon bond gives you no money with which you

can reinvest and earn the higher rate so the zero drops more in value. IM Figure 2 below

illustrates the effect of coupon on price volatility for a 10 year maturity bond with a yield

rate change from 7% to 6.5% for bonds with different coupons. Notice that lower coupon

bonds exhibit a greater price change for the given rate change. The greatest volatility is

exhibited by the zero coupon bond, but as with maturity, the price change increases at a

decreasing rate for a declining coupon rate. At this point in the development an investor

needs to consider both maturity and coupon to understand their exposure to interest rate

risk. One of the purposes of developing the duration concept in the next section is that

duration reduces the analysis to one dimension by incorporating the effect of coupon into

the maturity effect on price volatility.

2. Duration

a. A Simple Illustration for Duration

Duration is the weighted average time to maturity on a financial security using the

relative present values of the cash flows as weights. This definition will initially mean

very little to students. To understand the concept implied by the definition, think of an N

year annual payment coupon bond as a portfolio of N zero coupon bonds where the first

N-1 of the bonds pay the coupon amount and the last one pays the coupon plus the par

Ch 3- 1

Chapter 03 – Security Valuation 6th Edition

amount. The coupon bond’s duration is the average maturity of the portfolio of zero

coupon bonds. However, we cannot take a simple average because not all the cash flows

in each year are identical. Moreover, Chapter 2 tells us that we cannot compare a cash

flow in year 1 with a cash flow in year N. So we construct a series of weights that tell us

what percentage of our money (in today’s dollars) we recover in each year. To do this

take the present value of each cash flow divided by the purchase price of the bond. For

instance, for a 5 year bond suppose we recover in present value terms 5% of our

investment in year one , 4% in year two, 3% in year three, 2% in year four and 86% in

year five. We receive cash in each of the next five years (or a zero matures in each of the

next five years): 1, 2, 3, 4 and 5. Thus, the bond’s duration is the weighted average

maturity of the zeros or (5%1) + (4%2) + (3%3) + (2%4) + (86%5) = 4.6 years.

Duration may perhaps be slightly better defined as a weighted average of the times in

which cash is received, a slightly different wording than the more common definition

above.

Teaching Tip: The above 5 year maturity coupon bond has the same price sensitivity as

a 4.6 year maturity zero coupon bond (ignoring convexity).

Teaching Tip: Thinking of duration as a weighted average life of a bond assumes the

bond’s cash flows do not change over the life. This concept of duration is problematic for

mortgage bonds or any bond with embedded options. In some of these cases duration

may be longer than the life of the bond or may be negative and the time concept of

duration then makes no sense. In these situations one should think of (modified) duration

as the percentage price change for a 100 basis point change in interest rates.

b. A General Formula for Duration

PV

r)(1

tCF

Dur

N

1t

t

t

For example: INT = $90 per year, annual r = 10%, Maturity = 6 years, m = 2

compounding periods per year, PV = $955.68}

Annual duration = 9.46 ÷ 2 = 4.73 years

Closed form version of the duration equation:

Ch 3- 2

Equation 5

Equation 4

$955.68

(1.05)

12$1045

(1.05)

t$45

periods annual–semi 9.46Dur

11

1t 12t

)PVIFAr)((1N

r)(P

INT

NDur Nr,

o

r

)(11

PVIFA where

N

Nr,

r

Chapter 03 – Security Valuation 6th Edition

This formula is from: Caks, J., W. Lane, R. Greenleaf, and R. Joules. (1985). A Simple

Formula For Duration, The Journal of Financial Research, 8(3).

