1.1.1.1.1Chapter Three

Interest Rates and Security Valuation

1.1.1.2 I. Chapter Outline

1. Interest Rates as a Determinant of Financial Security Values: Chapter Overview

2. Various Interest Rate Measures

a. Coupon Rate

b. Required Rate of Return

c. Expected Rate of Return

d. Required versus Expected Rates of Return: The Role of Efficient Markets

e. Realized Rate of Return

3. Bond Valuation

a. Bond Valuation Formula Used to Calculate Fair Present Values

b. Bond Valuation Formula Used to Calculate Yield to Maturity

4. Equity Valuation

a. Zero Growth in Dividends

b. Constant Growth in Dividends

c. Supernormal (or Nonconstant) Growth in Dividends

5. Impact of Interest Rate Changes on Security Values

6. Impact of Maturity on Security Values

a. Maturity and Security Prices

b. Maturity and Security Price Sensitivity to Changes in Interest Rates

7. Impact of Coupon Rates on Security Values

a. Coupon Rate and Security Price

b. Coupon Rate and Security Price Sensitivity to Changes in Interest Rates

8. Duration

a. A Simple Illustration for Duration

b. A General Formula for Duration

c. Features of Duration

d. Economic Meaning of Duration

e. Large Interest Rate Changes and Duration

Appendix 3A: Duration and Immunization

Appendix 3B: More on Convexity (All appendices are available through McGraw-Hill’s

Connect. Contact your McGraw-Hill representative for more information on making the

appendix available to your students).

II. Learning Goals

1. Understand the differences in the required rate of return, the expected rate of return, and the

realized rate of return.

2. Calculate bond values.

3. Calculate equity values.

4. Appreciate how security prices are affected by interest rate changes.

5. Understand how the maturity and coupon rate on a security affect its price sensitivity to

interest rate changes.

6. Know what duration is.

7. Understand how maturity, yield to maturity, and coupon rate affect the duration of a security.

8. Understand the economic meaning of duration.

1.1.1.3 III. Chapter in Perspective

This is the second chapter that is designed to familiarize the students with the determinants of

fixed income valuation. This chapter has seven closely related sections which focus primarily on

bond pricing and the bond price formula. From the first three sections of the chapter readers

should learn how to calculate a bond’s price, the difference between the required rate of return,

the expected rate of return and the realized return and how to calculate each. Efficient markets

are briefly introduced by relating the expected and required rates of return and by comparing

market prices to calculated fair present values. Section 4 introduces bond price volatility and

illustrates how changing interest rates can affect FIs. Sections 5 and 6 discuss the effects of

maturity and coupon on bond price volatility. Section 7 introduces the concept of duration and

illustrates how to calculate Macauley’s duration. Appendix 3A provides an example of

immunization using duration and Appendix 3B demonstrates using the concept of convexity its

effect on bond price predictions.

1.1.1.4 IV. Key Concepts and Definitions to Communicate to Students

Required rate of return Price sensitivity

Expected rate of return Maturity and price sensitivity

Realized rate of return Coupon and price sensitivity

Coupon rate Duration

Market efficiency Elasticity

Zero coupon bonds Modified duration

Par, premium and discount bonds Convexity

Yield to maturity Fair present value

1.1.1.5 V. Teaching Notes

1. Interest Rates as a Determinant of Financial Security Values: Chapter Overview

This chapter applies the time value of money concepts developed in Chapter 2 to explain bond

pricing and rates of return. The determinants of bond price volatility, duration and convexity are

also discussed. Financial intermediaries are subject to risk from changing interest rates (termed

interest rate risk) because changing rates can cause changes in profit flows and in market values

of both assets and liabilities. This chapter provides the building blocks needed to understand

how to measure and manage interest rate risk.

