Chapter 18 – Pension Funds 6th Edition

1. Financial Asset Investments and Recent Trends

a. Private Pension Funds

Major assets include 2002 2004 2007 2010 2013

Corporate equities 45.75% 38.03% 47.27% 32.37% 30.89%

Mutual fund shares 15.88% 26.41% 27.75% 34.10% 35.98%

Treasury and agency securities 8.16% 7.49% 6.75% 11.12% 7.40%

Corporate and foreign bonds 8.05% 7.45% 5.22% 8.29% 5.97%

Over the period private pension plans have shifted assets out of direct ownership of

equities into mutual funds. Funds increased holdings of Treasuries and agencies in 2010

before reducing the percentage in 2013.

Pension funds are the largest institutional investor in the U.S. stock market. Growth in

pension fund assets has been phenomenal. The percentage invested in equities increased

during the strong bull markets of the 1990s, but had fallen from the 1999 level of 50.7%

in 2004 only to recover by 2007. The financial crisis led to a reduction in overall equity

investments that is still ongoing.

In 2013 defined benefit plans held 41.11% of their assets in equity and 15.92% in mutual

funds for a total of 57.03%. Defined contribution plans held 24.77% in equities and

47.96% in mutual funds for a total of 72.73%. Defined contribution plans directly held

less fixed income securities than defined benefit plans. The defined benefit plans appear

to be slightly more conservative than DC plans.

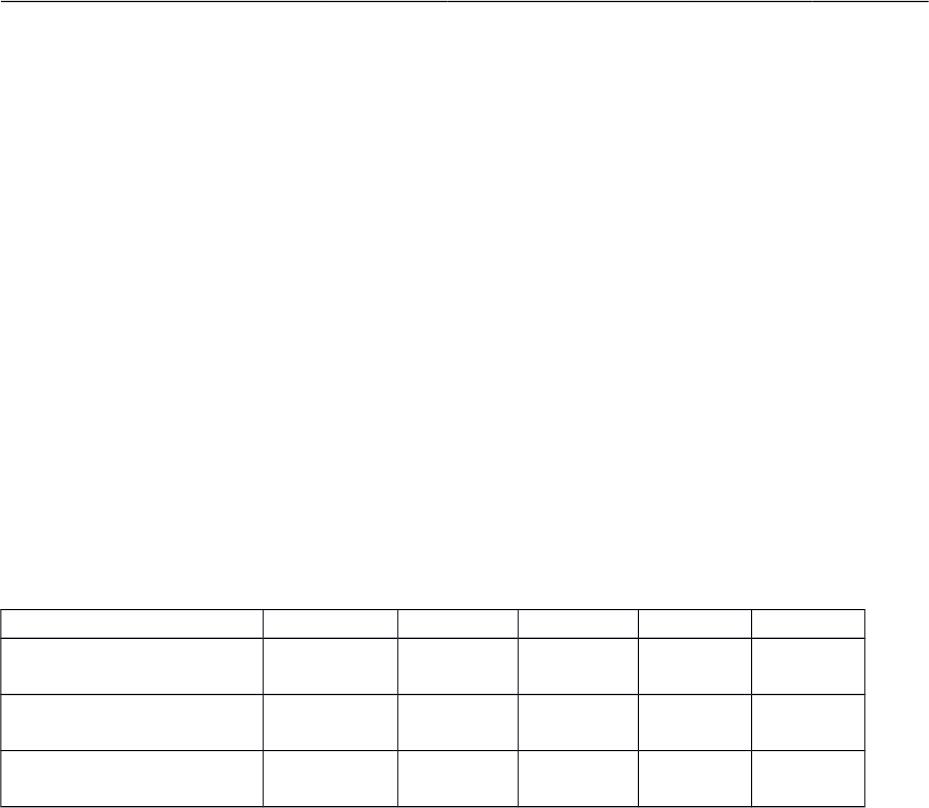

b. Public (State & Local) Pension Funds

Major assets include 2002 2004 2007 2010 2013

Corporate equities 55.99% 58.13% 64.03%

58.97

%

63.83

%

Treasury and agency

securities 17.82% 14.75% 14.45%

17.22

%

12.45

%

Corporate and foreign

bonds 15.72% 16.08% 7.91%

11.40

% 8.55%

Investment in equities increased substantially before the financial crisis and has risen in

2013 after dipping in 2010. Note that public pension funds hold more fixed incomes than

private plans.

