BT

Call

Prot

1. Options

a. Basic Features of Options (See Chapter 10 for details)

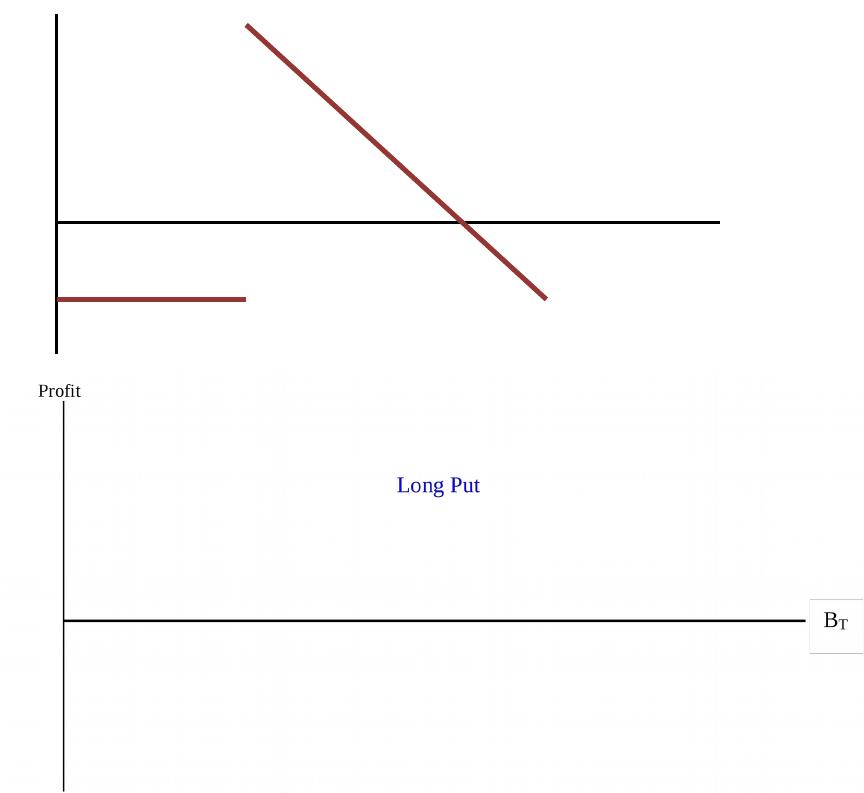

Buying options: A call option on a bond gives the holder gains if interest rates fall. Thus

buying bond calls is a useful hedge against falling rates. A put option on a bond gives the put

holder gains if interest rates rise and prices fall. Thus buying bond puts can hedge rising interest

rates. Recall that options differ from forwards and futures in that the holder has the right, but not

the obligation, to buy or sell the commodity at a set price. This right causes the asymmetric

nature of option hedge outcomes.

At expiration profit diagram of a long bond call and put option respectively:

The maximum loss is the call or put premium respectively. The call makes money when bond

prices rise (interest rates fall). The put makes money when bond prices fall (interest rates rise).

