1.1.1.1 Equity Value Change

E = – [3 – (0.901)] $500 million (0.0050 / 1.12) = –$4,687,500.

To find the percentage change in equity, divide both sides of the equation by E:

E = $500 million (1-0.90) or E = $50 million so that:

E/E = – [3 – (0.901)] ($500 million/$50 million) (0.0050 / 1.12) = – 9.375% or E/E may

be more simply found as -$4,687,500 / $50,000,000 = -9.375%.

Changes in the value of equity for different duration gaps

Recall that duration measures the value change of the assets or liabilities for a given interest rate

change. If we assume similar rate changes for assets and liabilities then the following

generalizations can be made:

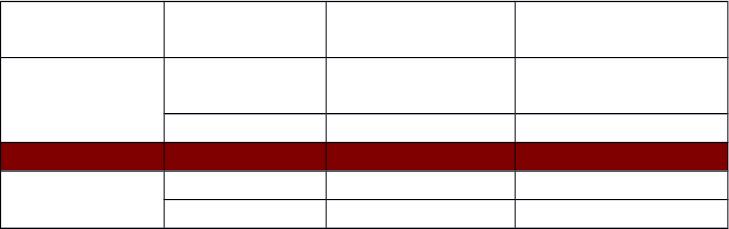

Duration Gap

Interest Rate

Change

Biggest Value

Change

1.2 Equity

Value

Positiv

e

2 Increas

e

Assets Decreases

Decrease Assets Increases

Negative Increase Liabilities Increases

Decrease Liabilities Decreases

Both asset and liability values for fixed income contracts increase when rates fall and decrease

when rates rise. However, for a positive duration gap the absolute value of the change in value

of the assets is greater than the change in value of the liabilities when interest rates change. With

a negative duration gap the change in value of the liabilities will be larger in absolute terms than

the change in value of the assets.

Teaching Tip: The duration of a variable rate contract may be thought of as the time until the rate

reset. This will typically be much shorter than the maturity. Thus, a 30 year mortgage with a

rate adjustment due in 6 months has a 6 month duration. Contracts with a maturity of 3 months

or less may be thought of as having a duration equal to their maturity without substantively

affecting the analysis. This simplifies the duration calculations for many accounts.

If the bank has a positive duration gap and is forecasting rising rates, they may wish to switch to

shorter term assets and/or variable rate assets and try to lengthen the duration of the liability

portfolio. Alternatively, the off balance sheet tools discussed in Chapter 23 could be used. If the

leverage adjusted duration gap is zero, the equity value will be approximately unchanged for

small changes in interest rates.

Problems with the duration model include:

Duration matching can be time consuming and costly. Although this is still true, with

today’s computing power this criticism is less valid than in the past.

Immunization (setting and keeping the duration gap at zero) is a dynamic process. The

durations of the assets and liabilities will change every time interest rates change and will

change at uneven rates over time (the duration formula is not linear with respect to time).

This implies that maintaining a given duration gap requires frequent on or off balance

sheet adjustments, and implies that trading costs have to be weighed against the benefits

of duration management.

Immunization does not provide protection for large interest rate changes due to convexity

because duration predicts a linear price change with respect to interest rates. In actuality

the capital loss associated with a given percentage interest rate increase is less than the

capital gain associated with a given interest rate decrease. Duration thus overpredicts

capital losses and underpredicts capital gains because of convexity.

Teaching Tip: The duration model can cause bankers to become complacent about the interest

rate risk they face. Aside from convexity, which can be a significant problem in an abnormal

market, the duration model suffers from many of the same problems as the RPM. For instance,

the effects of defaults, prepayments, and call features of securities are difficult to include in the

duration calculations. This can lead to the belief that the bank precisely knows its risk level

when in fact a large interest rate move that changes investor behavior is not incorporated into the

model.1

1. Insolvency Risk Management

a. Capital and Insolvency Risk

Equity is the FI’s main cushion against insolvency. It also serves as a source of funds and as a

requirement for growth given the minimum capital to asset requirements in force for DIs. Equity

can be thought of as either the book value of assets minus the book value of liabilities, with

some adjustments allowed by regulators, or as the market value of assets minus the market

value of liabilities. Book values are only rarely accurate representations of market values.

Teaching Tip: Book values are not necessarily good representations of liquidation values either.