Social Security contributions are invested in Treasuries. The low rate of return on

Treasuries and the increasing age of the population are contributing factors to the

impending SS insolvency.

2. Regulation of Pension Funds

The Employee Retirement Income Security Act (ERISA) is a major piece of regulation

covering retirement funds. The Department of Labor enforces ERISA. The major

provisions include:

Minimum funding requirements for private pension defined benefit plans.

18–1

Chapter 18 – Pension Funds 6th Edition

Maximum time period (10 years) for vesting of employee benefits. Vesting refers to

the time period required until the employee ‘owns’ any employer contributions to the

employee’s pension plan.

Establishment of the prudent man rule. This rule requires pension funds to invest the

money as if they were ‘prudent.’ Prudent was purposefully left undefined.

Allowing employees to transfer pension benefits from one employer to another.

Established the Pension Benefit Guarantee Corporation (PBGC or ‘Penny

Benny’) to insure benefits in defined benefit plans.

In 1994 the Retirement Protection Act increased premiums on underfunded plans. In

1999 PBGC came under fire for failing to notify beneficiaries of failed plans the full

amounts they were owed (some waited over 13 years!) and for poor internal control

procedures. PBGC charges premiums for insurance. In 2011 the rates were $35 per

participant for single employer plans and $9 per participant for multi-employer plans in a

fully funded plan. Underfunded plans pay an additional $9 per $1,000 of vested benefits.

Nevertheless PBGC has continued to generate operating losses.

The PBGC was responsible for pensions for over 1.5 million people. Workers in a failed

defined benefit plan may not receive full benefits because PBGC payouts are capped. In

2012 unfunded pension liabilities were an estimated $470 billion. Pension funds

continue to use unrealistically high expected rates of returns on investments so the actual

amount of underfunding is even greater. Nevertheless most of the companies with

pension liabilities are sound and can pay more to fund their pension liabilities if needed.

The PBGC does not have enough capital to withstand many large corporate failures with

underfunded plans. The PBGC’s loss exposure in 2012 was estimated at $295 billion.

The Pension Protection Act of 2006 increased premiums from $19 to $30 for funded

plans and instituted cost increases for underfunded plans tied to the amount the plans

were underfunded. These amounts are now higher at $49 in 2014 for single-employer

plans and $12 for multiple employer plans. Plans now have five years to reduce the

underfunding. Disclosure to employees about the extent of the deficit was also required.1

3. Global Issues

Pension plans vary across the European Union (EU). Most EU countries are working

toward establishing and improving private pension plans and reducing public pension

plans. Funding levels of plans vary from country to country, but there is general

agreement concerning the need to increase plan funding. The EU would like to

encourage standardization to encourage portability of pension benefits and free

movement of capital among member countries.

1 Britain created its own version of the PBGC called the Pension Protection Fund and it

too is having funding problems.

18–2

Chapter 18 – Pension Funds 6th Edition

In general one can classify European pension plans as to whether the link between the

amount paid in and the benefits received is weak or strong:

In countries with weak linkages such as France and Germany the benefits tend to be very

generous relative to amounts paid in. These plans are more costly, with average

expenditures on state pensions at over 10% and projected to rise to 14% by 2040 (U.S.

expenditure is 4.3% and Britain’s is 5.5%). Some of these plans are quite complex and

generous. Certain public workers in France can retire on full or near full benefits at age

55 for instance although in 2010 France’s parliament passed a bill to increase the

retirement age from 60 to 62. As part of the bailout plan organized by the IMF, Greece

had to agree to raise its retirement age from 65 to 67. Weeks of strikes in Greece, France

and Spain followed these and other modest reforms.

As noted before part of the pension problem in the U.S. arises from the aging of the

population. However, Europe is aging more rapidly than the U.S. Italy in particular will

have serious funding problems unless their demographics change. Japan is also aging

rapidly and will face growing funding problems in both retirement and health care.

Typical responses to the funding problems of public pensions are benefit reductions,

requirements or incentives to work longer, and privatization. Sweden, Britain,

Argentina, Australia and Chile have all added privatization elements to their public

pension plans with varied success, but generally speaking the plans have resulted in better

fiscal situations and reasonable returns to participants. There are lessons to be learned

from examining overseas pension plans (See Articles #1 and #3 for more details).

