1.1.1.1.1Part V: Risk Management in Financial

Institutions

1.1.1.1.2

1.1.1.1.3Chapter Nineteen

Types of Risks Incurred By Financial Institutions

1.1.1.2 I. Chapter Outline

1. Why Financial Institutions Need to Manage Risk: Chapter Overview

2. Credit Risk

3. Liquidity Risk

4. Interest Rate Risk

5. Market Risk

6. Off-Balance-Sheet Risk

7. Foreign Exchange Risk

8. Country or Sovereign Risk

9. Technology and Operational Risk

10. Insolvency Risk

11. Other Risks and Interactions among Risks

II. Learning Goals

1. Describe the major risks faced by financial institutions.

2. Recognize that insolvency risk is a consequence of the other types of risk.

3. Understand how the various risks faced by financial institutions are related.

1.1.1.3 III. Chapter in Perspective

In Part V the text provides a more detailed examination of risk management at financial

institutions. Chapter 19 provides an introduction to Chapters 20-24 by discussing why risk

management is crucial to today’s institutions and by categorizing the major risks faced by

financial intermediaries. The subsequent chapters highlight a specific component of risk, or a

specific tool to manage risk and provide current applications. The chapters in Part V ask the

reader to apply their knowledge of both markets and derivatives to risk management problems at

intermediaries. Many texts include applications of risk management with the chapter on

derivatives, or with the chapter about the specific intermediary’s line of business. The text

authors have separated the introductory chapters from the risk management chapters so that the

instructor can cover some, all or none of the applications chapters. Chapters 20 through 24 are

more difficult than the prior chapters because of the applications covered, although they are still

suitable for an introductory level course. To help ensure readability, many of the mathematical

applications are relegated to appendices. Chapter 20 covers the management of credit risk that

arises from balance sheet activity. Chapter 21 illustrates the management of liquidity risk.

Chapter 22 develops tools to manage interest rate risk and institutional insolvency risk with the

repricing and duration gaps. Chapter 23 presents the use of derivatives to manage risk and

Chapter 24 covers loan sales and securitization.

1.1.1.4 IV. Key Concepts and Definitions to Communicate to Students

Credit risk Letter of credit

Firm specific credit risk Foreign exchange risk

Systematic credit risk Country or sovereign risk

Liquidity risk Technology risk

Interest rate risk Operational risk

Market risk Insolvency risk

Off balance sheet risk Interactions among risks

Net interest margin Refinancing risk

Reinvestment risk Primary and secondary claims

Off balance sheet risk Event risk

1.1.1.5 V. Teaching Notes

1. Why Financial Institutions Need to Manage Risk: Chapter Overview

The goal of a FI is the same as any for profit corporation, namely to maximize shareholder

wealth. The major difference between a financial institution and a nonfinancial corporation is in

the nature of their assets and liabilities and the degree of regulation. A majority of financial

firms’ assets are pieces of paper. They are not readily differentiable from assets of competitors;

this leads to very low ROAs as discussed in Chapter 13. In order to offer shareholders a

competitive rate of return, FIs must therefore incur substantial risk. This risk takes the form of

using a high amount of leverage, investing in assets riskier than the liability positions funding

them and maintaining minimal liquidity positions. Consequently, small errors in judgement can

have serious negative consequences for the solvency of FIs. Because many institutions depend

upon the public’s perception of their soundness to attract business, events that erode the public’s

confidence in one or several large domestic or foreign FIs can quickly spread and lead to major

profit and solvency problems in many FIs.1 The following sections outline the major risks faced

by FIs today.

2. Credit Risk

Credit risk is the possibility that a borrower will not repay principle and interest as promised in

1The fear of contagion effects has encouraged regulators to bail out many insolvent or near

insolvent financial institutions around the world including the March 2008 bailout of Bear

Stearns engineered by the Federal Reserve. As it turned out more failures did occur due to the

severity of the financial crisis.

a timely fashion. To limit this risk, FIs engage in credit investigations of potential funds

borrowers, or in the case of investments they may rely on externally generated credit ratings. FIs

lend to many different borrowers to diversify away firm specific (borrower specific) credit

risk. Systematic credit risk will remain (credit risk due to ‘systemic’ or economy wide risks

such as inflation and recession) even in a well diversified portfolio. Many of the S&L problems

of the 1980s can be attributed to an underdiversified loan portfolio overexposed to certain types

of lending in certain regions. Chapters 20 and 24 provide methods of assessing and managing

credit risk.

