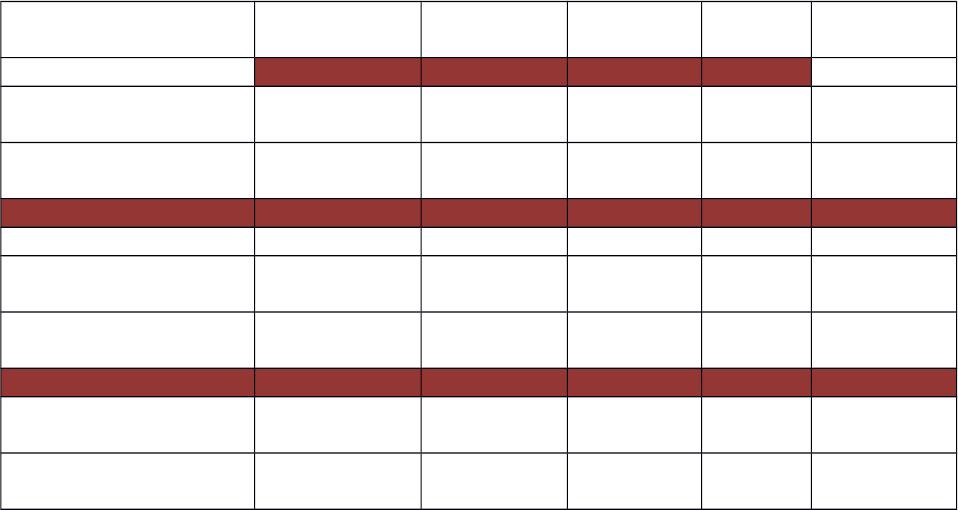

. Comparison of Hedging Methods

Table of Exposures and Methods of Hedging

Interest Rate Exposure Risk

Futures/

Forwards

Call/Put

Options

Caps &

Floors Swaps

Macrohedges Side to Pay:

+ Repricing gap or

– Duration Gap Falling rates Long Call Floor Variable

– Repricing gap or

+ Duration Gap Rising rates Short Put Cap Fixed

Microhedges

Long security or future

commitment to sell Falling prices Short Put na na

Short security or future

commitment to buy Rising prices Long Call na Na

Total Return

Swaps

Pure Credit

Swaps

Credit exposure from

loans or investments

Deteriorating

credit quality Buy Buy

a. Writing versus Buying Options

Writing options is riskier than buying options because hedges with written option positions

generally offer limited gains and unlimited losses, whereas hedges involving purchased options

offer limited losses and unlimited gains.

b. Futures versus Options Hedging

Futures hedges typically place an absolute ceiling on both gains and losses, whereas options

hedges can limit downside loss while allowing the hedger to enjoy large gains if prices move

favorably. As you might expect, hedging with options will normally involve more outright or

out of pocket costs than hedging with futures because the option buyer is purchasing a right

which can be used if it is profitable, rather than committing to a future purchase or sale.

Teaching Tip: The tradeoffs are largely due to differences in out of pocket costs and opportunity

costs plus the effects of marking to market on futures. With options there are greater up front out

of pocket costs. Options are less frequently used for hedging because many managers feel they

are too costly. Futures have less up front out of pocket costs, but may require bridge financing to

cover marking to market and because futures are a commitment they have larger opportunity

costs. Managers overcome these by partially hedging and actively trading. I don’t have hard

data but I believe that futures trading costs for institutions are also less than for trading options.

Both can have similar high leverage ratios. Leverage reduces the cost of hedging because the

hedger has lower costs to hedge with a higher leverage ratio.

c. Swaps versus Forwards, Futures, and Options

Swaps and forwards are OTC custom contracts with fully flexible terms. Futures and listed

options are highly standardized and have only limited maturities available. One of the big

advantages of swaps is their potentially long maturity. Some last 20 years or more, thus swaps

allow longer term hedging than is available with any other contract. OTC options are available

that are more flexible and may have longer maturities than listed options and futures.1 Futures

are marked to market daily and may require a hedger to put up more cash before realizing

offsetting gains in the cash market. This can distort near term earnings and may cause concern to

upper level FI managers (particularly to those that do not fully understand the hedging program).

Futures and listed options have little or no default risk. Forwards and swaps may involve

significant counterparty risk unless a third party guarantees performance. Finally, futures and

options contracts are more liquid than forwards and swaps.

