1.1.1.1.1Chapter Two

Determinants of Interest Rates

1.1.1.2 I. Chapter Outline

1. Interest Rate Fundamentals: Chapter Overview

2. Loanable Funds Theory

a. Supply of Loanable Funds

b. Demand for Loanable Funds

c. Equilibrium Interest Rate

d. Factors that Cause the Supply and Demand Curves for Loanable Funds to Shift

3. Movement of Interest Rates over Time

4. Determinants of Interest Rates For Individual Securities

a. Inflation

b. Real Risk Free Interest Rates

c. Default or Credit Risk

d. Liquidity Risk

e. Special Provisions or Covenants

f. Term to Maturity

5. Term Structure of Interest Rates

a. Unbiased Expectations Theory

b. Liquidity Premium Theory

c. Market Segmentation Theory

6. Forecasting Interest Rates

7. Time Value of Money and Interest Rates

a. Time Value of Money

b. Lump Sum Valuation

c. Annuity Valuation

1.1.1.3 II. Learning Goals

1. Know who the main suppliers of loanable funds are.

2. Know who the main demanders of loanable funds are.

3. Understand how equilibrium interest rates are determined.

4. Examine factors that cause the supply and demand curves for loanable funds to

shift.

5. Examine how interest rates change over time.

6. Know what specific factors determine interest rates.

7. Examine the different theories explaining the term structure of interest rates.

8. Understand how forward rates of interest can be derived from the term structure of

interest rates.

9. Understand how interest rates are used to determine present and future values.

1.1.1.4 III. Chapter in Perspective

This is the first of several chapters that familiarize students with the determinants of valuation of

bonds and related securities. In this chapter the authors first focus on the economic determinants

of interest rates using the flow of funds theory of interest rates. Subsequently, unique

characteristics of securities that give rise to different interest rates are discussed. This chapter

has four major sections. The first major topic covers interest rate formation in a ‘loanable funds’

framework. The loanable funds theory is the most basic explanation of real risk free interest rate

formation in the economy and is easily understood by students. The loanable funds theory

describes general economic forces in the economy that determine the opportunity cost of funds

which may be thought of as the real, riskless rate. The next section explains why individual

investments have different interest rates because of their unique characteristics. The effect of

maturity on interest rates is explained in greater detail in the term structure discussion. Three of

the main theories of the term structure are presented. The chapter then provides a brief example

of using term structure mathematics to forecast interest rates. The final section provides a review

of basic time value calculations. The sixth edition of the text drops the discussion of calculating

the effective annual rate that had been in prior editions.

1.1.1.5 IV. Key Concepts and Definitions to Communicate to Students

Real riskless rates vs nominal riskless rates Inflation

Compound and simple interest Default risk premiums

Annuity Liquidity risk premiums

Unbiased expectations Term structure

Liquidity premiums Maturity premiums

Market segmentation Future value and present value

Forward rates Safe haven

1.1.1.6 V. Teaching Notes

1. Interest Rate Fundamentals: Chapter Overview

1.1.2 The interest rates that you actually see quoted are nominal interest rates; as a

result, nominal rates are sometimes called ‘quoted rates.’ The purpose of the

chapter is to examine the components of the nominal interest rate. They are a) the

real riskless rate of interest that is compensation for the pure time value of money,

b) an expected inflation premium that is time dependent and c) a risk premium for

liquidity, default and interest rate risk.

2. Loanable Funds Theory

The interaction of supply and demand of funds sets the basic opportunity cost rate (real riskless

interest rate) in the economy. The Federal Reserve estimates supply and demand of funds from

households, business, government and foreign sources through its flow of funds accounts. Flows

of funds tables are available at the Federal Reserve website at www.federalreserve.gov. The

Federal Reserve (Fed) has pushed short term interest rates to near record lows in order to

stimulate the economy and has pursued a policy of quantitative easing (purchasing government

and mortgage debt by creating money) in an additional attempt to encourage spending and

investment. In mid-2013 the Fed announced it would begin gradually tapering its bond

purchases although the Fed has continued to promise to keep short term interest rates low well

into 2015.

a. Supply of Loanable Funds

Source Federal Reserve

Flow of Funds Matrix

Year 2012 data

Net Supply in Billions

of Dollars

Households & NPOs $982

Business Nonfinancial 219

State & Local Govt. -253

Federal Government -1,126

Financial Sector 56

Foreign 446

The predominant suppliers of loanable funds are households. Household savings rates have

increased since the financial crisis. The second largest net supplier of funds is the foreign sector.