Banks, thrifts, mutual funds and life insurers usually face more credit risk than certain other

intermediaries such as MMMFs and P&C insurers because the former tend to have longer

maturity loans and investments.

Teaching Tip: What may appear to be relatively small loss rates can quickly bring about the

threat of insolvency at depository institutions (DIs). For instance, unexpected loss rates of 5% to

6% of the total loan portfolio can easily cause a bank to fail. Most charge off rates on specific

types of loans are much lower than this amount at well managed banks, although credit card loss

rates are significantly higher than most other types of domestic loans. Foreign lending,

particularly sovereign lending, has traditionally been the most risky throughout all of the history

of banking and has led to the loss of many fortunes and caused many failures.

Teaching Tip: Only the unexpected portion of loan losses generates solvency risk per se because

banks set aside an allowance for loan loss account against to cover expected loan losses.

Net charge offs (NCOs) vary by loan type. Text Figure 19-1 illustrates that credit card NCOs

were quite high after the financial crisis, peaking at an all-time high of 13.21% in March 2010

before falling to 3.28% in early 2014 according to the FDIC Quarterly Banking Profile. The

credit card market is quite large at $3.261 trillion in 2013, although it has declined from

pre-crisis levels. Charge offs of C&I loans and charge offs on real estate loans also rose during

the crisis (as high as 2%) but net charge offs in 2014 were 0.23% and 0.24% respectively.

The Bankruptcy Reform Act was passed in October 2005. The Act made it more difficult for

higher income individuals to seek bankruptcy protection. As the text indicates there was a large

spate of filings before the act went into effect followed by a large drop off in filings afterwards.

Filings then increased during and subsequent to the financial crisis in the late 2000s. Bankruptcy

filings have generally trended down since the recovery although there was an increase in 2012.

3. Liquidity Risk

Liquidity risk arises because there is a mismatch in the terms and maturity of a FI’s assets and

liabilities. In many cases liabilities either have an uncertain maturity (they are due upon demand

for instance), or they have a shorter maturity than the assets. Many FI’s assets are also less liquid

than the FI’s liabilities. Even if the existing assets and liabilities were perfectly maturity

matched, loan commitments and the undesirability of turning away potential loan customers

would lead to liquidity risk as borrowers increased their take downs or new loan customers

arrived unexpectedly at the FI. FIs maintain precautionary liquid assets to meet unexpected

liquidity needs and may purchase liquidity via brokered deposits, fed funds borrowed, reverse

repos or via other short term financing sources. Chapter 21 covers liquidity risk and liquidity

management at FIs. The Fed lowered interest rates, including the discount rate, during the

subprime crisis to encourage lending during the liquidity problems in the short term markets

engendered by the subprime crisis. The Fed even opened up discount window borrowing to

non-bank institutions that are not extensively regulated such as securities brokers. IndyMac

failed in 2008 in the midst of a liquidity crisis. As news spread that IndyMac was in trouble

depositors began to withdraw large sums from the bank, even those under the FDIC insurance

limit. Within a week the FDIC was forced to take over the bank. IndyMac was later acquired

by One West Bank Group.

4. Interest Rate Risk

Interest rate risk arises from intermediaries’ function as an asset transformer. Recall that many

intermediaries invest in direct claims issued by borrowers (assets) while providing separate

claims to individual savers (liabilities). This process is a form of maturity intermediation. The

maturity of a FI’s assets will normally differ from the maturity of its liabilities. When this is the

case changes in interest rates can lead to changes in profitability and/or equity value. These

changes caused by unexpected movements in interest rates give rise to interest rate risk. Banks

and thrifts engage in maturity intermediation to a greater extent than other institutions such as

life insurers. Consequently the former two types of FIs face more interest rate risk.