1.1.1.1 Appendix 23A: Hedging With Futures Contracts (available in Connect or

from your McGraw-Hill representative)

The reader should be comfortable with the material presented in Chapter 3, Chapter 10, and both

Chapters 22 and 23 before attempting the appendices and supplement.

a. Microhedging with Futures

The number of futures contracts (NF)

From Chapter 3: (D = Duration)

F/F = -DF (RF/(1+RF)) or

F = -DF F (RF/(1+RF)) F = Total futures value F = dollar change in F

P = -DP P (R/(1+R)) P = Market value of the instrument to be hedged

If P is fully hedged then F = P, the dollar change in F offsets any dollar change in P, or

substituting from above:

-DF F (RF / (1+RF)) = -DP P (R/(1+R))

Assuming that RF / (1+RF) R / (1+R)

-DF F = -DP P

F = NF PFWhere PF = the price per contract

Substituting this in:

-DF NF PF = -DP P or

NF = (-DP / -DF) (P / PF)

Teaching Tip: The concept of NF is easy to understand as mentioned above in Section 2b. The

number of contracts needed to hedge a position is calculated as a function of two factors: 1) the

size of the cash position relative to the futures contract size (P / PF) and 2) the price volatility of

the spot relative to the price volatility of the futures contract (-DP / -DF). The larger the cash

position relative to the quantity specified for delivery in the futures contract, the greater the

number of contracts required to hedge. The greater the price volatility of the spot relative to the

1 Exchanges are concerned about trading volume because that is how they profit from a contract

and long term contracts almost always have significantly lower trading volume, limiting their

desirability for exchanges.

price volatility of the underlying futures commodity with respect to interest rates, the larger the

number of contracts needed to hedge.

Example 5:

A bank has a long position in $500,000 face value 11.03% yield Treasury Bonds that have a

duration of 11 years. The bank is concerned about rising interest rates between now and August.

The bonds have a price quote of 91 1/32 or $455,156. T-Bond futures contracts call for the

delivery of $100,000 face value of Treasury Bonds. The September contract (the nearest to

August) has a price quote of 89 (or $89,000) and the underlying T-bonds to be delivered have a 7

year duration and a 9.397% yield.2 How many futures contracts are needed to fully hedge the

position?3

NF = (-11 / -7) ($455,156 / $89,000) = 8.036 or 8 contracts should be sold. Always round the

number of contracts down, because hedging efficiency is improved if one slightly underhedges

rather than overhedges.

If prices move according to the duration predictions (convexity notwithstanding) then the hedge

should prevent large gains or losses from occurring for normal interest rate movements. For

instance if rates rise 50 basis points:

F = PF NF = – 7 (0.0050 / 1.09397) $89,000 = $2,847.43 gain per contract 8 contracts

= $22,779.42.

The price of the futures contract drops, but a drop in price makes money for a short position in

futures.

The predicted change in the spot value is

P = – 11 (0.0050 / 1.1103) $455,156 = -$22,546.68

The predicted net gain or loss is the difference or $232.74.

b. Macrohedging With Futures

A macrohedge is normally designed to immunize the equity value with respect to interest rate

changes. I.E. we desire E = 0. From Chapter 22,

E = – [DA – kDL] A (R / (1+R))

F = – DF NF PF (RF / (1+RF)) Setting E = F and if the interest rates and rate changes

are the same:

– [DA – kDL] A = -DF NF PF Solving for NF yields:

2T-bond futures contracts are priced according to the cheapest to deliver bond. The deliverable

bond must have at least a 15 year time to first possible call or maturity, and is priced as if it were

an 8% coupon bond. I used these terms to arrive at the yield price combination on the futures

contract.

3In this case RF does not equal R but R = RF. Omitting the (1+R) and (1+RF) terms usually

does not materially affect the hedge. If the change in rates is not likely to be similar between the

cash and futures instrument (as in a cross hedge), then one should include the different rate

changes. For instance, RF may be characterized as an expected percentage of R based on

regression analysis of historical changes of the two rates.

FF

LA

F

PD

AkDD

N

Example 6:

Suppose a $500 million bank has an average asset duration of 3 years and an average liability

duration of 1 year (See Chapter 23 of the IM for this example). The bank also has a total debt

ratio of 90%. If R is 12% and the bank is expecting a 50 basis point increase in interest rates,

how many T-bond futures contracts are required to fully hedge the equity value if the Treasury

bond futures terms are the same as in Example 5?