The U.S. remains highly reliant on foreign sources of funds to meet our funds’ demands. This

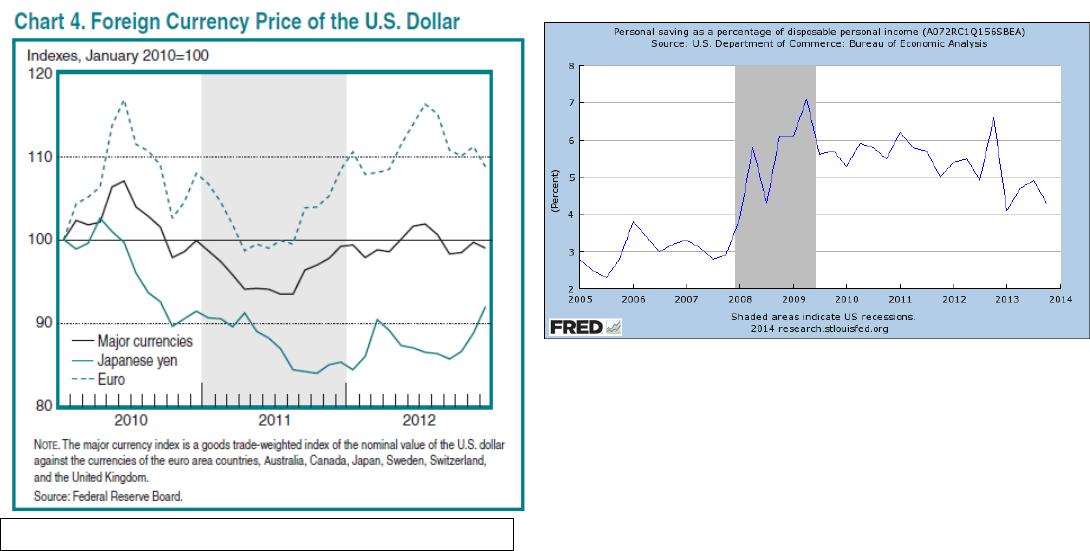

reliance becomes increasingly problematic with the continued long term fall in the value of the

dollar.

Household savings increase with higher interest rates and the supply curve is upward sloping

with respect to interest rates. However, the main determinants of household savings are 1)

income and wealth, the greater the wealth or income, the greater the amount saved, 2) attitudes

about saving versus borrowing, 3) credit availability, the greater the amount of easily obtainable

consumer credit the lower the need to save, 4) job security and belief about safety of the Social

Security system and 5) tax policy. In the U.S. tax policy favors borrowing but taxes virtually all

savings (except retirement savings). As a result, the supply curve is steeper than one might

expect. The instructor may wish to explain that at higher interest rates, savers do not have to

save as much to hit specified future values, so savings are not that sensitive to interest rates.

Where consumers put their savings is sensitive to interest rates, they move out of liquid accounts

as interest rates rise (as the price of foregoing higher rates of return to maintain liquidity rises).

Source: www.bea.gov/scb/pdf/2013/10%20October/1013_internaonal_services.pdf

Source: FRED data, Federal Reserve Bank of St. Louis

Households apparently try to smooth consumption patterns over different levels of income. As

income falls they save less to maintain consumption, as income rises households save more.

Other factors include the perceived riskiness of investments, near

term spending needs, Federal Reserve policy and general economic conditions. Favorable

economic conditions also increase savings by increasing income and wealth. Note that on net the

foreign sector is the second largest supplier of funds. Foreign funds suppliers examine the same

factors as U.S. suppliers except that they must also factor in expected changes in currency

values, global interest rates, different tax rates and sovereign risk. There is typically some built

in demand for U.S. investments however because the U.S. is considered a safe haven, i.e., a

country with relatively low political and economic risk and a stable currency.

The dollar is used to price many commodities, including oil and gold; the dollar is the primary

foreign currency reserve asset for many central banks and many exports are dollar denominated

even if the ultimate destination is not the U.S. Some feel that the dollar will lose its reserve

status eventually if China continues to grow and dominate Asia and if Europe increases its

commitment to growth policies while continuing to deconstruct some of their increasingly

expensive social welfare programs. The time frame required for a major shift away from the

dollar may be ten to twenty years or even much longer however, because China will remain far

too risky for quite a while and Europe must demonstrate a commitment to growth and solve its

Source: St. Louis Federal Reserve FRED data

sovereign debt problems. China has made several moves lately to free up yuan trading. China

now allows exporters to sell some of their foreign currency earnings, allows limited individual

trading in its currency and allows yuan financing in international markets. China still maintains

capital controls however.

Foreign central banks hold a large amount of foreign currency reserves, the bulk of which are in

dollars (about 60% of foreign currency reserves are in dollars).