INT

= Periodic cash flow in dollars

r = periodic interest rate

n = Number of compounding or payment periods

Dur = Duration = # Compounding or payment periods

Teaching Tip:

Variations of the basic duration formulae can be used. The versions shown above may be

used for annual or semiannual payment bonds or for amortizing loans. The duration

answer obtained from these equations will be in the number of compounding or payment

periods. For instance, if you use Equation 4 or 5 to find the duration of a semiannual

payment bond as shown above, you will get an answer in terms of the number of

semi-annual periods, rather than years. If one replaces PV in Equations 4 and 5 with

(m*PV), then the resulting duration answer will be in years.1 Alternatively, Equation 4

could be modified as follows to give an annual duration result for a semiannual payment

bond:

N

2/1t

t

PV

tPVCF

Dur

where PVCFt is the present value of the cash flow in time t, where t = ½, 1, 1½ , … N.

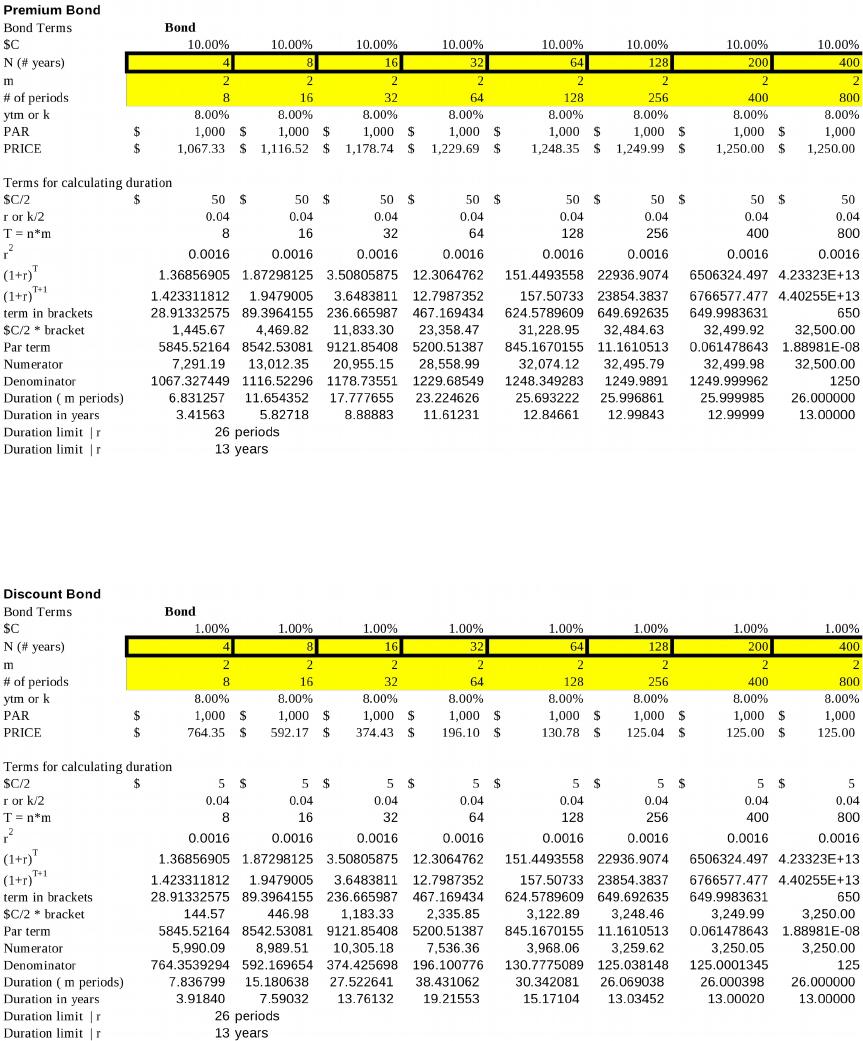

c. Features of Duration

Duration of a security with fixed cash flows and term may be thought of as a time

measure, usually presented in years. A greater coupon payment results in a shorter bond

duration. With a greater coupon the percentage weights on the early years are increased,

thus reducing the average maturity. The duration of a zero coupon bond is its maturity

because it has a 100% weight on the year in which the terminal cash flow occurs and a