Expected E from the rate change is – [3 – (0.901)] $500 million (0.0050 / 1.12) =

–$4,687,500.

39.685,1

000,89$7

Million500$)190.0(3

N

F

Or the FI should sell 1,685 contracts.

If interest rates increase 50 basis points and prices move according to duration predictions then

the gain on the futures position will be:

F = PF NF = – 7 (0.0050 / 1.09397) $89,000 = $2,847.43 gain per contract 1,685

contracts = $4,797,920

As before the price of the futures contract drops, but a drop in price makes money for a short

position in futures. The net gain (loss) is $4,797,920 – $4,687,500 = $110,420.

1.1.1.2

1.1.1.3 Appendix 23B: Hedging with Options (available in Connect or from your

McGraw-Hill representative)

This supplement examines hedges with purchased options, not written options for the reasons

discussed in the chapter.

Let O = the total dollar change in the value of an option position and then O = (NO o)

where NO = the number of option contracts and o equals the dollar value change per contract.

For a Treasury bond contract let B = market value of the underlying T-bonds ($100,000 face

value).

B

B

R

R

B

B

o

o

Appendix Equation 2

o / B = the option’s delta (see Chapter 10). It is in the range 0 to +1 for a call option and 0 to

–1 for a put option. It is literally N(d1) from the Black-Scholes model and measures the change

in option value per dollar change in the underlying bond price. Write the delta as . Rather than

differentiate between the hedging equations for puts and calls, it is simpler to remember that the

delta is positive for a call and negative for a put.

B / RB = the change in the underlying bond price per 1 basis point change in interest rates.

This is equal to [-DurB / (1+RB)] B. (Note that DurB / (1+RB) is sometimes called the ‘modified

duration’ or MD for short so B / RB = -MD B.)

In words, the first component measures the change in option value per dollar change in the

underlying bond’s price, the second term measures the underlying bond’s price response to an

interest rate change, and the third term measures the size of the interest rate change.

Rewriting Equation 2

B

B

BB

B

B

R

R

xBDurRB

R

Dur

o

11

Appendix Equation 6

Recall that N0 = total number of option contracts purchased and then the total dollar change in

option value O = NO x o.

To hedge O must equal Spot.

Spot

R

R

DurSpot

Spot

Spot

Spot

1

Equation A

Setting Spot = O, letting br =

)Spot

Spot

B

R(

R

)R(

R

1

1

B

and solving for NO:4

brBDur

SpotDur

N

B

Spot

O

Appendix Equation 13

Example 7: (Continuation of Example 5)

A bank has a long spot position in $500,000 face value 11.03% yield Treasury Bonds that have a

duration of 11 years. The bank’s managers are concerned about rising interest rates between now

and August. The bonds have a price quote of 91 1/32 or $455,156. September put options on

T-bond futures are available with an exercise price of $90 per $100 of face value. The

September options (the nearest to August) have a premium of $1.625 per $100 of face value and

the put option delta is –0.52. The contracts are for $100,000 face value T-bonds. The underlying

T-bonds to be delivered have a 7 year duration and a 9.397% yield for an $89,000 price. How

many put option contracts are needed to fully hedge the position?

4 For a macro hedge the numerator to Equation 13 will be (DurA – k DurL) x A. See Appendix

Equation 8.

NO =

contracts 15.22

1.01493$89,00070.52

$455,15611

or 15 put contracts should be purchased. The

total cost of the contracts is 15 $1.625 $100,000 / $100 = $24,375 or 5.35% of the market

value of the bonds.

If prices move according to the duration and delta predictions, then the hedge should prevent

large gains or losses from occurring for normal interest rate movements. For instance if rates

increase 50 basis points:

O = o No = 0.52 – 7 (0.0050 / 1.09397) $89,000 = $1,480.66 gain per contract 15

contracts = $22,210.

As before Spot = – 11 (0.0050 / 1.1103) $455,156 = -$22,547.

The net difference in this case, is -$337 excluding the put premiums. The net loss including the

premiums is -$24,375 + -$337 = -$24,712. Recall that option outcomes are not symmetric, if the

bond price increases the puts will expire worthless but the gain in bond prices may outweigh the

put premiums. You may wish to have the students calculate the breakeven point as an exercise.

The breakeven would occur when prices have risen $24,375 if the puts had been exactly at the

money.