2. Various Interest Rate Measures

a. Coupon Rate

b. Required Rate of Return

c. Expected Rate of Return

d. Required versus Expected Rates of Return: The Role of Efficient Markets

The bond’s coupon rate is the annual dollar coupon divided by the face value. Although the

coupon rate is quoted annually, bonds usually pay interest semiannually. If a bond has no

periodic interest payment it is a zero coupon bond. The required rate of return (r) is the

annual compound rate an investor feels they should earn on a bond given the risk level of the

investment. The r is used as the discount rate in the bond price formula to calculate the fair

present value (PV) of the security. The PV is then compared to the existing market price to

ascertain whether the security is over, under or correctly valued. The expected rate of return

(E(r)), or promised yield to maturity, is the annual compound rate of return the investor can

expect to earn if he/she 1) buys the bond at the current market price, 2) holds the bond to

maturity and 3) reinvests each coupon for the remaining time to maturity and earns the E(r) on

each coupon. The E(r) may be calculated using the current market price as the present value and

the expected cash flows in the bond price formula. Note that this definition of the E(r) assumes

that either there is no possibility of default risk, or the expected cash flows used in the bond price

formula are probability weighted according to the expected probability of default. If the E(r) is

greater than the r, the security is overvalued. If the bond markets are efficient any divergences

between the market price and the PV (or the r and E(r)) are quickly arbitraged away.

Calculating PV:

For a $90 annual payment coupon corporate bond (INT = $90, with r = 10% maturing in n = 6

years:

6

6

)10.1(

1000$

10.0

)10.1(

1

1

90$45.956$

If this same bond has an actual market price of $945, what is the E(r)?

6

6

))r(E1(

1000$

)r(E

))r(E1(

1

1

90$945$

E(r) = 10.27%

This bond would be a good buy since the market price is less than the fair PV. If the appropriate

opportunity cost (r) is 10%, the investor can expect to earn more than he or she should (10.27%)

for the risk level the investor is bearing.

Teaching Tip:

Equation 1

Equation 2

n

n

r

Par

r

r

INTPV

)1(

)1(

1

1

The third assumption underlying the investor’s expectation of earning the E(r) is that the coupons

have to be reinvested at the E(r). Students may become confused over this point. For instance, if

you buy a $1,000, 8% coupon bond at par and receive $80 per year, that appears to be an 8%

annual return regardless of what the investor does with the money. It is in fact an 8% simple

interest return, but not an 8% annual compound return. This concept can be easily

demonstrated. If you invest $1,000 for 5 years and expect to earn an 8% compound rate of return

per year, at the end of five years you must have a pool of assets worth $1,000 1.085 =

$1,469.33. If you stash the cash in the mattress and do not reinvest any coupons you will have

only ($80 5) + $1,000 = $1,400 at the end of five years and your realized annual rate of return

will be 6.96%. Likewise, at any reinvestment rate less than 8%, you will wind up with less than

$1,469.33 and have less than an 8% realized return. (See Gardner, Mills and Cooperman,

Managing Financial Institutions: An Asset/Liability Approach 4th ed. Dryden Press, 2000.)

Teaching Tip:

The current yield is the annual dollar coupon divided by the bond’s closing price. It is akin to the

dividend yield on the stock and it measures the simple interest annual rate of return if you do not

sell the bond. For bond investors who use a buy and hold strategy and spend the coupons, (the

prototypical grandmother living off the coupon income for example) the current yield is a better

measure of the annual rate of return they are earning than the promised yield to maturity.

Students though tend to be confused by the term ‘current yield.’ On a test at least some are liable

to think this means the current promised yield to maturity.

Teaching Tip:

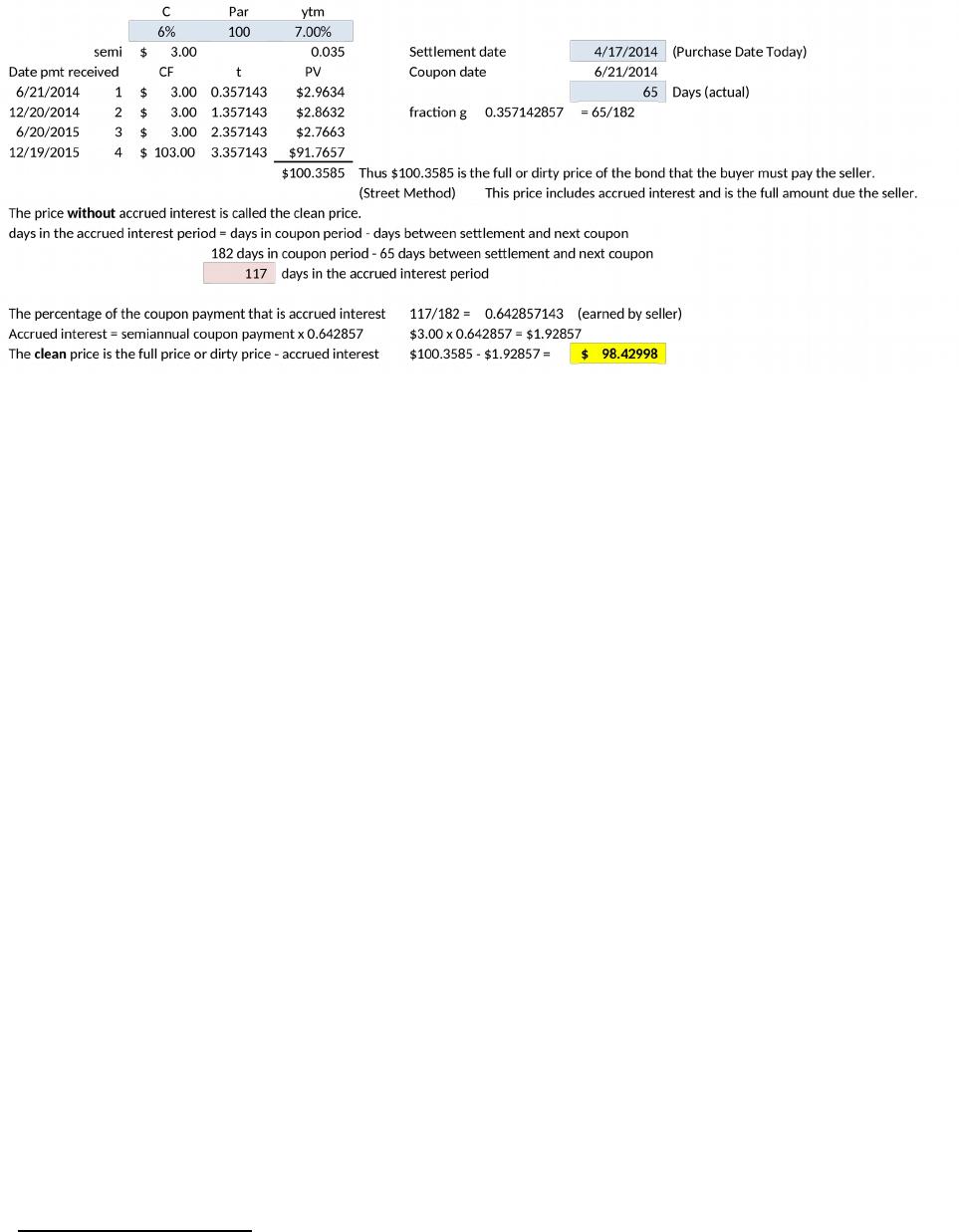

The price calculations in the text are ‘clean’ prices, not ‘dirty’ prices. That is, they do not include

accrued interest. To value a bond between payment dates first calculate the fraction g of time

between the settlement date and the next coupon payment date from the following: g = days

between settlement and next coupon payment / days in coupon period.1 Treasuries use the actual

day count in this calculation while corporates and munis use 30 days for all months (and 360

days in the year). The calculated present value a bond buyer must pay is tCFt/(1+r)(t-1+g) where t

is an integer representing each subsequent cash flow. This value is called the ‘dirty’ price, the

full price or the invoice price. The amount of accrued interest (AI) = semiannual coupon(1-g).

The bond’s clean price without accrued interest is the full price minus accrued interest. See the

example below.

Bond pricing example between coupon payment dates example for a 4 payment 6% coupon, 7%

yield Treasury bond with semiannual payments with a settlement date on April 17, 2014 and the

next coupon payment date on June 21, 2014:

1 This method is not in the text and it is drawn from Fabozzi, F., Fixed Income Analysis, 2nd Edition, 2007, Chapter

5.

e. Realized Rate of Return

The realized rate of return (

´r

) is the rate of return actually earned over the investment

period. It can be above or below the E(r) and the

´r

and can be negative. The text uses a

naïve method to calculate the

´r

is to find the interest rate using the realized cash flows in the

bond price formula. If the investor knows the actual reinvestment rate on the coupons the

modified internal rate of return (MIRR) method should be used to calculate the realized rate of

return.2 For example, suppose an investor buys a par bond at 6% and holds it for three years

before selling it at $1,050. However, each $60 coupon was actually reinvested at an interest rate

of 5%. Solving the bond price formula gives an

´r

of 7.55%. The future value of the three

$60 coupons is actually $189.15, so the actual future value of all the cash inflows is $1,050 +

$189.15 = $1,239.15. With a $1,000 initial investment, the actual rate of return is 7.41%, much

less than the solution implied by the bond price formula. Anytime you solve the bond price

formula for the discount rate you are implicitly assuming the cash flows were reinvested at that

discount rate. Only by coincidence will this be correct. Only if you have no other information

about the reinvestment rate is solving the bond price formula to find the realized rate of return

reasonable. Ex-post, one should know the reinvestment rate; ex-ante, one should use the term

structure to estimate the expected reinvestment rate.