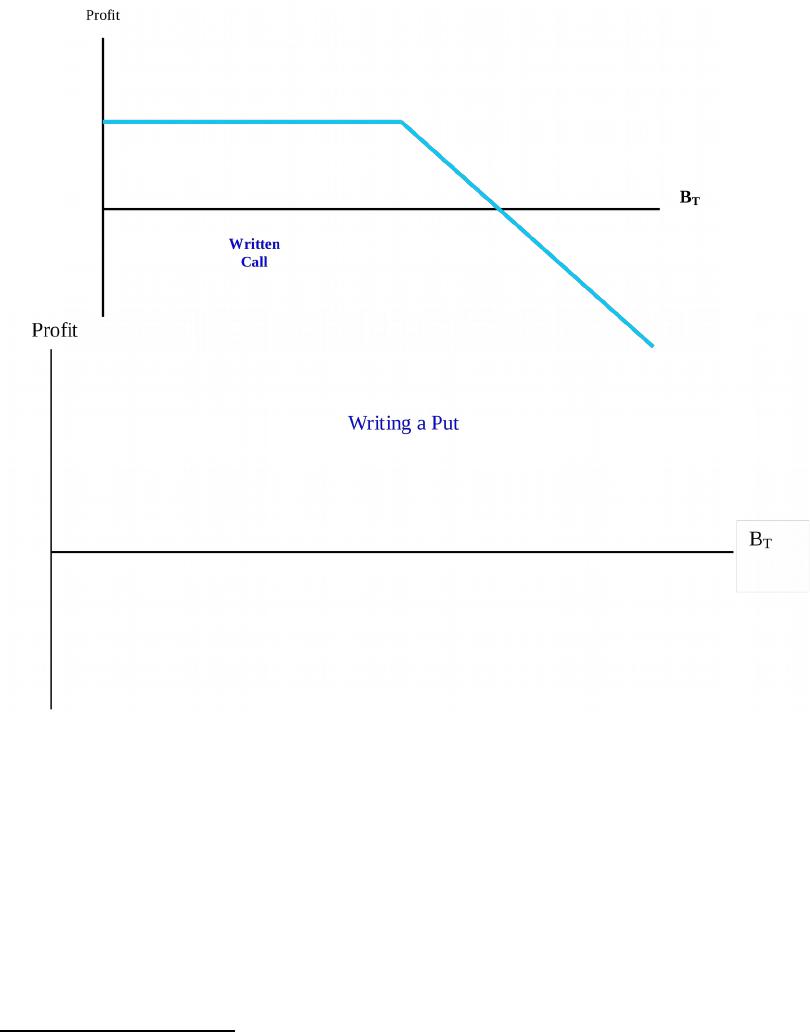

Writing options: When you write a call (put) option you receive the premium up front but you

have granted someone else the right to make you sell (buy) the underlying commodity at the

exercise price if it is advantageous for the counterparty to do so. The maximum gain is the

premium that the writer receives and it occurs if bond prices move such that the option winds up

out of the money. The maximum loss is generally unlimited and losses increase with rising

(falling) bond prices on a written call (put) option. Writing naked or uncovered options is thus

riskier than buying options, and these are appropriate strategies only in low volatility

environments.1

At expiration profit diagram of a written bond call and put option respectively:

The maximum loss is unlimited with the call and is quite large, but finite for the put. The written

call provides a limited gain equal to the call premium when bond prices fall (interest rates rise).

The put earns the put premium when bond prices rise above the exercise (interest rates fall).

b. Actual Interest Rate Options

See Chapter 10 for a discussion of actual contracts available.

c. Hedging with Options

If the FI’s spot position is exposed to falling interest rates, a call option may be purchased (or a

1For instance, the call option writer does not gain from large price drops (high downside price

volatility) and incurs large losses if prices rise (high upside price volatility). This strategy is a

bet that prices will not move much in either direction, i.e. low volatility. The same conclusion is

true for writing puts although the direction of the price effects is reversed.

put option may be written) to limit the FI’s net exposure.