Basis risk: On a direct hedge basis risk can probably be safely ignored. The correction for basis

risk is the term br and it may be omitted for a direct hedge.

Appendix 23C: Hedging with Caps, Floors, and Collars (available on Connect or from your

McGraw-Hill representative)

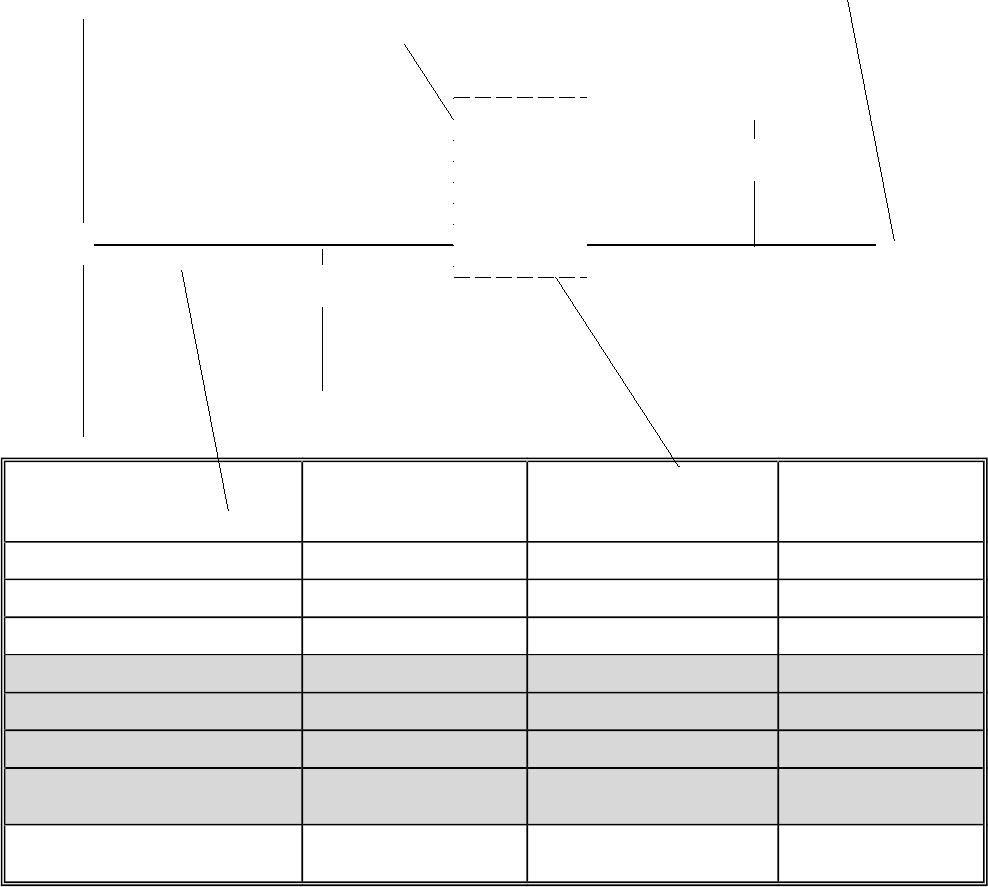

An FI has the following balance sheet categorized over a 2 year planning period:

Assets

Amount

(Mill $)

Liabilities

& Equity

Amount

(Mill $)

RSAs @ 5% $ 50 RSLs @ 4% $100

FRAs @ 6% $350 FRLs @ 5% $300

NEA $ 60 Equity $ 60

Total $460 Total $460

Current Profitability Amount Spread Profitability

RSAs financed by RSLs $ 50 1% $0.5

FRAs financed by FRLS $300 1% $ 3

FRAs financed by RSLs $ 50 2% $ 1

$400 Total $4.5

Since the category NEA financed by equity has a zero spread

and does not contribute to profitability it can be omitted.

Profitability after rate

increase Amount Spread Profitability

RSAs financed by RSLs $ 50 1% $0.5

FRAs financed by FRLS $300 1% $ 3

FRAs financed by RSLs $ 50 1% $0.5

$400 Total $4.0

The FI has a 1% spread on rate sensitive and fixed rate assets, but the FI has a negative repricing

gap of $50 million and is thus at risk from rising interest rates.5 This FI could purchase a 2 year

cap with a cap rate of 4.5% with a notional principal that matches the bank’s gap of $50 million

with payments made annually. The cap may cost the FI $5,000. Let interest rates increase such

that that all RS rates increase 100 basis points. The FI would then receive the difference between

5.5% and the cap rate of 4.5%. In other words the FI would receive 1% * $50 million =

$500,000.