3. Bond Valuation

a. Bond Valuation Formula Used to Calculate Fair Present Values

To calculate the PV of a bond with semi-annual compounding, divide the coupon rate and the r

by two and multiply the number of periods by two. Note that the r (or promised yield) is an

APR for bonds that pay interest semi-annually. The effective annual return for the bond is

larger than the bond’s APR.

For the same bond used above, the PV with semiannual compounding would be:

INT = 90 per year, r = 10%, n = 6 years, m = 2 compounding periods per year}

2 The MIRR method is not in the text.

Premium bonds are priced above par, discount bonds are priced below par.

Teaching Tip: If a fixed income bond is paying a 12% coupon and has a 10% required (and

expected) rate of return, the only way the investor will earn less than the coupon rate in a given

year is if they have a capital loss to offset the extra 2% interest they are earning. This tells us

that when the coupon rate is above the r the bond is selling at a premium to par and that this

premium disappears as maturity approaches. Likewise, a bond paying only an 8% coupon that

has a 9% required yield must be selling below its redemption value (discount bond), and must be

expected to increase in price as maturity approaches because this is the only way one can expect

to get the 8% interest yield up to a 9% total rate of return. If the bond’s coupon rate and required

rate are equal, the price will equal par regardless of maturity because the entire rate of return is

received through the coupon and no price adjustment is needed.

Example:

A bond’s return (r) consists of the sum of two components:

1. Receiving (and reinvesting) the coupon payment

2. Capital gain or loss on the bond’s value

Both are measured in relation to the purchase price of the bond. Ignoring any reinvestment on

the coupon, a bond’s one year holding period return is the sum of the current yield and

percentage price change of the bond.

Premium bond pricing and annual return:

If a semiannual payment bond has a 15 year maturity with a 6% coupon and a 4% ytm the bond’s

price is $1,223.96. The same bond with a 14 year maturity should have a price of $1,212.81.

Ignoring any reinvestment income from the semiannual coupon, the bond’s current yield is

$60/$1,223.96 = 4.90%. The percentage change in the price of the bond is -0.90%. The total

annual holding period return is 4.90% + -0.90% = 4.00%. Since the investor is supposed to earn

4% and the yield from the coupon is higher than this amount the investor must have a capital loss

of 0.90% to offset the high coupon.

Discount bond pricing and annual return:

If a semiannual payment bond has a 15 year maturity with a 6% coupon and an 8% ytm the

bond’s price is $827.08. The same bond with a 14 year maturity should have a price of $833.37.

Ignoring any reinvestment income from the semiannual coupon, the bond’s current yield is

Equation 3

mn

m n

(r/m))(1

Par

r/m

(r/m))(1

1

1

INT/cPV

12

12

(1.05)

$1000

0.05

(1.05)

1

1

$45$955.68

$60/$827.08 = 7.25%. The percentage change in the price of the bond is -0.75%. The total

annual holding period return is 7.25% + 0.75% = 8.00%. Since the investor is supposed to earn

8% and the yield from the coupon is only 7.25% the investor must have a capital gain of 0.75%

to offset the low coupon.

Bonds are priced at par if the coupon is equal to the yield because the yield rom earning the

coupon equals the required return on the bond so no price change is required to provide the

investor with the necessary return.

Pull to par:

Bond prices approach par as a bond approaches maturity. Premium bonds approach par from

above and discount bonds from below. This is termed the ‘pull to par.’

Teaching Tip: The normal annual discount or premium amortization due to approaching maturity

is taxed as ordinary income (loss), not as a capital gain or loss.

b. Bond Valuation Formula Used to Calculate Yield to Maturity

Assuming away default risk and noting the reinvestment assumption above, this is the same as

calculating the bond’s required rate of return using the bond price formula. It cannot be solved

algebraically in the multiperiod case, but most business calculators are preprogrammed to find

the promised yield. Note that on the Hewlett-Packard and Texas Instrument business calculators

either the left hand side or all of the right hand side of the bond price formula must be negative.