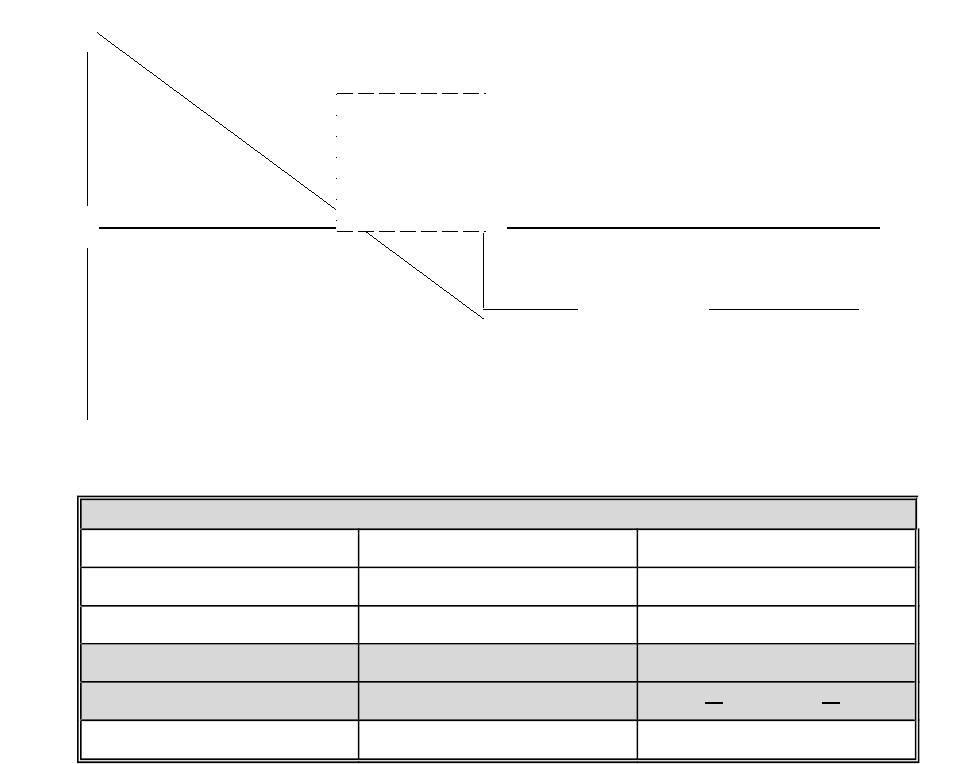

Example 2:

Suppose a FI has sold bonds short. It is at risk from falling interest rates (rising bond prices). In

order to hedge this risk the FI may purchase call options on the bonds. This would entail a small

capital investment relative to the size of the cash position and would limit the risk from rising

bond prices (see the graph below).

Profit

Figure 1

1.1 HEDGE A SHORT BOND POSITION WITH BOND CALLS

1.1.1 Profit Table ST < E ST > E

S0 – STS0 – STS0 – ST

-C0-C0-C0

+CT0 ST – E

= Profit S0 – ST – C0S0 – ST – C0 + ST – E

Breakeven ST = S0 – C0

S = Spot value at given time, C = Call value at time t where the time subscripts are 0 = hedge

initiation time, and T = expiration of the hedge and option contract. E = option exercise or strike

price.

The hedged position has a small maximum loss. The loss is limited to the initial call premium if

the call was originally at the money and the position has a potentially large gain. Note that the

combination of the short bond position and the call creates a synthetic put.

If an investor were long in bonds, an appropriate option hedge may be obtained by purchasing

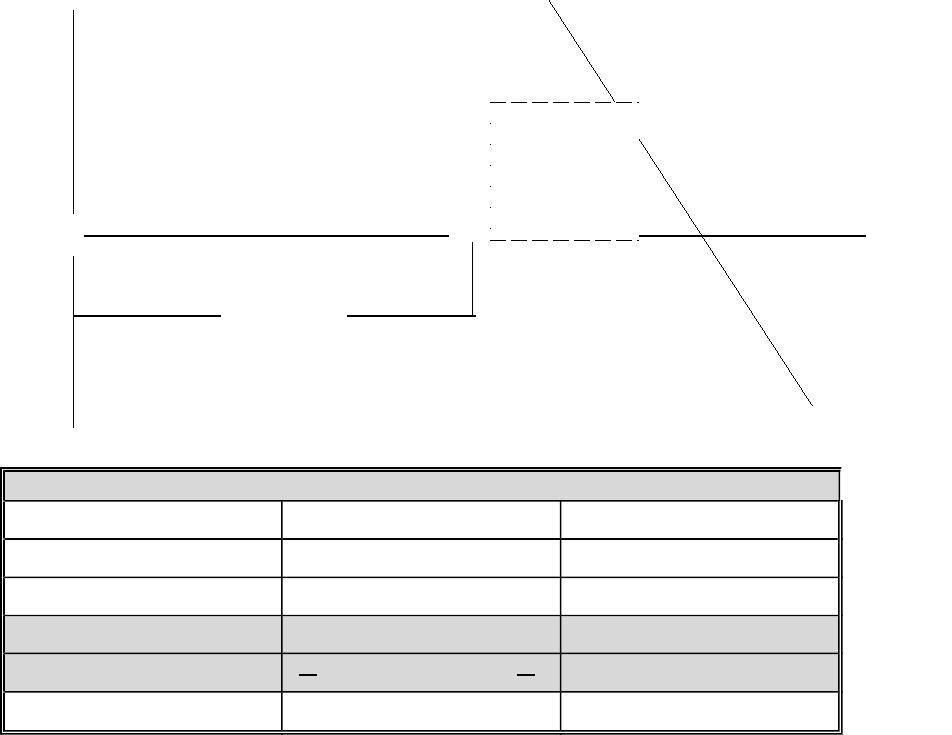

puts to limit the risk of falling bond prices. This situation is depicted below in Figure 2:

St

S0 – C0

S0 – C0 – E

E

ST = S0 – C0

$0

Profit

Figure 2

1.2 HEDGE A LONG BOND POSITION WITH BOND PUTS

1.2.1 Profit Table ST < E ST > E

ST – S0ST – S0ST – S0

-P0-P0-P0

+PTE – ST 0

= Profit ST – S0 – P0 + E – STST – S0 – P0

Breakeven ST = S0 +P0

S = Spot value at given time, C = Call value at time t where the time subscripts are 0 = hedge

initiation time, and T = expiration of the hedge and option contract. E = option exercise or strike

price.