Profitability after rate

increase with Cap Amount Spread Profitability

RSAs financed by RSLs $ 50 1% $0.5

FRAs financed by FRLS $300 1% $ 3

FRAs financed by RSLs $ 50 1% $0.5

$400 Total $4.0

Cap $50 1% $0.5

Total w/ Cap* $4.5

* Ignoring the cost of the cap

The cap protects the FI’s profits from an increase in interest rates for two years with payments

made each year. Note that the hedge is not perfect, particularly if the rate sensitive accounts

reprice more frequently than once a year. A floor would work similarly for an institution at risk

from falling interest rates. The FI may wish to sell a floor to defer some of the costs of

purchasing the cap.

Collars:

The above FI may wish to hedge with a cap, but feels that the cost of the cap is too high. The FI

could then also sell a floor with a lower interest rate of say 4%. To simplify, assume that the cap

and floor are for one year and have only a payment at maturity. In this case the FI’s profit

diagram, including the on balance sheet changes, would be as follows:

5 Recall that in this case the FI has $50 million in FRAs financed by RSLs.

Profit

1.1.2 Profit Table at Time

T when the options

expire in one year IT < EFloor EFloor < IT < ECap 1.1.3 IT > ECap

NP*(FRA – RSLT) NP*(FRA – RSLT) NP*(FRA – RSLT) NP*(FRA – RSLT)

-NP*(FRA – RSL0) -NP*(FRA – RSL0) -NP*(FRA – RSL0) -NP*(FRA – RSL0)

-C0-C0-C0-C0

+F0+F0+F0+F0

+CT 0 0 NP*(RSLT – Cap)

-FT -NP*(Floor -RSLT) 0 0

= Profit

-C0+F0 +

NP*(RSL0 – Floor)

-C0+F0 +

NP*(RSL0 – RSLT)

-C0+F0 +

NP*(RSL0 – Cap)

Breakeven

F0 – C0

=NP*(RSL0-RSLT)

NP = Notional principal, assumed the same for the gap and the options, Ct and Ft represent the value of

the cap and floor at time t respectively. T = 1 year, 0 = today. E = exercise rate

1.1.3.1 Supplement: Hedging with Swaps

c. Macrohedging with Swaps

To protect the value of equity the swap should be designed to yield a gain equal to E (the

change in equity value) if interest rates change. The swap is a negotiated contract so that the

duration of the fixed and variable sides of the contract can be constructed as needed. Likewise

the notional principal is negotiable. The swap designer is limited only by the ability to attract a

counterparty willing to enter into the deal. It is also only necessary to manage the net duration of

the swap. The swap duration to a fixed rate payer is equal to the duration of the variable

payments minus the duration of the fixed payments. The converse is true for the variable rate

payer. Nevertheless it is convenient to solve for the optimal notional principal for a given

duration of the fixed and variable sides of the swap. Note that the duration of the variable

EFloor

St

E

$0

ECap

F0 – C0 =

NP*(RSL0–

RSLT)

payments (or floating payments) is simply the time until the payments are reset.

The optimal notional principal of the swap NS can be found as:

NS = [(DA – kDL)A] / [Dfixed – Dfloating] where Dfixed is equal to the duration of the fixed payments

and Dfloating is equal to the duration of the floating or variable payments.

Example 8: Continuation of Example 6

Suppose a $500 million bank has an average asset duration of 3 years and an average liability

duration of 1 year. The bank also has a total debt ratio of 90%. R is 12% and the bank is

expecting a 50 basis point increase in interest rates.6 The FI can enter into a swap where the

duration of the fixed rate payments is 6 years and the duration of the variable rate payments is 1

year. What is the optimal notional principal of the swap that immunizes the equity value? Does

the FI make or receive the fixed rate payments?

NS = [(3 – (0.91))$500 million] / [6 – 1] = $210 million. The FI has a positive leverage

weighted duration gap so it has longer duration assets than liabilities. To reduce the duration gap

the FI would pay fixed (effectively extending the liability duration) and receive variable

(effectively shortening the asset duration).

d. Fixed Floating Currency Swaps

Example 9:

A Japanese FI has made variable rate dollar denominated loans to Taiwanese borrowers.