It is not clear to this author exactly what book value of equity actually measures. It is roughly

the sum of past decisions on asset acquisitions less the face amount borrowed. As such it appears

to be roughly a measure of net sunk costs by managers. It has the advantage of being calculated

according to a set of rules that limit management’s ability to manipulate equity value, and it

provides a fairly predicable number on a day to day basis. For those who remember their

economics training, this very stability implies that the book value of equity cannot be a fair

representation of the ongoing day to day value of the firm in a dynamic marketplace.

The Capital Purchase Program (CPP) was part of the TARP funding in 2008-2009. The

Treasury purchased over $200 billion of senior preferred equity under the program. These

purchases qualified as Tier 1 capital for FIs. Citigroup and Bank of America received additional

special funding under this program totaling $25 billion and $20 billion respectively. The CPP

was designed to help FIs increase their capital with the aim of increasing lending to the general

public. Lending fell in 2008, 2009 and 2010, so in this sense the program was a failure, although

presumably lending would have fallen even farther without it and more failures may have

occurred. The program came with stipulations on maximum executive pay, golden parachutes

and clawback provisions on executive pay based on earnings and limits on tax deductions

1This is a false precision problem. VAR suffers from similar criticisms, as the failure of Long

Term Capital Management showed.

associated with executive compensation.

Capital and credit risk:

Loan losses are written off against capital. As loans are marked to market, capital is reduced.

When enough loan losses eliminate all the existing equity, the institution is insolvent.

Capital and interest rate risk:

Realized losses in value of securities and loans are also written off against capital. If losses due

to rising interest rates (net of the reduced value of liabilities) are large enough to wipe out the

FI’s capital, the institution becomes insolvent.

Market value accounting and insolvency

If regulators closed an institution as soon as its market value of capital became zero, theoretically

no liability holders or taxpayers would suffer any losses and the FDIC’s DIF would never be

required. This is not the case if regulators wait until the book value of equity is zero to close the

institution. Book value of equity is composed of par value + surplus + retained earnings + loan

and lease loss reserves. It is not automatically adjusted downward as credit or interest rate losses

occur. For instance, under GAAP, FI managers do not have to recognize loans as ‘bad’ and write

them off in the year in which payment problems develop. Managers may also sell other assets

that have gains in value (these are marked to market when sold) and inflate the book value of

capital even though losses on other loans and securities have not been recognized. This practice

is called ‘gains trading’ and can be used to postpone insolvency (while generating larger losses).2

The use of book value does not recognize losses due to interest rate risk either. As interest rates

rise, an institution with a positive duration gap suffers losses to the market value of equity. The

book value of equity is unchanged until the assets and liabilities are marked to market. This

explains why over half of all S&Ls were insolvent in the early 1980s under market value

accounting but were allowed to continue to operate. The insolvent S&Ls went on to generate

even larger losses that eventually bankrupted the industry’s insurer, the FSLIC. Examinations

help limit the difference between book value and market value of capital by forcing FIs to

recognize its true losses. Loan and security sales also reduce the difference. However, in times

of high credit losses and high interest rate volatility, the difference between the book and market

value of equity can become quite large. One can attempt to measure this difference by

examining an institution’s market to book ratio. The market to book ratio is the market value

of equity divided by the book value of equity. In a small sample of large banks, the market to

book ratios ranged from a low of 0.849 for Deutsche Bank to as high as 3.312 for Bank of New

York Mellon.3

In summary, using book value accounting increases the government’s potential liability to

depositors and other claimants.

Predictably, the industry is against implementing market value accounting. The reasons usually

cited are:

1. Banks and thrifts maintain that implementing market value accounting is difficult and

burdensome, particularly for smaller institutions that have many nontraded assets for which it

2 New market value accounting rules should help minimize gains trading.

3 The text data includes thrifts.

would be difficult to obtain a market value. However, it seems fairly easy to impute a market

value for financial assets and liabilities, so this argument does not seem particularly relevant

except perhaps for very small institutions.

2. Managers do not want unrealized (paper) gains and losses to be reflected in income, claiming

this would excessively destabilize earnings and equity. Accounting theory tells us that the

purpose of income as it is measured is to smooth out fluctuations in cash flows through time

to provide a better picture of value than short term, highly variable cash flows. Accruals

adjustments supposedly give a truer picture of the cash flow potential of the firm over the

long term. Stock prices appear to more closely follow income than short term cash flows or

EVA adjusted cash flow measures. Managers claim they hold many of their assets and

liabilities to maturity and marking them to market would simply distort the value of the bank

to shareholders. Moreover, the FDIC claims that marking to market could cause them to

have to close an institution that might otherwise survive simply because of a short term

interest rate movement. Both arguments have some validity but are incorrect theoretically.