The hedged position again has a small maximum loss. The loss is limited to the initial put

premium if the put was originally at the money and the position has a potentially large gain.

Note that the combination of the long bond position and the put creates a synthetic call.

d. Caps, Floors, and Collars

As an alternative to buying a put or call on a bond, a FI can hedge interest rate risk by buying

caps and floors. A cap is conceptually a type of European call option on interest rates with

multiple exercise dates. If an interest rate or rate index is above the cap rate (equivalent to the

exercise price on a standard call on a security) at one or more specified dates in the future the

seller of the cap pays the buyer the difference between the interest rate and the cap rate times the

notional principal amount. The seller of the cap receives a premium (sale price) at the time of

sale. These are OTC options and the terms are negotiated. Counterparty credit risk can be

substantial.

St

E – S0 – P0

E

ST = S0 + P0

$0

A floor is similar to a put option on interest rates. If an interest rate or rate index is below the

floor rate (equivalent to the exercise price on a standard call on a security) at one or more

specified dates in the future the seller of the floor pays the buyer the difference between the

interest rate and the floor rate times the notional principal amount.

The floor is equivalent to a call option on bond prices while the cap is equivalent to a put option.

A collar is a simultaneous position in a cap and a floor. These may be of two kinds. The FI may

simultaneously buy (sell) both a cap and a floor. This would limit the effect of rising and falling

interest rate movements on the FI’s profitability or market value. Alternatively, the FI could buy

(sell) the cap and sell (buy) the floor with different exercise rates. Suppose a bank constructs a

collar by buying a cap and selling a floor. When used this way the cap hedges increases in

interest rates (the FI receives money if interest rates rise above the cap rate) and the sale of the

floor helps finance the cost of purchasing the cap. This position is illustrated in the appendix.

2. Risks Associated with Futures, Forwards, and Options

The risks associated with derivatives vary with exchange traded and OTC deriviatives. Both

carry substantial trading risk if used improperly because of the high amount of leverage

employed in these contracts. OTC contracts also carry an additional risk that the text terms

‘contingent risk.’ Contingent risk results from the possibility that the counterparty will default.

Contingent risk would include the costs of replacing the contract and the losses that arise from

the spot position that is no longer hedged. Exchange traded options and futures contracts have a

very small chance of default, thus they have only limited contingent risk. With exchange traded

contracts the exchange backs the performance of the counterparty. Daily marking to market,

margin requirements, position limits and daily price limit change rules employed by exchanges

all help limit the exchange’s risks so that their performance guarantee is credible and sound.

Default and contingent risk can be substantial on OTC contracts and if participants are concerned

about counterparty default, collateral may be required on the contract.

3. Swaps (See Chapter 10 also)

There are five types of swaps: Interest rate swaps, currency swaps, credit risk swaps, commodity

swaps and equity swaps.

a. Hedging with Interest Rate Swaps

Interest rate swaps are by far the largest component of the swap market. An interest rate swap

is akin to a series of forward rate agreements although the payments are not known with certainty

at contract initiation. The major advantages of swaps over other hedge types are related to their

flexibility. These are custom contracts that can be tailored to meet the specific needs of hedgers.

They can be for much longer time periods than typical futures or option contracts (see table

below). In a plain vanilla swap one party makes a variable rate payment and the counterparty

makes a fixed rate payment on a given notional principal amount. The dollars due are calculated

by multiplying the appropriate interest rate times the agreed upon notional principal. Only the net

amount due is exchanged on an enactment date. Swaps may enact quarterly, semiannually or

annually.