The loans are funded by fixed rate yen deposits. The Japanese FI is at risk from dropping

Eurodollar interest rates and from a depreciating dollar.

A U.S. bank has made fixed rate yen loans to multinationals operating in the Far East, but

these loans are funded by variable rate dollar deposits. The U.S. bank is at risk from

rising U.S. interest rates and from a depreciating yen (appreciating dollar).

The two institutions can design a swap that limits the risk of both parties. Separate the

risks and handle them individually when faced with more complex swap arrangements.7

The Japanese FI faces interest rate risk from falling interest rates. They have too many variable

rate assets so the Japanese FI will pay a variable rate of interest in exchange for receiving a fixed

rate of interest.

The U.S. FI faces interest rate risk from rising interest rates. They have too many fixed rate

assets so the U.S. FI will pay a fixed rate of interest in exchange for receiving a variable rate of

interest.

The Japanese FI faces currency risk from a depreciating dollar as this will reduce the yen value

of repayments made by the Taiwanese borrowers. The Japanese FI will thus pay dollars in

6 R may be thought of as either the average rate or return on assets and liabilities or as the return

on equity.

7This assumes the risks are not hedged elsewhere. There is also an implicit assumption that the

swap deal is the cheapest source of hedging the risk. On balance sheet hedges (called money

market hedges) could also be used. The Japanese FI could borrow dollars at a variable rate and

directly hedge the risk. The size and popularity of the swap market indicates that swaps are often

the cheapest method of reducing the risk.

exchange for receiving yen. The yen received will be used to pay off its fixed rate yen

depositors.

The U.S. FI faces currency risk from an appreciating dollar (depreciating yen) as this will reduce

the dollar value of the yen repayments made by the multinational borrowers. The U.S. FI will

thus pay yen in exchange for receiving dollars.

Putting it together is now simple in concept:

The Japanese FI will pay dollars at a variable rate of interest in exchange for receiving

yen at a fixed rate of interest.

The U.S. FI will pay yen at a fixed rate of interest in exchange for receiving dollars at a

variable rate of interest.

1.1.3.2 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal Reserve

http://www.fdic.gov/ The Federal Deposit Insurance Corporation website has net

charge off rates for banks and thrifts.

http://www.occ.treas.gov/ Office of Comptroller of the Currency

http://www.cmegroup.com/ Chicago Mercantile Exchange Group (website of both

CME and CBOT since the merger)

http://www.bis.org/ Bank of International Settlements website. The BIS

collects data about derivatives usage and promulgates risk

based capital requirements including requirements for

derivatives usage.

http://www.isda.org/ International Swaps and Derivatives Association is a global

trade association for the derivatives industry.

http://www.economist.com/ The Economist, an excellent current event magazine

covering international business, politics, finance and

economics. Excellent source of context about countries

and regions of the world.

http://www.fasb.org/ FASB webpage

http://www.americanbanker.com/ ABA website

http://www.wsj.com/ Website of the Wall Street Journal Interactive edition. The

web version of the well known financial newspaper can be

personalized to meet your own needs. Instructors can also

receive via e-mail current events cases keyed to financial

market news complete with discussion questions.

1.1.3.2.1.1 VII. Student Learning Activities

1. Research the failure of the so called hedge fund, Long Term Capital Management.

An excellent video on LTCM titled “Trillion Dollar Bet” is available from WGBH Boston

Video (the video may also be seen from time to time on PBS Television). Was LTCM a hedge

fund? Why or why not? What was the problem with their hedging strategy? Does hedging

reduce risk to the extent that textbook examples imply? Why or why not?

2. Go to the CME group website and read the introduction to financial futures. What are

the specific contract terms for the T-bond contract? What is meant by the ‘cheapest to deliver’

bond? How does one determine which bond is cheapest to deliver? What are the ‘adjusted

futures price’ and the ‘adjusted cash price?’

3. Go to the FDIC website and calculate each of the following ratios (you will have to

examine several tables):

For interest rate contracts

Notional value of interest rate swaps / Gross Loans for all banks and the largest and

smallest bank categories

Futures and forward contracts / Gross Loans for all banks and the largest and smallest

bank categories

Purchased options / Gross Loans for all banks and the largest and smallest bank

categories

Written options / Gross Loans for all banks and the largest and smallest bank categories

Explain what the numbers mean and the differences among the different size banks.

4. How does the Dodd-Frank 2010 Act affect over the counter derivatives? Research the

bill and summarize the main changes that affect deriv