1. Credit Analysis

Teaching Tip: Credit analysis is geared towards one decision, “Does the FI grant the loan?” The

purpose of credit analysis is to generate profitable loans that do not expose the lender to

excessive amounts of risk. The reason for the accept or reject decision should be clearly

documented and the decision should be in accordance with the bank’s stated loan policy.

Criteria used must not be discriminatory; thus, the determinants of the decision cannot be race,

gender, location, ethnicity or religious persuasion. If the loan officer is to err, the errors should

be conservative. In the long run it will cost the lender much more to handle a failed loan than to

incorrectly turn down a loan that would not have failed. This is true because lending has

asymmetric outcomes. Distributions of returns on loans exhibit negative skewness. Lowering

credit quality tends to increase the negative skewness, although if the risk is priced this may also

increase the average rate of return on the loan portfolio. Regulators impose quality standards on

lenders to help ensure they do not take on too much risk in attempting to increase the average

return on the loan portfolio.

Teaching Tip: The bank’s loan policy includes the desired portfolio of loans by category and

includes minimum credit standards such as collateral requirements and minimum ratios. Other

provisions include lending limits for certain loan officer positions, standards for grading loans,

requirements for monitoring existing loans, policies on inside loans and the documentation

required to evaluate a loan application. Many banks now use standard application forms for each

type of loan. The loan officer will be trained in the specific form the bank uses.

Nonperforming Loans to Total Loans All Banks 2002-2010

Date C&I Real Estate Consumer

2002 2.92 0.89 1.51

2003 2.10 0.86 1.52

2004 1.17 0.65 1.46

2005 0.75 0.70 1.20

2006 0.64 0.81 1.24

2007 0.64 1.62 1.48

2008 0.78 2.12 1.51

2009 3.57 6.69 2.12

2010 (March) 3.12 8.03 1.41

2010 (Sept) 2.77 7.67 1.92

Note the large increase in nonperforming rates on Real Estate and Consumer loans beginning in

2007. Banks with assets greater than $10 billion generally had higher rates of nonperforming

loans. Because all banks normally have about 50 to 60% of assets in loans and only about 10%

in equity, even small amounts of loan losses can quickly deplete equity.

Nonperforming loan rates have improved but remain elevated. See Text Figure 20-1. While

U.S. banks were not significantly exposed to Greek debt during the euro crisis, they were heavily

exposed to Spain, Ireland, Portugal and Italy with loans topping $120 billion in aggregate. Thus,

the euro crisis was a significant credit event for U.S. banks. The so called London whale trades

that went awry were attempts to limit credit risk exposure to the euro area and exploit credit

spread differences with U.S. corporate debt.

a. Real Estate Lending

Residential mortgage applications are usually very standardized because of the active secondary

market for these claims. The two major factors in making the accept or reject decision for the

mortgage loan are 1) the applicant’s ability and willingness to repay the loan and 2) the value of

the borrower’s collateral. In assessing the first requirement standard ratios and/or credit scoring

models may be used. The character of the borrower is also very important. Character is

assessed by examining the stability of the borrower as indicated by family status, time in

residence, time in job, savings history, payment history and any personal knowledge the lender

may have of the borrower. Assessing character is essentially assessing two factors:

1. Whether the potential borrower is mature enough to manage credit, and

2. Whether the borrower will consider the debt as a moral obligation that he or she will

work hard to repay even if difficulties arise.

The second aspect of the first requirement is the borrower’s ability to repay the loan. To assess

sufficiency of income the lender may calculate the following ratios:

1.1.1.1 Gross Debt Service

GDS = (Annual mortgage payments + Property taxes) / Annual gross income

The maximum for loan approval is usually 25% to 30%.

1.1.1.2 Total Debt Service

TDS = Annual total debt payments / Annual gross income

The maximum for loan approval is usually 35% to 40%.