0% weight on all other years. Except for certain deep discount bonds, the longer the

maturity of a bond the longer the bond’s duration (see the charts below). Notice that

duration increases at a decreasing rate as maturity increases. Duration has a limit with

respect to maturity for a given interest rate. The maximum duration of a bond can be

found as (1/ r) +1 where r is the periodic rate found as the ytm/2 for a bond and the

solution is the maximum number of payment periods. As you can see in the chart, for a

premium bond, the duration increases monotonically towards this maximum (26 periods

or 13 years. With an 8% APR the periodic rate for a semiannual payment bond is 4% and

1 Recall that m = number of compounding periods per year. In the prior chapter the text used c for m.

Ch 3- 3

Equation 4a

86325.8

2

0.05

(1.05)1

PVIFA

1

Nr,

periods annualsemi 9.468.86325)(1.0512

0.05)(955.68

45

12Dur

Chapter 03 – Security Valuation 6th Edition

the maximum is found as (1/0.04) + 1) as N is increased. Note that in the charts, m = c or

the number of compounding periods.

For a deep discount bond, the duration initially rises with maturity and then declines as

illustrated below:

Teaching Tip: Students should be aware that although duration is a modified measure of

maturity, it is still a measure of maturity and maturity is the predominant effect on

duration.

Ch 3- 4

Chapter 03 – Security Valuation 6th Edition

The higher the promised yield to maturity the shorter the duration. Using a higher

interest rate decreases the percentages weights on more distant cash flows (because of the

compounding effect the present value of more distant cash flows drops (%) more than the

present value of near term cash flows).

d. Economic Meaning of Duration

Taking the partial derivative of the bond price formula with respect to interest rates for a

zero coupon bond yields a simple relationship:

%P = – Maturity r / (1 + r) (r = yield to maturity)

%P = elasticity

Maturity can be used to predict the price change for small interest rate changes when

there are no coupons. This equation does not work for coupon bonds; its use in this case

would overestimate the volatility since coupons dampen a bond’s price volatility.

Duration is however a modified measure of maturity that reflects the reduced maturity

due to the early payment of interest (coupons) prior to maturity. In particular the duration

of a coupon bond has the same price sensitivity as a zero coupon bond that has a maturity

equal to the coupon bond’s duration (ignoring convexity). Thus it follows (without

calculus even) that %P = – Duration r / (1 + r) for a coupon bond. Duration may

be used to predict price changes for small interest rate changes for coupon bonds. For

convenience, practitioners sometimes calculate what is called ‘modified duration’ which

for bonds is Duration / (1 + rsemi) so that the only variable to be added to predict the price

change is r.

Important Note: Modified duration is Duration / (1 + rperiod). The ‘period’ would be

semiannual for most bonds and monthly for most loans. However when modified

duration is used to predict the price change in the formula, the rate change used is an

annual rate: %P = – Modified Duration / (1 + rannual). This can be a confusing point for

students.

Teaching Tip:

Why should students have to learn duration when today one can easily predict the bond

price change via a hand calculator, or better yet, with a spreadsheet? Two reasons:

1) Duration can be used as a strategic tool in trying to earn a higher rate of return, or to

minimize the risk associated with earning the promised yield to maturity. For instance,

for a given investment horizon one can try to lock in the current promised yield to

maturity by choosing a bond with a duration equal to the investment horizon. This is a

standard institutional bond investment strategy called immunization and it is described

in Appendix A. However, one can also try to beat the promised yield. If interest rates

are projected to fall one could choose a bond with a duration greater than the

investment horizon. If the investor is correct and rates fall, the gain in sale price of the

bond will more than outweigh the lost reinvestment income caused by the lower

reinvestment rate and the overall realized rate of return will be greater than the

promised yield. Conversely, one who is projecting rising rates can beat the promised

yield by choosing a bond with a duration shorter than the investment horizon.