Generally speaking privatization can work but transition costs can be high, the options

should probably be kept simple, such as indexing or some limited choice of mutual funds,

and the government will have to work to keep costs down and prevent fraud.

The text refers to public pensions primarily but several European companies face large

unfunded pension liabilities as well. For instance according to Article #2 below,

Volkswagen, British Airways and Daimler-Chrysler have unfunded pension liabilities of

between 50% and 80% of market capitalization.

18–3

Link between payments &

benets

Weak

France

Germany

Strong

UK, Sweden,

Italy, Chile

Italy

Chile

Chapter 18 – Pension Funds 6th Edition

Appendix 18A: Calculation of Growth in IRA Value During an Individual’s Working

Years (available in Connect or from your McGraw-Hill representative)

The appendix depicts the growth of an initial $10,000 in an IRA with an annual

contribution of $5,000 in a retirement account. The calculations show the amount of fund

contributions and earned interest.

Sources and for more information see the following:

1. “From Nations That Have Tried Similar Pensions, Some Lessons” By Bob Davis

and Matt Moffett Staff Reporters of The Wall Street Journal, February 3, 2005;

Page A.1

2. “European pension accounting: Painful,” From The Economist print edition, Nov

11th, 2004.

3. “Other countries’ pension policies: Horror movies? Not really,” From The

Economist print edition, Feb 10th 2005

4. “The Basics of Social Security, Why It’s at a Crossroads Now, And What It Might

Become,” By David Wessel, Staff Reporter of The Wall Street Journal,

February 1, 2005; Page B1

5. “Pension Agency’s Gap Is Expected To Balloon to $71 Billion in Decade,” By

Michael Schroeder, Staff Reporter of The Wall Street Journal June 9, 2005;

Page A4

1.1.1.1 VI. Web Links

http://www.ssa.gov/ Social Security’s website

http://www.wsj.com/ Website of the Wall Street Journal Interactive edition. The

web version of the well known financial newspaper can be

personalized to meet your own needs. Instructors can also

receive via e-mail current events cases keyed to financial

market news complete with discussion questions.

http://www.economist.com The website of the Economist, one can search for

information about pension plans in different countries and

about the effects of privatization.

http://www.dol.gov/ U.S. Department of Labor website. The DOL administers

ERISA and the full text of ERISA is available here.

http://www.ici.org Investment Company Institute website. See the Mutual

Fund Factbook for industry statistics on IRAs.

http://www.pbgc.gov/ The Pension Benefit Guaranty Corporation website.

http://www.retirementplanners.com A good website with a wealth of information on

different types of retirement plans.

18–4

Chapter 18 – Pension Funds 6th Edition

1.1.1.1.1.1 VII. Student Learning Activities

1. Go to the Social Security website http://www.ssa.gov/ and find the retirement

calculator. (This calculator may not work for Macs.) Enter your age (at least 23) and

your expected annual income using the ‘quick’ version of the calculator found under

‘benefit calculators.’ What levels of inflated Social Security earnings can you expect

at retirement? Does it matter at what age you retire? How much longer would you

have to live to make it worthwhile to retire at the minimum possible age rather than

the latest age?

2. Using the comparison calculator between a Roth IRA and a regular IRA found at

http://tcalc.timevalue.com/ decide whether an individual with the following data is

better off with a regular IRA or a Roth IRA:

Current IRA amount: $10,000

Current tax bracket: 28%

Retirement tax bracket: 15%

Projected rate of return on investments: 8%

Planned saving amount is $2,000 per year, (before taxes)

Retire in 30 years

3. Go to http://www.asec.org/int-blpk.htm and use the calculator there to ascertain how

much one needs to invest per year to generate adequate retirement income given the

following data:

Income of $60,000 per year

Age 30

Retire at age 65

Money already saved $10,000

How much more must the individual save if they were age 40 with the same data?

4. Go to the Pension Welfare Benefits Association website at

http://www.dol.gov/ebsa/. Answer the following questions:

a) What types of fees are assessed on a 401(k) plan? How do they impact an investor’s

return?

b) What is different about retirement savings requirements for new job entrants,

mid-career and near retirement individuals?

5. At the PWBA website learn about vesting requirements. What are the graded vesting

schedule and the Cliff vesting schedule?

18–5