Example:

A mortgage loan applicant has the following data:

Gross Income

Monthly

Mortgage P&I

Payment

Annual

Property Taxes

Annual

Homeowner’s

Insurance

Other Debt

Payments / year

$175,000 $3,500 $4,500 $950 $29,000

GDS Ratio = (Annual mortgage payments + Property taxes) / Annual gross income

= (($3,500*12) + $4,500) / $175,000 = 26.57%

Conclusion: Pass

TDS Ratio = Annual total debt payments / Annual gross income

= (($3,500*12) + $4,500 + $950 + $29,000) / $175,000 = 43.69%

Conclusion: Fail

Based on these ratios the applicant would not be granted a loan because the TDS ratio is too

high.

Teaching Tip: I encourage students to meet with a loan officer or at least make phone contact

once they are established in a job, even if they do not currently need a loan. This helps establish

the potential borrower (the student) in the mind of the loan officer as a mature person who is a

professional to be taken seriously.

A credit score may be calculated to provide a broader assessment of the various factors that

underlie the loan evaluation process. A credit score is a mathematical model that uses loan

applicant characteristics to assist the lender in deciding whether or not to grant the loan. Credit

scoring models can be developed by examining the characteristics of both good and bad loans

the bank has previously made, and then attempting to ascertain what characteristics can be used

to discriminate between the good and bad loans. Typical credit scoring attributes include

annual income,

a score based on TDS and or the GDS ratios,

history with the lender,

age,

whether the borrower’s residence is owned or not,

length of time in the current and prior residence and time in the current job,

credit history, etc.

Based on scores of past good and bad loans, the lender can establish a minimum credit score

below which a loan will not be granted, an intermediate score where additional credit analysis is

warranted and another level beyond which a loan will automatically be granted. Credit scores

provide objective, low cost, quick evaluation methods that are particularly suitable for smaller

loan amounts that can utilize standard evaluation methods. I have reproduced the form from

Example 20-2 in the text.