2) Given the individual bond durations, the duration of a portfolio is a simple weighted

average of the durations of the bonds in the portfolio. Using the portfolio’s duration

Ch 3- 5

Chapter 03 – Security Valuation 6th Edition

makes it very easy to predict the net value change of the portfolio for a given change

in interest rates.

e. Large Interest Rate Changes and Duration

Duration is an accurate predictor of price changes only for very small interest rate

changes. For day to day fluctuations duration works quite well but when interest rates

move significantly, such as when the Fed makes an announcement of a rate change, the

predicted pricing errors can become significant. The prediction errors arise because bond

prices are not linear with respect to interest rates. At lower yield rates, bond prices are

more sensitive to interest rate changes than at higher initial promised yields. A given

percentage change in interest rates will result in a larger bond price change for a low

yield bond than for a high yield bond. Thus, a graph of bond prices versus interest rates

would be convex to the origin. Duration does not capture this change in sensitivity (or

convexity) of bond prices to interest rates. Duration predicts that the price changes of

bonds are linear with respect to changes in interest rates and thus duration predicts

symmetric price changes of a given interest rate increase or decrease. An examination of

Text Figures 3-7 and 3–8 indicates that this is not a true assertion. As mentioned above,

the bond’s price with respect to interest rates is convex to the origin. The duration is the

first derivative or slope of the line in Text Figure 3-7. Hence, the error in the bond price

prediction is due to the curvature of the line, and the degree of curvature is called the

convexity. Greater convexity leads to greater pricing prediction errors. The errors can

be quite economically significant for larger portfolios and for bigger interest rate changes.

Notably, convexity works in the investor’s favor. Duration over-predicts the price drop

that follows from an interest rate increase and under-predicts the price increase that

results from a yield decline. Investors will desire convexity in their bonds.2 The greater

the interest rate change, the greater the error in predicted prices and rates of return from

ignoring convexity. All fixed income securities that have cash flows prior to maturity

exhibit convexity. For more on convexity see Appendix 3B.

Appendix 3A: Duration and Immunization (Available on Connect or from your

McGraw-Hill representative)

Suppose you have a 5 year investment horizon and you are looking to immunize and lock

in the current promised 8% ytm. You find a likely candidate in an 8% coupon, 8% ytm

corporate bond with a 6 year maturity.

Duration: [80/1.08 + (80*2)/1.082 + (80*3)/1.08 3 + (80*4)/1.08 4 +(80*5)/1.085 +

(1080*6)/1.086] / 1000 = 4.9927, approximately 5 years

At the end of 5 years you must have achieved an ending wealth position of $1000 * 1.085

= $1469.33 if you are to have actually earned an 8% compound rate of return per year

(ytm).

Case 1: Rates stay same:

Future value (FV) coupons = $80 * [(1.085 – 1)/.08] = $ 469.33

2 This assumes that investors are long in bonds.

Ch 3- 6

Chapter 03 – Security Valuation 6th Edition

Price of bond end of 5th year = $1000.00

Total Ending Wealth = $1469.33

Case 2: Rates fall immediately after purchase to 7.5%:

Future value (FV) coupons = $80 * [(1.0755 – 1)/.075] = $ 464.67

Price of bond end of 5th year = $1080/1.075 = $1004.65

Total Ending Wealth = $1469.32

Realistically the investor must sell the bond immediately after the rate change, otherwise

rates may stay low for 4.9 years and then increase at the time of sale at year 5. The sale

will yield a price of $1,023.47, which can be reinvested at 7.5% for five years to give a

future value of $1,469.32

Case 3: Rates rise immediately after purchase to 8.5%:

Future value (FV) coupons = $80 * [(1.0855 – 1)/.085] = $ 474.03

Price of bond end of 5th year = $1080/1.085 = $ 995.39

Total Ending Wealth = $1469.42

Realistically the investor must again sell the bond immediately after the rate change.

This will yield a price of $977.23, which can be reinvested at 8.5% for five years to give

a future value of $1,469.42

If an investor chooses a bond with a duration greater than their investment horizon, their

pretax nominal realized yield will be improved by falling interest rates because the gain

in sale price will more than outweigh the loss in reinvestment income. Likewise, If an

investor chooses a bond with a duration less than their investment horizon, their realized

yield will be improved by rising interest rates because the loss in sale price will be

smaller than the gain in extra reinvestment income. (This example is drawn from

Gardner, Mills and Cooperman, Managing Financial Institutions: An Asset/Liability

Approach 4th ed. Dryden Press, 2000.)

