1.1.1.1.1Chapter Twenty

Managing Credit Risk on the Balance Sheet

1.1.1.2 I. Chapter Outline

1. Credit Risk Management: Chapter Overview

2. Credit Quality Problems

3. Credit Analysis

a. Real Estate Lending

b. Consumer (Individual) and Small-Business Lending

c. Mid-Market Commercial and Industrial Lending

d. Large Commercial and Industrial Lending

4. Calculating the Return on A Loan

a. Return on Assets (ROA)

b. RAROC Models

Appendix 20A: Loan Portfolio Risk and Management, available on Connect or from your

McGraw-Hill representative

II. Learning Goals

1. Examine trends in nonperforming loans at commercial banks.

2. Understand the processes financial institutions use to evaluate a mortgage loan application.

3. Use a credit-scoring model.

4. Appreciate the analysis that is involved in mid-market commercial and industrial lending.

5. Analyze large commercial and industrial loans.

6. Calculate the return on a loan.

1.1.1.3 III. Chapter in Perspective

This chapter discusses methods of credit analysis and rate of return calculations on loans. Loans

are the main line of business at depository institutions and finance companies. Credit problems in

the loan portfolio are the primary cause of failure at lending institutions so the analysis of credit

risk is of primary importance to many FIs. An understanding of credit risk and credit analysis is

useful regardless of whether one works in the credit department of a lender, or if one is involved

in presenting loan applications on behalf of a corporate borrower, or even for someone who just

wishes to increase their chances of success when seeking a personal loan. Methods of credit

evaluation differ for various types of loans and by the size of the borrower. The primary

concerns of credit analysis for four of the major types of loans are presented. Calculating the

rate of return on the assets invested for a loan with fees and compensating balances is presented

as well as the newer risk adjusted return on capital model. The appendix presents an application

of modern portfolio theory to determine the best diversified loan portfolio.

1.1.1.4 IV. Key Concepts and Definitions to Communicate to Students

Junk bond EBIT

GDS ratio EAT

TDS ratio Conditions precedent

Credit scoring system LIBOR

Perfecting collateral Prime lending rate

Foreclosure Compensating balances

Power of sale Minimum risk portfolio

RAROC model KMV model

Base loan rate Credit risk premium

5 Cs of credit Loan policy

Appraisals Liens

HLT loans Extreme loss rate

FICO scores

1.1.1.5 V. Teaching Notes

1. Credit Risk Management: Chapter Overview

FIs in the purest form of their function are asset transformers (see Chapter 1). They provide

savers with low risk, liquid claims that savers desire and channel funds to borrowers by granting

higher risk, less liquid loans to funds demanders. To put it succinctly, FIs take peoples’ money

and invest it in risky claims. As such, the ability to assess, monitor and appropriately price the

riskiness of loans is of paramount importance to many FIs. Loan defaults must be written off

against equity; thus, high levels of defaults can quickly impair an institution’s capital.

Teaching Tip: From a macroeconomic perspective a sound private banking system is necessary

to appropriately price risk and allocate capital to its best uses. It is rare for countries to generate

substantial sustained economic growth without private internal capital allocation methods. These

methods usually center around the banking industry. Sound banking systems are also often

precursors to strong internal capital markets. Japan’s protracted economic difficulties have

been significantly worsened by the problems and lack of competitiveness of the Japanese

banking system.

U.S. FIs had significant credit problems in the 1980s and into 1990. In the early 1980s problems

in residential and farm mortgages, particularly in certain regions of the economy, led to the

failures of many banks and S&Ls. S&Ls had difficulties with junk bond holdings in the latter

part of the 1980s. Problems in commercial real estate and LDC loans developed and hurt the

profitability of both the banking and thrift industries. In the 1990s there were worries about high

credit card debt levels, major defaults in Russia and moratoriums on debt repayments in

Indonesia and Malaysia. The end of the 1990s saw improvements in the credit quality of most

bank loan portfolios however and the level of nonperforming loans (loans 90 days or more past

due or not accruing interest) and loss reserves declined. The recession in the early part of this

century reversed these trends, but as the economy improved in the mid 2000s loss rates again

fell, particularly on C&I loans as corporations improved their balance sheet positions

dramatically and began to hold large cash balances. Personal bankruptcy filings have continued

to grow, but recent changes in bankruptcy laws slowed this trend until the financial crisis

increased the number of bankruptcies (see Chapter 19 for data). Overseas, in 2001 Argentina

defaulted on $130 billion of government issued debt and in September 2003 defaulted on a $3

billion loan from the IMF. In 2005 Argentina unilaterally announced it would pay only $0.30 per

dollar on loans and bonds outstanding from its 2001 debt restructuring. In June 2014 a U.S.