Country Foreign Currency Reserves (all $ in billions)

China $3,317

Saudi Arabia 643

Russia 538

Taiwan 398

S. Korea 327

Source: Economist 2013

These high levels of reserves are indicative of foreign central bank activity to limit the growth in

the value of their currencies against the dollar. This may be done to stimulate their export

sectors. The dollars are often reinvested in the U.S., typically in Treasuries. This provides an

additional source of financing to the U.S. and helps remove a market discipline from U.S.

borrowers. Since the money is more or less automatically rechanneled into the U.S., U.S.

interest rates don’t rise as much as they would have otherwise when U.S. entities spend more

than their income and need to borrow the difference from overseas. This promotes overspending

by U.S. entities and can result in asset price bubbles similar to what happened in stocks in the

later 1990s and housing in the 2000s.

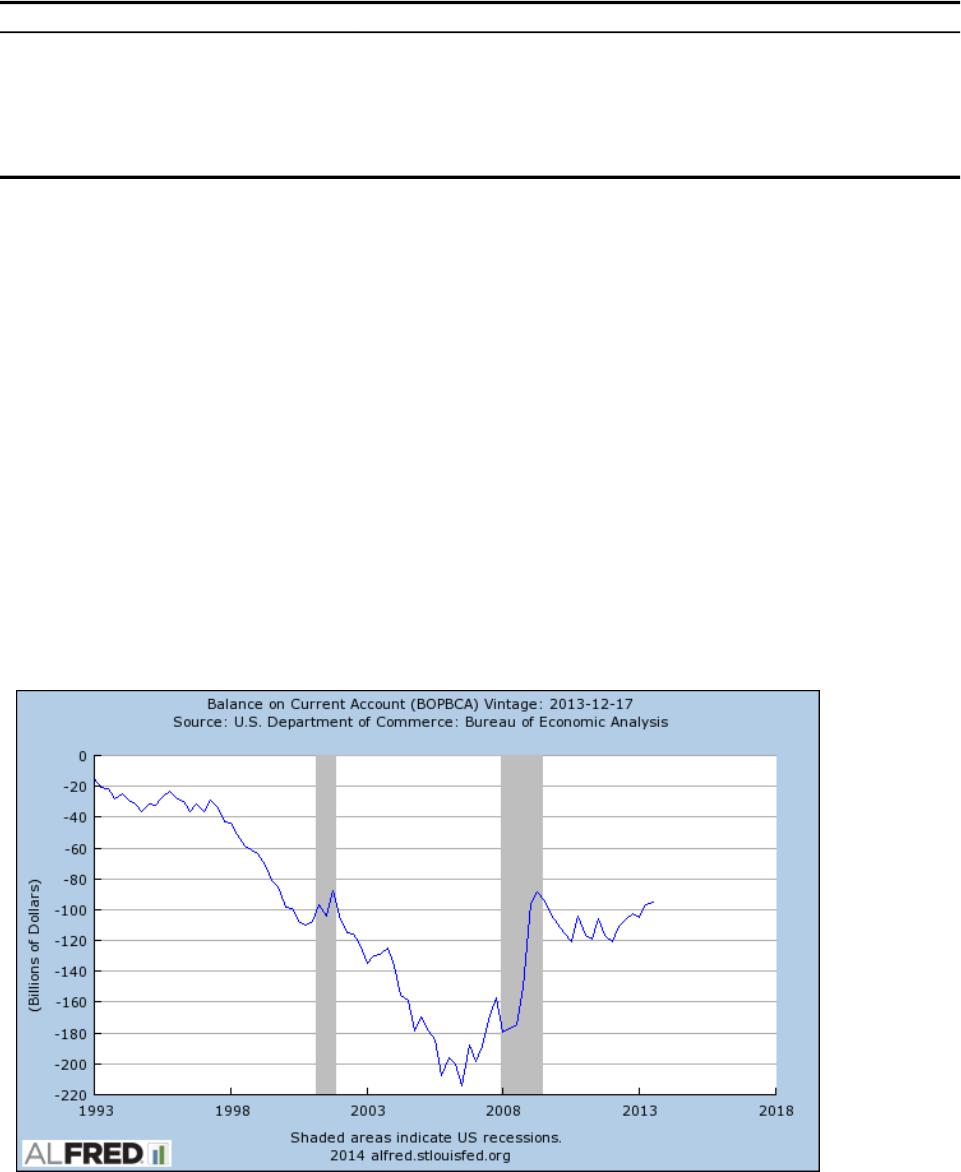

The negative balance on the U.S. current account (see below) represents excess importing over

exporting, or similarly, excess spending over income. The balance has to be financed with

capital account transactions or offset by changes in official reserves to prevent the dollar from

declining. For the most part the balance is maintained by borrowing from overseas (and net

selling of U.S. assets to foreigners). The U.S. net indebtedness to the rest of the world was about

$4.46 trillion in 2013 (about 27% of GDP).