Appendix 3B: More on Convexity (available in Connect or through your McGraw

Hill representative)

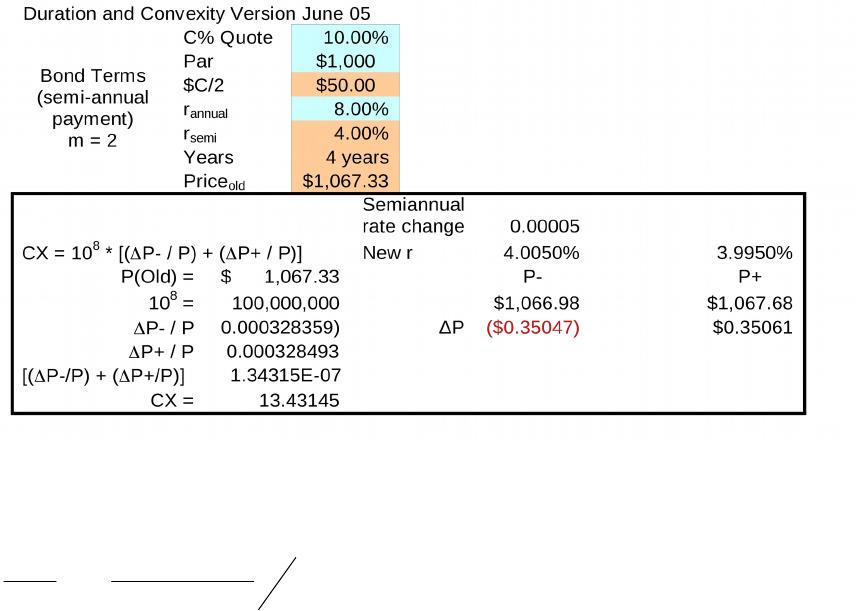

I. Measuring Convexity

There are various ways to measure convexity (CX). Cornett & Saunders measure CX

from the following formula:

CX = Scaling factor * [% loss in bond price from a 1 basis point rise in rates + % gain in

bond price from a 1 basis point drop in rates] written as:

CX = 108 * [(ΔP– / P) + (ΔP+ / P)] (This is called effective convexity)

The scaling factor used is 108; the factor is chosen to scale up the result to represent a 100

basis point change in rates.

The instructor may wish to include the following example calculation of CX for a 4 year

bond that pays interest semiannually (8 periods total) with a 10% annual coupon and an

8% annual promised ytm (r):

(m = number of compounding periods per year rather than c)

Ch 3- 7

Chapter 03 – Security Valuation 6th Edition

Teaching Tip:

If your students have had calculus, convexity can be found by taking the second

derivative of the bond price formula with respect to interest rates. The result is:

T

1t

2

old

)2t(

sem i

t

2

2

)m*ice(Pr

)r1(

CF)1t(t

)r(d

dP

(m = # compounding periods per year)

see for instance, Page 650 in Chapter 21in Investments: A Global Perspective, J.C.

Francis and R. Ibbotson, 2002, Prentice Hall, Upper Saddle River, NJ 07458.