Average swap maturity

Percent of swaps Swap Maturity

40% 1 year or less

36% >1 to 5 years

24% > 5 years

Source: Bank International Settlements Latest Tri-annual Survey, 2013

Example 3:

A U.S. insurer has a positive repricing gap of $50 million and believes that interest rates may

fall, reducing their profitability. A bank with a considerable amount of mortgage loans has a

negative repricing gap of $50 million. The bank is concerned that rates may rise, hurting their

profitability (See Chapter 22 for explanations of the repricing and duration gaps). The insurer

does not have enough rate sensitive (variable rate or short maturity) liabilities, the bank has too

many. The risk of both can be reduced by setting up a swap with a $50 million notional principal

where the insurer pays a variable rate of interest to the bank, and the bank pays a fixed rate to the

insurer. This swap will effectively reduce the repricing gaps of both institutions to zero. The

insurer effectively ‘transforms’ $50 million of fixed rate liabilities to rate sensitive liabilities, the

bank ‘transforms’ $50 million in fixed rate liabilities to rate sensitive liabilities. It is very likely

that the deal will be arranged through a third party FI, probably a large commercial or investment

bank. The swap broker takes a fee for arranging the deal. The swap broker may also guarantee

the payments of each participant in the swap (for an additional fee) so that counterparty default

risk may not be an issue. Also note that basis risk still exists to the extent that the variable rate

index specified in the swap (often LIBOR) is not perfectly correlated with the institution’s own

cost of funds or asset earning rate.2

2 Recall that basis risk is the risk that the spot price (or rate) and the price (or rate) on the

hedging instrument do not move together or as predicted.

b. Hedging with Currency Swaps

Fixed-fixed currency swaps

Example 4:

Ohio Bank has all of its assets in dollars but is financing some of them with an issue of the

equivalent of $75 million of 5 year fixed rate notes denominated in British pounds. Bulldog

Bank, a British FI, has a net $75 million dollar fixed rate liability. Ohio Bank is at risk from a

depreciating dollar (or an appreciating pound) because this would increase the cost to pay off the

pound notes. Bulldog Bank is at risk from a rising U.S. dollar (depreciating pound) because it

must use some of its pounds to pay off the dollar debt. Both FIs can reduce their currency risk

by engaging in a swap, this time of both interest and principal. Ohio bank agrees to pay the

dollar interest and principal on $75 million of principal for 5 years. In return, Bulldog agrees to

pay the pound interest and principal on a similar amount. Both have eliminated their exchange

rate risk. This may be less expensive than refinancing at current market rates.

Fixed-floating currency swaps can also be arranged. If Ohio had borrowed at a fixed rate of

interest as before, but Bulldog had incurred a floating rate liability and if Ohio had rate sensitive

assets it wished to match, then a fixed-floating swap might be possible to arrange (See the

Supplement).

Large FIs may act as swap dealers (act as the counterparty) even if no other customer with

opposing needs can currently be found because the FI knows that eventually it will be able to

engage in other swaps that offset the risk involved in the current swap deal. FIs keep a ‘book’ of

their swap deals and manage their net risk exposures.

c. Credit Swaps

In 2013 commercial bank credit default swaps (CDS) outstanding were $11.2 trillion, down from

$14.47 trillion in 2010. Banks may buy CDS to increase or maintain loans and investments

while shifting risk to other parties such as insurance companies and hedge funds. Swap buyers

make periodic payments to the sellers and the sellers pay the buyer in the event of default. CDS

contracts may be cash settled or physical settled. If physical settled then the CDS buyer has an

option of which securities to deliver. Many CDS were cash settled however.

Total return swaps (TRS) provide a way for a lender to offset the risk of a decline in value

associated with a drop in credit quality of the loan. For example a TRS buyer may agree to make

a fixed rate payment to the seller plus the capital gain or minus the capital loss on the underlying

instrument. In exchange the TRS seller may pay a variable or a fixed rate of interest to the buyer.

In this type swap the capital gain or loss may be on a related index to avoid liquidity problems

with individual loans. Thus, basis risk and interest rate risk remain.

In a pure credit swap, the swap buyer makes fixed payments to the seller and the seller pays the

swap buyer only in the event of default. The payment is usually equal to par – secondary market

value of the underlying instrument.

d. Credit Risk Concerns with Swaps

There is now a risk based capital requirement imposed on banks who engage in swaps. Credit

risk on interest rate swaps is generally much lower than on loans of equivalent principal amounts

because:

1. Only the net payment is due on the swap payment dates, and this amount will be less than the

typical interest payment on an equivalent principal loan.

2. Swap payments are often interest only and not principal, so the notional principal is not at

risk.

3. If a swap partner is concerned about the counterparty’s creditworthiness they may require the

counterparty to obtain a standby letter of credit or to post collateral.

Currency swaps usually do involve principal swaps. The biggest risk however is probably with

credit default swaps. The failure of Lehman and AIG resulted from losses on mortgage related

CDS contracts the firms had sold.