In general, if an institution has longer maturity assets funded by shorter maturity liabilities, it is

at risk from rising interest rates. Suppose the FI has two year fixed rate assets funded by one

year fixed rate liabilities. The FI’s liabilities will reprice sooner than its assets. If interest rates

rise, the cost of funding on the liabilities will increase in one year, but the income from the assets

will remain the same throughout the second year, reducing the net interest margin. The

institution has refinancing risk because the liabilities must be rolled over or reborrowed before

the assets mature. Refinancing risk is the risk that at rollover dates the liability cost will rise

above the asset earning rate.2

An institution in this situation will however benefit from declining interest rates.

The converse also holds. Institutions with an asset maturity shorter than the liability maturity will

benefit from rising interest rates, but will be hurt by falling interest rates. If the assets mature

more rapidly than the liabilities then the institution faces reinvestment risk. Reinvestment risk is

the risk that the returns on funds to be reinvested will fall below the cost of those funds.

Teaching Tip: These ideas are easily illustrated as follows:

A FI has $100 million of fixed earning assets that mature in 2 years. The assets earn an average

of 7%. These are funded by 6 month CD liabilities paying 4%. So in this case the asset maturity

is longer than the liability maturity. The bank’s Net Interest Margin (NIM) = [(7% – 4%)*$100

million] / $100 million = 3%. If in 6 months interest rates increase 100 basis points, the 2 year

assets will still be earning 7%, but the new 6 month CDs will have to pay 5%, reducing the NIM

by one-third to 2%. This illustrates refinancing risk.

Although changes in profitability affect equity value, the effect of a change in interest rates can

2 Refinancing risk would also encompass increases in rates that reduced the NIM, even if it did

not become negative.

be more directly measured by examining how the present value of the existing assets and

liabilities will change as interest rates change.3 The conclusions are similar to above. A FI with

longer term (duration) assets funded by shorter term (duration) liabilities will suffer a decline in

the market value of equity if interest rates rise. This occurs because the market value of the

assets will decline more sharply than the market value of the liabilities.

Causes and measures of interest rate risk are provided in Chapter 22; using derivatives to hedge

interest rate risk is presented in Chapter 23.

5. Market Risk

Market risk arises when FIs take unhedged positions in securities, currencies and derivatives.

Income from trading activities has increased in importance during recent years. In general, the

volatility of asset prices and currency values causes market risk.

Teaching Tip: The failure of Barings bank is an extreme example of market risk (see the Off

Balance Sheet section).

Bank assets and liabilities can be separated into ‘banking book’ and ‘trading book’ assets or

liabilities based on the account’s maturity and liquidity. Trading book accounts are on and off

balance sheet accounts that are held for a short time period and are generally speculative in

nature. They are held in hopes of generating price gains or as part of making a market in a given

security or contract. Banking book accounts are those held for longer time periods and generate

interest income or provide long term funding.

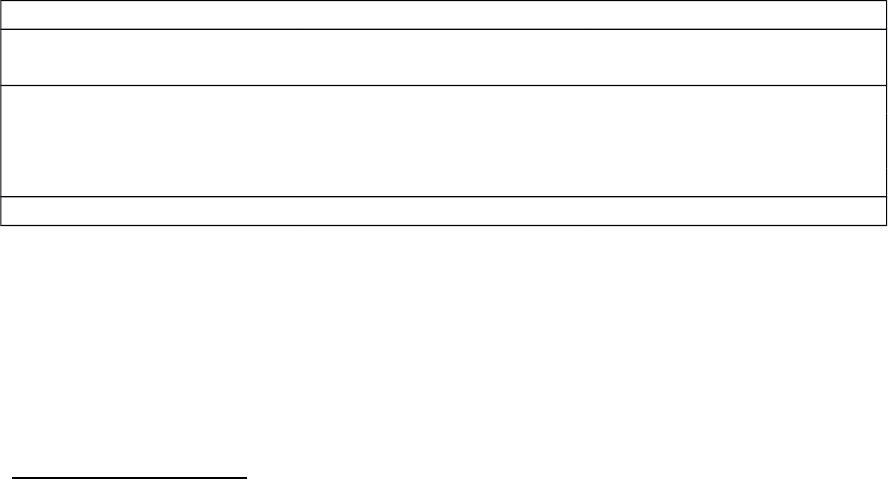

Text Table 19–3 with examples of both is reproduced below:

Assets Liabilities

Banking Book Loans Capital

Other illiquid assets Deposits

Trading Book

Bonds (long) Bonds (short)

Commodities (long) Commodities (short)

FX (long) FX (short)

Equities (long) Equities (short)

Off Balance Sheet Derivatives (long) Derivatives (short)

Value at Risk (VAR) is a relatively new method of assessing overall institutional risks.4 VAR

attempts to measure the maximum dollar amount a FI is likely to lose in a given short time

period, usually a day, with some probability.

Teaching Tip: The VAR is a probabilistic method that estimates the likely loss that could occur at

a given confidence interval (usually 95%). A simple VAR model would attempt to identify and

estimate likely values for the major portfolio risk factors, such as stock price changes, currency

3The text labels this risk “present value uncertainty or price risk.” It arises from a difference

in the duration of the FI’s assets and liabilities.

4The text also uses the term Daily Earnings At Risk or DEAR.

changes, interest rate changes, etc. Based on either the factor’s historical variability or the use of

Monte Carlo simulation the VAR model attempts to estimate the likely changes of each variable

over the time interval, incorporating the correlations between the variables so that the FI can

more realistically estimate the maximum loss likely to occur with 95% confidence. VAR was

originated by J.P. Morgan and information about VAR may also be found at their website under

the title Risk Metrics.

The financial crisis provides a perfect illustration of how seriously market risk can affect an

institution’s balance sheet. When the mortgage market began to meltdown many institutions took

large losses on mortgage backed securities (MBS). The securitization market stopped

functioning and banks had to hold their securities as losses built. The securities even became

known as ‘toxic’ assets. The result was the failure of Lehman, the buyout of Merrill Lynch and

Washington Mutual. As a result of these events in 2008 the Dow fell 500 points, then the biggest

drop in seven years and global markets followed suit.

6. Off-Balance-Sheet Risk

The last twenty years have brought about tremendous growth in off balance sheet activities

ranging from loan commitments to swaps to OTC derivatives. Commercial banks alone held off

balance sheet claims of $233.853 trillion in 2013, a staggering number.5 Derivatives allow

institutions to reduce risk arising from other aspects of their business, offer risk reduction

services to their clients, and to generate income growth through fees without growing the balance

sheet. The latter is important because of regulations associated with balance sheet growth

(particularly capital regulations).

On balance sheet activities are current primary claims (assets) or current secondary claims

(liabilities). Off balance sheet activities are contingent claims that can affect the balance sheet

in the future. A letter of credit is used as an example in the text. A letter of credit issued by a FI

is a contingent promise to pay off a debt if the primary claimant fails to pay. Profitability is the

incentive driving the off balance sheet business. FIs are generating fee income to reduce the

dependence on interest rate spreads and because of the increased competitive pressures on their

traditional lines of business. Off balance sheet assets and liabilities have grown so much that

ignoring them may generate a significantly misleading picture about the value of stockholder’s

equity. Net worth (NW) is properly measured as

NW = MVAssetsOn – MVLiabilitiesOn + MVAssetsOff – MVLiabilitiesOff

where MV stands for market value of the given category.

There are many off balance sheet activities including:

Loan commitments

Mortgage servicing contracts

Positions in forwards, futures, swaps and other derivatives (mostly by the largest FIs)

5 This number significantly overstates the size of actual bank commitments because the number

includes notional principal amounts which are not actually at risk and does not represent net

payments due on these contracts.

Two aspects of certain types of derivatives lead to additional risks involved with their usage.

First, calculating derivative values and payouts is complicated. This is particularly true for

many OTC derivatives that banks sell. The selling banks typically understand the risks better

than the clients. Second, derivatives typically involve large amounts of leverage. These two

attributes imply that misuse of derivatives is likely to occur, and can result in extreme losses (or

extreme gains, but rarely are the winners upset about those). There have been many cases in

recent years where derivatives usage has led to problems:

1. In 2012, Bruno Iksil, a trader for J.P. Morgan Chase, made large bets (the so called

London Whale) by trading credit default swaps on an index of corporate bonds that

eventually cost the bank about $6 billion.