Whether or not this is a serious problem depends on how much money is reinvested in the U.S.

and how we use the money reinvested. It certainly points out the U.S. dependence on foreign

funds.

b. Demand for Loanable Funds

The quantity of loanable funds demanded is greater at lower interest rates. Businesses prefer to

finance internally when interest rates are high. The demand for loanable funds by households for

big ticket items is quite sensitive to interest rates as these items comprise a large percentage of

their budget (homes, autos, boats, etc). The Federal government’s demand for funds is relatively

insensitive to interest rates, but not wholly so because much of the interest owed on the Federal

debt is financed by borrowing. As interest rates rise, the Federal government has to borrow more

to pay off the interest on the existing debt. The Federal budget is likely to remain in deficit for

the next 10 years at least.

State and local government financing is also quite sensitive to interest rates. New municipal

offerings drop when interest rates rise. Not surprisingly, government entities that cannot print

money (or raise taxes) are more sensitive to financing costs! Many states are now in financial

difficulty because many are required to balance their budgets under state laws, and the recession

has decreased the amount of tax revenues and increased state spending on assistance programs.

Moreover, the weaker economy has highlighted the overly generous pension benefits promised to

state workers that now look unaffordable as federal stimulus money ends.

c. Equilibrium Interest Rate

It is the job of the 12 Federal Reserve banks to estimate aggregate supply and demand of funds

from the various sectors at different interest rates and then build the aggregate supply and

demand curves. In free capital markets the interest rate observed will tend toward equilibrium at

the rate that intersects the supply and demand curves for each traded instrument.

d. Factors that Cause the Supply and Demand Curves for Loanable Funds to Shift

1.1.2.1.1.1.1 Increase in Affect on Supply Affect on Demand

Wealth & income Increase N/A

As wealth and income increase, funds suppliers are more willing to supply funds to

markets. Result: lower interest rates

Risk Decrease Decrease

As the risk of an investment decreases, funds suppliers are less willing to purchase the

claim. All else equal, demanders of funds would be less willing to borrow as well.

Result: higher interest rates

Near term spending needs Decrease N/A

As current spending needs increase, funds suppliers are less willing to invest. Result:

higher interest rates

Monetary expansion Increase N/A

As the central bank increases the supply of money in the economy, this directly increases

the supply of funds available for lending. Result: lower interest rates

Economic growth Increase Increase

With stronger economic growth, wealth and incomes rise, increasing the supply of funds

available. As U.S. economic strength improves relative to the rest of the world, foreign

supply of funds is also increased. Business demand for funds increases as more projects

are profitable. Result: indeterminate effect on interest rates, but at more rapid growth

rates interest rates tend to rise.

Utility derived from assets Decrease Increase

As utility from owning assets increases, funds suppliers are less willing to invest and

postpone consumption whereas funds demanders are more willing to borrow. Result:

higher interest rates

Restrictive covenants Increase Decrease

As loan or bond covenants become more restrictive, borrowers reduce their demand for

funds. Result: lower interest rates

Tax Increase Decrease Increase

Taxes on interest and capital gains reduce the returns to savers and the incentive to save.

The tax deductibility of interest paid on debt increases borrowing demand. Result:

Higher interest rates

Currency Appreciation Increase N/A

Foreign suppliers of funds would earn a higher rate of return if the currency appreciates

and a lower rate of return measured in their own currency if the dollar depreciates.

Foreign central banks often buy U.S. Treasury securities as part of their attempts to

prevent their currency from appreciating against the dollar.

Result: Lower interest rates

Expected inflation Decrease Increase

An increase in expected inflation implies that suppliers will be repaid with dollars that

will have less purchasing power than originally anticipated. Suppliers lose purchasing

power and borrowers gain more than originally anticipated. This implies that supply will

be reduced and demand increased. Result: Higher interest rates

The marginal propensity to consume (MPC) and the marginal propensity to save (MPS) affect

household choices of how much of their income they wish to spend and save respectively. The

MPC had increased (and the MPS decreased) inter-generationally in the U.S. before the financial

crisis. This change probably came about because of reduced stigma associated with debt and

increased availability of credit. Since the crisis the amount of consumer credit to riskier

individuals has declined, along with income growth, and one would thus expect savings rates to

be higher than during the boom years.

3. Movement of Interest Rates Over Time

Interest rates fluctuate in a nearly continuous manner due to the actions of traders. In a free

market (capitalist) society, governments do not set prices. Interest rates are the price of

borrowing money associated with a specific instrument or claim. Actions to buy, sell and issue

securities affect interest rates. In turn, demand and supply of funds fluctuate daily as current and

expected macro and instrument specific conditions evolve.