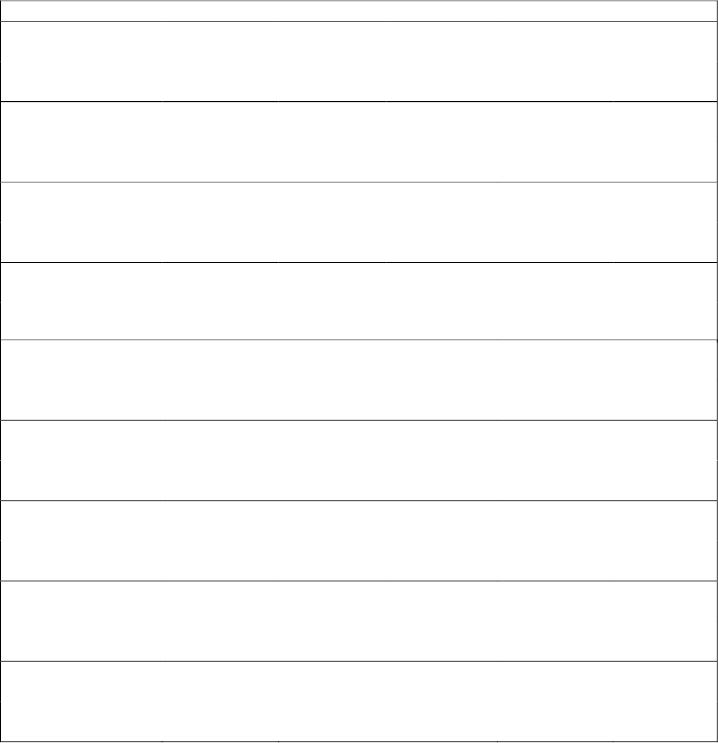

Sample Credit Score

Characterisc Values and Weights

Gross Income <$10,000

$10,00

0

–

$25,00

0

$25,00

0

–

$50,00

0

$50,00

0

–

$100,00

0

>$100,000

Score 0 1

5

3

5

5

0

7

5

TDS >50% 35%-50% 15%-35% 5%–15% <5%

Score 0 1

0

2

0

3

5

5

0

Relao

n

with FI Non

e

Checking Savings Both

Score 0 3

0

3

0

6

0

Major credit

card

Non

e

1 or

more

Score 0 2

0

Age <25 2

5

-6

0

>60

Score 5 3

0

3

5

Residenc

e

Live w/ parent Rent Own/Financ

e

Own Outright

Score 0 5 2

0

5

0

Length of re

s

idenc

e

< 1 year 1–5

years

> 5 years

Score 0 2

0

4

5

Job stability < 1 year 1–5

years

> 5 years

Score 0 2

5

5

0

Credit history No

record

Pmt missed in last 5 year

s

Met all pmt

s

Score 0 -1

5

5

0

Automac rejecon level

score

: 120

Automac acceptance

level

score

: 190

Scores between 120 and 190 are reviewed by a loan o=cer or loan

commi>ee

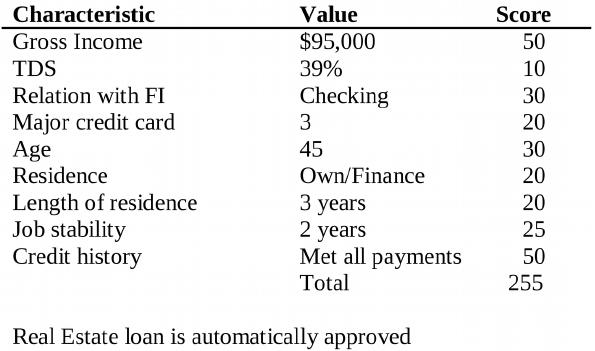

An individual with the following characteristics and credit scores would be approved for the

mortgage. (Note that my characteristics and total score are different from the text example.)

Teaching Tip: The decision to approve or reject many mortgage and small consumer loans is

made very quickly. Please don’t leave your students with the impression that this is a long drawn

out process entailing meetings with a loan committee, etc.

Teaching Tip: The Federal Reserve requires that credit scoring criteria not be discriminatory.

Nevertheless age is used in credit scores. This is presumably acceptable because older potential

borrowers are normally assigned higher credit scores in that category. Some credit scores assign

a lower score for age brackets where the borrower is likely to have college age children. Note

that if the Justice Department continues to apply ‘disparate impact’ as a test of discrimination

then usage of credit scoring models is likely to become problematic.

Verification of the applicant’s information is necessary and the loan application will grant the

lender the right to check relevant sources. Lying on a loan application will normally

automatically result in a rejection.

Teaching Tip: Lying on loan applications probably contributed to the subprime mortgage crisis.

First, originators used so called “low doc” and/or “no doc” loans where loan applicants did not

have to provide verifying documentation for the loan application and/or the information provided

was not verified. Some lenders allegedly even encouraged applicants to falsify certain

information such as income or debts to ensure the loan would be granted. In most cases the

loans were sold and there was no recourse to the loan originators as long as the first three

mortgage payments were made on time. The loans became euphemistically known as ‘liar’s

loans.’