2. In February 2008, Societe Generale, a large French bank, indicated that a rogue trader,

Jerome Kerviel had generated $7.2 billion in losses on futures trades. 6 This was the

largest market risk related loss ever. Kerviel used his knowledge of the “back office”

order processing systems to hide trades.

3. In 1995 Barings Bank failed when a so called ‘rogue trader,’ Nick Leeson, bankrupted

Barings after the bank allowed him to run up extremely large losses in futures and option

trading on Tokyo and Singapore derivatives exchanges. Interestingly, Barings did not

complain when he supposedly generated large gains for the bank and allowed Leeson to

run back office order processing as well as trading activity, a clear violation of sound

internal control procedures.

4. In 1995, a trader at Sumitomo incurred losses of $2.6 billion from commodity futures

trading. Losses of this size just shouldn’t happen if the bank’s internal controls are

functioning properly.

5. Bankers Trust sold several complicated OTC swaps to customers. In one of the swap

deals the customer (Gibson Greeting Cards) had to make variable rate payments based on

Libor2. In the second swap deal with Procter and Gamble, P&G would have to make

high variable rate payments if either short term or long rates rose, and extremely high

variable rate payments if both rose, which is what happened. Both customers sued

Bankers Trust claiming they did not understand the risks they were facing. The fallout

helped lead to the Deutsche Bank takeover of BT.

6. Orange County investment advisor Bob Citron, a portfolio manager with very little

formal finance or investment training, purchased structured notes from Credit Suisse First

Boston. The notes were a type of inverse floater that would drop in value if rates

increased, which of course they did. Citron had used an extreme amount of leverage in

an attempt to earn higher returns (which he did for several years). When rates rose,

losses mounted quickly and he could not repay the borrowings and the municipality went

bankrupt, losing $1.5 billion. Twenty banks were sued; CSFB paid $52 million to settle

charges.

After the fact, the problems in the financial crisis indicate that banks hid risks in their derivatives

activities and did not have sufficient capital to back these commitments. Losses on MBS and

collateralized mortgage obligations (CMOs) were very high. Recovery rates on CMOs ranged

from only $0.05 to $0.32 per dollar of par value. Investors purchased claims in very complex

instruments that turned out to be very risky. One reason they did so was because of high ratings

6 Apparently a ‘rogue’ trader is one who gets into trouble.

from the credit ratings agencies. In some cases the securities were so complicated that ratings

agencies and regulators had to rely on the bankers’ assessment of the riskiness of the securities.

This is obviously a flawed operating procedure. Part of the problem has been an overreliance on

mathematical risk modeling. Actually, I don’t believe the pricing models were seriously flawed.

Rather the inputs were developed by statisticians who relied excessively on historical data, rather

than examining whether future economic conditions supported such conclusions.

Credit line draw-downs rose dramatically in 2008. Firms like GM maxed out their credit line

borrowing as other short term money sources dried up. Unused commitments on lines fell

sharply and about 45% of banks announced commercial loans increases associated with

previously arranged credit lines. The draw-downs increased liquidity problems at some FIs, and

in response the Fed created the Commercial Paper Funding Facility (CPFF), to assist in funding

for short term markets. The Fed began purchasing commercial paper to assist funding of

institutions and corporate issuers of paper.

Teaching Tip: To what extent do these problems imply we should limit derivatives usage? Are

we comfortable with the caveat emptor philosophy currently employed? Even after

Dodd-Frank, the regulators have trouble keeping track of this market. In 2014 the CFTC

admitted to misstating the size of the credit default swap market by an estimated $250-$300

billion and in 2013 the Depository Trust & Clearing Corporation (DTCC) underestimated swap

notional principals by about $55 trillion.7

7 Acknowledging Mistake, U.S. Regulators Still Struggle to Oversee Derivatives Market: CFTC

Says It Published Inaccurate Data on Swaps Similar to ‘London Whale’ Going Back to

November, by Andrew Ackerman and Katy Burne, The Wall Street Journal Online, May 1, 2014.