court of appeals ruled that Argentina could not repay its restructured debt without paying in full

the holdouts to the restructuring deal. As of this writing Argentina is refusing to comply with the

court order.1

Mortgage delinquency rates increased dramatically beginning in the last quarter of 2006 and

remained high through 2007. Foreclosure filings increased 93% in July 2007 from the same

month in the prior year. Insured institutions set aside a record $31.3 billion in provision for loan

losses in the fourth quarter of 2007 and one quarter of all institutions larger than $10 billion

reported a net loss for the quarter. Institutions associated with subprime lending and those with

significant trading activity had the largest earnings declines. Net charge offs (NCOs) rose to 5

year highs in the fourth quarter as well reaching $16.2 billion, up from $8.5 billion in the fourth

quarter of 2006. NCOs on residential mortgages increased 144.2% and NCOs on home equity

lines increased 378.4% while charge offs on credit card loans were up 33% and charge offs on

loans to individuals increased 58.4%.2 This made the annual ROA at 0.86% the lowest since

1991. In the first quarter of 2008 new loan volume in the riskier parts of the lending market fell

dramatically with some parts of the market dropping upwards of 80%-90%. These areas

included collateralized loan obligations, loans funding LBOs and high yield bonds. Banks were

also beginning to restrict higher quality lending. For instance, as banks focused on capital

restoration credit lines less than one year became increasingly popular as they carry lower capital

requirements.3

1 Argentina says it has no team for talks in debt battle, by Alexandra Ulmer and Jorge Otaola,

Reuters, June 19, 2014,

http://www.reuters.com/article/2014/06/19/us-argentina-debt-idUSKBN0ET1RK20140619

2Source: FDIC Quarterly Banking Profile

3“1Q08 U.S. Loan Market Review: Been Down So Long It Looks Like Up To Me,” Press

Release of the Loan Pricing Corporation, March 28, 2008, www.loanpricing.com.

Losses from both on and off balance sheet claims resulting from the subprime crisis were

over $2.3 trillion worldwide. Net charge off rates reached record highs in the fourth quarter of

2008 at 1.95% and remained high in early 2009 at 1.94%. The high loss rates led to the failures

or buyouts of Countrywide and IndyMac Bank. The seizure of IndyMac cost the FDIC between

$4 billion and $8 billion and was the largest bank failure in over 20 years.

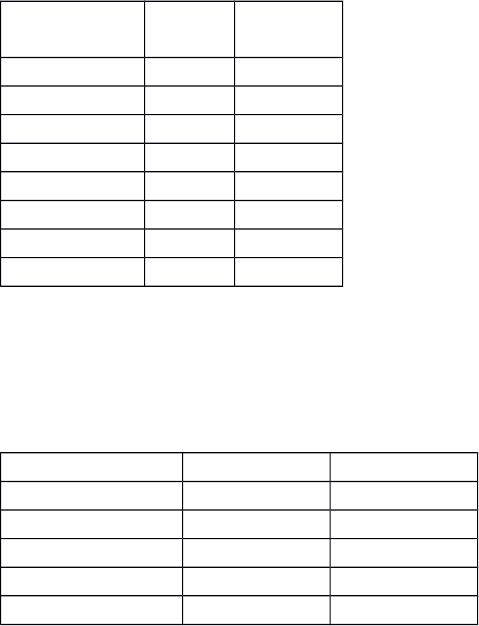

Bank failures by year (Source FDIC Historical Stats, 1st Quarter 2014)

#

Assets

(Bill $)

2007 3 2.615

2008 25 371.945

2009 140 169.709

2010 157 92.085

2011 92 34.923

2012 51 11.617

2013 24 6.044

2014 1st qtr 5 0.718

At the end of 2013 there were 467 banks on the problem bank list with assets of $153 billion.

More recent net charge off rates from the Quarterly Banking Profile reveal improving credit

conditions:

Net Charge-off Rates (NCOs) as of December 2010 & 1st Quarter 2014

All FDIC insured institutions

2010 2014

Overall 2.54% 0.52%

Real Estate 1.96% 0.24%

C&I 1.75% 0.23%

Consumer 2.05% 0.83%

Credit Card 10.08% 3.26%

Every category has improved significantly since 2010.