The managers’ claim that we should not update values as market conditions change implies

that equity should measure something other than present value of expected future cash

flows.4 An economic variable that measures future prospects must be unstable if those

prospects are changing. Bankers and accountants don’t think this way though. They want a

measure of value that is stable and encourages accountability. The FDIC’s argument forgets

that during the 1980s the FSLIC went bankrupt (and the FDIC came close) because book

value accounting allowed institutions to build large losses which the insurer eventually had to

pay. There is also an implicit assumption in their argument that an interest rate change will

be reversed in time to restore profitability to the institution. I doubt the validity of that

argument, but more importantly, I would counter that if a short term interest rate move can

put an institution under then the regulators need to bring about a change in management at

that institution anyway.

3. FIs also maintain that they would be less likely to engage in long term lending and investing

if these accounts were regularly marked to market. This statement itself is very revealing as it

indicates that FI managers recognize that the current accounting rules allow managers to

take on more risk than they could otherwise. There might be disruptions in the short run,

but in a free capital system, other new lenders would emerge if banks refused to make these

loans. They may not make as many, or they may increase the price of the loans, or they may

simply hedge more. This appears to be a disingenuous argument.

4. The industry argues the lack of liquidity in the recent crisis led to unrealistically low market

values of assets and marking to market imposed excessive losses on institutions.

Consequently the Financial Accounting Standards Board (FASB) allows management to rely

on internal estimates of cash flows to estimate fair value. This is referred to as ‘marking to

model’ rather than ‘marking to market.’ This makes sense in a non-functioning market

environment but it still allows FIs to not update the value of assets and liabilities to current

market conditions and adds subjectivity that is likely to be manipulated by management.

4 Alternatively managers may be implicitly implying that the maturity of their investments is the

proper time horizon over which value should be measured, but equity does not mature when their

investments do so they are ignoring reinvestment risk over the longer time horizon, the value of

which is better captured by current market values.

5. As of April 2009 FASB allows DIs to not recognize losses in earnings and regulatory capital

on accounts that are a) designated as held for investment rather than sale and b) temporarily

impaired in value due to market conditions rather than underlying credit deterioration. The

losses must be accounted for and revealed separately. This again adds subjectivity that can

be used to hide losses. The new rules imply that regulators will be able to evaluate these

issues and will be willing to do so.

This discussion is part of a larger debate between accountants and bankers who favor book value

and rules based measures and financial economists who favor letting the market determine value.

Accounting rules are designed to provide a stable measure of historical value that minimizes

managerial manipulations and preserves management accountability. However, in a dynamic

world where value is determined as the present worth of expected future firm prospects, book

value cannot possibly accurately measure daily fluctuations in economic firm value. If you

believe that firm value is the aggregation of the past and current decisions of the firm’s

management, then you will probably prefer book value measures of equity. If you instead

believe that firm value is properly an estimate of the value of the current and future prospects of

the firm then you should prefer market value.

1.1.1.1 VI. Web Links

http://www.federalreserve.gov/ Website of the Board of Governors of the Federal Reserve

http://www.fdic.gov/ The Federal Deposit Insurance Corporation website has net

charge off rates for banks and thrifts.

http://www.fasb.org/ FASB webpage with full text and summaries of FASB

statements

http://www.americanbanker.com/ ABA website.

http://www.wsj.com/ Website of the Wall Street Journal Interactive edition. The

web version of the well known financial newspaper can be

personalized to meet your own needs. Instructors can also

receive via e-mail current events cases keyed to financial

market news complete with discussion questions.

1.1.1.1.1.1 VII. Student Learning Activities

1. Go to the FDIC website and find the Quarterly Banking Profile. How has the average

duration gap been changing at institutions? Are the banks currently more or less vulnerable to

rising or falling interest rates? Explain why.

2. Go to the FDIC website and find the Quarterly Banking Profile. What has been

happening to the book value of equity capital? Why have these changes occurred? Has the

number of problem banks increased or decreased recently? Ascertain why. Find an index of

bank stocks. What has been happening to the market value of equity capital? Are the changes

similar? Why or why not?

3. Go to http://www.fasb.org/ and find the summary of FASB statement No. 114,

“Accounting by Creditors for Impairment of a Loan.” According to this statement how should

lenders value problem loans? Why are all loans not valued this way? Explain.

Find the FDIC DOS Manual of Examination Policies: Market Risk, Section 7.1 on the web.

What are the primary goals of examiners when they evaluate a bank’s interest rate risk (IRR)?

What are the ‘earnings approach’ and EVE? How do they differ? What is the FDIC looking for

in its IRR