Standardized Credit Scoring Models

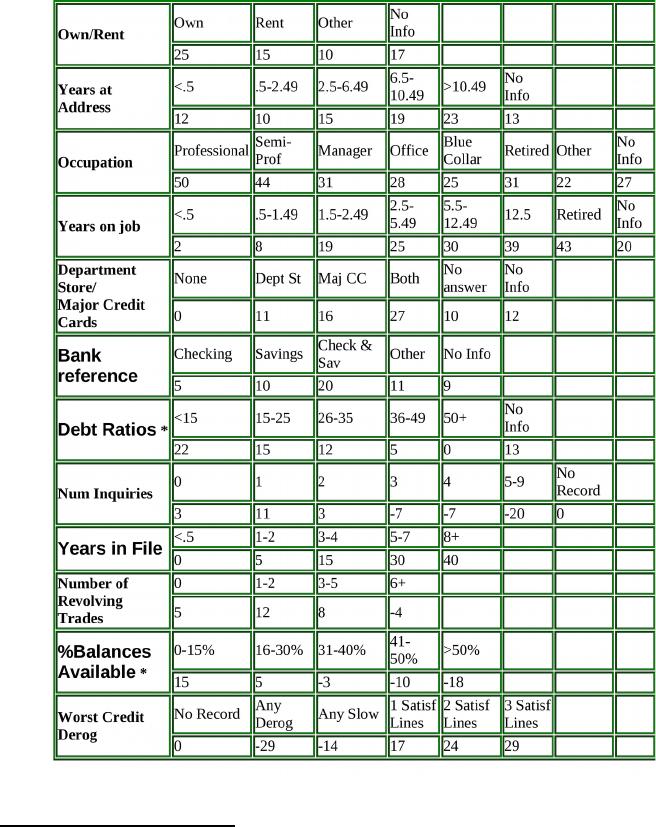

Standard FICO scores can be used to evaluate consumer and mortgage loans. FICO scores assess

the following 10 characteristics to arrive at a score:

1. Major derogatory items on your report (bankruptcy, foreclosures, slow pay)

2. Time at present job

3. Occupation

4. Time at present address

5. Ratio of balances to available credit lines

6. Are you a homeowner?

7. Number of recent inquiries

8. Age

9. Number of credit lines on your report

10. Years you have had a credit in the credit bureau database

FICO scores run from 300 to 850 with the majority of scores between 600 and 800. Scores of

720 or higher are usually sufficient to receive a good mortgage rate.

The actual complete FICO model is proprietary. However according to the information from

Fair Isaac on the Federal Trade Commission site found at

http://www.ftc.gov/bcp/creditscoring/present/sld001.htm some of the scoring numbers used in

FICO scores include the following:1

Teaching Tip: FICO states that payment history comprises 35% of the FICO score, amount owed

1 This site contains a PowerPoint presentation with details on the credit scoring model criteria

and how the cutoffs are determined. The presentation also compares data for high minority

areas, presumably to demonstrate the model is not discriminatory with respect to minorities.

This source is no longer available as of this writing in 2014.

is another 30%, length of credit history is 15%, new credit applications 10%, and ‘other’ factors

such as a mixture of credit types counts for 10% of the total score.2

The other major aspect of real estate credit analysis is the assessment of the value of the pledged

asset and its suitability to serve as collateral. The lender must ensure that the house is free and

clear of any liens and all back taxes that could prevent seizure in the event of foreclosure or

power of sale.3 This process is termed perfecting the interest in the collateral. The lender must

also ensure that the legal description is correct, which will normally require a current survey.

The value of the collateral will be assessed by an appraiser.

Teaching Tip: Some FIs use their own appraisers, but most hire independent appraisers. Some

appraisals are written up after only driving by the property, others involve more detailed

inspections. The appraisal process relies heavily on the sale price of nearby homes that are

supposedly comparable properties. This is one reason why one should not buy the most

expensive house in the neighborhood.

b. Consumer (Individual) and Small-Business Lending

Consumer loans are typically scored similarly to real estate loans. There will be a greater

emphasis on examining whether the individual has the capacity (cash flow) to repay the loan and

on the individual’s character. The credit scoring models are likely to reflect these different

weights.

Evaluation of small business loans is more difficult. Many young firms find themselves in

financial difficulty at some point in their history. Some FIs employ minimum time in business

requirements to grant a loan, or may include the time in business in a credit scoring model.

Profitability on small business loans is generally not large considering the extra time and effort

needed to evaluate the loan. The ‘life blood’ of most small businesses is cash flow, and the

credit evaluation process is likely to emphasize cash flow, the soundness of the business plan and

the character of the borrower.

2 FICO Score Fact Sheet,

http://www.fico.com/en/wp-content/secure_upload/FICO_Score_2775FS.pdf.

3 Foreclosure is seizing the collateral in the event of non-repayment of the loan in exchange for

discharging the debt. The power of sale is the process of seizing collateral and selling it to pay

off the loan when the borrower fails to repay the loan. In this case any excess sale value beyond

the loan amount & costs would be returned to the mortgagor and if the sale value is not sufficient

to discharge the debt the lender would then become an unsecured creditor for the difference.