A common mistake students make is to enter only part of the right hand side as negative (either

the coupon or the future value, but not both.).

4. Equity Valuation Models

The text presents the zero growth, the constant growth and the two stage dividend discount

growth models for equities.

P = D / rs in the zero growth case (Dt = Dividend in time t)

P = D1 / (rs – g) in the constant growth case and

n

s

s

n

n

tt

s

t

r

gr

D

r

D

P

)1(

)(

)1(

2

1

1

for the two stage growth model where D1 to Dt must be estimated,

using individual growth rates or an average growth rate g1, and g2 is the long term steady state

growth rate that applies from time n through .

5. Impact of Interest Rate Changes on Security Values

Open market interest rates fluctuate daily due to the actions of traders. Buying, selling and

issuing securities all affect interest rates, which in turn affect security prices. Mathematically, as

required rates rise, PVs fall since the required rate is in the denominator of the bond price

formula. Conceptually, the actions of traders force market prices to act in similar fashion. If you

are holding a bond expected to yield 10% and identical new bonds are issued that pay 12%, you

are not happy! Enough traders begin to sell the low yield bond so that its price begins to fall and

at the lower price its yield rate rises. This continues until the yield rate moves to 12%. Hence,

prices and interest rates move inversely. Since the cash flows are discounted at a compound rate

of return (rates raised to an exponent) the bond price is not linear with respect to interest rates.

Take the same bond above and let the r rise to 11%

The new PV is

12

12

)055.1(

1000$

055.0

)055.1(

1

1

45$81.913$

This is a drop in PV of $41.87 (=$955.68 – $913.81). A financial intermediary (FI) primarily

holds financial assets (such as loans and bonds) and financial liabilities. Consequently the FI

must manage the relative price changes of its financial assets and liabilities. If interest rates rise

and the PV of the assets fall by more than the PV of their liabilities, the PV of the equity will

decline. Because most FIs employ very large amounts of leverage and little equity, an institution

that fails to manage its interest rate risk can quickly face insolvency due to unfavorable interest

rate moves.

6. Impact of Maturity on Security Values

a. Maturity and Security Prices

Fixed income security prices approach par as maturity nears (the so called ‘pull to par’) even if

interest rates don’t change. The discount or premium on non par bonds decreases slightly each

year.

b. Maturity and Security Price Sensitivity to Changes in Interest Rates

Price sensitivity or price volatility is the percentage change in a bond’s price for a given current

change in interest rates. Note the specificity of this definition. Students will often think that a

longer term bond is more price volatile because over a longer time period rates are more likely to

change. Their logic is correct but this belies the definition. Price sensitivity measures how much

a bond’s price will change if rates change right now. Longer term bonds are more price sensitive

because the current worth of distant cash flows is very sensitive to the discount rate. The price

sensitivity increases at a decreasing rate, so a twenty year bond is not twice as price sensitive as a

ten year bond. See IM Figure 3.1 below from an Excel spreadsheet:

IM Figure 3.1 illustrates the limit of the price change for a given coupon rate and a yield rate

increase of 50 basis points for bonds of different maturity. Notice that as maturity is increased

from 1 to 5 to 10 years, the price volatility increase is quite large on a percentage basis.

However as maturity is increased beyond 30 years there are only small increases in price

volatility.3 At the limit, the price change is equal to 1 – (rold / rnew). This limit formula is correct

for all coupon paying bonds, with higher coupon bonds reaching the limit more quickly, and low

coupon bonds reaching the limit price change much more slowly.

Teaching Tip: Extreme examples often help to illustrate a concept. For example, if you are

holding a 5% coupon bond that you can’t get rid of for 30 years and suddenly rates rise from 5%

to 10%, you might expect that you and other investors in the bond are not very happy and its

price will drop a large amount. However, if the bond matures tomorrow, would you expect its

price to move much?

Teaching Tip: Any security that pays more money back sooner, ceteris paribus, will be less price

volatile. Specifically, the value of any security that returns a greater percentage of the initial

investment sooner will be less sensitive to interest rate changes. Text Tables 3-7 through 3-10 can

be used to illustrate this simple concept for different coupons and different maturity.

3As maturity increases the bond price formula converges to the present value of a perpetuity where PV = $ Coupon /

r. This allows one to develop the predicted limit price change as (C/rnew / C/rold) – 1.