II. Using Convexity

The predicted change in bond price for a given change in interest rates can now be found

from:

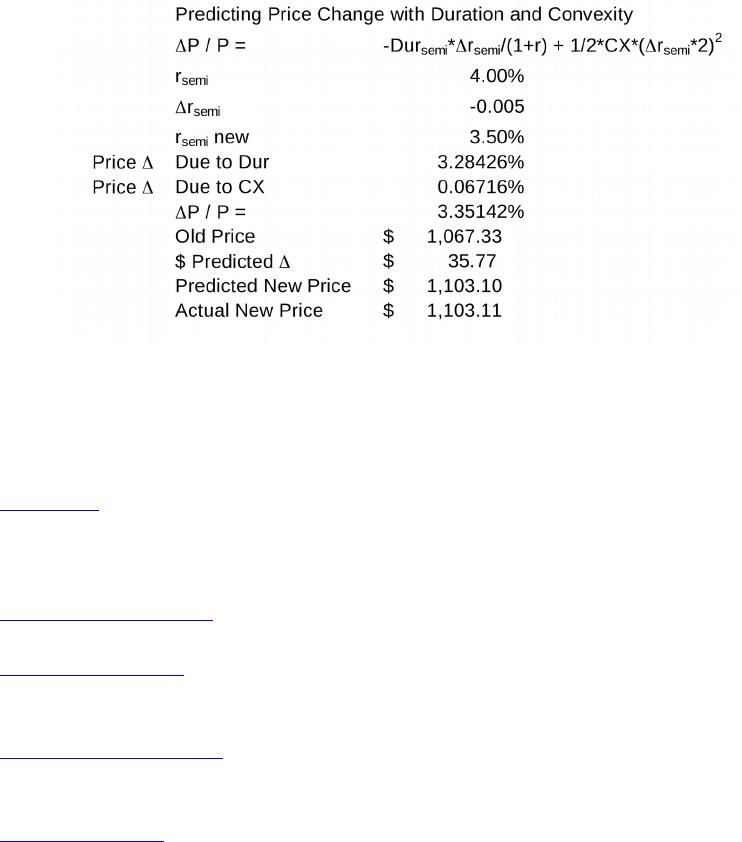

ΔP / P = -Dursemi*Δrsemi/(1+r) + 1/2*CX*(Δrsemi*2)2

where the first term is the price change based on duration and the second term adds the

correction needed due to convexity. An example is provided below:

Ch 3- 8

Chapter 03 – Security Valuation 6th Edition

With the convexity correction, there is only a negligible pricing prediction error.

Convexity increases with maturity and is inversely related to the coupon rate and

promised yield rates.

1.1.1.1 VI. Web Links

www.ft.com Financial Times, won two Espy awards for best new site

and best non U.S. news site. Coverage of global events and

markets.

www.americanbanker.com Website of the American Banker’s Association

www.bondsonline.com A bond oriented website with daily market commentary and

yield spreads

www.investinginbonds.com The Bond Market Association website has a wealth of

information for individual bond investors.

www.wsjonline.com Although not the best site for bond data the Markets Data

Center does have some key bond statistics

1.1.1.1.1.1 VI. Student Learning Activities

1. Using a spreadsheet construct a graph depicting how a bond’s price is affected by

interest rates for the following two annual payment corporate bonds:

Bond A: 5 year maturity, 12% coupon

Bond B: 25 year maturity, 6% coupon

Using whole number interest rates ranging from 4% to 15% calculate the associated

PVs and graph them. How do the two graphs differ? Why?

2. In number 1 above, if interest rates are initially at 8% and they increase to 8.5% what

is the predicted price change for each bond? What is the actual price change for

Ch 3- 9

Chapter 03 – Security Valuation 6th Edition

each? What is the error in the predicted price change for each bond? Why is the

error greater for one bond than the other? Do your answers differ if rates fall from

8% to 6.5%? Why or why not?

3. Go to the following website of the Bond Market Association: www.investinginbonds.com

and read in the section entitled, “Bond Basics,” under the “Learn More” tab the

subsection on fundamental investment strategies. Describe the four strategies found

there.

4. Go to www.alamocapital.com and describe the ‘bond of the day.’ What services are

available at this website?

5. Go to www.bondsonline.com and read the daily bond market commentary. Briefly

describe the major news events of the day.

6. Find the approximate spread between AAA and BBB rated bonds. Discuss why this

spread exists. If a AAA and a BBB rated bond have the same duration and convexity

will they have the same level of interest rate risk? Why or why not?

Ch 3- 10